RBI’s financial stability report- understanding financial health

India’s financial system, which we often overlook in our frequent discussions because of the depressing state of the economy, is one such attention-worthy parameter that has the potential to make or break the country’s future prospects. It is said that India never recovered from the 2008 financial crisis of the world because the twin balance sheet problem we’re dealing with in terms of the banks and non-banking financial institutions has now turned into a four-balance sheet one owing to the lack of appropriate measures by the governments and economic action.

The pandemic has only further aggravated the deteriorating state of the market, due to a number of factors, which we’ll read as we go through the Reserve Bank of India’s financial stability report in detail.

The primary purpose of this twice in a year issued report is to assess and ultimately, express the health of the financial system of the country. While we are aware of measures to figure the economy’s health through some impact factors like consumption, inflation, labor market and indices based on it, assessment of the financial health of the system is a little different.

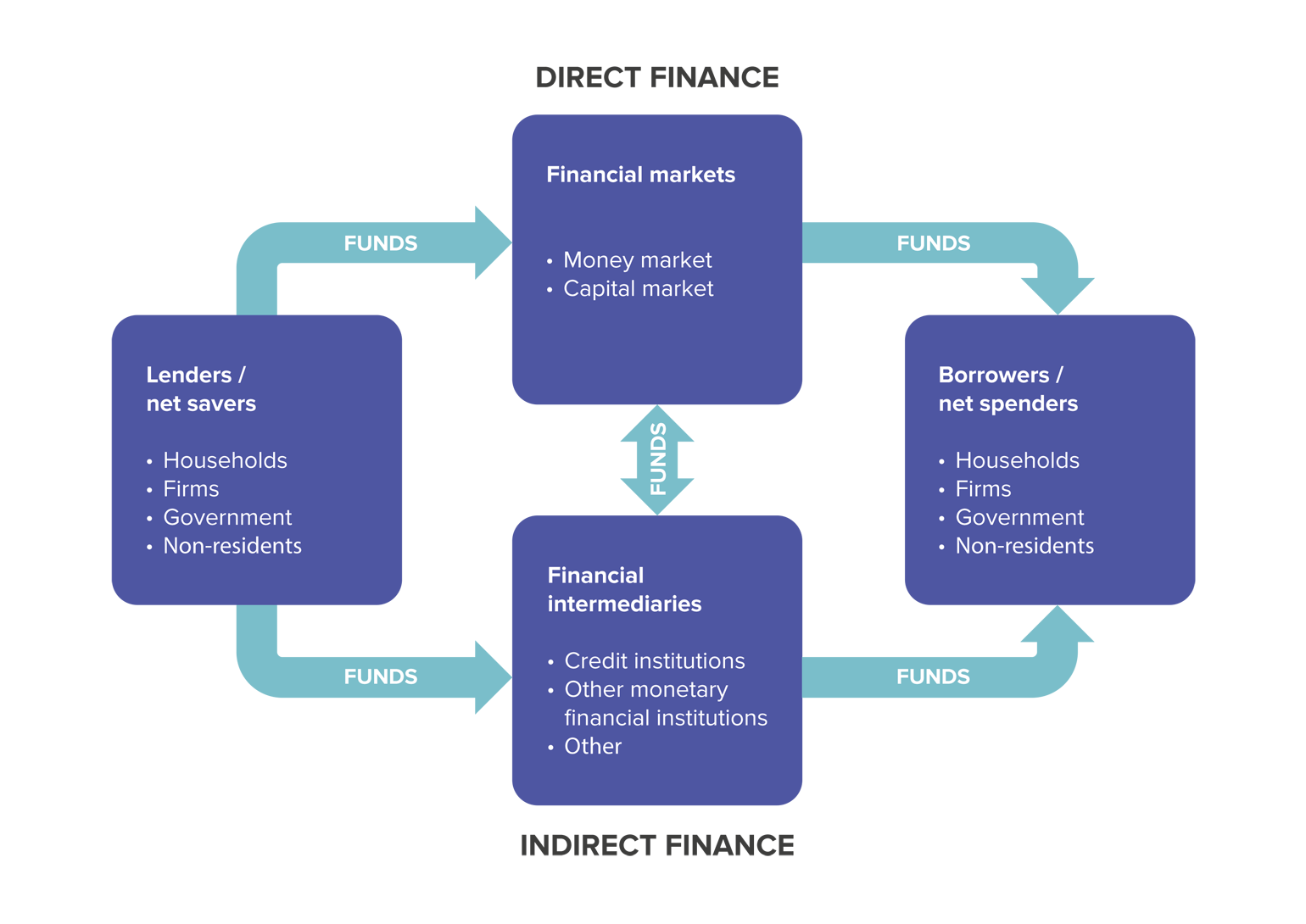

To understand how we measure a country’s financial health, let us first pose a few questions, the answers to which eventually draw up our path to know the financial system’s health. However, not that a financial system consists of banks, NBFCs, households, companies, insurance brokers and other related ones, interlinked by an inter-dependent system of borrowing, investing and lending.

The primary health parameter for banks is liquidity checking, meaning a check on if they have enough resources and capital to effectively run their operations, both in the case of the public and private sector banks. Other than that, are all the sectors and households in credible need of credit for economic activity able to do so? Say, for example, a corporation seeking credit for expansion, a small business owner seeking credit for initiation, or a household looking to buy a house.

Another primary health parameter, that goes hand in hand with the former, is if the bad loans or the non-performing assets within sustainable limits. Especially after the country’s twin balance sheet problem, this parameter has become a rather important health check. In an attempt to locate answers to these questions, the central bank undertakes a hefty research and survey approach and collects rather bulky data and information, aiding the central bank to answer the questions posed above and assess the state of the country’s financial system.

It also allows the Central Bank to put together links required to attain information, and draw up analysis on related sections of the economy, say, the state of the domestic economy, or macro-financial risks associated with the financial system. The world has had enough lessons in the past to draw up links as to why calculation of the aforementioned factor is important. However, to give you an overview of what I’m referring to, trace back to the financial crisis of 2008 that began as a bad debt series for banks in the United States and led to distortion in the global economy with growth contraction, and slumped economic indicators.

This example is to indicate how the problem in one part of the long-chained financial system has an impact on the other parts, which in turn, causes disruption for the economy at a larger scale.

To be bluntly honest, the health of India’s financial system has been critical for quite some time now. I’ve been referencing the twin-balance sheet problem time and again to fixate on the idea that a primary problem in the country’s financial institutions hasn’t been solved as yet, given the long due set of action plans for it. This is reflected in a large number of non-performing assets in the country.

Well, as can be unsurprisingly estimated, the COVID-19 pandemic made it simply worse. This is why RBI undertakes Systemic Risk Surveys, which are basically just stress tests to analyze what would happen to the health of the financial system if the economy at a larger scale worsens, or any global factors affecting India, say a rise in global prices of crude oil, would affect the system’s working.

Back in 2020, when the financial Stability Report was released, the Central Bank was worried about an increase in the proportion of non-performing assets because of the high overall stress level in the economy. This rooted in the higher probability of loans turning bad thanks to the weak economic position and loss of household and corporate income. To provide numbers to the notion, the Financial Stability report released back in 2020 assessed that non-performing assets could increase from 8.5 percent of gross advances and loans to a disturbing high of 14.7 percent by the end of March 2021.

Well, to our benign surprise, the estimated number of 14.7 percent was, in fact, limited to 7.5 percent in bad loans. The restriction to these numbers is an effect of the credit policies induced by the Reserve Bank during the stress period, like loan moratoriums, cheaper credits and loan restructuring, which have proven to be successful to contain the loans turning bad even in the high-stress periods. Loan moratoriums especially have stood out during the period for they have been a significant relief during the time.

However, one key thing to note here is that while these policies proved to be an aid on the borrowers’ end, the lenders, however, had a hard time going by it especially because their primary conditions wasn’t so strong to begin with.

This means that even though loan moratoriums are given this time around, their duration, however, cannot be as long because the banking institutions and financial corporations aren’t in a very strong position to support it, as mentioned by the Central Bank itself. In the financial stability report of 2021, the central bank has revealed that macro-stress tests for credit risk show that the GNPA ratio of Scheduled Commercial Banks may increase from 7.48 per cent in March 2021 to 9.80 per cent by March 2022 under the baseline scenario and to 11.22 per cent under a severe stress scenario.

This point more explicitly to the condition of medium and small enterprises, which may deteriorate as the virus continues to wreak havoc on the economy, despite a number of policies adopted by the central bank for MSME relief.

Further, as and when the situation gets over and the central bank takes back its relief policies like cheap loans and loan moratoriums, the true impact on non-performing assets would then be felt because there is a rather soft cushion for them to fall on.

The FSR explains the quandary: “Historical experience shows that credit losses remain elevated for several years after recessions end. Indeed, in EMEs [Emerging Market Economies], non-performing assets typically peak six to eight quarters after the onset of a severe recession. Eventually, support measures will be phased out. The longer that blanket support is continued, the higher the risk that it props up persistently unprofitable firms (‘zombies’), with adverse consequences for future economic growth.”

However, if the relief measures are phased out before the ideal time that is before the businesses’ cash flows recover, tightening of lending standards by the bank could hinder growth and recovery prospects. The situation is rather difficult right now and a proper solution and analysis could be offered once the virus fully exploits its way in the country.