Bank of Baroda, established in 1908, stands as a distinguished name in the realm of banking and finance. With a rich history spanning over a century, Bank of Baroda has evolved into one of India’s leading public sector banks, offering a comprehensive range of financial services and solutions to its customers.

Founded on July 20, 1908, by Maharaja Sir Sayajirao Gaekwad III, the ruler of Baroda (now Vadodara) in Gujarat, Bank of Baroda was originally known as “The Bank of Baroda Limited.” The bank’s inception was driven by a vision to support local businesses, encourage economic development, and foster entrepreneurship in the region. Over time, the bank expanded its footprint, embracing technological advancements and adapting to the changing financial landscape.

Bank of Baroda‘s initial years were not without their challenges. Limited financial resources, a lack of infrastructure, and the need to build trust within the community posed significant hurdles. However, with perseverance and determination, the bank overcame these obstacles and laid a strong foundation for its future growth. Today, it continues to thrive under public sector ownership, with the Government of India holding a majority stake. While the initial founders are no longer directly involved, their vision and legacy remain ingrained in the bank’s ethos. Bank of Baroda operates under its original name, reflecting its commitment to preserving its identity and heritage.

The bank’s product and service portfolio has evolved and expanded to cater to the diverse needs of its customers. The bank offers retail banking services, corporate banking solutions, treasury operations, wealth management services, and specialized financial products. These offerings encompass a wide range of services, including savings and current accounts, loans, credit cards, insurance products, mutual funds, and customized financial solutions for businesses.

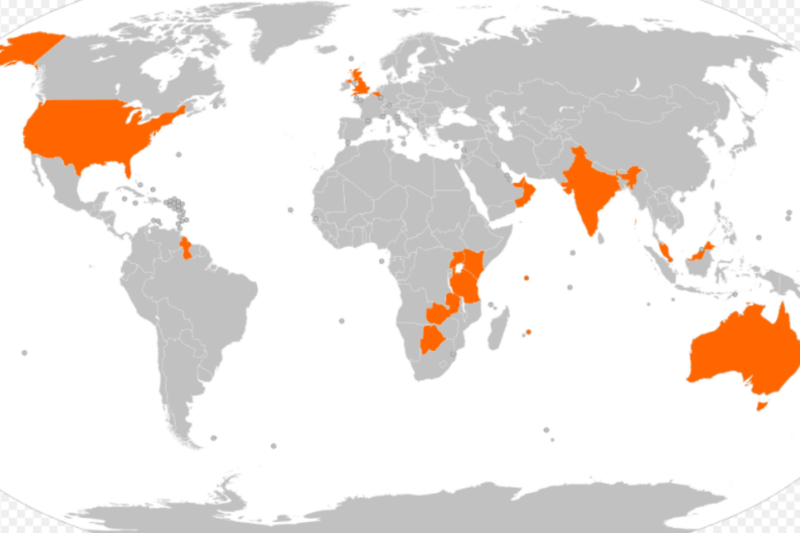

It has also made significant strides in its international expansion efforts. The bank has established a global presence, with branches and subsidiaries in various countries and cities worldwide. The bank operates a network of 107 branches and offices in 24 countries, excluding India. This includes 61 branches and offices of the Bank of Baroda itself, 38 branches of its eight subsidiaries, and one representative office in Thailand. Additionally, the bank has a joint venture in Zambia, which operates with 16 branches. This expansion has not only reinforced the bank’s global presence but has also facilitated its ability to serve a diverse clientele.

As a reputable financial institution, the bank closely monitors key performance indicators (KPIs) to assess its operational efficiency and financial health. Metrics such as net interest margin, cost-to-income ratio, return on assets, and capital adequacy ratio provide insights into the bank’s performance and help identify areas for improvement.

Bank of Baroda has upheld its commitment to corporate social responsibility (CSR) by actively participating in initiatives that contribute to the betterment of society. The bank has supported education, healthcare, women empowerment, rural development, and environmental conservation through its CSR programs, further solidifying its reputation as a responsible corporate entity.

-

Founding and Founders

Maharaja Sir Sayajirao Gaekwad III, Ruler of Baroda

Bank of Baroda, a prominent financial institution, was founded on July 20, 1908. Its establishment can be attributed to the visionary leadership of Maharaja Sir Sayajirao Gaekwad III, the ruler of Baroda (now Vadodara) in Gujarat, India. Alongside Maharaja Gaekwad, a group of astute entrepreneurs and professionals came together to lay the foundation of this prestigious institution.

Driven by a noble motive, the founders of the bank sought to address the banking needs of the local businesses and contribute to the region’s economic development. Recognizing the importance of a reliable financial institution, they aimed to foster entrepreneurship, facilitate trade and commerce, and enhance overall prosperity.

Under the guidance of Maharaja Gaekwad and the collective wisdom of the founders, the bank embarked on a journey to provide a comprehensive range of banking services. Their vision and commitment to serving the community set the stage for the institution’s growth and success in the years to come.

2. Initial Name, Products, and Objective

Bank of Baroda, initially known as “The Bank of Baroda Limited,” commenced its operations with a clear objective and a range of essential products and services. The institution was founded on July 20, 1908, by Maharaja Sir Sayajirao Gaekwad III, the ruler of Baroda (Vadodara) in Gujarat, India.

The bank’s initial name, “The Bank of Baroda Limited,” has remained unchanged throughout its history. From its inception, the Bank of Baroda aimed to serve as a catalyst for economic development and prosperity. Its founders envisioned a bank supporting local businesses and financially stimulating trade and commerce.

In line with its objective, the Bank of Baroda offered a range of traditional banking services right from the start. These included deposit facilities for individuals and businesses, loan products to support entrepreneurship, and remittance services for efficient fund transfers. The Bank of Baroda aimed to foster economic growth, empower local businesses, and contribute to the nation’s overall progress by providing these essential financial services.

3. Initial Hindrances and Challenges

During its early years, the Bank of Baroda encountered several hindrances and challenges that tested its resilience and determination. The initial hindrances were multifaceted and posed significant obstacles to the bank’s growth and success.

Limited financial resources were one of the primary challenges faced by the Bank of Baroda. Starting with modest capital, the bank had to strategically allocate its resources to establish a robust infrastructure and support its operations. This constraint required careful financial management and a focus on generating sustainable growth.

Building trust within the community was another hurdle for the Bank of Baroda. As a new entrant in the banking sector, the institution had to prove its reliability and credibility to attract customers. Overcoming the skepticism and gaining the trust of individuals and businesses required consistent delivery of quality services, transparent practices, and ethical conduct.

Infrastructure development was yet another challenge for the bank. Establishing a network of branches and expanding its operations necessitated significant investment in physical infrastructure, technology, and skilled personnel. Creating a strong foundation to support its growth ambitions demanded meticulous planning and execution.

Furthermore, the competitive landscape posed challenges to the Bank of Baroda. Competing with established players in the banking industry required the bank to differentiate itself through innovative products, personalized services, and superior customer experience.

4. Current Ownership and Name

The current ownership of the Bank of Baroda rests with the Government of India, which holds a significant stake of 63.97% in the bank. As a public sector bank, the Bank of Baroda operates under the guidance and oversight of the government. This ownership structure ensures the bank functions in the country’s economy’s best interest and serves the public’s needs.

Regarding leadership, the Central Government has appointed Shri Debadatta Chand as the Managing Director and Chief Executive Officer (MD & CEO) of the Bank of Baroda. With his extensive experience and expertise in the banking sector, Shri Debadatta Chand is responsible for leading the bank’s strategic direction and day-to-day operations.

Additionally, the Bank of Baroda has Dr Hasmukh Adhia serving as the Non-Executive Chairman. Dr. Adhia brings a wealth of knowledge and a distinguished career in public service, having previously held important positions within the Government of India.

5. Current Products and Services

Bank of Baroda offers a comprehensive range of products and services to cater to the diverse needs of its customers. Whether it’s retail banking, corporate services, global solutions, or personal finance, the bank strives to provide efficient and customer-centric offerings. Here is an overview of the various products and services provided by the Bank of Baroda:

- Retail Banking: Bank of Baroda offers various retail banking services, including savings accounts, current accounts, fixed deposits, recurring deposits, and personalized deposit schemes. It also provides consumer loans, home loans, vehicle loans, education loans, and loans against property.

- Rural/Agri Banking: Bank of Baroda is committed to serving the rural and agricultural sectors. It provides specialized banking solutions such as agricultural loans, Kisan credit cards, agri-business loans, and various products tailored to meet the unique requirements of farmers and rural communities.

- Wholesale Banking: Bank of Baroda offers comprehensive wholesale banking services, including working capital finance, term loans, trade finance, cash management services, and treasury solutions for large corporates, mid-sized enterprises, and government organizations.

- SME Banking: Bank of Baroda provides a dedicated suite of products and services for small and medium-sized enterprises (SMEs). This includes working capital finance, machinery loans, trade finance, export-import financing, and various customized solutions to support the growth and development of SMEs.

- Wealth Management: Bank of Baroda offers wealth management services, including portfolio management, mutual funds, insurance products, and financial planning services to help individuals and families grow and protect their wealth.

- Demat: Bank of Baroda facilitates the dematerialization of securities through its demat services. It enables customers to hold their securities electronically, providing convenience and safety.

- Internet Banking: Bank of Baroda’s internet banking platform, bob World Internet (Net Banking) India, and Baroda Connect (Net Banking) International, allow customers to access their accounts, make online transactions, pay bills, transfer funds, and avail various banking services conveniently from anywhere.

- NRI Services: Bank of Baroda offers a wide range of services for non-resident Indians (NRIs), including NRI accounts, remittances, foreign currency credits, correspondent banking, and investment opportunities in India.

- Credit Cards & Debit Cards: Bank of Baroda provides credit cards and debit cards with various features and benefits to cater to the diverse needs of customers.

- International Services: Bank of Baroda offers a range of international services, including foreign currency credits, external commercial borrowings, offshore banking, finance for export and import, correspondent banking, and global treasury services.

These are just a few highlights of the extensive range of products and services the Bank of Baroda offers. The bank continuously innovates and updates its offerings to meet the evolving needs of its customers and maintain its position as a leading financial institution.

6. International Expansion of Bank of Baroda

Bank of Baroda’s international expansion has been integral to its growth strategy. The bank operates a network of 107 branches and offices in 24 countries, excluding India. This includes 61 branches and offices of the Bank of Baroda itself, 38 branches of its eight subsidiaries, and one representative office in Thailand. Additionally, the bank has a joint venture in Zambia, which operates with 16 branches.

Bank of Baroda has strategically established its presence in major global financial centers such as New York, London, Dubai, Hong Kong, Brussels, and Singapore. These branches enable the bank to serve a diverse clientele and facilitate international trade and financial transactions.

The bank’s subsidiaries are crucial in expanding its retail banking operations. Through its subsidiary branches, the Bank of Baroda offers retail banking services in countries like Botswana, Guyana, Kenya, Tanzania, and Uganda. The bank has also demonstrated its commitment to growth by upgrading its representative office in Australia to a full-fledged branch. Furthermore, it has embarked on a joint venture to establish a commercial bank in Malaysia, strengthening its presence in the Southeast Asian market.

Mauritius, in particular, holds significance for the Bank of Baroda, as the bank has a substantial presence in the country. With approximately nine branches spread across Mauritius, the Bank of Baroda caters to the financial needs of both individual and corporate customers.

Through its extensive international network, the Bank of Baroda showcases its commitment to providing global banking solutions and serving customers across borders.

7. Key Performance Indicators (KPIs)

Key Performance Indicators (KPIs) play a crucial role in assessing the operational efficiency and financial performance of Bank of Baroda. Here are five key KPIs that the bank focuses on:

- Net Interest Margin (NIM): Net Interest Margin is a fundamental KPI that measures the profitability of a bank’s core lending and deposit-taking activities. Bank of Baroda closely monitors its NIM to maintain a healthy spread between the interest earned on loans and the interest paid on deposits.

- Cost-to-Income Ratio (CIR): The Cost-to-Income Ratio indicates the efficiency of a bank’s operations by measuring the proportion of operating expenses to its total income. Bank of Baroda aims to keep its CIR low, indicating effective cost management and optimized utilization of resources.

- Return on Assets (ROA): ROA is a critical KPI measuring the profitability of the bank’s total assets. Bank of Baroda strives to maintain a high ROA, demonstrating its ability to generate earnings from the assets deployed.

- Non-Performing Assets (NPAs): NPAs are loans borrowers have not repaid and are at risk of default. Bank of Baroda closely monitors its NPA ratio to measure asset quality and credit risk. The bank aims to keep its NPA ratio low, indicating prudent lending practices and effective risk management.

- Capital Adequacy Ratio (CAR): CAR measures the bank’s capital adequacy and ability to absorb potential losses. Bank of Baroda ensures it maintains a healthy CAR, complying with regulatory requirements and safeguarding against unforeseen risks.

8. Legal Matters

Bank of Baroda has encountered legal matters that have attracted attention in recent years. In 2021, the bank faced a significant fraud case involving approximately Rs 6,000 crore. According to news reports, the Central Bureau of Investigation (CBI) filed supplementary chargesheets in relation to the scam, which allegedly involved the creation of fake accounts and fraudulent transactions. The case led to the arrest of several individuals connected to the fraud.

In another incident in 2017, the Bank of Baroda was embroiled in a forex scam, resulting in the arrest of two businessmen by the Enforcement Directorate (ED). The fraud involved illegal remittances and irregularities in foreign exchange transactions.

Bank of Baroda has also faced challenges in 2018 related to its operations in South Africa. According to an investigation, the bank’s involvement in the country’s political crisis was linked to a series of mistakes, including improper handling of funds and transactions.

Additionally, the Bank of Baroda faced legal action in 2021 when Dubai-based businessman BR Shetty and an international accounting firm sued the bank over alleged irregularities and misconduct. The lawsuit highlighted the complexities and legal disputes surrounding the bank’s operations.

9. Financial Performance

Bank of Baroda has consistently demonstrated strong financial performance, reflecting its robust position in the banking industry. Here are some key financial metrics that showcase the bank’s recent achievements:

Market Capitalization: Bank of Baroda’s market capitalization stood at INR 973.25 billion, reflecting the market’s confidence in the bank’s growth potential and financial stability.

Revenue: As of March 31 2023, Bank of Baroda achieved a total business of INR 21,73,236 crore, representing a remarkable growth of 16.6% year-on-year (YoY). This growth signifies the bank’s ability to attract and serve a diverse range of customers across its various banking segments.

Net Profit: Bank of Baroda is expected to report a standalone net profit of INR 4,070 crore for the quarter ended March 2023. This positive net profit indicates the bank effectively manages its income and expenses, resulting in a healthy bottom line.

These financial figures underscore Bank of Baroda’s commitment to sustainable growth and profitability. By leveraging its extensive branch network, innovative product offerings, and prudent risk management practices, the bank has successfully captured opportunities and delivered value to its shareholders.

10. Corporate Social Responsibility

Bank of Baroda has upheld a strong commitment to corporate social responsibility (CSR) initiatives, contributing to the social and economic well-being of the communities it serves. The bank has actively supported education, healthcare, women empowerment, rural development, and environmental conservation through various CSR programs.

Conclusion

Bank of Baroda’s journey from its humble beginnings to becoming a leading financial institution reflects the spirit of entrepreneurship, innovation, and resilience. With a focus on customer-centric solutions and a global presence, the Bank of Baroda plays a vital role in shaping India’s banking landscape and contributing to the country’s economic growth. As the financial industry evolves, Bank of Baroda remains steadfast in its commitment to excellence, serving as a trusted partner for individuals and businesses alike.