UPI: The Biggest Innovation Of The Last Decade That Became The Backbone Of Indian Digital Payments.

UPI transactions have increased in recent years as a result of the introduction of multiple such interfaces, and individuals are increasingly using them to make all kinds of payments, from tiny retailers to large institutions.

After the historic success of Chandrayan 3 and the onset of the year’s grandest event, the G20 summit, it seems that India is nowhere to stop in climbing the ladder of success. For the first time in August, the instant payment system UPI (Unified Payments Interface) surpassed the historical threshold of 10 billion transactions. According to a PwC India analysis, Unified Payments Interface has become India’s biggest digital payments network, with the number of transactions rising by 59% year on year and a predicted milestone of 1 billion daily transactions by 2026-27.

According to current IMF statistics, improved access to credit feeds increased spending, which is a significant driver of India’s expected 6.1% GDP growth. As India strives for greater economic success, the expansion of the middle class from 31% to 61% of the population in 2046-47 becomes critical. Growing middle-class growth and increased consumer expenditure are closely related to increased credit availability, paving the road for economic development.

Unified Payments Interface transactions have increased in recent years as a result of the introduction of multiple such interfaces, and individuals are increasingly using them to make all kinds of payments, from tiny retailers to large institutions. Only a week after Unified Payments Interface transactions in India reached an all-time high of 10 billion in August, the NPCI is now seeking to increase UPI transactions from 10 billion to 100 billion per month.

National Payments Corporation of India, aka NPCI, which manages the Unified Payments Interface network, has announced four new products in this regard. New features released include the following.

A credit limit on UPI.

The payment platform will allow consumers to pay for transactions via credit by connecting pre-sanctioned digital credit lines from banking institutions. Further, the payment channel will be the exact same as existing transactions for the new feature.

As per NPCI, through ‘credit line on UPI,’ the approach of availing, connecting, and utilising credit lines will be greatly expedited. This is also predicted to give a leg-up to banks and financial establishments to directly give credit to a wider base of users than depend on credit apps for distribution. Third-party payment platforms Paytm, Google Pay and HDFC PayZapp will be among the first to launch this facility. This has the potential to make credit available in real time, and the team is working on a service layer to empower customers to control and use credit.

UPI Lite X for offline payments.

This will allow users to both send and receive funds while being fully offline, unlocking the use-case to even flights, underground metros and other merchant locations. Last year, NPCI gave us UPI Lite, which allowed consumers to make small-ticket payments without entering the transaction PIN. This new service is an extension of the Lite version.

UPI Tap and Pay.

It allows users to make near-field communication (NFC)-based transactions.

Conversational Payments – Hello! UPI & BillPay Connect.

NPCI announced Hello! UPI, which will allow users to conduct voice-enabled UPI payments in Hindi and English via UPI Apps, telecom calls, and IoT (Internet of Things) devices. It intends to launch the service in more regional languages.

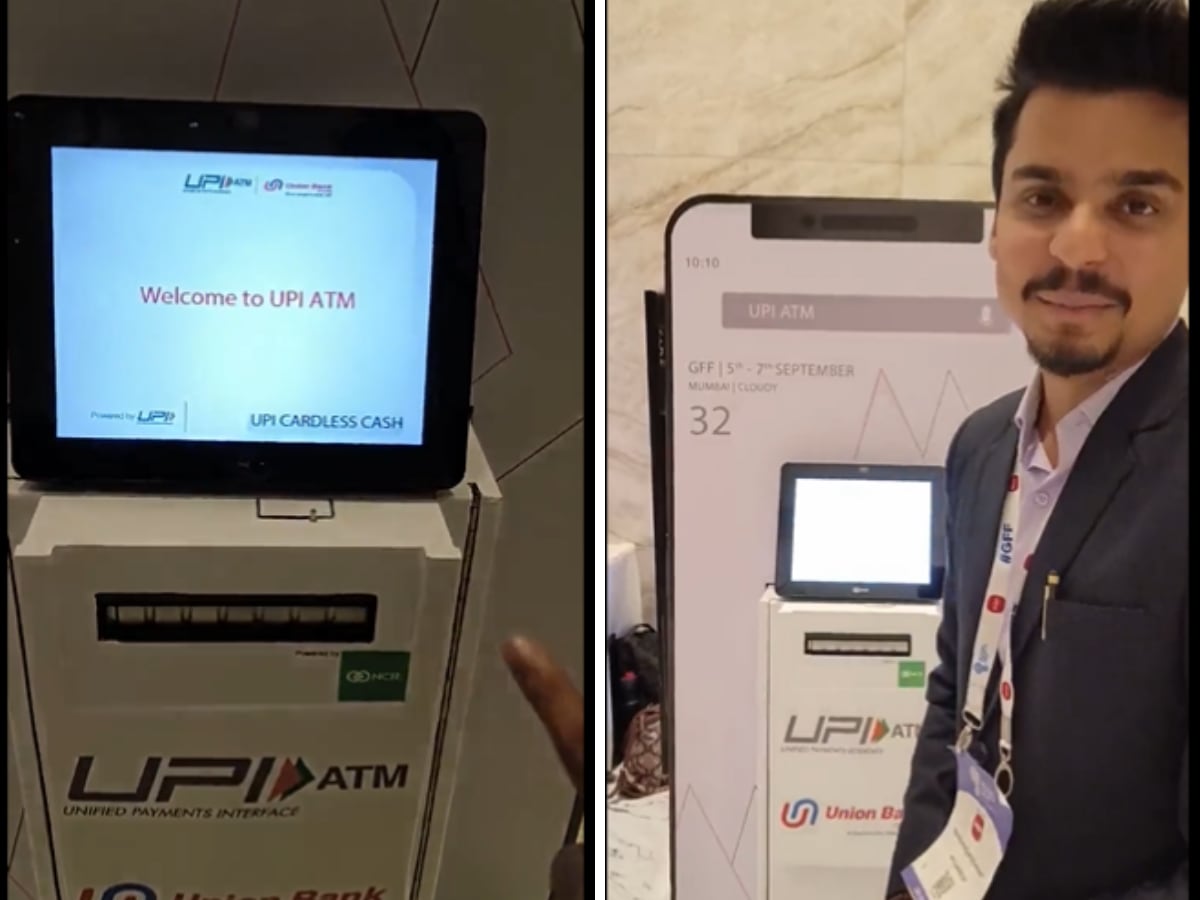

UPI ATM.

And if you think the list is over, wait. UPI has another surprise for you. It’s great when in sudden need of cash and having nothing in hand except the mobile. And for the same marks, the entry of UPI ATM. Yes, you read that right. This recent development as a UPI ATM will enable you to withdraw cash by scanning the QR code in the UPI ATM setup, eliminating the need for physical cards.

Conclusion.

As it supplies its payment stack, NPCI is projected to have payment infrastructure in 50% of the top 30 markets for cross-border transactions. Unified Payments Interface is now operational in Bhutan, Sri Lanka, France, and Singapore. The NPCI is aggressively involved in creating the required infrastructure to facilitate cross-border transactions, giving significant potential for Indian fintech businesses pursuing worldwide development.