The three medications that will be success in reviving India’s ETF market in 2022: Promotion, Affordability, and Liquidity

In many states, people have been talking sourly about lemon prices for the past month. (ETF) Experts say that the prices went up because of bad weather and a sudden heatwave that hit the whole country. But, once again, it came down to a difference between supply and demand.

This imbalance controls prices and markets for both things you can touch and things you can’t. Because of this imbalance, India’s exchange-traded funds (ETFs) are in bad shape. Because of this, there isn’t enough money in India’s ETF industry.

ETFs are growing in India, but it has taken them a while. The 100th exchange-traded funds was listed on NSE in July 2021, and it took 19 years to get to 100. In 2020 and 2021, 21 Exchange-traded funds were put on the stock market. But there have been worries about liquidity. For example, the Motilal Oswal Nasdaq 100 exchange-traded funds has assets worth INR6,130 crore and is currently trading at INR104.50, 9 percent more than its net asset value (NAV). Similarly, the market price of the Hang Seng BeES, which is managed by Nippon Life India AMC and has assets worth INR88 crore, is INR305, which is 18% more than its NAV.

As was said above, this difference between NAV and market price is caused by demand and supply differences.

But why even think about ETFs? ETFs are easy to invest in, and investors have more access to their money than they do with mutual funds (consider lock-in periods).

At the moment, exchange-traded funds that track international indices can only invest up to USD1 billion in foreign stocks, and they can’t buy more units by getting more money. But because they still trade on both NSE and BSE, their prices aren’t the same as their NAVs.

Even though there is a problem with how international exchange-traded funds are regulated on Indian exchanges, the prices of Indian ETFs have always been messed up.

This problem is getting worse because investors want exchange-traded funds based on indices whose underlying assets are not liquid.

How can we get out of this?

Unwrapping exchange-traded funds

There are now a lot of exchange-traded funds based on indices that measure things like quality, alpha, value, or size (midcap ETFs), but the underlying asset isn’t liquid, so prices are being messed up.

Even though there is no easy answer, most investors should follow a market-cap index like the Nifty 50 and exchange-traded funds based on it, like the SBI Nifty 50 exchange-traded funds or the Nippon Nifty BeES.

But even when the drawdowns were the worst, these exchange-traded funds didn’t live up to investors’ hopes.

So, what’s wrong with Indian exchange-traded funds?

“In India, the structure of the exchange-traded funds market itself is a problem,” says Anish Teli, managing partner of QED Capital PMS. Exchange-traded funds can only be sold as passive investments. In the US, exchange-traded funds are less taxed than mutual funds, and Cathie Wood has a basket of exchange-traded funds based on themes like innovation and genomics that are actively managed. So, traders from different time frames trade the underlying stocks and exchange-traded funds every day, and liquidity is usually not an issue.

NSE says that in the last five years, the AUM of passive funds has gone from INR52,368 crore on March 31, 2017, to INR499,319 crore on March 31, 2022. (annualized growth rate of approximately 57 percent ).

Experts in the field say that 92 percent of EPFO’s funds are passive, while individual investors hold only 2 percent.

“The lack of liquidity in exchange-traded funds today is primarily because most retail investors don’t know what exchange-traded funds are. Also, Pratik Oswal, head of passive funds at Motilal Oswal Asset Management, said that most large buyers of ETFs (pension funds, family offices, etc.) tend to skip the exchange and go straight to the AMC to buy ETF units.

In India, cash flow is significant.

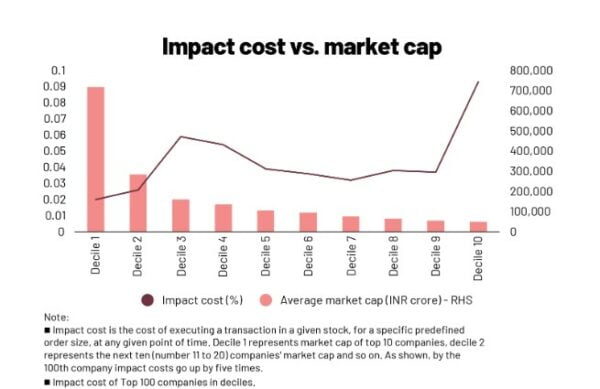

If you take out the top 100 stocks, you can see that liquidity, measured by impact costs, starts to go down. This is a problem with how the Indian markets are built since they are not very deep.

When investors have few options, they want to buy as many products as they can from the listed exchanges. This causes a premium over the NAV, which means the investor loses money because he buys a product with low costs of 0.25 percent to 0.50 percent but ends up paying more.

“With index funds, you buy and sell with the mutual fund company at NAV. With exchange-traded funds, you buy and sell at the exchange, where the last-traded price of the exchange-traded funds can be very different from its published NAV. Ravi Saraogi, the co-founder of Samasthiti Advisors, says, “This means that the total cost of ownership of an ETF can be much higher than that of an index fund.”

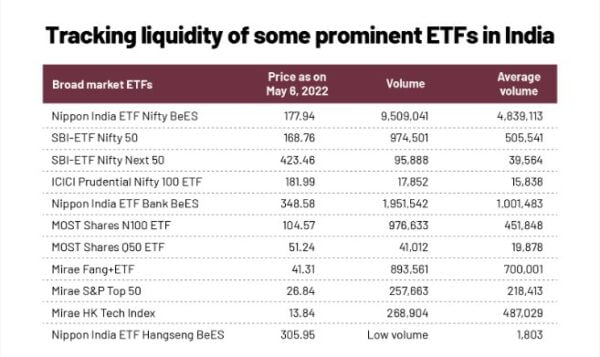

He thinks that even for well-known exchange-traded funds like the Nifty BeES exchange-traded funds, there are times when the exchange price isn’t the same as the NAV. Even Nifty BeES, which usually has a daily turnover of more than INR20 crore, works the same way.

SBI-exchange-traded funds Nifty 50 is less well-known than Nifty BeES, the oldest exchange-traded funds; it came out in 2001, and brokers and investors find it useful. Even though SBI-exchange-traded funds Nifty 50 is worth INR128,960 crore, this is the case.

Before small investors can feel confident about investing in other, smaller, and more recent exchange-traded funds with low trading volumes, AMCs will need to provide market-making support.

Get the word out

Industry players say that liquidity will only get better if brokers are promoted because brokers are the ones who will bring liquidity to the markets in the end.

Also, a Sebi rule must let smaller investors come directly to the exchange instead of buying a basket. There must also be rules about how to give market-makers an incentive.

Sometimes the lack of cash is made up.

For example, Kotak Mutual Fund’s Kotak Nifty Alpha 50 exchange-traded funds, released in December 2021 and based on the Nifty Alpha 50, a diversified 50-stock index, holds mid-and small-cap stocks that are often hard to sell.

For example, its top holdings, Brightcom Group (10.46%) and Tata Teleservices (Maharashtra) or TTML (6.31%), have the highest impact costs among the top 500 stocks on the NSE. Both of these stocks have given very high returns in the past year, but they are hard to sell.

Because these stocks were not easily traded, the exchange-traded funds was not easily changed.

Sebi exchange-traded funds rules say that an exchange-traded funds should hold all the stocks in an index, but the Kotak Nifty Alpha 50 exchange-traded funds didn’t have these two stocks. The tracking error was almost 3% because the fund didn’t buy 16 percent of the index held by the exchange-traded funds. Market-makers won’t add liquidity to an exchange-traded funds that doesn’t have enough.

Due to liquidity problems, Edelweiss Mutual Fund had to turn Edelweiss Nifty 100 Quality 30 and Edelweiss Nifty 50 from ETFs into index funds in October 2021.

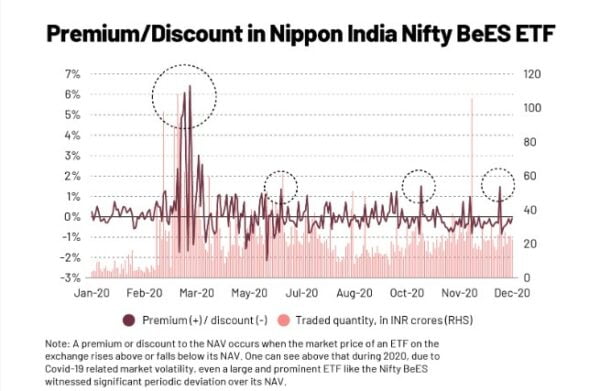

Even back in March 2020, when the market fell by 40% from its peak when liquidity was low, the SBI exchange-traded funds Nifty 50 lost a lot.

The price of SBI ETF Nifty 50 went up by 1.16 percent at the end of trading on March 16, 2020, while Nifty fell by 7.6 percent. The ETF did not follow the benchmark indices because market-makers had trouble getting enough cash to cover their positions in a volatile market.

Both fund houses and investors realized for the first time that ETFs are much more volatile and even risky than their index funds.

Even new fund houses that just started up to don’t want to launch ETFs because they think the lack of liquidity in the space will make their new investors lose trust in them right when they are starting up.

Outside view

John Bogle, the inventor of passive investing and founder of the Vanguard Group, has never liked ETFs, and he has always thought that index funds are a better choice.

Bogle thinks that traditional index funds are better than ETFs because they don’t make people try to time the market badly. In the past, volatile ETFs made it hard for passive investors in the US markets to make money.

In the first quarter of 2018, US ETF funds saw volatility like never before, with colossal ETF basket redemptions that threatened the market’s stability. It was thought that short-term speculators were buying and selling ETFs quickly, which made the index very volatile.

In the same year, Bogle said, “More and more speculators are using ETFs to get into the market. We have a trading mentality that shouldn’t affect long-term investors, but ETF investors have earned a 5% return in the last 12 years, while investing in traditional index funds has gained about 8%. The investor in a conventional index fund made 180% of their money, while the investor in an ETF made about 100%.

In ETF schemes, index baskets are made or sold based on what investors want, and the fund manager has almost no control over how much is put into or taken out of the fund. In other types of passive investments, like index funds, investor demand only makes the AUM corpus grow, and the fund manager chooses index stocks on their own based on their passive investment strategy.

So, the size of the fund, its volatility, and how much people want index stocks in baskets have nothing to do with the investor’s skill.

Currently, the domestic mutual fund industry has 110 ETFs in categories like equity, smart beta, international, debt, bond, gold, and silver.

US ETFs have a total AUM of USD4.9 trillion, and there are 1,643 of them that trade on US markets. Institutions like pension funds and hedge funds use ETFs to invest passively all over the world.

Investors have control over their stock exposures through the structure of ETFs, and the fund manager would decide how much exposure to stocks the fund would have in index funds. The other side of institutions owning ETFs is that demand-driven ETF volatility has often caused trouble in equity markets.

Because of this, there is a temporary shortage of index stocks that ETFs can buy, which puts pressure on exchange-listed ETF units to buy.

This makes the prices of listed units go up above the basket-price NAV, which creates a premium.

As the number of ETF trades goes down, there is more pressure on new investors to buy, which drives up the prices of ETF units until the AMC can step in and make short ETF baskets.

But the contradiction is that the AMC can’t make fast baskets of the index if the underlying stocks are like the Nifty Alpha 50 index. That pent-up demand moves to the stock market to buy ETF units, which creates more premium gaps.

“Because of the limits set by the RBI, Motilal Oswal AMC can’t add more liquidity or new units to its Nasdaq 100 ETF on the exchange. Due to the high demand for the Nasdaq ETF, prices on the exchange are trading at a premium,” says Oswal of Motilal Oswal AMC.

In conclusion

Overall, institutions that manage pension or insurance money have been more interested in ETFs. As a passive investment usually held for a long time, it fits well with the slow and steady approach of pension funds and insurance funds.

For retail interest in ETFs to grow, listed-units trading is a low-cost way for people to buy ETFs from the exchange. In India, Sebi needs at least two market-makers for each ETF listed on a business to create liquidity by giving buy and sell quotes in both directions. This is expected to help regular people buy ETFs and sell them when they want to.

Even though listing ETFs is suitable for retail investors from a business standpoint, there is a downside to exchange listing of ETFs when the listed price goes above or below the ETF’s NAV. At a premium, the person who buys an ETF gets less money back, and at a discount, the person who sells an ETF doesn’t get the most money.

If the volume on the exchange stays at a healthy level, ETFs for the domestic market will be a lot more efficient.

The Association of Mutual Funds in India’s (AMFI) “Mutual fund Sahi hai” campaign should focus on making low-cost investing in ETFs popular with the general public, starting with ultra HNIs and HNIs.

These wealthy investors will be able to buy or sell in large amounts on exchanges because they have a lot of money. This could lead to higher and more consistent trading volumes.