All you need to know about Credit and Credit cards ;Top 8 ways to increase your CIBIL score

All you need to know about Credit and Credit cards ;Top 8 ways to increase your CIBIL score

The reason many people believe credit should be available to everyone is because it creates a level playing field. A small business owner can obtain business credit along as they are deemed a worthy borrower who will pay back the loan. A big company can also borrow money and support a new, small business.

Why do we need credit? To answer this question, we need to understand why people buy cars, houses, and other items. In the India, we tend to buy these things to benefit our financial state and provide security for ourselves in the future.

If we want to buy a car, we need to make sure it will provide us with a good driving experience and make sure we can afford it once it is paid for. We need to purchase a house as we need somewhere to live, as well as a place for our family to live and grow. Credit’s usefulness is established in a variety of ways in addition to those described above.

CREDIT CARDS

Credit in the India has become very accessible and easy to obtain thanks to the introduction of the credit card. Some people use credit to help fund a business venture, as they often need to take out large amounts of money in one go to help with the initial costs. This is known as using credit to fund business and is often used as a short-term measure until the business has found its feet and is able to sustain itself.

Improper and irresponsible credit use can put you in serious financial difficulty and have a negative impact on your ability to obtain future credit. It is your responsibility to make sure that all your financial obligations are met.

If you miss a payment, you may end up in debt or foreclosure. The best way to prevent this is by maintaining a good credit score. To help you create a solid credit history, we recommend that:

1.you stay in good standing on all of your major credit accounts and that you close accounts that are in collections or have a past due balance.

2.Use credit cards responsibly and always pay off the entire amount due each month.

3.Maintain your balance on each credit card at the minimum amount each month.

4.Do not make more than the required minimum payment on any card.

5.Never carry a balance on your cards. If you do, you may end up in debt or in foreclosure.

6.Insure your home and car.

7.Get a copy of your credit report on a regular basis to monitor your credit situation.

There is a wide range of free resources that offer helpful advice on the Internet. If you are unable to pay off your debt, or if you are in danger of foreclosure or a collection action, contact the appropriate agencies and file for bankruptcy or wage garnishment as soon as possible.

CREDIT REPORT

A credit report is a report, given by credit agencies, of your financial history. The type of information contained in a credit report is determined by the credit agencies. The credit report is a record of information about your debt and credit accounts.

These agencies gather information from the companies to whom you have applied for credit, such as banks, credit card companies, stores and others. The information contained in your credit report is collected and sold to lenders, landlords and employers who are considering extending credit or for other purposes.

These reports are not guaranteed by the law, and there is no way to get copies of them. However, you have the right to get your credit report for free from the agencies on a regular basis.

WHAT IS CIBIL SCORE?

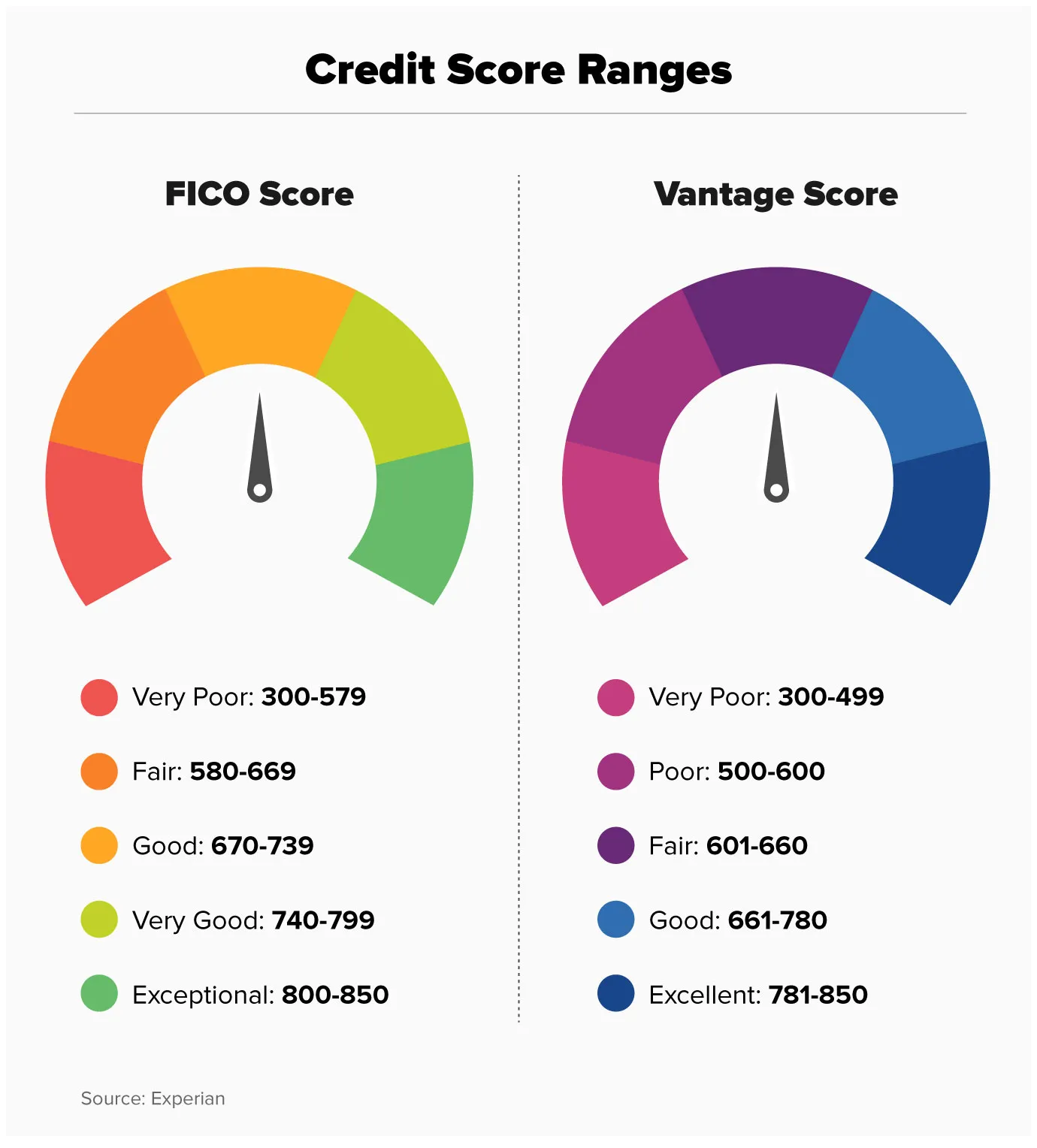

The CIBIL score is a three-digit numerical summary of a person’s credit history that reflects their credit profile. The credit score is a key metric that lenders use to assess a potential borrower’s creditworthiness. One of India’s four credit rating agencies is CIBIL.

A good CIBIL score is one that ranges from 700 to 900 points and demonstrates to the lender that you are creditworthy.

The CIBIL database is a database of past due payments, credit limits and overdue debts; the database is made up of information collected from the data centres of the participating credit information bureaus. These credit information bureaus include: CIBIL, Experian, Equifax, TransUnion, and TUJ.

As of February 2015, CIBIL’s main database (CIBIL Core database) had a subscriber base of more than 2.5 million customers, with individual credit bureau data including all the CIBIL data. Its other database (CIBIL-MIS) had more than 5 million customers.

The company uses technology for its data collection. All consumer credit-related activities, such as loan application and disbursal, account opening and account status queries, are automatically processed by their systems. CIBIL offers other services, such as checking the individual’s credit history.

CIBIL provides a free credit score to individuals with an inquiry, however, in India, only those with active credit accounts, for example, a credit card, have access to CIBIL scores.

History

CIBIL started its operations in India in February 2000. CIBIL was founded in 1995, based on “data-rich” credit rating. The company is now one of the largest credit rating companies in the world.

CIBIL’s provides information about an individual’s credit history to service providers and also for businesses, so that businesses can evaluate the credit risk of potential employees, customers, vendors, partners and other individuals and businesses.

In 2015, CIBIL’s database contained information on more than 30 million borrowers. The company processes more than 100,000 individual queries daily. It sells credit scores to banks, insurance companies, retailers and companies offering loans to individuals and institutions. The company is headquartered in Gurgaon, India and has offices in Singapore, United States and Australia.

HOW TO IMPROVE CIBIL SCORE

In the world of banks and NBFCs, your CIBIL score is the first thing they look at and the most important factor while lending. It doesn’t matter how much money you have or what type of a loan you apply for, your CIBIL score is what will eventually decide your fate. But as a responsible citizen and in pursuit of a good CIBIL score, you will naturally want to improve your CIBIL score. Anything below 700 should be worried about. While your credit score will not change overnight, major and minor changes in your financial habits can help in making a significant difference.

So what is the process you need to follow to improve your CIBIL score:

- The CIBIL report: In order to get a fresh CIBIL report, it is important that you should have kept your CIBIL account clean and current for at least six months. It should be current and clean in the sense that you have not taken a hit to your current account balance or the credit limit. You should not have taken any loan or used your CIBIL credit card. Also, the payment should not be pending.

- Monitor your CIBIL balance: If you are worried about how your CIBIL score is going down, you should first check your CIBIL balance. If your CIBIL balance is high and you haven’t taken a hit to it then try to spend less money. But if your CIBIL balance is low and you haven’t made any purchases with it, then you should not worry.

- Your loan repayments: Your next move is to start repaying your loan with your financial institution. The better you manage your repayment (in terms of frequency, amount and time) the better your score will be. So it is very important that you repay as per your lender’s condition.

- Check your credit cards: If you are using CIBIL to check your credit cards, it is important that you check your credit cards. If you find that they have been maxed out and you haven’t applied for any new credit cards, it’s a big red flag.

- Increase your credit limits: This is another important move that will help you improve your CIBIL score. If you have not requested for any increase in your credit limit, try to request for an increase. If the bank or NBFC doesn’t agree to it, try to approach other banks for an increase.

- Pay extra: If you don’t want to take a hit on your CIBIL balance, you can try to pay more than the minimum amount on your loan. While paying more than the minimum amount on your loan, don’t forget to set a reminder for yourself to make it to your bank’s site to check your loan status on a regular basis.

- If you are a good borrower, then we recommend you to try to pay the highest possible interest rate and the minimum monthly installments, and if you do this, then there is no limit to your score, and there is no point chasing your score as higher scores mean higher return on your loans, which can make your loans cheaper.

- Your score also increases if you have made a timely repayment, provided a positive appraisal to the bank and have a good customer service record.

Please note that the only way to get a higher score is to repay on time, pay the highest interest rates and the minimum monthly installments

How to check CIBIL score

-A Simple Step In short, you get your score in the following 10 ways

1) Make sure that the documents have been duly signed, scanned or sent to you. If you haven’t received these in the past couple of days, then please call to check if they have come in. A signature is not valid unless it is affixed at the time it was signed, that is, you must get the “SIGNED” receipt, and not one that you may have found by searching the system in the future. Also, remember to add any information about the courier if the documents have not been delivered to you by courier

2) Don’t forget to send you copy of the letter by post or courier if you want to get the credit report changed

3) In case you forget to mention or did not attach these in your loan application documents, they should not have any information on the last date of the loan. For example, you mention that your loan has to be completed by Dec 31st. Any documents after this date have no value and do not matter for calculation. If they have, then please take steps to attach these along with the loan application

4) In case you have no clue how to send it to you, then first, log on to your CIBIL account from your browser and there is a facility of forwarding any mail to you. Also, if you want to get your credit report on loan from any other bank, then it should be done with your loan reference number and you need to attach the copy of your application letter for that

5) If you attach the signature on loan application instead of courier receipt, then you may want to take back the papers and get a new signature affixed before getting your loan sanctioned.

6) At last, we will check the date on your courier receipt if you didn’t mention it with the application. Then we will take into account any documents that you have that are beyond the loan application date. There is no specific time limit for this, but if you have not gotten your receipt and don’t remember anything about the courier then it does not matter as long as it is in the past couple of days, you have not provided any other document.

7) After you have all the information available to you, you need to send the information to CIBIL online using the form.

8) Now your CIBIL score will be calculated. It can take up to 3 business days to get your score. You can follow the progress on the CIBIL website.

9) There is no limit to your score, but it is usually between 300- 600 as long as you have been a CIBIL customer for 3 years, have paid the installments regularly and haven’t defaulted on any loans. If you have defaulted on loans or have been late to pay the installments, your score can go down, as in all cases it is a negative score.

Edited and published by Ashlyn Joy