Following a widely shared LinkedIn post by renowned financial commentator, former Bain consultant, and ‘Redemption of a Son’ author Jayant Mundhra, Paytm and its founder Vijay Shekhar Sharma (VSS) are under serious questions in what could end up being one of the biggest corporate governance controversies in India’s startup ecosystem. According to Mr Mundhra’s disclosures, the recent storyline surrounding Ant Financial’s “departure” from Paytm, a Chinese investment, is not only inaccurate, but also dishonest.

It all started when Indian media recently celebrated a 100% Indian-owned Paytm, declaring that Alibaba affiliate Ant Group’s arm (Antfin) had finally sold its remaining stake. Indeed, in early August 2025 Reuters and other outlets like The Economic Times reported Antfin’s sale of a 5.84% stake (roughly ₹3,800 crore) in Paytm, giving headlines as ‘Zero-Chinese Ownership’. Headlines proclaimed an end to “all Chinese ownership” in Paytm. But deep-dive reports and regulatory filings tell a more troubling story: founder Vijay Shekhar Sharma (VSS) quietly parked 10.3% of Paytm shares in a Netherlands shell, allowing Antfin to keep an economic claim. In other words, the “exit” may be largely on paper.

Multiple sources confirm that in July 2023, Antfin’s 10.3% stake in Paytm was transferred not for cash but via a debt instrument to Sharma’s own Dutch company. This maneuver has gone largely unreported in India’s mainstream media. As one fintech expert told The Economic Times, the deal effectively lets Sharma “own a larger chunk” of Paytm while Antfin retains the economic value. Critics argue this setup kept Antfin’s interest alive behind the scenes, despite the headlines.

The Shadowy Timeline of Chinese Exit In Paytm: RAM BV and the 10.3% Transfer

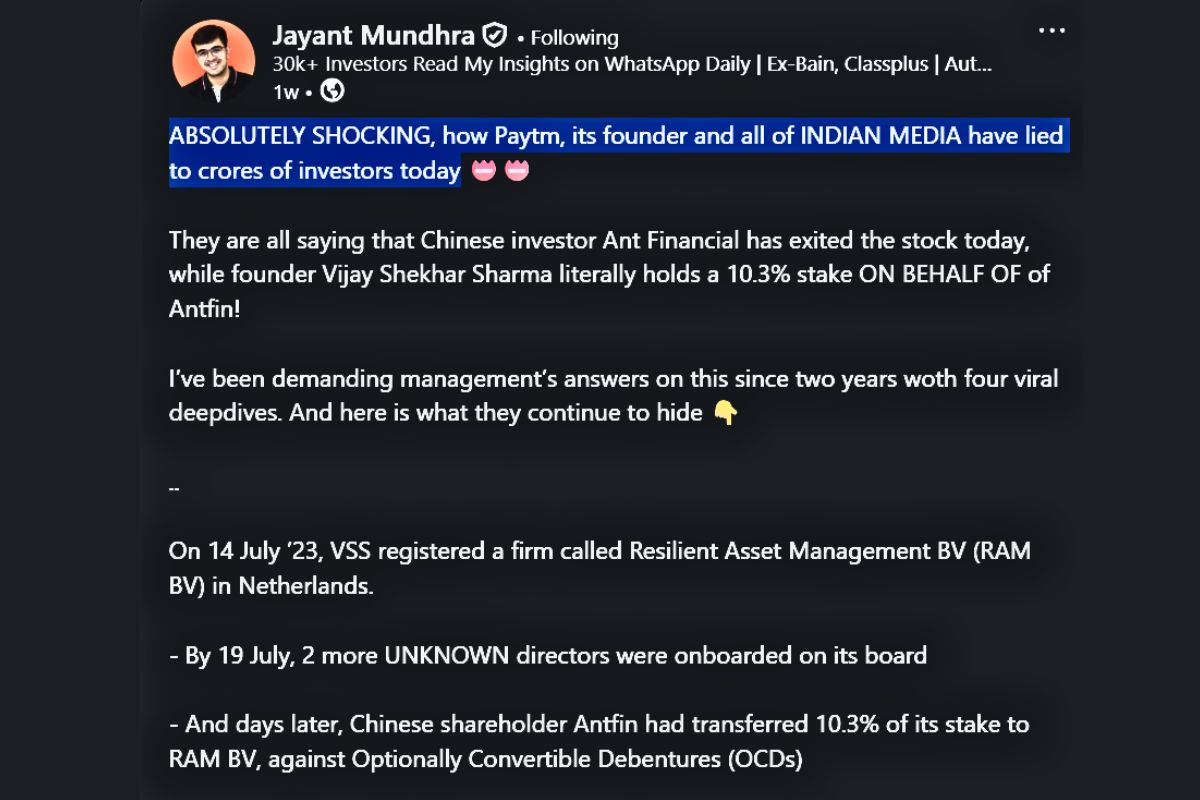

Corporate records and investigative posts shed light on what happened. Dutch registry data show Resilient Asset Management B.V. (RAM BV), a company controlled by VSS, was incorporated on July 13, 2023. Within days, “two unknown directors” joined its board. By late July, Antfin’s 10.3% Paytm stake (originally held via Antfin (Netherlands) Holding BV) was shifted into RAM BV. Crucially, it was exchanged not for cash but for optionally convertible debentures (OCDs) issued by RAM BV.

Key dates (from public filings and reports) are:

- July 14, 2023: VSS registers Resilient Asset Management BV in the Netherlands.

- July 19, 2023: Two additional directors (names not widely reported) are added to RAM BV’s board.

- Late July 2023: Antfin transfers 10.3% of Paytm’s equity into RAM BV in exchange for OCDs, according to a Paytm stock exchange filing.

Unlike a straightforward share sale, this structure left Antfin holding a convertible debt instrument rather than outright selling its equity. Paytm’s filings make the arrangement clear: “neither any cash payment had been made, nor any value assurance was provided by Sharma”, and instead “Resilient will issue OCDs to Antfin allowing Antfin to retain economic value of the 10.30% stake”.

/tice-news-prod/media/media_files/2025/08/05/what-is-behind-antfin-stake-deal-2025-08-05-19-10-03.png)

What Are OCDs? (Convertible Debentures Explained)

For lay readers, optionally convertible debentures (OCDs) are essentially a loan instrument that can be converted into equity later. Crucially, Antfin retains the right to convert that debt back into shares of RAM BV at a future date (subject to the debenture terms).

This means that Antfin’s exit wasn’t permanent. Even though Antfin no longer appears as a shareholder on the books, it still holds a claim. It can either convert those debentures and reclaim the shares later, or even sell the debentures to another party. That is, Sharma was given decades-long credit to pay for the shares, which is a tacit admission that Antfin’s economic interest remained fully alive.

According to independent analysts, this setup has major implications:

- Antfin can convert OCDs at will. If and when conditions are right, those debentures can be turned into equity in RAM BV, restoring an indirect 10.3% stake in Paytm to Antfin.

- Conversion terms are undisclosed. To date, Paytm has not publicly revealed the timeline or conditions for conversion. Mundhra’s analysis notes “No fixed timeline or terms for this conversion have been disclosed publicly”.

- Investors remain in the dark. Ordinary shareholders and even regulators were not informed of this structure ahead of time.

In short, this creates a doubt that the 10.3% stake is merely “parked” in a shell company for now? Antfin retains a form of control until those debentures are dealt with, making the so-called “exit” far from clean.

Is the ownership is only on Paper, as signalled by Sharma’s Dutch Vehicle and Regulatory Labeling?

Although RAM BV is technically “owned” by Vijay Shekhar Sharma, regulators have noted the cozy link to Antfin. NDTVProfit’s April 2025 report laid it out: “Sharma also controls 10.27% stake through Resilient Asset Management BV in agreement with Antfin (Netherlands) Holding BV”. In other words, even as Paytm’s filings list RAM BV (and its 10.3%) under foreign shareholding, insiders know it’s really part of Sharma’s sphere.

Moneycontrol adds context: it points out that in August 2023 “Sharma agreed to purchase a 10.3 percent stake from Antfin through Resilient Asset Management BV, which is owned by Sharma”. Strikingly, despite this being Sharma’s own entity, Paytm classified the 10.3% as “Foreign Direct Investment” in its June 2024 shareholding disclosures. (Presumably to appear compliant with India’s “non-promoter” norms.) In effect, all these pieces highlight a discrepancy: VSS on paper took control of those shares, but only under a veil of convertible debt.

)

The 2025 filings reveal the full extent of Sharma’s influence. By March 2025, Sharma directly owned ~9.1% of Paytm and 4.87% through a family trust, and on top of that he effectively controlled the 10.27% via RAM BV. That means a combined promoter grip of roughly 24.24%; which is more than enough to make Sebi consider him a “de facto promoter.” Normally, SEBI would combine all these holdings when checking promoter limits, but Paytm’s regulators had accepted the Netherlands filing as FDI. This loophole is now under scrutiny in Sebi’s investigations into IPO disclosures.

Regulatory Roadblocks: Will Indian Authorities Take Note Of This?

The backdrop is that Indian regulators have long scrutinized Paytm’s Chinese links. When Paytm applied for various licenses in 2022–2024, the RBI and IRDAI repeatedly balked, often citing FDI ownership caps. Among the major obstacles:

- Payment Aggregator License (RBI): RBI initially rejected Paytm’s application for a payments aggregator licence in late 2022, explicitly pointing to FDI norm non-compliance. Paytm had to secure a fresh FDI nod from the Finance Ministry in August 2024 before reapplying.

- General Insurance Deal (IRDAI): Paytm’s plan to buy Raheja QBE General Insurance (announced 2020) fell apart after years of delays. By May 2022, Paytm publicly stated the acquisition SPA was terminated because it could not complete “within the agreed time period”. Media and analysts believe IRDAI’s inaction on approvals was a key cause. (Paytm later said it would seek a new insurance license instead.)

- Payments Bank (RBI): Paytm Payments Bank has been under the scanner for non-compliance for years. In February 2024, RBI froze its ability to take new deposits and began winding down its operations. By mid-2024, RBI had effectively cancelled the bank’s licence, a development the press widely reported. (With Paytm owning 49% of PPBL, Sharma stepped down as its chairman under RBI’s deadline.)

These setbacks were all linked to compliance issues and risk perceptions. Crucially, analysts and Paytm insiders have connected them to Chinese ownership: having Antfin (or any Chinese entity) on the cap table was cited as a red flag. Indeed, “foreign shareholding concerns” were specifically mentioned as reasons for regulatory denials. In short, India’s regulators have been signaling that Paytm needed to diminish its Chinese ties before any fresh approvals.

By July 2023, it appears Paytm’s strategy was to present a ‘clean’ ownership structure to regulators, even if it meant sidestepping transparency. Sharma’s maneuver gave him a bigger piece of Paytm and cleaned up its cap table. It is predicted this could accelerate approval of Paytm’s other pending businesses. In fact, experts said the shift “may help the company apply for regulatory nod” for new financial licences.

Put simply, the goal was clear: reduce visible Chinese shareholding to appease RBI/IRDAI. And this actually happened. As recent, Paytm Payments Services has received the RBI’s approval to operate as an online payment aggregator. This lifts restrictions on onboarding new merchants, in place since November 2022. On paper, Antfin’s name vanished from the stock registry. And sure enough, after the block deal in Aug 2025, media outlets joyfully noted Paytm now had “zero Chinese ownership”. The stock even got a bump, as analysts said removing the Chinese overhang could unlock RBI’s approvals.

However, critics argue this is a classic shell game. The real control arguably never left Antfin; it merely moved behind VSS’s vehicle. If regulators focus only on public share listings, they may be misled. In a normal scenario all shares held by one person (even via different entities) would be counted together. Here, Paytm’s own filings explicitly diverged from that practice by classifying the Resilient-held stake as foreign investment. This technicality let Sharma declare compliance with promoter rules, but it also obscures the true picture.

Isn’t This A Fake Exit As There Are The Risks of the OCD Structure?

Even if Paytm now secures those licences (and some media optimism suggests it might), Antfin’s convertible debt could spring back. Analysts stress that nothing prevents Antfin from converting or selling its stake later. As Jayant Mundhra bluntly summarizes: “Antfin has the right to convert the OCDs into a direct shareholding in RAM BV, which will give it back an indirect shareholding in Paytm, any damn moment!”.

Putting another way, the shares were merely lent out. If Paytm’s fortunes improve or regulations finally ease, Antfin could reclaim the shares it never really sold. In fact, the fintech media outlet The Head&Tale reports a Paytm insider saying Sharma has “enough timeline where he can arrange for the money and pay”, implying decades of credit extended to him to redeem the debentures. That’s not an exit, it’s a long-term loan guarantee.

Moreover, Antfin need not convert the debentures at all. Mundhra points out that Antfin could simply sell these convertible instruments to any investor if Paytm’s price rises later. The Reuters-blockdeal reports confirm a slew of bulge-bracket banks handling share trades—Goldman Sachs and Citi were even tapped for Antfin’s most recent sale. Any qualified buyer (perhaps even Sharma himself) could purchase the OCDs, effectively stepping into Antfin’s shoes.

In short, the exit is illusory. It can be observed that the transaction was done through a holding entity wholly owned by Sharma, meaning SEBI might eventually club all stakes together. Until the OCDs are fully retired, Antfin retains hidden leverage over Paytm’s future. Investors who assume the Chinese have truly left are being sold a mirage.

Remarkably, almost no mainstream outlet raised these complications. Press coverage of Antfin’s sale in August 2025 simply parroted corporate news releases and noted the regulatory blessing. All emphasized “zero Chinese ownership” and potential license approvals. None flagged the Dutch entity or OCD structure. Paytm’s own statement to exchanges was laudatory, framing the 2023 deal as strategic “share deal” to satisfy regulators (without detail).

Meanwhile, Vijay Shekhar Sharma himself has stayed mostly quiet on the matter. Since the IPO he has faced show-cause notices (from SEBI) and PR challenges on unrelated issues, but he has not publicly explained why this 10.3% transfer was done the way it was. Paytm’s regulatory filings disclose the facts only cursorily, and its investors have not been given a clear explanation of the conversion timeline or terms. Notably, the senior executives at Paytm who negotiated this deal are still at large (Sharma remains CEO), and none have faced charges specifically for misleading shareholders about it.

The only detailed critique so far comes from independent analysts like Jayant Mundhra. In a viral LinkedIn exposé (picked up by fintech blogs) Mundhra lists a barrage of unanswered questions: Why is the OCD conversion timeline undisclosed? Who are the other directors of RAM BV, and what is their relationship to Antfin? Has SEBI probed this arrangement as a possible disclosure lapse? Mundhra argues that without these answers, shareholders and regulators cannot trust the rosy narrative.

To date, however, the Indian media has largely ignored these issues. The bold statements from a foreign securities regulator (RBI) about Paytm’s banking license violations, or SEBI’s show-cause over IPO ESOPs, have grabbed headlines. But the subtle mechanics of the 2023 Antfin deal have remained in the shadows of quiet filings and specialized reports.

Questions That Remain

The expose by Mundhra and other analysts paints a disturbing picture: Paytm’s purported “Chinese exit” may simply be a regulatory facade. The key facts cited in company filings and credible media are clear:

- Sharma’s Dutch shell holds 10.3% of Paytm (transferred from Antfin).

- Antfin got convertible debentures in return, with rights to reclaim that stake.

- No cash changed hands; the deal was structured as debt.

- Regulators denied Paytm key licences citing foreign ownership.

- Media outlets claim all Chinese owners are gone, but ignore the devil in the details.

If RBI and IRDAI finally lift their objections on the basis of the cleaned cap table, which has already started; the convertible debt could be exercised, subverting the whole point. On the other hand, if approvals remain stubbornly withheld, Antfin still stands to profit: it could sell or otherwise transfer its dormant claim at a high price in the future.

For millions of small investors and fintech customers, this is far from a trivial matter. Paytm’s valuation and growth plans depend on trust in governance and transparent operations. The opaque way this stake was handled effectively hiding a major shareholder via technicalities,which undermines that trust.

Now that the deal has come under scrutiny, it is time for the truth to be told. Paytm’s management should publicly clarify the nature of the OCD agreement (including tenure and interest terms), and confirm whether Antfin can re-enter Paytm’s equity. SEBI and other regulators ought to probe whether this transfer complied with securities laws (especially promoter/FDI norms). Indian journalists and analysts should not be satisfied with PR boilerplate; they should demand detailed disclosures of who ultimately owns the company’s critical stakes.

Until these questions are answered, the sensational headlines of “Chinese exit” ring hollow. The 10.3% of Paytm has merely changed hands in legal form; a sleight of paper that has left serious issues unresolved. In the complex world of fintech regulation, the devil remains very much in the details.