From Insolvency To IPO In 3 Years: BPTP’s 180° Turnaround!

On one side Kabul Chawla in a tuxedo receiving an award for “builder of the year” to applause; on the other side, a group of middle-class buyers holding a candlelight vigil outside an unfinished BPTP building, holding placards that read “Justice Delayed = Justice Denied”.

Introduction: How to Nearly Collapse and Still Laugh to the Bank

In the stories of corporate comebacks, few can rival the jaw-dropping “turnaround” of Business Park Town Planners (BPTP) Ltd., a Delhi-NCR real estate developer that went from staring at insolvency in late 2022 to pitching a ₹5,000 crore IPO by 2026. It sounds like a plot twist straight out of a dark comedy. One moment, creditors are knocking on its doors desperate to recover dues, and the next, BPTP is waltzing down Dalal Street, all sins seemingly scrubbed clean. How did they do it? Sheer genius, of course – if by genius we mean a mix of last-minute legal jukes, “creative” financing, and a healthy dose of audacity masked as corporate resilience.

In this writeup, we chronicle BPTP’s journey through frauds, scams, and legal scrapes. We should actually raise a toast to appreciate BPTP’s ability to flout norms, dodge accountability, yet somehow emerge stronger (and richer). From a 2011 fraud case that resulted in an arrest warrant (never executed, naturally) to an August 2025 Enforcement Directorate raid that uncovered “financial ingenuity”, to the grand finale of an IPO that promises to convert past baggage into public money, we’ve got it all.

We’ll laud BPTP’s “innovations” in real estate cheating, applaud their “sustainable” approach to both green buildings and red flags, and marvel at how Kabul Chawla, the company’s elusive founder, managed to collect awards on stage while buyers and law agencies chased his shadow. In the end, you might just join us in a round of sarcastic applause for BPTP, the unsinkable ship that not only stayed afloat but is about to set sail on the stock market, leaving a wake of unfinished projects and incredulous onlookers behind.

The Near-Collapse of 2022: Insolvency?

Every great comeback story needs a cliffhanger moment. For BPTP, that moment came on November 14, 2022, when the National Company Law Tribunal (NCLT) admitted an insolvency petition against the company. An operational creditor, RBCL Projects, had finally had enough of waiting for dues from BPTP’s long-delayed construction projects and moved to trigger a Corporate Insolvency Resolution Process (CIRP).

It looked like curtains for BPTP; the tribunal even appointed an Interim Resolution Professional and declared a moratorium on the firm’s assets. Imagine the desperation of suppliers clamoring for ₹5.9 crore in unpaid bills, a litany of “pre-existing disputes” conjured by BPTP dismissed as “afterthought and moonshine” by the court. One day in, BPTP was officially on the brink of bankruptcy.

But fear not, our hero BPTP has a black belt in last-minute escapes. On November 15, 2022, just one day later; BPTP miraculously “settled” the dispute with the creditor. (What timing, almost as if insolvency was optional.) By Nov 19, 2022, the appellate tribunal (NCLAT) was informed of this sudden moment, and NCLAT promptly stayed the NCLT’s order initiating insolvency. In the words of the order, “In the meantime, we stay the order dated November 14, 2022.” Translation could be insolvency crisis averted. Just like that, BPTP lived to see another day; no restructuring, no resolution plan, just a swift payment to hush the aggrieved creditor. Problem solved, right?

Let’s all cheer BPTP’s ability to negotiate under pressure. It takes real talent to bring a company back from the verge in 24 hours. Should we praise them for this last-minute settlement to avoid complete collapse? Absolutely! After all, it’s not about addressing underlying issues, it’s about kicking the can down the road in style. This was merely a “stayed crisis, not a resolved one”, but why focus on that negativity? BPTP taught us that if you can stall disaster today, you can always deal with consequences, tomorrow. Maybe. In the meantime, the insolvency shadow remained just that a shadow; while BPTP moved on as if nothing happened. Nothing to see here, folks!

Little did we know, this brush with bankruptcy was just the prelude. The real show was about to begin as a series of revelations about BPTP’s past escapades that would make even the boldest scamsters blush, and yet, none of it stopped the company from charging toward that blockbuster IPO. Let’s rewind the clock a bit and take a tour of BPTP’s greatest “achievements” in the fraud department, shall we?

Flashback to Fraudland: BPTP’s Greatest Hits (2011–2014)

To understand BPTP’s journey, one must begin at the fertile grounds of Faridabad, from 2006-2011. Back then, BPTP was busy selling the dream of new plots and flats in its ambitious projects. Homebuyers, including over 1,000 individuals and notably 300+ retired military officers who’d served the nation invested their life savings for promised homes in Faridabad. By 2010–2012, those homes were supposed to be delivered. But they weren’t. What unfolded instead was one of the National Capital Region’s largest alleged real estate frauds, a mega-scam of roughly ₹400 crore that would set the tone for BPTP’s operations for years to come.

2011: The FIR and the (Never Executed) Warrant

Our story truly kicks off in January 2011, when Faridabad police registered the first major FIR against BPTP Limited. The allegation was that BPTP collected enormous payments but failed to deliver the plots and flats in a housing project, essentially duping buyers on a grand scale. The complainants were frantic homebuyers who realized that even as deadlines whooshed by, BPTP hadn’t even obtained basic approvals for the project; meaning those glossy brochures were selling nothing but an illusion.

The case escalated quickly. By December 2011, a Delhi court (Patiala House) issued a non-bailable warrant for BPTP’s MD, Mr. Kabul Chawla, after he repeatedly ignored summons in a cheating case. One specific complaint by a businessman detailed how he paid ₹40 lakh for a commercial plot booking in 2006, only to discover BPTP hadn’t secured the required land approvals at all. When he raised questions, BPTP promptly cancelled his allotment and forfeited his money, a classic move from the BPTP playbook. The court apparently found prima facie evidence of cheating and hence the warrant.

Now, in a normal universe, a non-bailable warrant against a company chief would result in, you know, an arrest. But welcome to the BPTP universe, where normal rules bend. Shockingly (or not), as of 2026, a full 14 years later, Mr. Chawla has never been arrested on that warrant. The man literally became a globe-trotter instead. Reports say he fled India around 2011 and set up base in the United States (primarily New York City), all while the warrant gathered dust. Unfortunately, an Indian court-issued warrant has been lying unenforced for over a decade, even as its target hobnobs abroad.

Perhaps we should commend Mr. Chawla for his exceptional evasion skills. Not everyone can dodge Indian law for 14 years and counting! It takes finesse, or maybe just strong political connections in his home state of Haryana to achieve this level of untouchability. And look at BPTP, still operating cheerfully with headquarters in Gurugram all this time, as if its CEO isn’t officially a wanted man. In the official narrative, BPTP “grew faster than seasoned real estate giants” in the past decade. Who cares about a pesky warrant when you’re busy expanding your empire? BPTP likely viewed the 2011 warrant as a mere paper tiger, and so far, they’ve been right.

Faridabad Fiasco: 1000+ Homes, 0 Delivery

The 2011 FIR was just the tip of the iceberg. The Faridabad projects scam encompassed multiple projects (like Discovery Park, Park Serene, etc.) launched between 2006–2008. BPTP’s modus operandi was straightforward, that sell units without getting necessary approvals, collect 100% upfront payment from eager buyers, promise a delivery date a few years out, and then, well, see what happens. What happened was nothing, for years.

By 2011, not a brick in place, hundreds of crores had vanished, and over a thousand middle-class families were stuck paying EMIs for homes that only existed on paper. Many of these buyers, as noted, were retired Army and Navy officers, the very folks who defended the country only to be swindled when they tried to secure a peaceful retirement home.

Under mounting pressure, BPTP did attempt some damage control. In 2018, a decade late, the company hurriedly constructed 5 residential towers in Faridabad to pacify the protesters. Success, right? Not so fast. These hastily built towers came without basic amenities; no water supply, no electricity connections, no proper road access. Even the promised lush parks and clubhouses were missing.

It was like gifting someone a car without an engine. The buyers, understandably, refused to take possession of these half-baked units in 2018, saying “thanks but no thanks.” So BPTP pivoted to Plan B, which was a settlement. In 2019, they signed an agreement with buyers promising to complete everything by September 2020. Great, as now you expect the problem to be solved; except BPTP treated that deadline as casually as the first. By the time September 2020 rolled around, COVID-19 had hit, giving BPTP a convenient excuse to halt construction yet again.

And so, as of 2025-26, many of those Faridabad buyers are still waiting, now 15+ years since payment. Some buildings remain glorified concrete shells, and those “completed” lack livable conditions. Yet, through all this, BPTP kept launching new projects elsewhere, and Mr. Chawla kept a safe distance (by an entire ocean, in fact).

What if we call attitude a positive one- BPTP showed admirable patience and consistency – sticking to their buyers’ money all these years. They also demonstrated flexibility; when caught selling unapproved land, they didn’t let it slow them down. They simply cancelled bookings and forfeited payments of anyone who asked too many questions- a proactive customer service strategy, perhaps? If some call it fraud, BPTP might call it “creative project financing”. After all, collecting interest-free advances from buyers sure beats taking expensive bank loans.

And why rush with approvals or construction when you have a 15-year rolling timeline? Eventually, maybe you throw up a few towers (better late than never!) and hope the buyers’ fatigue leads them to accept whatever they get. Brilliant! In a cynical way, BPTP’s Faridabad playbook was almost ahead of its time; it prefigured many Indian realty scams to come. Of course, none of this stopped BPTP from marketing itself as a successful developer with a “presence” across NCR and thousands of units delivered (we’ll get to those claims).

FIRs Everywhere, and Not a Drop of Justice

Once the dam broke in 2011, there was a deluge of legal cases against BPTP and its enigmatic MD. Between 2011 and 2016, police in multiple jurisdictions, Faridabad, Gurgaon, Delhi, registered over a hundred FIRs alleging cheating, criminal breach of trust, conspiracy, and even forgery by BPTP officials. By 2014, Faridabad police had expanded their fraud case as more than 1,000 buyers came forward.

In 2016, Gurgaon police lodged three separate FIRs for a Sector 102 plot scheme where investors were allegedly duped of around ₹3 crore, with charges under IPC Sections 420 (cheating), 406 (breach of trust), 467,468,471 (forgery of documents), and 120-B (criminal conspiracy) being invoked. It appears BPTP’s legal department was perhaps busier than its construction department!

The Enforcement Directorate’s records later noted that “multiple FIRs are registered against BPTP Ltd. and its Directors across various police stations in Delhi-NCR for non-completion of projects and diversion of funds”. When the federal financial sleuths casually mention your company in the same breath as fund diversion, you know you’ve made it to the big leagues of scandal. There were also murmurs of Delhi Police’s Economic Offences Wing (EOW) probing some cases, and even an Interpol Red Corner Notice being considered at one point when Chawla refused to return to India.

Yet, through this thicket of FIRs and legal processes, notice something; BPTP’s projects kept selling, and the company never stopped operations. It was almost as if the law was on one planet and BPTP on another. Homebuyers filed criminal cases, courts issued orders, but on the ground, BPTP marched on, launching new phases and collecting fresh bookings. Money has a way of dulling the noise, perhaps. And those who already paid? Well, they learned to join the queue of litigants or shout into the void on consumer forums (more on that later).

A lesser company might have crumbled under the weight of 100+ FIRs. But not BPTP. Such resilience! One could argue BPTP treated FIRs as a mere occupational hazard – an opportunity, even, to engage their lawyers in full employment. If you think about it, BPTP kept courtrooms across NCR busy, contributing to the economy by way of legal fees. An unsung CSR activity? Perhaps we stretch. Regardless, the ability of BPTP to continue business as usual while being entangled in so many criminal allegations is almost; admirable, in a twisted way. It’s like they wore these FIRs as invisible badges of honor – proof that they were pushing boundaries (of law and customer patience) to the absolute limit.

Money Magic: ED Raids, Hidden Assets and the Great Escape

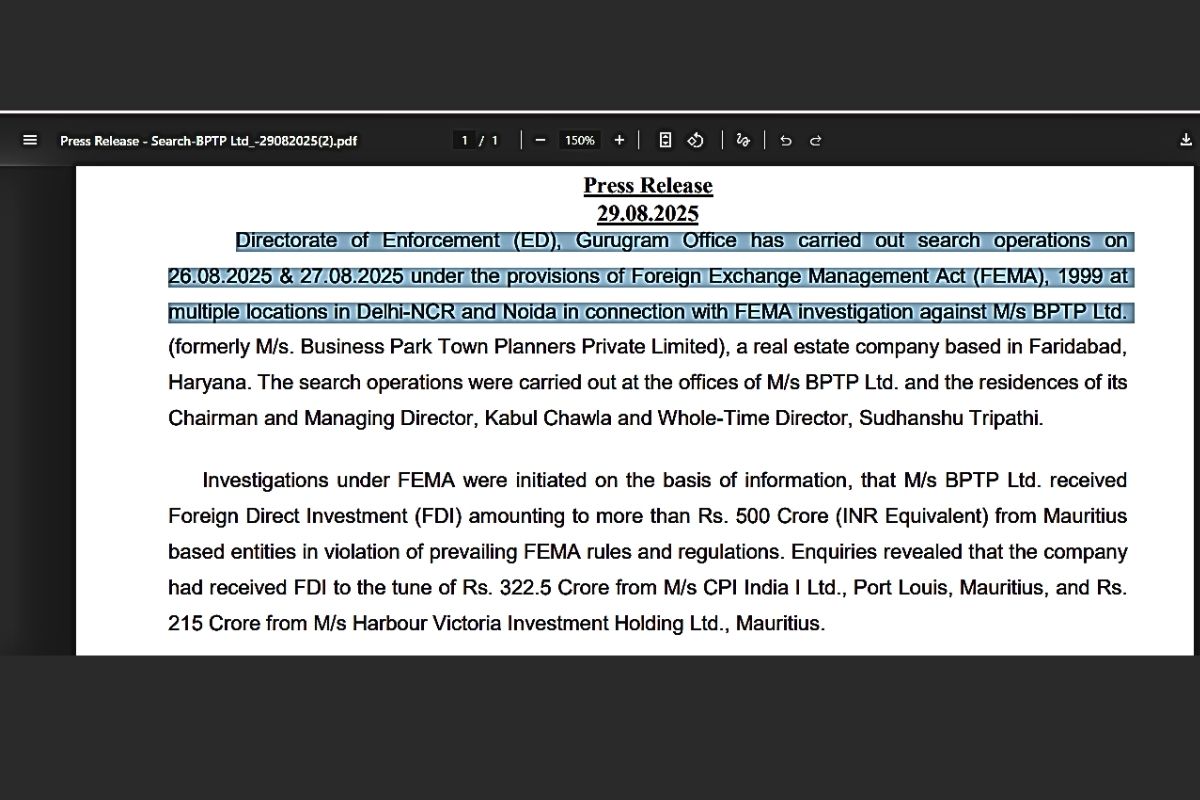

If the local police cases were pesky mosquitoes, the Enforcement Directorate (ED) swooping in was a bit like a hawk circling overhead. By 2025, the Indian authorities finally got markedly more serious about BPTP’s financial shenanigans. Enter the ED – investigating money laundering and foreign exchange violations. And oh boy, did they find some interesting things.

In August 2025, the ED conducted multi-city raids on BPTP’s offices in Delhi, Noida, and Faridabad, as well as at the plush residences of Kabul Chawla and his lieutenant, Director Sudhanshu Tripathi. This was no minor inquiry; it was under the Foreign Exchange Management Act (FEMA) and Prevention of Money Laundering Act (PMLA), suggesting the suspicion of serious financial crimes.

According to the ED’s official press release, BPTP had received over ₹537.5 crore of Foreign Direct Investment (FDI) from two Mauritius-based entities back in 2007–08. Nothing wrong with FDI, except these funds came with illegal put-option guarantees (assuring the investors a fixed exit price) which violated RBI rules and FEMA regulations. In lay terms, BPTP had allegedly promised its foreign investors (one of which was Citi’s fund and another JPMorgan’s fund, as it turns out) guaranteed returns – a big no-no for FDI in real estate.

What did the ED do? They froze bank lockers, seized incriminating documents and digital evidence, and likely gave BPTP’s remaining management a few sleepless nights. Crucially, ED investigators found that despite RBI directing BPTP to amend those shady investment clauses, the company simply didn’t – effectively thumbing its nose at the central bank.

The ED uncovered that Kabul Chawla was the beneficial owner of multiple offshore entities, “one of which had been used to acquire a costly immovable property in New York, USA”. Aha! That infamous New York condo makes a cameo (more on that in a moment). The ED also noted that those foreign investments and the overseas assets were under scrutiny, along with evidence that funds meant for projects were diverted abroad.

Media sources summed it up. ED alleged BPTP routed about ₹500+ crore via Mauritius in 2007-08 through unauthorized means, and that Mr. Chawla quietly held foreign assets (like luxury property) even as homebuyers’ projects languished. It was further reported that over ₹200 crore may have been siphoned to Singapore and the U.S. through these maneuvers – presumably helping fund the high life overseas. The money trail was hot, and for the first time perhaps, BPTP faced the real possibility of large penalties (FEMA violations can attract fines triple the amount involved, theoretically) and asset seizures.

Now, now, before we rush to judgment, let’s consider the bright side. BPTP was simply engaging in “global diversification” of assets. Isn’t it prudent for a company to hedge its bets by moving money overseas, lest it all be stuck in one country’s real estate? Sarcasm aside, the ED’s findings basically confirmed what angry buyers had long suspected, that their hard-earned money for flats might have been used to buy Mr. Chawla a fancy pied-à-terre in Manhattan and to enrich mysterious shell companies abroad. If true, one must admire the audacity. Why limit yourself to the Indian market when you can leverage Mauritius, Singapore, New York – truly a global strategy!

BPTP could argue they were forex pioneers, exploring innovative ways around Indian regulations. And the timing, doing this in 2007-08, was impeccable, coinciding with that first IPO attempt. Sure, ED called it violation of law and possible laundering, but maybe BPTP would call it “strategic fund allocation”. In their defense, the company claimed full cooperation with investigators. Insiders, however, described a scene of panic at BPTP’s offices, the kind of vibe you get when the DJ ED crashes your party.

The New York Penthouse: Living it Up While Homes Burn Down

Ah yes, the New York connection, perhaps the most flamboyant chapter in BPTP’s saga. Around the same time BPTP’s Indian buyers were protesting with placards in Faridabad, it emerged that Kabul Chawla had acquired a 4,050 sq. ft. super-luxury condominium on the 76th floor of the Time Warner Center in Manhattan, New York. Price tag? Roughly $19 million (that’s about ₹140 crore in today’s money).

This was around 2011-2012, literally the same time the first FIR was filed and that NBW was issued back home. The irony is delicious: one day you’re named an accused for cheating ₹400 crore from Indian homebuyers, a few months later you’re buying a five-bedroom sky palace in NYC with what one can only presume is very luck-based money.

This came to light thanks to an investigative report by The New York Times, which inquired into foreign money flowing into Manhattan real estate. They found Mr. Chawla’s name (and one other Indian developer’s) listed as owners of big condos in that elite building. When confronted, Chawla of course denied owning the Time Warner apartment, claiming perhaps it was just an “investment vehicle” or that he was only staying there as a guest.

But leaked emails and records told a different story, and even BPTP’s own PR to Indian media couldn’t fully put out that fire. Business Standard noted how Chawla “grabbed headlines for buying a ~$19 million New York apartment at a time when BPTP was facing the ire of consumers over delays and poor quality”. The optics of that are astounding. imagine dozens of middle-class families in Faridabad slogging to pay both rent and a home loan because their BPTP flat is delayed indefinitely, while the man responsible is reportedly enjoying Central Park views from a high-rise in NYC. It’s almost poetic in a twisted way.

Mr. Chawla also reportedly purchased a posh bungalow on Amrita Shergill Marg in Lutyens’ Delhi, one of India’s most expensive addresses. Because why not diversify one’s luxury real estate holdings? All this while officially absconding and not showing face in any Indian court.

We must give credit that Mr. Chawla truly lived the BPTP brand. BPTP sold dreams of luxury lifestyles to buyers; Chawla went ahead and enjoyed a luxury lifestyle, just maybe not exactly where the buyers expected. Perhaps BPTP could spin this as “proof of concept” that the MD demonstrating what high-end living looks like (just not in the BPTP properties marketed). On a serious note, the New York condo became a symbol of BPTP’s alleged fraud, prompting outrage that echoed from consumer forums to social media.

It confirmed people’s fears that their money had been siphoned off abroad. By 2025, even the ED explicitly cited the “overseas property” in New York connected to Chawla as under examination. Meanwhile, Indian authorities toyed with issuing a Red Corner Notice to get Interpol’s help in nabbing him, but somehow it never materialized effectively. One almost imagines Mr. Chawla sipping champagne in Manhattan, watching news of protests outside BPTP’s Faridabad site, and saying, “So glad I’m not there.” As a character in a satire, he’s almost too on-the-nose, where the fugitive tycoon enjoying life abroad while victims back home chant his name in vain. If this were a movie, critics would pan it as unrealistic – yet here we are.

A Deluge of “Fan Mail”: Consumer Complaints Galore

While Kabul Chawla was “living it up” abroad, back in India ordinary homebuyers were flooding every forum imaginable with complaints against BPTP. If BPTP had a fan club, it existed on sites like ConsumerComplaints.in, MouthShut, Voxya, and countless Facebook groups of aggrieved buyers – except the tone was less fanboy gushing and more furious ranting. Over the past 10-15 years, thousands of complaints have been lodged, many unresolved to this day. It reached a point where BPTP’s name became synonymous with delay and deceit in certain circles. Let’s summarize the greatest hits of these grievances (keeping our diplomatic filter on, of course):

- Non-Delivery of Homes: The most common refrain – “We paid 90-100% for our flat/plot, and a decade later BPTP still hasn’t delivered possession.” Projects launched in 2007-09 with promised handovers by 2011-12 were, by 2025, still incomplete. By one estimate, over 5,000 units across 15+ projects were delayed for years. Imagine paying EMIs for a home that only exists in a brochure – thousands of BPTP customers didn’t have to imagine.

- Building Without Approvals: Many realized to their horror that BPTP sold them projects that lacked government approvals (from HUDA or the town planning authorities). BPTP would launch a project, take money, and then maybe apply for clearances. In cases like Faridabad’s, approvals were not in place when bookings happened. A classic “oops, we forgot to mention” scenario.

- Arbitrary Changes & Charges: Buyers often complained that even after signing agreements, BPTP would come up with surprise charges or changes. For instance, suddenly increasing the super area of the flat on paper (hence demanding more money), or introducing development charges for facilities that never materialized. It was like a gym membership that keeps billing you for equipment you never get to use.

- Lack of Basic Amenities: BPTP sometimes did deliver units (hooray!) but then forgot to provide basics like water, electricity, sewage, or road access. For example, in Faridabad, a handful of towers built had no water or power connections as late as 2018. In their glossy ads, BPTP promised lush green parks and state-of-the-art clubs; on ground, people got dry taps and unpaved paths. Some delivered projects lacked the very amenities that were charged in advance.

- No Refunds, No Exit: When buyers, fed up with delays, asked for refunds, BPTP’s response was a consistent “No.” They would neither finish the project nor refund the money. Buyers were trapped in limbo: they couldn’t even sell the property easily because no completion certificate was in sight. It’s the classic Hotel California of real estate – you can check out any time you like, but you can never leave (with your money).

- Incomplete Documentation: In many cases, BPTP didn’t even execute final Builder-Buyer Agreements on time (or at all). Take the case of Ms. Shahin Akhtar, who booked a floor in 2012 – BPTP never gave her a formal buyer’s agreement for years, despite her repeated requests. They were happy to take her money, of course, but without the agreement she couldn’t get her home loan fully disbursed. When she pressed, BPTP casually canceled her allotment and kept her money, forcing her into a legal battle. (Spoiler: the consumer court lambasted BPTP for this “unfair trade practice” and ordered refund with interest. But that took years.)

These issues weren’t one-offs, they were systemic. Projects repeatedly mentioned in complaints and case filings include Discovery Park (Faridabad Sector 80), Park Serene, Princess Park, Amstoria (Gurugram Sector 102), Spacio, Park Elite Floors, and more. For instance, buyers of BPTP Discovery Park were still fighting after 9+ years; towers L & M of that project were promised by 2020 and remained incomplete in 2025.

In BPTP Amstoria, a buyer Raghbir Singh (in a 2021 case) pointed out he paid a premium for a “luxury” plot which stayed a barren piece of land for years. BPTP Park Serene had such issues that even the Central Bureau of Investigation (CBI) reportedly looked into it around 2011 because it involved hundreds of defence personnel. By 2024, Park Serene was infamous again for an unrelated tragedy (we’ll come to that).

It got so bad that resident associations and buyer groups organized protests, went to media, even approached the Haryana government and RERA (Real Estate Regulatory Authority). Sometimes a small victory came – e.g., Haryana RERA in one 2025 case (Navneet Kumar vs BPTP) did grant some relief (though in another, they denied compensation because the buyer took possession despite defects, which BPTP touted as a “win” even though it wasn’t exactly a clean chit). But by and large, the consumer agony continued unabated, a testament to the slow grind of justice and the persistence of BPTP in not doing what it promised.

One almost feels for BPTP here – maintaining such consistent performance across so many projects is truly hard work. (Consistently defaulting, that is.) In a satirical sense, BPTP excelled at a certain customer experience: the run-around. They kept buyers united – unfortunately for them, united in anger. The volume of complaints became a chorus so loud that any prospective IPO investor doing a cursory Google search would find horror stories on page after page. Yet, remarkably, BPTP’s official marketing never skipped a beat: they claimed “customer satisfaction” and bragged about how many units they delivered.

For the record, BPTP’s pitch asserts they delivered 24,500 units across 2,000 acres. Perhaps they did, but thousands of undelivered ones don’t feature in the brochure. Should we applaud BPTP’s customer engagement? They certainly engaged – albeit via courtrooms and protest rallies. If nothing else, BPTP brought many strangers together as friends, bonding over mutual frustration. A twisted social service? That might be too diplomatic, let’s just call it what it is: a mess that BPTP deftly sidestepped publicly while quietly dealing (or not dealing) with complaints on a case-by-case basis, often only when legally compelled.

Courtroom Capers: When Buyers Fought Back

For all its nonchalance, BPTP couldn’t entirely ignore the courts. A number of cheated buyers took the fight to consumer courts and won significant judgments against BPTP. The National Consumer Disputes Redressal Commission (NCDRC, the top consumer forum) in particular delivered some withering orders. But true to form, BPTP often tried every trick to delay or dilute these outcomes. Let’s highlight a couple of emblematic cases (with our sarcastic kudos ready):

- Rakesh Kumar vs BPTP (2020/2023): Mr. Rakesh Kumar booked a flat in BPTP’s Gurgaon project Terra. By 2016, despite paying ₹77.77 lakh (out of a ₹1+ crore price), he hadn’t gotten possession – years beyond the promised date. BPTP even demanded an extra ₹20+ lakh arbitrarily at one point. Fed up, he filed a case. In January 2020, NCDRC ordered BPTP (and its subsidiary Countrywide) to refund the entire ₹77.77 lakh with 9% interest, plus ₹50,000 compensation for harassment. This was a big win for the consumer. BPTP’s response? Appeal, delay, review – basically stonewall. They filed a review petition (to reargue the case) and then asked the NCDRC to postpone enforcing Rakesh’s refund until that review was decided. Nice try – but in March 2023, NCDRC slammed the door on that, stating there was “no justification to postpone” relief and that the buyer should not be made to wait for some interminable review process. They reaffirmed BPTP must pay up within 2 months. In legalese, the court basically said stop playing games and refund the man. BPTP finally had to cough up the money (we presume, unless they found another labyrinthine legal avenue).

- Shahin Akhtar vs BPTP (2020): We previewed this one. NCDRC (or a state commission) in Oct 2020 found BPTP’s conduct utterly indefensible. BPTP’s failure to give Ms. Akhtar a buyer’s agreement, then canceling her flat without cause, was termed a “clear case of unfair trade practice” causing loss and injury. The court ordered BPTP to refund her nearly ₹10 lakh with interest, plus ₹2 lakh for harassment and ₹50k legal costs. The judgment noted how the company utilized her money for years and gave nothing in return, and how she had to wage a “long drawn legal battle” for relief. It’s scathing to read – the court essentially calling out BPTP’s behavior as oppressive and arbitrary. If BPTP had any shame, it wasn’t apparent; but at least the law recognized the injustice.

- Other Cases: In Pradeep Sharma vs BPTP (Dec 2019), a batch of appeals saw NCDRC upholding consumer rights again – with the Commission stating that despite any technical objections, it “is still open to courts to grant relief which is appropriate, justified and warranted” in such cases. Translation: BPTP’s typical defenses won’t fly when the facts show clear wrongdoing. There’s also Raghbir Singh vs BPTP (2021) about Gurugram’s Amstoria project delays, and numerous executions where even after “consent terms” were agreed (e.g. promising to give possession by X date), BPTP still didn’t comply, forcing contempt actions.

And what were BPTP’s common defenses in court? It’s almost comedic:

(a) They’d point to an arbitration clause in the builder-buyer agreement and claim the consumer forum had no jurisdiction. Courts repeatedly smacked this down, saying a developer can’t contract out of statutory consumer rights – nice try.

(b) They’d argue the buyer is an “investor” who bought multiple units and thus not a genuine consumer. Unless the buyer was actually a property dealer (and most weren’t), courts didn’t buy this. Simply owning 2 flats doesn’t disqualify one as a consumer.

(c) They’d say complaints were time-barred (filed too late). But each delay is a continuing breach, and limitation clocks often reset when a project is indefinitely delayed.

(d) They blamed external factors: market slowdown, government permission delays, and later, the pandemic. Courts acknowledged COVID might justify some delay, but not a decade of non-performance. In one NCDRC order, the bench remarked that BPTP’s excuses were meritless in light of “the oppressive delay and breach”. Ouch.

Let’s clap for BPTP’s legal tenacity. They might lose in court, but they sure make the other side work for it! It’s almost an art form how they leveraged every procedural avenue to delay justice. From filing review petitions to appealing orders to sometimes just ignoring orders until contempt loomed – BPTP showcased a full repertoire. In satire-land, one might say BPTP kept the justice system on its toes, ensuring judges remained sharp and alert to crafty tactics. To be fair, the judiciary largely saw through their ploys.

The NCDRC in one order even said it saw no need to wait for some unrelated arbitration or pending application – the buyer deserved relief now. These verdicts also underscore that BPTP’s malpractices were not mere one-off errors but a pattern. Each court victory by consumers became another exhibit in the case against BPTP’s credibility. And each time BPTP paid up with interest, it effectively admitted that, yes, we took your money and failed you. But here’s the kicker: none of these cases, however damning, deterred BPTP from forging ahead with its grand IPO dreams. If anything, perhaps paying a few 9% interest refunds was just the cost of doing business until they could hit the jackpot of public markets.

Image Makeover: Awards, PR, and the Art of Reputation Laundering

At this point, you might wonder, how does a company with such a track record even think of going public? The answer lies in a well-worn corporate strategy of rebrand, distract, and amplify the positives (even if manufactured). BPTP spent the mid-2020s polishing its image. The pièce de résistance was when Kabul Chawla, in May 2025, received the “IGBC Fellow Award” from the Indian Green Building Council – one of the highest honors in sustainable building circles.

Yes, while ED investigations simmered and homeowners vented online, Mr. Chawla was on stage being feted as a green visionary. The award ceremony was held at a BPTP project (Capital City in Noida) which proudly had a platinum green rating. In his acceptance, Chawla spoke of sustainability as a core value. (We presume he meant environmental sustainability; some wags quipped that financial sustainability of siphoned funds was the subtext.)

BPTP’s PR machinery trumpeted this: press releases in outlets from Times of India to Financial Express quoted how this honor “reflects the efforts of the entire BPTP team” in pioneering sustainable development. Around the same time, articles appeared highlighting BPTP’s “tech-enabled green urbanism” and how their projects align with India’s smart city vision. They boasted of certifications like LEED Platinum and waxed poetic about customer-centric design. If you only read these press snippets, you’d think BPTP was a model developer of timely deliveries, happy customers, a dynamic MD with a golden touch.

This dichotomy was stark. On one hand, public awards and puff pieces; on the other, NBWs and FIRs still unresolved. “Chawla, often portrayed in company PR as a visionary leader honoured with awards like the IGBC Fellow, faces a barrage of allegations that paint a far grimmer picture.” It noted that court records show him as an accused in multiple cases of cheating, breach of trust, forgery, and conspiracy. Indeed, it is almost surreal. In May 2025 he’s getting a trophy for sustainable contributions, and by August 2025 the ED is freezing his bank lockers for allegedly laundering money overseas. Talk about multitasking.

Meanwhile, BPTP’s official narrative was all about how much they’ve delivered and how satisfied their customers are. Their website and brochures boasted of “on-time delivery” and “customer delight” – claims that thousands of forum posts would strongly contest. The company also touted new project launches – e.g. a grand new township on Dwarka Expressway and commercial complexes – to signal growth momentum. They conveniently omitted mention of legacy issues in any investor communication.

This strategy is textbook of “drape yourself in awards and good deeds to overshadow the skeletons in the closet”. One almost admires the brazenness. It’s as if BPTP said, “Yes, we may have a 14-year-old arrest warrant and scores of angry customers, but look, we also have a shiny plaque from CII for being eco-friendly! So all is forgiven, right?” It raises uncomfortable questions.

How did nobody object to giving a public accolade to someone who hasn’t shown up in court for a decade? Perhaps the award committees don’t do background checks, or maybe Chawla’s “strong political connections” in Haryana (often whispered about) smoothed the way. Either way, BPTP effectively used these honours as reputation laundry, scrubbing off some dirt in the public eye. Media interviews around that time feature Chawla talking about industry trends and sustainable housing, with nary a tough question about his pending criminal cases.

On one side Kabul Chawla in a tuxedo receiving an award for “builder of the year” to applause; on the other side, a group of middle-class buyers holding a candlelight vigil outside an unfinished BPTP building, holding placards that read “Justice Delayed = Justice Denied”. It’s a bit contradicting, isn’t it? Yet, this incongruity barely caused a blip in BPTP’s march forward. With image suitably burnished (at least for casual observers or newcomers who didn’t know the history), BPTP was ready for its endgame, the grand IPO.

Financial Gymnastics: From Debt to Wealth (and Ghost Revenues)

Let’s delve for a moment into BPTP’s finances – the boring stuff that might hide exciting red flags. One might expect a company with so many stalled projects to be drowning in debt. Interestingly, BPTP’s on-paper debt wasn’t astronomical; that’s because it largely financed itself through buyer advances. Essentially, customers were the unwitting lenders – handing over crores upfront, which BPTP used and didn’t have to count as bank debt. This model works great until you actually have to deliver the project – which, as we’ve seen, BPTP found ways to indefinitely delay.

By 2015, however, BPTP did face a crunch. Remember those foreign investors (Citi’s CPI fund and JPMorgan’s fund) who put in ₹563 crore in 2007-09? They were supposed to exit via the planned 2010 IPO. When that IPO failed (more on that soon), they eventually took BPTP to arbitration, claiming breach of contract. The pressure was on to repay them their investment (with returns).

So between 2015-2018, BPTP undertook some major asset sales to raise cash. The biggest was in 2015: BPTP sold its 800,000 sq. ft. IT Park “BPTP Crest” in Gurgaon to RMZ Corp for ₹850 crore. This infusion was used to buy back the stakes of JP Morgan and CPI for about ₹693 crore. Basically, they paid off the foreign funds to settle and get them out of the company’s hair. This asset sale seems like a “highlighted desperation”, as BPTP had to part with a prime income-generating asset to cover past obligations.

It’s telling that earlier in 2015, news of Chawla’s $19M New York condo had surfaced, coinciding with BPTP “facing ire of consumers” and scrambling for money. One might connect dots that as the foreign investors turned heat on, BPTP had to liquidate assets – maybe that NYC purchase was a pre-emptive parking of funds elsewhere? Pure speculation of course, but the timing is curious.

Anyway, having shed investors and assets, BPTP in late-2010s kept things afloat by raising project-specific loans and selling smaller land parcels. They positioned themselves as having trimmed down and ready to grow anew. By 2023-24, when IPO talks resurfaced, they projected rosy numbers; a 55% revenue CAGR (Compound Annual Growth Rate) and plans to hit ₹5,000 crore revenue in a few years; these are the claims that many analysts found very hard to believe given the track record.

Skeptics pointed out that IPO proceeds would likely go towards plugging the huge liability black hole – i.e. finishing those stalled projects, paying off settlements, and maybe satisfying any ED penalties – rather than truly expanding business. But if public investors bought the growth story, the current promoters could offload their legacy burdens onto fresh money. How convenient.

Market observers on social media were brutal, they labeled BPTP’s IPO plan as possibly “India’s biggest real estate scam” in the making and a “systematic conspiracy to defraud investors”. Posts warned that unsuspecting investors might see their money wiped out if BPTP’s house of cards collapsed post-listing. They cited that any adverse outcome of ED’s probe or a resurgence of insolvency claims could crash the stock, leaving the public holding the bag. These warnings were not without basis – companies with far cleaner histories have sunk investors; with BPTP’s unresolved baggage, the risk is obvious.

On the flip side (devil’s advocate moment), BPTP could argue: “Look, we survived the worst, we settled with creditors, we even grew revenues in recent years (assuming they did), so we’ve turned the page.” They would stress their land bank and new project pipeline in NCR’s hot property markets. They’d downplay the contingent liabilities; perhaps not even clearly disclosing the magnitude of pending suits (which is itself a red flag if they don’t).

BPTP’s financial journey shows a company always on the edge, yet never tipping over. Is that a virtue? In some corporate success stories, near-death experiences instill discipline and change. In BPTP’s case, one might cynically say each near-death (failed IPO 2010, insolvency 2022, ED raids 2025) was met not with reform, but with doubling down on image management and delay tactics.

Should we admire the financial acrobatics? They did manage to keep the ball rolling for over 15 years, which is no mean feat when you’re essentially robbing Peter to pay Paul. At one point, as per an Income Tax raid back in 2010-11, BPTP was accused of showing “ghost revenues” in their books (i.e., cooking the numbers) to hide issues – though details on that are scant publicly. If true, that’s a whole other creative accounting trophy for them.

In sum, BPTP’s finances were like a swan above water; seemingly gliding (they often reported profits in RERA filings) but paddling furiously beneath (rolling over buyer advances, extending timelines, selling assets, raising private debt). But now, with the IPO, they seek to raise a massive ₹5,000 crore in one go. One might say, if they pull it off, it’s the ultimate refinancing: converting money owed to angry homebuyers and creditors into equity from cheerful stock market investors. Wow! liabilities disappear, or at least get dispersed.

The 2010 IPO That Almost Happened (Or “Been There, Tried That”)

Many aren’t aware that this 2026 IPO isn’t BPTP’s first attempt at going public. Wind back to 2010, BPTP was riding high (on paper) and filed a Draft Red Herring Prospectus (DRHP) with SEBI in Dec 2009. The plan was to raise about ₹1,500 crore by selling 10-15% of promoter equity, implying a healthy valuation. SEBI gave its nod in May 2010, and BPTP was gearing up for the issue. But a series of events threw cold water.

First, global markets were shaky post-2008 crisis (poor timing). Second, and importantly, bad press and legal issues started cropping up – those FIRs and complaints we discussed were gaining attention around 2010-11. There were also murmurs of environmental clearance troubles on some projects, and a minor banking scandal where a mid-level bank manager was accused of giving illegal loans to some BPTP customers (not directly BPTP’s fault, but negative press nonetheless).

By late 2010, BPTP withdrew its IPO plans; officially citing unfavorable market conditions. Unofficially, it was clear that with all the smoke of scam accusations, investor appetite would be weak. This left those early foreign investors (Citi and JPMorgan funds) stranded, as they had been banking on the IPO for exit. By contract, BPTP had promised to list by July 2011 – missing that was a breach. Hence their arbitration and eventual settlement via the IT Park sale in 2015. BPTP learned a lesson: the public markets have scrutiny, and timing is everything.

So here we are, 15 years later, and BPTP is effectively saying “Take 2: This time it’ll be different, trust us.”

They have presumably cleaned up enough in the interim (settled with big investors, got some projects delivered albeit late, and quietened some complaints). They’re riding on a general boom in India’s real estate stocks circa 2025 – DLF, Macrotech (Lodha), etc., have seen upcycles, so why not BPTP? It’s almost like they waited for the collective memory to fade and for a new generation of investors (perhaps younger, unaware of 2010 events) to emerge. After all, 2010’s failed IPO is ancient history in market terms.

“Fifteen years later, the issues persist: Unfinished projects, pending FIRs, and ED probes. Yet BPTP projects rapid growth and expansion… Skeptics argue IPO proceeds will plug legacy holes, not fuel growth.”. That sentence pretty much sums it up. The skeletons haven’t gone away; they’ve just been swept under a plush new carpet laid out for the IPO roadshow.

Let’s charitably say BPTP’s 2010 IPO attempt was a trial run. They got a preview of pesky things like due diligence and investor questions. This time around, maybe they’re prepared with better answers (or better question avoidance). The fact that they even dared to revisit the IPO idea shows, if nothing else, audacity. Perhaps they assume that with a bit of lobbying and the right merchant bankers, the market will overlook past baggage.

To give them some credit, many retail investors do get swayed by the narrative of a turnaround and the allure of big land assets. BPTP might pitch itself as a “reformed prodigal son” of real estate – went astray, now coming back to the righteous path of SEBI-regulated transparency (try not to chuckle). Whether they truly intend to reform or just cash out is the big question. But hey, if at first you don’t succeed, IPO, IPO again!

Tragedy and Triumph: The 2024 Pool Incident and Business as Usual

No BPTP story would be complete without mentioning a tragic event that briefly united residents and homebuyers in outrage. The July 2024 drowning of a 5-year-old boy in a swimming pool at a BPTP project. This happened at the BPTP Park Serene society in Gurugram (Sector 37D) – one of those projects riddled with delays and issues. The child, little Mevansh, wandered into the adult pool area and drowned due to alleged negligence (the lifeguards on duty were reportedly looking at their phones). This heart-wrenching incident ignited a powder keg of resident anger that had been building from years of BPTP’s apathy.

Within days, residents organized protests. They took out a rally of about 80 cars with “Justice for Mevansh” posters, driving to the Gurugram Police Commissioner’s office. They shouted slogans against BPTP’s management, with some banners reportedly calling Kabul Chawla “Kabul Chawla kaatil hai” (a murderer), holding him morally responsible. The public pressure forced the police to act swiftly in this case – though not quite in the way protesters ultimately wanted.

The police arrested two lifeguards and a contractor who managed the pool maintenance, booking them for negligence. BPTP the company, or its higher-ups, faced no legal consequence. The company’s response came via a typical PR statement expressing sadness, offering condolences, and noting that the maintenance was handled by an external agency and they’re “cooperating with authorities”.

Residents, however, saw the incident as emblematic of BPTP’s callousness – delivering a society without proper safety measures, ignoring repeated requests from the RWA to secure the pool area (they had apparently written to management for two years about pool safety). The outrage wasn’t just about one tragedy; it was pent-up frustration of years. They demanded arrests of the real people in charge. For a brief moment, the calls for Kabul Chawla’s arrest got louder again in media. But as with previous such spikes of anger, nothing happened on that front. After the news cycle moved on, BPTP continued undeterred.

If one were cynical, one might note: even a child’s death in a BPTP property did not result in any top executive facing any heat. It underscores a sense of impunity that surrounds the company. Many buyers commented, “If this doesn’t shame the government into taking action, nothing will.” And indeed, nothing substantive happened to BPTP as a result – aside from probably a new caution sign or two near the pool.

It’s hard to joke about a tragedy, so we won’t. The diplomatic thing to say is that this incident was “very unfortunate” and “BPTP has surely learned to implement better safety measures”. But deep down, it’s a glaring example of how BPTP’s negligence had real human costs. We can only satirically “praise” BPTP’s ability to shield itself even in such dire circumstances. They deftly deflected blame onto a contractor. The pool was in a housing complex that likely wouldn’t have been so delayed (and thus perhaps better managed) had BPTP been more responsible from the get-go. But alas, connecting those dots doesn’t happen in legal terms easily. So the company carries on, officially saddened but practically unscathed.

For Kabul Chawla and team, it was apparently just another PR issue to manage. Some banners and protests? Issue a sympathy note, let lower staff take the fall, move on. And that’s what they did. Cue the IPO prep – full steam ahead, because who’s got time to dwell on negativity?

The Grand Finale: 5000 Crore IPO – Laundering Legacy into Legacy (Wealth)

And so we arrive at the present (early 2026). BPTP has reportedly hired merchant bankers, done preliminary paperwork, and is likely weeks or months away from formally launching its ₹5,000 crore Initial Public Offering. It’s being billed as one of the largest realty IPOs in recent times. From near-insolvency in 2022 to robust growth now, with big plans for the future. They cite projects in the pipeline (including a flashy ₹3,000 crore township on Dwarka Expressway), claim dominance in NCR markets, and showcase their massive land reserves. Unlisted shares of BPTP were even trading in the grey market at a hefty price (around ₹346/share) indicating some bullishness.

But behind the glossy prospectus lurks everything we’ve discussed. Can an IPO really wash it all away? BPTP seems to think so. The IPO, if successful, doesn’t just raise money – it legitimizes the company in a broader sense. Once listed, BPTP might hope that focus shifts to quarterly earnings and stock performance, rather than old legal cases. Public investors coming in at IPO are effectively providing exits to some existing stakeholders and certainly providing capital to handle those pesky stuck projects (finally). It’s like reputation laundering 101: take tainted past, add fresh public money, stir, and voila – you have a “clean,” rebranded entity marching into the future.

Of course, whether the public buys it is another matter. Regulators like SEBI will scrutinize the IPO disclosures. One would expect that all major risks – including the ED investigation, the hundreds of consumer cases, the potential liabilities – will have to be disclosed in the Red Herring Prospectus. If they are fully disclosed, it reads almost like a horror story in fine print.

If they try to minimize these, they risk regulatory ire or future class-action suits. SEBI, one hopes, will demand that the company settle at least the biggest issues before going public. There’s precedent – regulators have halted IPOs of companies with serious pending legal troubles. Will they here? Or will the IPO sail through in the exuberance of the market?

Market commentators have urged caution and vigilance. They argue SEBI should not allow this IPO without BPTP cleaning house: resolving the ED case, delivering or refunding in all those delayed projects, etc.. Listing a company with such legacy issues could erode trust in the markets if things go south, they warn. In other words, this IPO could be a trap for investors, passing BPTP’s time-bomb to the public.

BPTP’s take, undoubtedly, is different. They likely say: “We’ve endured and survived, which proves our resilience. Now we just need growth capital to finish everything and expand.” They might position Kabul Chawla in the background (perhaps officially he might step down from directorship if his legal issues are a problem, who knows) and let some professional front it. They’ll highlight those awards, the green projects, the thousands of happy customers (glossing over the unhappy ones). They’ll ride the current optimism in real estate. And if they price the IPO attractively, there will be takers – memories are short when there’s money to possibly be made.

In a story like this, one is tempted to say “And they all lived happily ever after (except the homebuyers)”. BPTP’s 180° turnaround from virtual collapse to a mega-IPO is nothing short of extraordinary; in the literal sense of beyond the ordinary. It reflects a “masterstroke” by the promoters in repackaging a troubled legacy into a narrative of redemption. If the IPO succeeds, it will validate, for better or worse, BPTP’s strategy of delay, deflect, settle, and re-emerge. It’s almost a textbook on how not to run a business ethically, yet still come out on top financially.

So, should we slow-clap or face-palm? Perhaps both. As a satirical salute, we acknowledge BPTP’s audacity. It cheated death (figuratively and, sadly, literally in one case), negotiated its way out of insolvency, kept the law at bay, courted the high life abroad, and never stopped hustling. And now it stands on the cusp of raising billions from the public. There’s a perverse punchline here: in a fair world, a company with BPTP’s record might be facing stern justice, not ringing the opening bell of a stock exchange. But in the real world, at least as of today, it’s the latter scenario that’s about to unfold.

In conclusion, BPTP’s saga is a cautionary tale wrapped in diplomatic humor. We’ve chronicled scams and scams-disguised-as-oopsies, but presented with a straight face. If BPTP indeed lists successfully, one might say the market has a short memory and an appetite for risk. If it fails or gets derailed by authorities stepping in at the eleventh hour, that too would speak volumes. Either way, the story isn’t over. For the thousands of long-suffering BPTP customers, an IPO isn’t the end of their woes – though it might offer a fresh avenue to pressure the company (as public shareholders can raise questions too). For new investors, caveat emptor – buyer beware – has never been more apt.

At the end, what we could see is BPTP’s Miracle; From Insolvency Papers to IPO Pamphlets in 36 Months…

BPTP’s journey from breakdown to bounce-back could be seen as an inspiration (of what to avoid). They demonstrated how to bungle almost everything and still land on their feet (for now). It’s almost comedic if it weren’t true. “Promoter integrity is the bedrock of investor trust. With warrants and probes hanging over Chawla, BPTP’s IPO is a red flag waving in the wind.”.

Take that as you will. The grand IPO will be the final test of whether this audacious rebranding gamble pays off. If it does, BPTP will have pulled off one of the most cynical yet successful reputation laundries in corporate India. And if it doesn’t, well, there’s always another last-minute settlement or two up their sleeve, presumably.