BPTP- An Empire Built On Hooda’s Midas Touch?

“The securities market is built on trust. When trust is violated, the market suffers.” Granting BPTP access to public funds without holding it accountable to its past is a sure-fire way to violate trust. Until BPTP truly rights its wrongs, its IPO indeed looks less like a legitimate capital raise and more like “a calculated scheme to offload liabilities onto public shareholders while promoters escape accountability.

IPO Dreams Built on Broken Promises: The BPTP Saga Unveiled

On a humid September afternoon in 2014, a crowd of retired military officers gathered at Jantar Mantar, New Delhi’s protest hotspot. They clutched property allotment papers and faded checks – proof of payments made nearly a decade earlier for dream homes that never materialized. These veterans were among 400 middle-class buyers who had paid almost 100% of the price for apartments in BPTP’s Park Serene project, only to watch the developer miss deadline after deadline. Their frustration was palpable as they accused BPTP Limited, once touted as a rising star in North India’s real estate, of swindling them of their life savings.

Meanwhile, over 7,000 miles away in New York City, BPTP’s founder Kabul Chawla enjoyed the comforts of a sprawling five-bedroom condominium overlooking Central Park. The posh pad, valued at roughly \$19 million, sat on the 68th floor of Manhattan’s Time Warner Center, cloaked behind a shell company with a Singapore address. Chawla publicly denied owning the luxury apartment, claiming it belonged to a cousin, but correspondence uncovered by The New York Times tied the property directly to him. The contrast could not be starker: as hundreds of Indian families paid EMIs for nonexistent homes, the man responsible was allegedly globe-trotting and luxuriating in ultra-prime real estate abroad.

Fast forward to today, January 2026, BPTP Ltd., the same developer mired in these unresolved grievances, is stealthily maneuvering toward a massive Initial Public Offering (IPO) of around ₹5,000 crore. In the glittering narrative pitched to investors, BPTP claims to be a “key player” in Delhi-NCR real estate with over 50 projects and a “purported delivery” of 24,500 units across 2,000 acres.

But behind the glossy prospectus lies a darker reality – a two-decade trail of fraud allegations, legal battles, and customer misery. This report delves into that reality with a blend of hard data and candid analysis. We chart BPTP’s explosive rise under political patronage, its pattern of harassing homebuyers with delayed or duplicitous dealings, and the yawning gap between its public claims and court-documented facts. Ultimately, we ask, Should India’s regulators reward such a track record with access to public money? Or put more bluntly, is BPTP’s upcoming IPO a legitimate business milestone, or a cynical ploy to offload a “toxic legacy” onto retail investors?

It all started with Haryana’s land boom during the Hooda’s Regime: A Story of Licenses, Land Banks, and Political Patronage

To understand BPTP’s meteoric rise, one must begin in the mid-2000s in Haryana – a period of breathtaking real estate free-for-all enabled by the state government. In March 2005, Bhupinder Singh Hooda took charge as Chief Minister of Haryana, and what followed was a licensing bonanza unprecedented in the state’s history.

Hooda, who personally oversaw the Town & Country Planning Department (TCP), approved real-estate development licenses for over 20,500 acres in Haryana within seven years, “an increase of almost 150% over the previous 23 years combined”. In Hooda’s eight-year tenure, 24,825 acres of land were licensed to private builders, compared to just 8,550 acres in the 23 years before him. He notified repeated revisions of city master plans and handed out licenses at such a pace that insiders likened it to a “license-issuing bonanza.”

Critically, Hooda lowered the bar for who could become a coloniser. In April 2007, his administration quietly amended eligibility rules so that even companies with zero real estate experience could obtain colony licenses, so long as they roped in any token “collaborator” who had one. This opened the floodgates for rank newcomers – including firms that had never built so much as a tool shed – to amass huge land banks on speculation.

“Hooda allocated licences to over 350 real estate firms of all sizes, most of which were unknown or had no experience whatsoever in property development,” adding that builders frantically bought up agricultural land in advance wherever they sniffed an upcoming master plan expansion. In effect, politically connected players were tipped off about future development zones and got rich flipping farmland into gold, often without yet building anything.

Amid this gold rush, the single largest beneficiary was an obscure Delhi builder named Countrywide Promoters, better known by its brand name, BPTP. According to official records, BPTP snagged roughly 1,635 acres of prime Haryana land under Hooda’s regime, the most among all developers. To put that in perspective, BPTP’s land acquisitions dwarfed those of established giants like DLF (568 acres) and Unitech (~830 acres) in the same period.

Yet, up till 2005 BPTP was virtually unheard of. The company had been incorporated back in 1996 (as Rainbow Promoters Pvt. Ltd.) by a then-29-year-old Kabul Chawla, operating out of a modest address on Najafgarh Road in Delhi. Chawla had no significant projects to his name; he certainly did not rank among Haryana’s traditional realty players. But Hooda’s ascent changed his fortunes overnight. Fueled by the Chief Minister’s seemingly limitless generosity with licenses, BPTP went from a no-name to a land baron in a span of just a few years. By 2011–12, BPTP was boasting a turnover of ₹1,400 crore and counting global investors like Citi, JP Morgan, and Blackstone as stakeholders.

The personal transformation of Kabul Chawla mirrored his company’s explosive growth. In less than a decade, Chawla leapt from middle-class obscurity to the ranks of the uber-rich. He moved into a sprawling bungalow on Delhi’s elite Amrita Shergill Marg – a property estimated at ₹300 crore in value. He also acquired a taste for overseas assets, including that $19 million Manhattan condo uncovered later.

Within industry circles, whispers spread that Chawla’s rise was no mere rags-to-riches tale, but one greased by political connections. Indeed, it emerged that Kabul Chawla had married into the family of another developer clan – the Tanejas of TDI Group, making him the literal “son-in-law” of Haryana’s real estate oligarchy. Familial ties and the Hooda government’s patronage provided the young BPTP with “insights and networks enabling its rapid growth”.

Hooda’s Midas touch didn’t just stop at doling out initial licenses, but his administration also bent rules to keep favoured builders afloat. For instance, licenses were routinely renewed even when developers failed to meet construction deadlines, allowing them to squat on land and flip plots at higher prices without delivering anything to end-buyers. Non-performing builders profiteered by squatting on a precious resource at the cost of the end-user, as one official put it.

In one illustrative case, BPTP was granted a license for ~14.8 acres in Gurgaon (Sector 106) in February 2008 despite the land being under a legal dispute. The original landowner, Surinder Pal Beniwal, had filed a formal complaint in 2007 that BPTP hadn’t paid him fully for the tract – prompting the Town & Country Planning (TCP) department to warn BPTP that any license would only be considered if the land was “free from all encumbrances.”

Yet just months later, the Hooda government issued BPTP the license for the encumbered land, and even renewed it subsequently, overlooking the fact that BPTP still had not obtained possession of the land or begun any construction. Such regulatory somersaults made a mockery of the rule of law. But they perfectly encapsulated the era’s ethos: if you had the right contacts, no obstacle – be it missing experience, pending payments, or even court cases – would hinder your land grab.

By 2009, BPTP’s swagger was on full display. The upstart developer stunned industry watchers by outbidding India’s biggest realty company, DLF, to win a high-profile Noida land auction for a record ₹5,000 crore. It was the largest single land deal in the country at the time. The audacity of a little-known firm beating a giant like DLF underscored just how turbocharged BPTP’s ambitions had become under Hooda’s patronage.

In hindsight, that Noida gamble proved too rich even for BPTP – the real estate market crashed soon after, and BPTP could only cough up money for 23 of the 95 acres it had bid on, eventually forfeiting much of the land. But the episode cemented Kabul Chawla’s image as a fearless high-roller in the property game.

Hooda, for his part, would later face his own reckoning. Multiple CBI investigations were opened into land deals during his tenure, including alleged scams in Manesar, Garhi Sampla, Gurgaon and elsewhere. The broad pattern in these cases: farmers were coerced to sell land cheap for “public purpose,” which was then licensed to private builders for windfall gains. Hooda’s name is now entwined with allegations of “persistent abuse of power” in Haryana land acquisition and release.

And at the center of many of those deals sits BPTP – the developer that Hooda’s decisions elevated from nothing into an empire. Behind BPTP’s Haryana land boom was indeed “the Midas touch of Hooda,” and everything BPTP touched thereafter has turned to…well, something far less golden for the common man.

Land of Broken Promises: Homebuyers at the Receiving End

If Hooda’s policies minted fortunes for BPTP, the flip side was experienced by thousands of ordinary homebuyers who invested in BPTP’s projects and spent the next decade trapped in a nightmare of delays and deceit. Nowhere is this more evident than in Faridabad’s sprawling Parklands project – BPTP’s flagship integrated township and the crown jewel of its Hooda-era land bank. Spread across approximately 1,700 acres, Parklands was launched with great fanfare in 2005-06.

By 2009, BPTP claimed it had pre-sold 10,685 apartments and 5,657 plots in Parklands, painting a vision of a vibrant city-within-a-city, complete with villas, high-rises, schools and shopping centers. But fast forward to the mid-2010s and that vision lay in shambles. BPTP’s Parklands became a “dystopia of vacant lots and half-finished structures,” as The New York Times memorably described it. A vast expanse of weed-choked plots and skeletal buildings greeted those who visited the site, instead of the thriving community BPTP had promised.

By 2015 – a full decade after launch – large portions of Parklands were still literally a jungle, lacking basic roads, electricity or water connections. The few towers that did get completed were isolated islands in a sea of unfulfilled plans.

How BPTP used legal techniques to fool the layman, non-lawyers, the homebuyers?

For the estimated 22,000 buyers who invested in various Parklands sub-projects, it has been a saga of unending agony. Consider the experience of Mr. Kanak Lal Mishra, one of Parklands’ early customers. Back in September 2005, Mishra paid ₹4 lakh by cheque as an advance to register for a 250-square-yard plot in Parklands. For three years, he heard little from BPTP.

Then, out of the blue in July 2008, he received an “Allotment-cum-Demand Letter” from BPTP offering him Plot No. X10-04, measuring 302 sq. yds. – significantly larger than what he had applied for. The catch? He was instructed to pay an extra ₹8.07 lakh within 15 days (and another ₹8 lakh within a month after that), or else his allotment would be cancelled.

The letter helpfully noted that “timely remittance of payments is the essence of the transaction,” warning that any delay would invite interest at a steep 18% per annum – and failure to pay altogether would result in cancellation “without any further notice,” forfeiting all his money.

Essentially, Mishra was being forced to pay for a bigger plot than he’d signed up for, on an impossibly tight schedule, under threat of forfeiture. BPTP’s demand letter ran many pages long, laden with legalese and one-sided clauses; the company’s buyer agreement is a tome of several hundred pages that few non-lawyers can decipher (it’s designed so that neither the broker nor the client can fully grasp its implications). Mishra somehow scraped together the funds and paid for the 302-yard plot. But his ordeal was just beginning.

In April 2009, BPTP sent another missive informing him that “due to changes in the layout plan,” his earlier allotment was being swapped to a different plot (No. LM2-45C) of 258 sq. yds. – smaller than the one he paid for. There was no offer to refund the difference in size. To add insult to injury, BPTP also levied enhanced External Development Charges (EDC) on all allottees when the Haryana government revised EDC rates – EDC more than doubled from ₹1,024/sq. yd. to about ₹2,400/sq. yd., a cost BPTP promptly passed to buyers like Mishra. Mishra paid that too.

And what does he have to show today, 17 years after his initial deposit? A paper allotment for a 258-yard plot in a deserted sector of Parklands where not a single brick has been laid by BPTP. His plot is literally a patch of dirt in the wilderness – unmarked, un-demarcated, un-serviced – unreachable by any proper road. BPTP has not even executed the final sale deed (registry) for his plot, meaning legally he doesn’t even own it yet despite paying nearly the full price and charges. The company, meanwhile, continues to hold his money.

Mishra’s story is distressingly common. Across BPTP’s projects, customers have alleged a consistent pattern of over-charging, under-delivering, and moving goalposts. Core grievances, as collated in thousands of complaints to consumer forums and regulators, include: collecting huge sums upfront without mandatory approvals in place, imposing arbitrary changes and fees after booking, delaying projects indefinitely under various pretexts, and refusing to refund buyers who sought to exit.

“Incomplete agreements, arbitrary delays, outright refund denials” – these issues began almost immediately after BPTP started selling properties around 2006 and have only snowballed since. The company’s mismanagement was so flagrant that by 2010-2011, even its deep-pocketed private equity investors (such as Citi and JP Morgan) accused BPTP of breaching commitments and took their dispute to arbitration. (BPTP ultimately had to sell a Gurgaon IT park in 2013 for ₹850 crore to buy out those peeved investors’ stakes.)

Let’s look at the scorecard of BPTP’s delivery (or lack thereof). In Parklands, which comprises multiple residential sub-projects, over 22,000 plotted and flat buyers are still awaiting possession as of 2025. Development in many sectors is years behind or completely stalled. In one segment called Park Elite, BPTP sold roughly 4,200 flats, but delivered only about 1,200 units – barely 28%.

Another much-hyped project, Discovery Park, launched around 2011, remains incomplete after 9–11 years, with buyers in limbo for over a decade. Even where construction finished, there were other let-downs: in Park Serene (Gurugram), BPTP delivered some towers but allegedly shrunk apartment sizes and altered layouts unilaterally, drawing ire from buyers. These shenanigans have led to a deluge of litigation.

Data from district consumer forums, state commissions, and the National Consumer Disputes Redressal Commission (NCDRC) show thousands of cases filed against BPTP over the past 10–15 years. Courts have repeatedly castigated the developer. For example, in Shahin Akhtar vs BPTP (2020), the forum lambasted BPTP for taking payments without executing timely buyer agreements or delivering possession. In Raghbir Singh vs BPTP (2021), a case involving BPTP’s Amstoria project in Gurugram, it was exposed that even premium-priced “luxury” plots were left barren and undeveloped for years. These judicial rebukes reinforce what homeowners have long said: BPTP’s promises were a mirage; what they got was a morass.

Regulators have started weighing in too. In a 2020 order, the NCDRC directed BPTP to refund ₹1.19 crore plus interest to a long-suffering homebuyer, calling the company’s conduct “gross negligence” in that project. More recently, in 2025, the Supreme Court of India – dealing with a batch of BPTP-related cases – observed that BPTP had engaged in unjust enrichment at the expense of homebuyers, by holding on to their money without delivering the properties or providing compensation.

Such a remark from the apex court is a withering indictment: it essentially labels BPTP’s business model as predatory. Even the Haryana Real Estate Regulatory Authority (RERA), set up in 2017 to protect buyers, has ruled against BPTP in several cases – ordering refunds with interest for delayed projects. (In other complaints, RERA controversially let BPTP escape on technicalities – for instance, rejecting compensation to buyers who took possession of substandard, delayed units on the logic that they had “occupied” them. But such half-victories are hardly vindication, as observers note.)

Beyond the courtroom, aggrieved buyers have taken to the streets and social media. As early as 2011, and then repeatedly in 2014 and 2015, large protests erupted in Faridabad and Delhi. In September 2014, it was the turn of those retired Army officers and their families – over 200 of them – rallying in public to demand justice for the delayed Park Serene apartments. They even appealed to the Army Chief for intervention, embarrassed that ex-servicemen were “reduced to dharna” for homes they paid for in full.

BPTP’s offices have been gheraoed by angry crowds on multiple occasions. In the age of Twitter (now X), these buyers have become unflinching whistleblowers: photos of waterlogged construction pits, videos of half-built flats with cracks, copies of police FIRs against the company, all circulate widely with hashtags calling BPTP a #RealEstateScam.

In one especially tragic incident in July 2024, a five-year-old child drowned in an open pit (a purported “swimming pool”) at a BPTP project that was left unguarded and half-finished, according to residents. The public outrage was swift – residents held candlelight vigils and demanded the arrest of Kabul Chawla and his site engineers for criminal negligence. It’s a grim measure of how badly things have gone wrong that buying a home from BPTP can literally be a life-threatening risk.

It would be unfair to say no progress has occurred. BPTP has indeed delivered some units and projects (often much delayed) and has tried to mollify customers with assurances. But even its rare successes are tainted by irregularities. For example, in 2016–17, BPTP hurriedly offered “possession” of some plots in Faridabad without paved roads or electricity, just to claim it had met a deadline – forcing gullible owners to build houses in the middle of what was effectively a construction site. These antics eventually drew the eye of insolvency courts.

By late 2022, BPTP’s financial strain led an operational creditor to drag it to the National Company Law Tribunal (NCLT), which admitted an insolvency resolution case. Panicked homebuyers flocked to that proceeding, fearing their claims would be buried. BPTP narrowly escaped a formal insolvency (the NCLAT stayed the process after BPTP struck a settlement with the creditor). But experts noted this was a warning flare: “a stayed CIRP (insolvency) postpones, not erases, liabilities,” one analyst said. In other words, BPTP’s house of cards was wobbling – and only an influx of funds or miracle in sales could shore it up.

The Promoter’s Shadow: Kabul Chawla and His Troubled Legacy

At the heart of BPTP’s saga is its founder and managing director, Mr. Kabul Chawla – a man hailed in glossy brochures as a visionary entrepreneur, but better known to law enforcement as an accused in myriad criminal cases. Chawla, now in his late 40s, cuts an enigmatic figure. He’s notoriously media-shy and seldom gives interviews (understandably so, given the questions he’d face). While company press releases portray him as an industry leader garlanded with awards – he was even made an “IGBC Fellow” in 2025 for contributions to green buildings – the reality is that Chawla has spent the past decade entangled in one legal quagmire after another.

Court records show Kabul Chawla is named in multiple FIRs (First Information Reports) alleging serious offenses. These include charges under IPC Section 420 (cheating), 406 (criminal breach of trust), 467–471 (forgery), and 120-B (criminal conspiracy). It is extraordinarily rare for the promoter of a once high-flying real estate company to face such accusations personally – and even rarer for the law to catch up. But in Chawla’s case, a non-bailable arrest warrant was indeed issued against him by a Delhi court in 2011, after investigators presented prima facie evidence of fraud in a case involving a BPTP project.

For a moment, it looked like Chawla might actually be put behind bars. Instead, according to media reports and Enforcement Directorate (ED) officials, Chawla opted for the tried-and-true tactic of the well-heeled Indian scamster: he left the country for long stretches. From about 2012 onward, Chawla has spent significant time abroad – allegedly shuttling between Dubai, London and New York – effectively dodging Indian authorities. Every time a court hearing neared or a protest swelled, he seemed to be conveniently “traveling” overseas. This pattern did not escape notice; it infuriated cheated homebuyers, who saw it as the act of a fugitive dodging accountability.

Chawla’s alleged modus operandi forms the template for BPTP’s troubles. Investigators say it boils down to misrepresentation and diversion: entice buyers with grandiose plans, collect large upfront payments even before securing mandatory approvals, and then stall the projects indefinitely while siphoning off the funds elsewhere.

In multiple cases under scrutiny, money trail analyses have suggested that crores collected for specific BPTP projects were routed to other ventures or shell companies, instead of being used to build the homes for which customers paid. This rob-Peter-to-pay-Paul strategy works until it doesn’t – eventually too many “Peters” (projects) are robbed and there aren’t enough new “Pauls” (buyers) to continue the jugglery. By 2019–20, BPTP was facing this reality as new sales dried up and old obligations mounted, pushing Chawla into a corner.

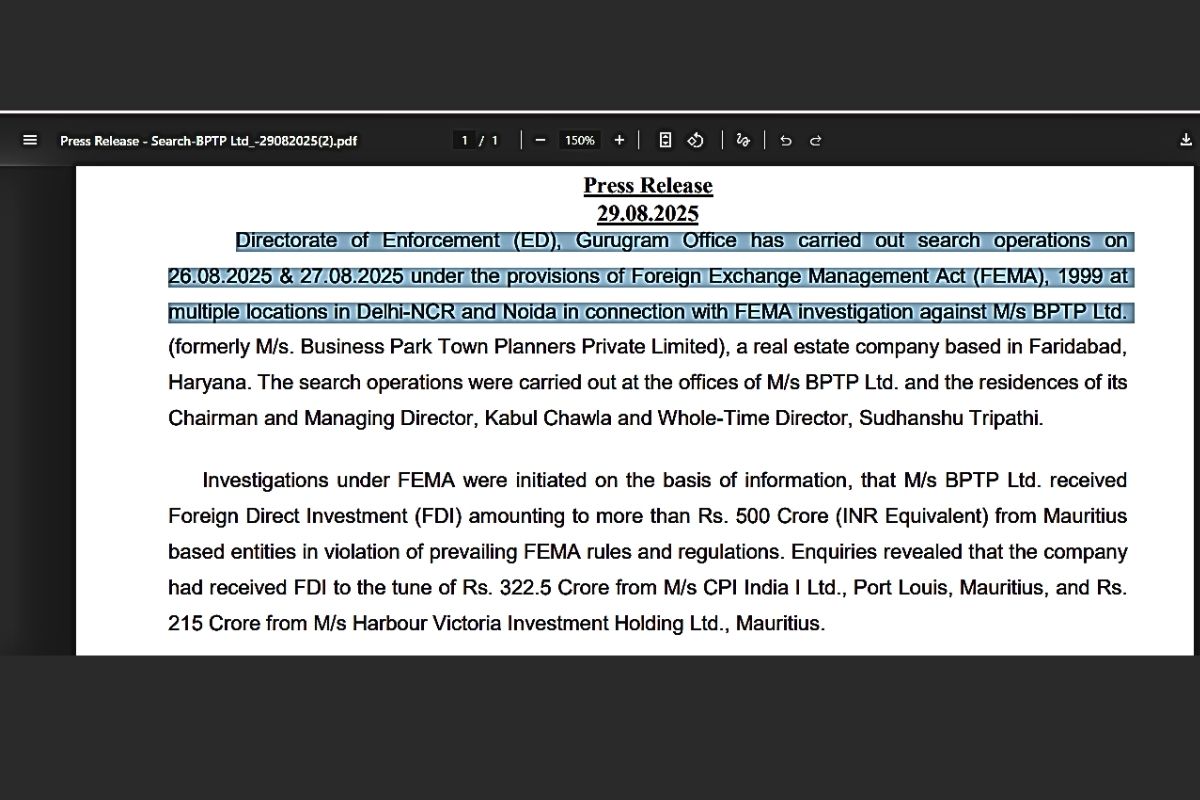

However, Kabul Chawla’s challenges aren’t limited to irate buyers and local police. India’s central financial crime agencies have also zeroed in on BPTP and Chawla for suspected money laundering and foreign exchange violations. In August 2025, the Enforcement Directorate (ED) conducted multi-city raids on BPTP’s offices and Chawla’s residences under the Foreign Exchange Management Act. This was a highly publicized operation: raids took place simultaneously in Delhi, Noida, Faridabad, and Gurugram, with officials seizing laptops, incriminating documents, and freezing several bank lockers.

The focus of the ED probe is explosive. ED alleges that BPTP brought in over ₹500 crore of foreign investment from Mauritius-based entities in 2007–08 in violation of RBI norms – using prohibited “put options” and other camouflage to guarantee those investors high returns. Essentially, BPTP is suspected of using offshore dummy corporations to funnel money into its projects (or perhaps into Chawla’s own pocket), bypassing regulations. One particularly intriguing thread the ED is tugging at: Chawla’s high-value property purchases abroad. They are examining whether the $19.4 million Manhattan condo was bought using siphoned funds from Indian homebuyers.

Recall that The New York Times expose in 2015 had already flagged this luxury apartment’s murky ownership structure and tied it to Chawla. The condo was held via an opaque Delaware LLC named “NYC Real Estate Opportunities” with links to Singapore – classic layering to hide the real owner. JPMorgan, one of BPTP’s early investors, was so alarmed by Chawla’s attempt to transfer that apartment that it went to a U.S. court to block him (they feared he was diverting assets).

Though JPMorgan’s lawsuit was dismissed on technical grounds, the Financial Express reported the whole saga, noting that Chawla’s denial of ownership rang hollow in face of broker emails tying him to the condo purchase. Now ED is investigating if buying that Manhattan trophy involved violating India’s foreign exchange laws or laundering unaccounted money.

Chawla, of course, insists he’s innocent of all these accusations. Through lawyers, he has sometimes claimed that project delays were beyond his control (blaming, for instance, government infrastructure not coming up, or economic slowdowns). BPTP’s official stance often casts itself as a victim of circumstances, and highlights whatever projects it has delivered.

The company also loves to cite awards and certifications it has received – like a LEED Platinum rating for a commercial project in Noida, or Chawla’s IGBC Fellow honor in 2025 – as proof that it is a credible, professional outfit. But these PR flourishes increasingly sound like a cruel joke to those on the ground. “These accolades ring hollow against the backdrop of unresolved cases,” an observer noted dryly. Or as a seasoned lawyer quipped, “Promoter integrity is the bedrock of investor trust. With warrants and probes hanging over Chawla, BPTP’s IPO is a red flag waving in the wind.”

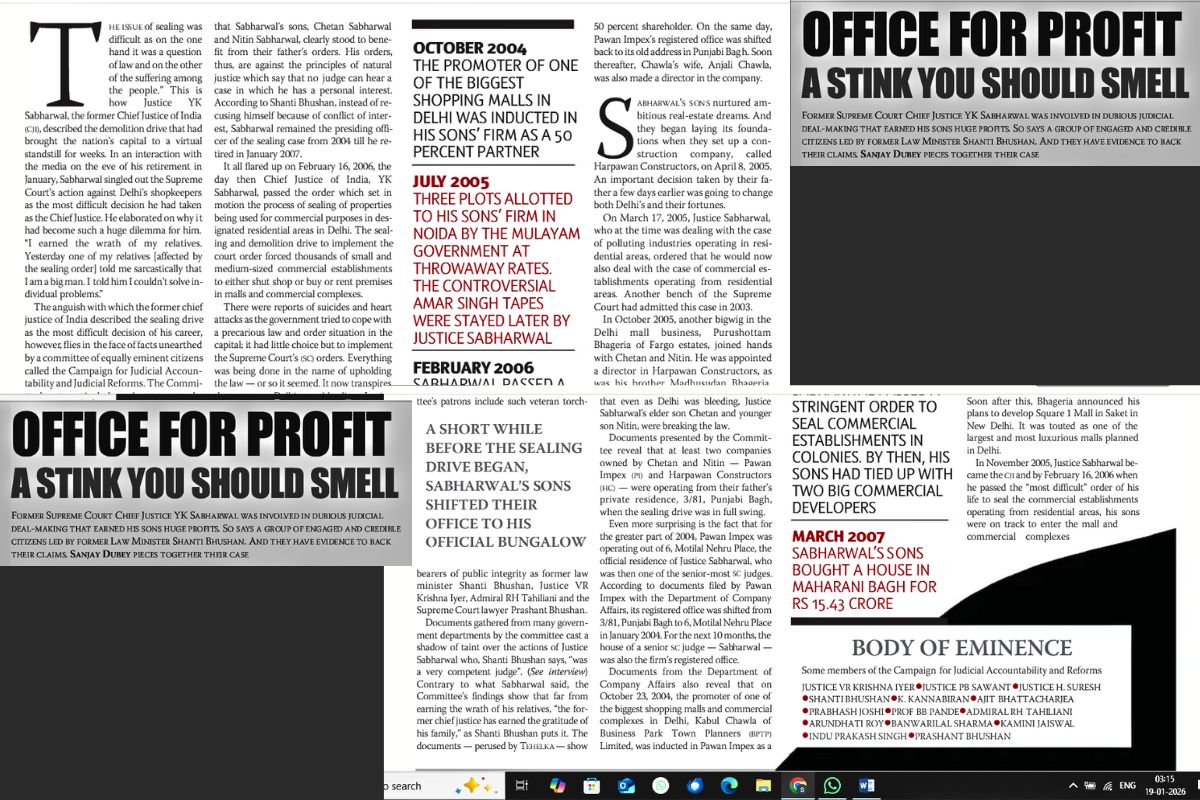

One more unsavory footnote in Chawla’s saga deserves mention. BPTP’s rise was not just aided by Hooda and the Tanejas; it also rubbed shoulders with the higher judiciary in ethically concerning ways. In 2007, a controversial land deal involving the sons of a then-sitting Chief Justice of India, Y.K. Sabharwal, had links to BPTP. Around the time Justice Sabharwal was adjudicating matters that affected real estate developers, his sons – through a maze of companies – ended up in possession of commercial space in a Delhi mall reportedly developed in collaboration with BPTP (then known as Business Park Town Planners).

This apparent conflict of interest was highlighted in the media as an example of judicial malfeasance and developer-politician nexus. While the scandal – dubbed “Sealgate” – faded without formal consequences, it reinforced the perception that Kabul Chawla had friends in very high places indeed. Little wonder that through the 2000s, nothing stuck to him: not complaints to police, not court orders, not media exposes. It is only in the past few years, as public outrage peaked and central agencies stepped in, that the accountability net seems to be tightening around Chawla and BPTP.

An IPO in Question: Can a Leopard Change Its Spots?

Given this damning track record, the obvious question is: How and why is BPTP now being allowed to tap the capital markets for a fresh ₹5,000 crore? The company’s IPO plan, if successful, would be one of the largest real estate public offerings in recent years. BPTP is hardly shy about its intentions – it has reportedly hired a cohort of investment bankers to prep the issue for 2026, and in stock market grey circles, unlisted BPTP shares were changing hands at around ₹340–350 recently, reflecting bullishness from some quarters.

The official rationale for the IPO sounds straightforward: BPTP claims it will use the funds to fuel new projects (they mention a big ₹3,000 crore project on Dwarka Expressway in Gurugram in the pipeline), to acquire more land, and to retire some debt. In other words, “Give us money so we can grow and also clean up our balance sheet.” This is the standard pitch any growing company makes to the public markets.

But let’s not be naive – there are many who suspect a more cynical motive. They argue that BPTP’s IPO is less about growth and more about providing an exit to its promoters and plugging the holes from past misadventures. Skeptics point out that BPTP nearly collapsed under insolvency proceedings in 2022, has “unfinished projects, pending FIRs, and ED probes” galore in 2023–24, and yet projects an image of resurgence. How? Possibly by painting an overly optimistic financial picture while sweeping its myriad contingencies under the rug.

There is a genuine fear that the IPO proceeds – instead of funding new development – will end up being used to quietly settle legal cases, pay off old creditors (maybe even pay fines if regulators impose them), and essentially bail out Kabul Chawla for his past mistakes. In blunt terms, new investors’ money might be used to fill the potholes that BPTP itself dug over the last 15 years, rather than to build shiny new highways of growth.

When BPTP attempted an IPO once before, in 2010, things didn’t go as planned. Chawla had filed for a ₹1,500 crore IPO in 2010 (for a 10-25% stake sale) and even obtained SEBI’s approval. But that issue was shelved at the last minute amid mounting complaints and market turmoil. The complaints referred to were likely the numerous fraud allegations surfacing by then – SEBI appears to have grown uncomfortable, and investors were not exactly queuing up to bankroll a scam-tainted builder. BPTP retreated, and as noted earlier, spent the next few years liquidating assets to pay off private investors who had initially bankrolled it.

Fifteen years later, the issues persist. It’s sobering that virtually nothing has changed on the ground between BPTP’s failed IPO of 2010 and its renewed IPO attempt in 2026, except perhaps the size of the offer (now more than triple). The homebuyers who were angry in 2010 are, if anything, angrier today. The undelivered projects from 2010 have multiplied in number. The criminal investigations, which had just begun nibbling at BPTP in 2010, have now dug their teeth in with full force. If BPTP was deemed too toxic for the market in 2010, why would it be palatable now?

This brings us to the role of the regulators – chiefly, the Securities and Exchange Board of India (SEBI). SEBI’s mandate is to protect investors and ensure fair, transparent functioning of the securities market. One might ask: Does SEBI scrutinize the track record and integrity of companies coming for IPOs, beyond just their balance sheets? The reality is that SEBI’s powers in this regard are somewhat limited. The regulations do require extensive disclosures: in its Draft Red Herring Prospectus (DRHP), BPTP will have to list all major pending litigations, regulatory actions, risk factors, etc.

And indeed, BPTP’s risk factor section could read like a thriller – pages of pending court cases, potential liabilities, and adverse findings. But disclosure is one thing; preventing dubious companies from accessing the market is another. Unless an entity or its directors have been convicted of serious fraud or declared willful defaulters (or unless the company’s financials violate certain thresholds), SEBI doesn’t outright bar them from listing. The onus is largely on investors to read the fine print and decide. This is a caveat emptor (buyer beware) model. And it’s a model that can fail spectacularly when retail investors, lured by glossy advertisements and big IPO hype, either don’t see or don’t understand the red flags buried in prospectuses.

SEBI itself seems aware of this dilemma. In January 2026, SEBI’s chairman Tuhin Kanta Pandey publicly flagged “persistent disclosure gaps” in IPO offer documents across the board. He admonished merchant bankers – calling them the “gatekeepers of transparency” – for not doing enough independent due diligence and relying too much on what the issuer companies tell them.

In the context of a company like BPTP, this warning is extremely apt: the risk factors and liabilities may be so complex and voluminous that there’s a real fear not all of it will be adequately disclosed or explained in the IPO documents. For instance, if ED’s probe is ongoing, BPTP must disclose that – but can it reasonably quantify the risk of a potential money-laundering charge or asset attachment? It might downplay it as “routine investigation” in the prospectus, whereas the actual risk is enormous (ED could, say, attach BPTP’s unsold inventory or bank accounts, crippling its operations).

SEBI has promised to intervene in IPOs if there is “serious misrepresentation or a clear breach of regulatory requirements”. Allowing BPTP to sail through would test that promise. If BPTP isn’t a clear case of “high risk, handle with care,” then what is?

Those bullish on BPTP’s IPO will argue that the company has “cleaned up its act” in recent years – that it completed some stalled projects, settled some disputes, and now has a “robust pipeline” for growth. Indeed, BPTP’s marketing machine is likely to trumpet a recovery story: e.g., home sales picking up post-pandemic, improved revenue in 2023, big new plans in Gurgaon and Noida, etc. They will try to shift focus to the future, glossing over the past as legacy issues.

But this is where investors must not lose sight of corporate governance and promoter integrity. As an equity holder, you’re not just betting on assets and projects; you’re betting on the people running the show to be honest stewards of your capital. Does BPTP’s leadership deserve that confidence? The record says otherwise.

A company that has scammed and defrauded thousands of its own customers – those who provided it interest-free money by booking properties – can hardly be expected to suddenly become a paragon of virtue to its shareholders. In fact, one might worry that an infusion of IPO funds could simply enable a larger scam – perhaps allowing the promoter to cash out or divert funds under the guise of new projects, leaving public investors holding worthless paper if things implode.

Multiple industry experts have called for SEBI to take a much tougher stance in cases like BPTP’s. Some suggest that SEBI should delay or deny clearance for the IPO until BPTP demonstrates real resolution of its pending issues – for example, completing a certain percentage of delayed projects, or settling a majority of consumer cases, or until the ED investigation reaches a conclusion. Otherwise, allowing the IPO “as-is” effectively lets the promoters offload their problems to the public.

Remember, an IPO also typically means partial exit for existing investors; it wouldn’t be surprising if some of BPTP’s early investors or even the promoter look to dilute their holdings in the offer. If those shares get picked up by retail investors who are unaware of the backstory, it would be the classic “greater fool” scenario – the public as the sucker at the poker table. One scathing commentary went so far as to say: “BPTP’s IPO isn’t an opportunity – it’s a trap. Public shareholders deserve better than to inherit a conspiracy of deceit.” Strong words, but fitting for a company that has arguably become synonymous with real estate malfeasance in Haryana.

Finally, let’s consider the worst-case outcomes. What if BPTP lists on the stock exchange and then the hammer falls? The ED could file a chargesheet and attach properties for money laundering; a court could order hefty damages in a class-action suit; a key project might be canceled due to regulatory lapses – any of these events could tank the stock. One analyst cautions that adverse findings post-IPO could trigger asset attachments, share price collapse, and even trading halts – “wiping out investor wealth overnight.”

This is not idle speculation; we’ve seen similar scenarios. Think of realty firms like Unitech and HDIL, where post-listing fraud revelations destroyed shareholder value. Or the case of DLF, which did list successfully in 2007 but later got penalized by SEBI for hiding key information (resulting in a 3-year ban from capital markets for DLF in 2014). If a blue-chip like DLF wasn’t above board in disclosures, can we realistically expect BPTP – with its far murkier baggage – to offer full candor?

The Bottom Line: A Test for SEBI and a Warning for Investors

BPTP’s imminent IPO is shaping up to be a litmus test for regulatory vigilance and investor awareness in India’s markets. On paper, our system leans on disclosure: SEBI will ask BPTP to enumerate its risk factors and ongoing cases, and if those are disclosed, the company technically meets the requirements to list. But paper compliance isn’t enough when a company’s entire history is a red flag. Regulators would be wise to demand ironclad resolutions to the major issues before green-lighting BPTP.

That means, ideally, closing the ED probe (one way or another), settling the bulk of consumer disputes, and committing to a court-supervised plan for completing pending projects. If BPTP cannot demonstrate these, proceeding with the IPO could gravely erode market trust – it would be akin to knowingly allowing a likely debacle. SEBI in the past has taken a firm stand by rejecting or delaying IPOs for lesser concerns; here we have serious allegations of fraud and public harm. The onus is on the regulator to show that the capital market is not a haven for whitewashing corporate sins.

For investors, the advice is straightforward: exercise extreme caution. Don’t get blinded by the glossy brochures of BPTP’s “NCR dominance” or its ambitious new project announcements. Those mean little when the company’s legacy is littered with broken promises. Read the fine print of the prospectus when it comes – the sections detailing legal proceedings and outstanding liabilities.

If ever there was an IPO where those risk factors aren’t boilerplate, it’s this one. Ask yourself: do you want to be a shareholder in a business that has arguably treated its own customers with such contempt? Keep in mind that shareholders rank even below customers in many ways – if homebuyers struggled to get refunds, shareholders will likely have zero recourse if things go south.

To put it in perspective, investing in BPTP now would be betting that a leopard can change its spots. Could it happen? Possibly – under new management, with sweeping reforms, anything’s possible. But no such change has visibly occurred at BPTP. The same promoter, the same culture, and the same problems persist. A fresh coat of paint via IPO won’t change the structure underneath.

One might recall the proverb: “Fool me once, shame on you; fool me twice, shame on me.” Thousands of homebuyers were fooled once by BPTP’s sales pitch – many of them bitterly regret it. If today’s investors let themselves be wooed by the second coming of that pitch, despite all the warnings writ large, the shame (and loss) will be entirely theirs.

In summary, BPTP’s story is a microcosm of everything that can go wrong in Indian real estate – venal politicians, compliant bureaucrats, fly-by-night developers, hapless consumers, and lax regulators – and now this toxic cocktail is being offered as a premium stock to the public.

The Securities Appellate Tribunal once observed in a case, “The securities market is built on trust. When trust is violated, the market suffers.” Granting BPTP access to public funds without holding it accountable to its past is a sure-fire way to violate trust. Until BPTP truly rights its wrongs, its IPO indeed looks less like a legitimate capital raise and more like “a calculated scheme to offload liabilities onto public shareholders while promoters escape accountability,” as one investigative report aptly put it.

Let the buyer – and the regulator – beware.