Financial Terror: How Hero Fincorp Harasses Their Customers?

When Lenders Become Predators: Hero FinCorp's Shocking Record of Customer Harassment

Have you ever heard the saying “a friend in need is a friend indeed”? Hero FinCorp clearly did not get that memo whatsoever. Instead, this non-banking financial company (NBFC) has a knack for taking advantage of customers when they are weakest, making small issues of payment into enormous legal pitfalls. What is first a mere loan application ultimately becomes into an amalgamation of aggressive methods, intimidation, and monetary coercion which leaves the borrowers gasping with terror!

Let’s learn one situation which is becoming a common trend in India. Think of having a clean payment history for months, always paying the EMIs promptly. Life runs smoothly. Suddenly, something goes wrong, a health emergency, a job loss, or some financial problem; and one payment is skipped. No problem, right? You’ll resume next month. But not if you ask Hero FinCorp. In their calculation, one mistake gives them the right to use all their collection tools to harass the customers.

How Hero Fincorp Harasses Their Customers?

The business model of the company is similar to that of a standard loan shark’s playbook, but with a suit and tie. They accept post-dated or blank cheques during the time of the loan, something which appears to be a standard precautionary measure; but these cheques become instruments quickly when the company decides to deposit them after a default in payment. When these cheques bounce (since if you were unable to pay the EMI, your account is probably not carrying enough money to honour the cheque amount), you are suddenly confronted with serious legal troubles under Section 138 of the Negotiable Instruments Act. A simple financial problem becomes a huge legal hassle that can destroy your financial future.

The case summary.

A customer took a loan from Hero FinCorp, a NBFC. Throughout the loan tenure, the customer maintained an excellent repayment track record, consistently paying all EMIs on or before the due date.

However, on one helpless situation, the customer missed a single EMI due to unforeseen circumstances. Despite having a clean repayment history, the NBFC, Hero FinCorp responded aggressively by presenting post-dated cheques previously collected from the customer (a common practice for security purposes). Unfortunately, the cheque(s) bounced, possibly due to insufficient balance or timing issues, which is a technical violation under the Negotiable Instruments Act.

Following the bounced cheques, the company initiated legal action or a penalty process, reportedly of a significant amount (running into lakhs of rupees). The customer, wanting to resolve the matter responsibly, immediately:

- Paid the penalty interest or “action initiation charges” levied by the company.

- Continued paying the remaining EMIs without default.

Despite fulfilling all financial obligations including the missed EMI, subsequent payments, and penalties, the company has not withdrawn the legal case or closed the initiated action. As a result, the customer continues to face unwarranted legal pressure and emotional stress, even though he has cleared all dues.

This is not an isolated incident or a mistake. There is a startling trend when you read complaints from customers on various websites where Hero Fincorp Had Harassed Their Customers!

Social media, customer forums, and court hearings all paint the same picture: a financial institution more concerned with fines and lawsuits than assisting customers with short-term problems.

Hero FinCorp’s offenses are a laundry list of predatory lending tactics. At the top of the list is the misuse of those blank cheques or post-dated cheques. Customers claim that they signed these cheques during the loan paperwork process without knowing how they would come back to haunt them in the future. When payments are missed, even temporarily, these cheques are cashed in full without notice. When they bounce, legal notices come in rapid motion.

And then there’s the question of over-the-top reactions. Several borrowers have been surprised at how Hero FinCorp leaps to court action over one late payment, even for customers who otherwise have perfect payment history. It’s like killing a fly with a sledgehammer, absolutely unnecessary and apparently done to frighten, not to settle.

One of the most problematic events is the intimidation tactics reported. Many customers said that Hero FinCorp uses bullying recovery agents who crosses the line of ethics and possibly the laws. These agents reportedly appear at workplaces and residences unexpectedly, embarrassing borrowers. Some customers have complained of aggressive actions, harassment of relatives, and threatening words. Picture explaining to your elderly parents or children why there are strangers at your home threatening you over a bill that is already being worked on.

Even after settling all that they owe, along with any penalty by the company, several assert that Hero FinCorp never stops legal actions. Therefore, the borrowers still have court cases and poor credit history even after settling what they owe. It is like paying back a loan and finding that you are still considered a defaulter, this is a harsh situation that could haunt customers for decades.

Hero FinCorp’s charges are unclear. Customers typically complain of stealthy charges, abrupt rate of interest fluctuations, and obtusely unclear penalties. When asked questions about such, borrowers usually receive an evasive reply that things are “as per company policy”, a reply that does little to explain things.

Individual cases document these alarming practices. For example, there is a case where Mr. Rajesh Kumar lodged a complaint against Hero FinCorp. In his complaint, the company took ₹40,000 from his bank account using his blank signed cheques without his consent. Although this complaint was rejected since there was no adequate evidence, it is in line with a pattern of complaints lodged by many other customers.

Another example is in the case of Synco Industries Ltd. They complained that Hero FinCorp was exploiting its market position. They complained that Hero FinCorp was not reducing interest rates when the RBI reduced rates and was charging unwarranted charges. The Competition Commission of India dismissed this complaint on technical grounds. They said Hero FinCorp was not in a dominant market position. Nevertheless, the allegations do capture the typical issues customers face.

In a deeply disturbing case, a person in reddit reported that he discovered a Hero FinCorp bike loan in their CIBIL report, a loan he never borrowed. They visited the Hero agency to get the issue resolved, but they were unable to obtain any details about this bizarre loan that was killing their credit score. Just think how irritating it is to be penalized for failure to pay a loan you never borrowed!

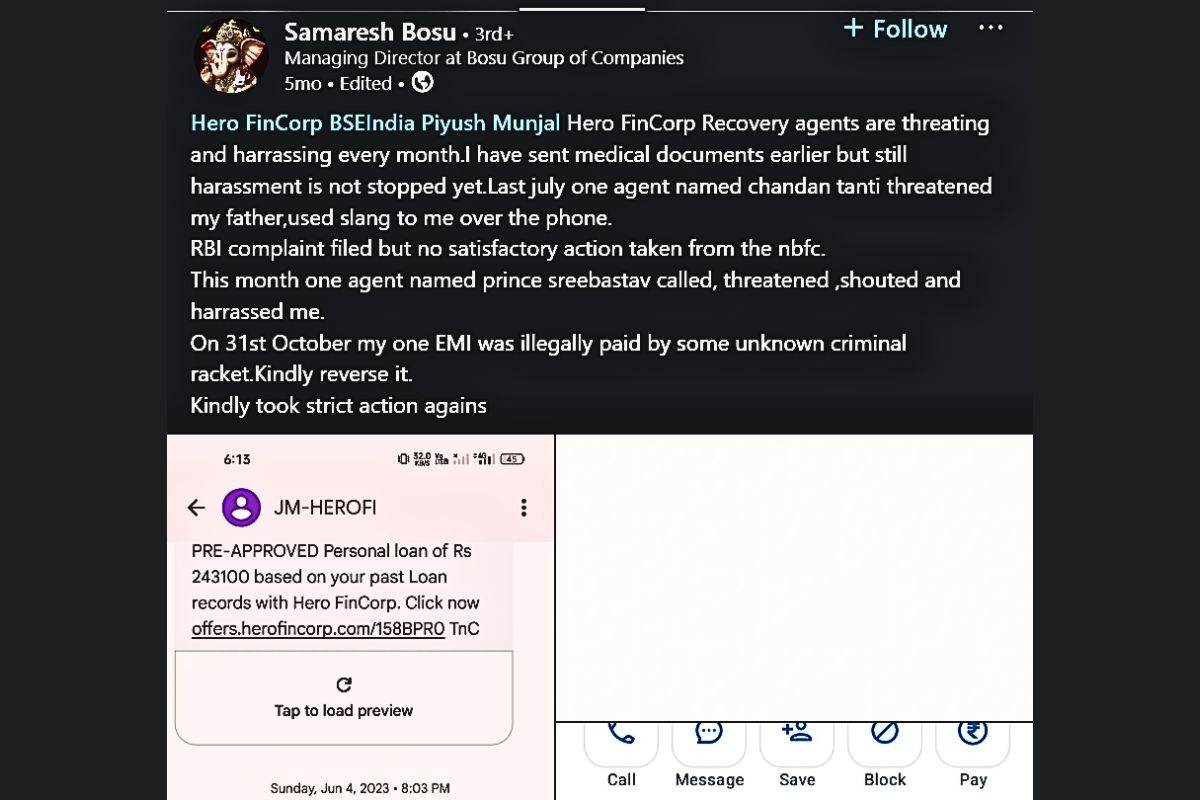

One of the borrowers in linkedin alleged that Hero FinCorp recovery agents were harassing and threatening them and their relatives despite the customer having submitted medical reports justifying their temporary inability to repay. This borrower resorted to the extent of filing a complaint with the RBI, but complained of receiving no satisfactory response.

Stained family ties.

It’s also to be noted that these practices are not in isolation. Hero FinCorp is a part of the Hero Group, and while the companies are separate, they have familial leadership connections. Abhimanyu Munjal, the CEO of Hero FinCorp, is actually the nephew of Pawan Munjal, Chairman and Managing Director of Hero MotoCorp. This connection turns out to be especially interesting in the context of the August 2023 searches by the Enforcement Directorate at the home of Pawan Munjal in the background of a case under the Prevention of Money Laundering Act. These searches were said to have been launched after the Directorate of Revenue Intelligence arrested a close associate of Pawan Munjal in possession of undeclared foreign currency.

This family connection does not necessarily imply Hero FinCorp was at fault, but it definitely makes one question the corporate culture and values of the broader Hero Group. If the top brass of a big company is under intense scrutiny, one can’t help but wonder if the same bad habits were perhaps prevalent in the rest of the company too.

The worst thing about these charges isn’t so much the individual behavior being alleged, but what they indicate about Hero FinCorp’s basic style of interacting with customers. Instead of treating borrowers as customers to be nurtured in hard times, the company seems to view repayment difficulties as a chance to make extra cash in the way of fines and litigation. This hard-nosed, business-oriented approach is not at all the company’s promotional materials and public image, which likely celebrate customer satisfaction and good customer service.

If you are thinking of taking loans from Hero FinCorp or any other lender, such complaints lead you to read the fine print, understand all the terms and conditions, and check the credibility of the lender in detail. It is especially important to understand how post-dated cheques can be used and what are the procedures for dealing with payment problems.

If you find yourself in the same situation with Hero FinCorp or such lenders, it is extremely important that you take a lawyer on board and document all your transactions. Knowing your rights as a borrower can keep the pressure tactics at bay, and making formal complaints to regulatory agencies like the RBI can work sometimes, although the process can be infuriatingly slow.

The primary issue here is regarding regulations for NBFCs in India. The RBI has regulations regarding fair practices by lenders, such as regulations regarding how they are allowed to raise money. But these regulations are not always obeyed. Stronger regulation and stricter punishments for violating regulations may help to curtail some of the rough tactics that firms like Hero FinCorp are accused of employing.

As the Indian financial sector grows and develops, consumer protection must grow with it. The power imbalance between giant financial institutions and individual consumers makes strong consumer protections not only a good idea, but a required one. Without them, the promise of increased financial inclusion through NBFCs might become a vehicle for financially vulnerable consumers to be taken advantage of.

The next time you consider borrowing from Hero FinCorp or any other such company, remember that the friendly loan officer might not be so friendly if you fail to make payments. As the saying goes, “The devil is in the details”, and in lending contracts, those details can turn a handy financial instrument into a fatal trap.