Why BPTP IPO Will Wipe Out Entire Investments Of The Investors?

Why Doesn't SEBI Investigate Companies Thoroughly Before Permitting an IPO?

In the bustling real estate landscape of India’s National Capital Region (NCR), BPTP Limited has long positioned itself as a major player, boasting ambitious township developments and a sprawling land bank. Founded in 2003 as “Business Park Town Planners Limited” and rebranded to BPTP in 2006, the company has navigated through boom cycles, regulatory hurdles, and market volatility.

Now, as of January 2026, BPTP is gearing up for what could be one of the largest real estate IPOs in recent years, aiming to raise between Rs 5,000 crore and Rs 10,000 crore. According to recent reports, the company has begun appointing merchant bankers and is targeting a listing in FY26 or FY27, with unlisted shares currently trading at Rs 346 per share. This move comes amid projections of revenue growth from Rs 3,000 crore in FY23 to Rs 5,500 crore in FY24, backed by a 45-50 million square feet land bank and plans for annual launches worth Rs 10,000 crore.

On the surface, this IPO appears as a golden opportunity for investors to tap into India’s thriving real estate sector, fueled by infrastructure pushes like the Dwarka Expressway and urban expansion in Gurgaon, Faridabad, and Noida. However, a deeper dive reveals a company riddled with historical scandals, ongoing regulatory probes, financial inconsistencies, and a promoter with a controversial track record.

Drawing from BPTP’s 2010 Draft Red Herring Prospectus (DRHP)—which led to a failed IPO attempt—and recent developments like Enforcement Directorate (ED) raids in 2025, this article argues that the upcoming BPTP IPO is not a pathway to prosperity but a potential trap designed to offload liabilities onto unsuspecting retail investors. With a pattern of disputes, fraud allegations, and unresolved litigations, participating in this IPO could result in total investment wipeouts, echoing the fates of overhyped debuts like Paytm.

This analysis is critical and analytical, dissecting BPTP’s operations through the lens of its own disclosures, court records, media reports, and market sentiments from platforms like X (formerly Twitter). We’ll explore the company’s troubled past, current controversies, financial red flags, promoter issues, and parallels to infamous IPO failures. By the end, it becomes evident why BPTP’s market entry could spell disaster for investors.

BPTP’s Troubled Past: Lessons from the 2010 DRHP

BPTP’s first brush with public markets came in 2010, when it filed a DRHP for a Rs 15,000 million IPO. The document, spanning 624 pages, was meant to showcase a robust real estate developer with a focus on NCR townships. Instead, it inadvertently highlighted a company fraught with operational risks, legal entanglements, and financial vulnerabilities—issues that have persisted and amplified over 15 years.

The “Outstanding Litigation and Material Developments” section (pages 258-320) alone paints a damning picture: over 300 cases against BPTP, its directors, and promoter group entities. These include 18 criminal cases involving cheating, forgery, and criminal breach of trust under IPC Sections 420, 467, and 468. For instance, a Faridabad landowner accused promoter Kabul Chawla of forging documents for 50 acres (page 273), leading to a 2011 FIR and non-bailable warrants—Chawla reportedly fled to the US.

Multiple homebuyer complaints alleged non-delivery of flats in Gurgaon projects like Sector 57, resulting in cheating charges (pages 258-265). Civil suits numbered over 50, focusing on specific performance and land disputes, such as unpaid considerations in Faridabad (pages 267-270), with one demanding Rs 100 million in damages.

Tax proceedings added another layer: 20+ cases with income tax authorities, including appeals on undisclosed income and misclassified deferred tax liabilities (pages 320-325, 301). Consumer disputes exceeded 100, centered on delayed possession and deficient services in projects like Parklands (Faridabad) and Park Serene (Gurgaon), with aggregate claims surpassing Rs 500 million (pages 280-290). Buyers in Sector 57 claimed non-refund of advances despite cancellations. Environmental violations included notices for Aravalli construction without clearances, leading to Rs 2 crore fines (later quashed in 2025 by the High Court, but procedural lapses noted) (pages 421-424).

Discrepancies in litigation disclosure were glaring. The DRHP classified many cases as “not material” without clear criteria, dismissing Rs 200 million in consumer claims as minor (page 258)—underplaying cumulative risks. A stark contradiction: Page 199 claimed “no outstanding litigation against the Promoter,” yet page 206 listed cases against Chawla. This high volume of land disputes suggests aggressive acquisition tactics, often involving incomplete payments or title flaws, echoing in later ED raids.

Financial sections (F-1+ and MD&A, pages 222-245) revealed further cracks. BPTP reported a FY2009 loss of Rs 879.74 million after FY2008 profits of Rs 2,164.85 million, amid the global downturn. Reclassifications and adjustments (pages 301-305) were rampant: Rs 24 million bank loans misclassified as unsecured in FY2005; deferred tax liability (Rs 13.21 million in FY2008) wrongly under current liabilities; license fees shifted from inventory to advances, inflating assets. Prior period errors, like government dues (Rs 24.07 million) netted incorrectly, indicated weak internal controls. Exceptional items included a Rs 2,141.19 million Noida project loss, blamed on “force majeure” but admitted as market-driven—contradicting “robust cash flows” claims (page 222).

Contingent liabilities stood at Rs 1,228.98 million in guarantees for subsidiary Vital Construction (page 302), with opaque tax impacts. Related-party transactions (pages 220-221, 307-320) were extensive: Rs 10,651 million advances to group companies like BPTP International Trade Centre, with directors holding positions in 50+ entities (page 220). This raised arm’s-length concerns, especially since Kabul Chawla controlled 99%+ in many. The MD&A claimed “no material impact,” but financials showed Rs 1,000 million+ in loans—a clear contradiction. Indebtedness reached Rs 10,660 million (FY2009) with 18% interest rates, relying on short-term debt (Rs 383.69 million) for land acquisition—risky in downturns.

Corporate structure loopholes abounded: Promoter group overlap with 56 entities (page 190), many in real estate, contradicting “no common pursuits” (page 220). Land reserves were 15.26% under agreements to sell (page 307), with unquantified title risks—contradicting “strategic acquisitions” (page 126) amid Noida losses. The history section (pages 126-165) claimed a “clean” record, but litigations begged to differ. The 2010 IPO ultimately failed amid these scandals and market conditions, setting a precedent for skepticism.

These 2010 revelations weren’t isolated; they’ve festered, manifesting in buyer protests and regulatory scrutiny. As one X post from 2025 noted, “BPTP IPO Faces Severe Allegations of Fraud; Investor Caution Advised” (Score: -80). This historical baggage alone should deter investors from the 2026 IPO.

Ongoing Scandals: From ED Raids to Fraud Probes

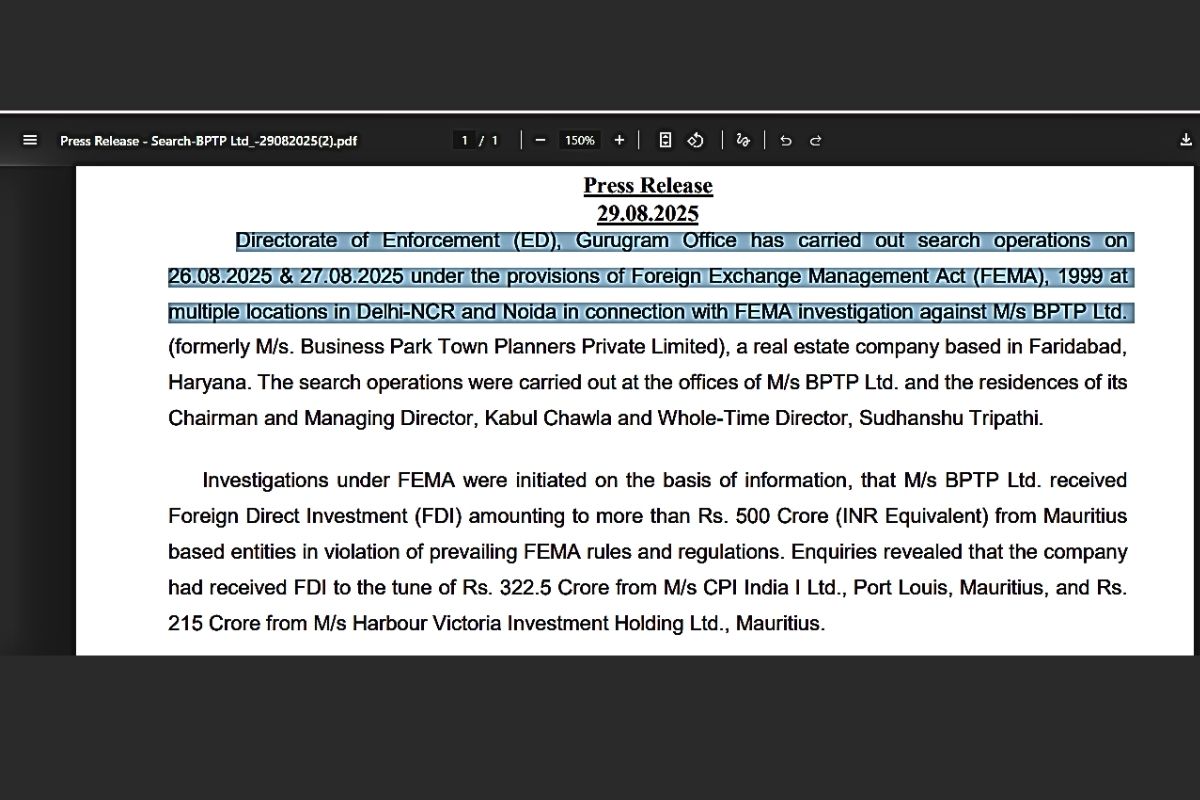

Fast-forward to 2025-2026, and BPTP’s issues have escalated into full-blown crises. The most damning is the August 2025 ED raids across Delhi-NCR offices and Chawla’s residences, probing Rs 500 crore FEMA violations involving Mauritius FDI with illegal “put/swap” options. Chawla is accused of being the beneficial owner of foreign entities, using diverted funds for a Rs 236 crore New York property. Documents were seized, linking to bank fraud and incomplete projects like Park Serene and Parklands. This echoes the 2010 DRHP’s Noida loss, potentially FDI-related.

Bank fraud FIRs from 2021-2025 total Rs 350 crore with PNB and others, alleging fund diversion. Customer protests persist: Thousands affected by 10+ year delays in Parklands (Faridabad), with X users calling it a “nightmare” and “fraudulent bills” (e.g., Rs 1 lakh for roads). Supreme Court and NCDRC have mandated refunds in 2022-2025, while insolvency petitions were stayed after settlements.

Environmental penalties include Rs 2 crore for Aravalli violations (quashed in 2025), but sewage issues linger. PMLA cases attached Rs 45 crore assets in 2024. Family ties to TDI (similar scams) compound suspicions. Inventiva labeled the IPO a “systematic conspiracy to defraud investors,” highlighting the “never-ending saga” of protests and delays.

Market sentiment on X is wary: Posts warn of “fraud” and “scam,” with one stating “BPTP IPO scam or fraud” amid broader IPO skepticism. Credit ratings reflect moderate risk (A3, 4% default probability as of Jan 2026), citing execution risks on projects like the Rs 6,000 crore Dwarka Expressway.

These scandals suggest BPTP is using the IPO to escape scrutiny, not build value. Investors risk entanglement in ongoing probes.

Financial Red Flags: A House of Cards

BPTP’s financials remain precarious. The 2010 DRHP exposed reclassifications masking weaknesses, like misclassified loans and inflated assets. Today, with debt burdens and related-party exposures, the story hasn’t changed. High-interest debts (18% in 2010) persist, with reliance on short-term funding for land—vulnerable to rate hikes.

Related-party transactions hint at siphoning: Advances to group entities controlled by Chawla raise conflict concerns. Contingent liabilities and unprovisioned risks (e.g., IT searches) understate dangers. Revenue projections (Rs 10,000 crore annual) seem optimistic amid NCR price peaks and cyclical risks.

Overvaluation looms: At Rs 346 unlisted, the IPO could price at premiums ignoring fundamentals. Like 2010’s “robust” claims amid losses, current hype ignores realities.

Promoter Issues: Kabul Chawla’s Shadowy Legacy

At the helm is Kabul Chawla, facing 6+ criminal cases in 2010 (forgery, cheating) and central to 2025 ED probes. His flight post-2011 FIR and foreign assets (NYC property) scream red flags. Promoter group overlaps (56 entities) enable fund flows, contradicting non-compete claims.

Chawla’s leadership has overseen delays, protests, and violations—hardly inspiring confidence. Investors betting on BPTP are essentially betting on him, a risky proposition.

Lessons from Past Failed IPOs: The Paytm Parallel

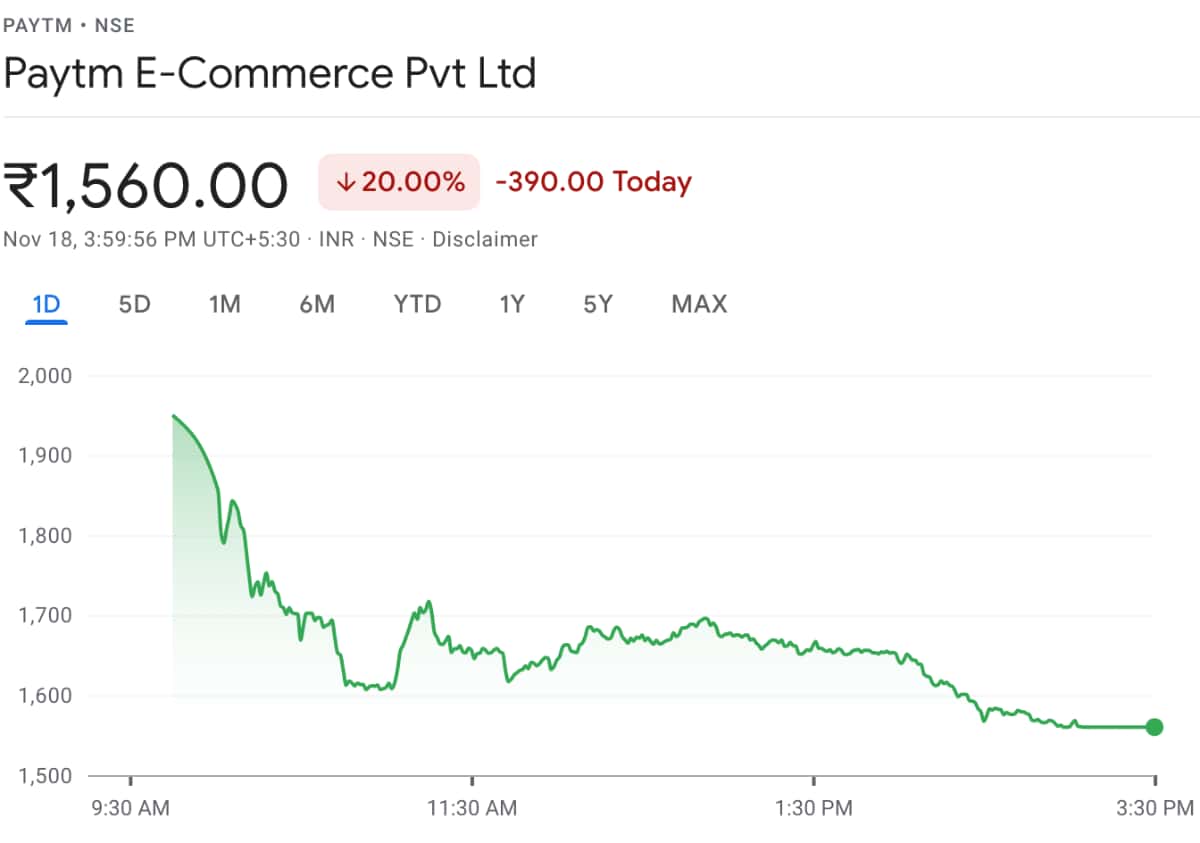

BPTP’s trajectory mirrors overhyped IPOs that crashed spectacularly. Take Paytm (One97 Communications), India’s largest IPO at Rs 18,300 crore in 2021. It debuted at a 9% discount, crashing 27% on day one to Rs 1,564 from Rs 2,150— the biggest listing-day loss in a decade. Shares have since fallen 80%, wiping $2.4 billion in market cap, leaving it at $3.3 billion by 2024.

Reasons: High valuation (45x sales), persistent losses, no clear profitability path, and fierce competition from Google, Flipkart. Hype lured retail investors, but reality bit: MDR rumors caused further 10% drops in 2025. Analysts cited “lack of focus” and “growth-at-all-costs.”

Similar to BPTP: Overhyped amid scandals, losses, and competition. Other examples include LIC’s 2022 IPO (crashed post-listing) and Zomato’s initial volatility, but Paytm exemplifies retail wipeouts from inflated valuations.

Why BPTP IPO is a Trap: Analytical Risks

BPTP’s IPO risks total investor wipeouts due to:

- Overvaluation: Priced on hype, ignoring litigations and probes.

- Market Timing: Amid NCR peaks and global volatility (A3 rating, 4% default risk).

- Execution Risks: Delays in flagships like Dwarka Expressway.

- Regulatory Overhang: ED, SC cases could halt or devalue.

- Retail Exposure: Like Paytm, retail (30% allocation in 2010) bears brunt.

X sentiments warn: “BPTP IPO scam” and “fraud.” Inventiva calls it a “conspiracy to defraud.”

In essence, BPTP’s IPO is a vehicle for promoters to exit amid liabilities, mirroring Paytm’s fate.

Conclusion: The IPO as a Loss-Passing Mechanism

BPTP’s story underscores a broader malaise in Indian markets: overhyped IPOs as escape hatches for troubled firms. With unresolved scandals, financial opacity, and a promoter under fire, this IPO could evaporate investments, leaving retail holders with worthless shares.

Ultimately, companies use IPOs to pass their losses to retail investors, offloading risks while promoters cash out— a pattern BPTP exemplifies.