High Government taxes is the most responsible reason for the falling economy.

What is the relationship between taxes and economic growth?

Higher taxes do not affect long-term growth rates, but short-term growth rates permanently reduce the size of the economy. Decomposing the total tax burden, Tomljanovich discovers that income, property, and sales taxes have no significant effects on growth, while corporate taxes have a positive impact.

Justification for the government raising taxes

Tax and fee collection is a critical development priority. It is essential to finance investments in human capital, infrastructure, and the delivery of services to citizens and businesses, as well as to establish the appropriate price incentives for long-term private-sector investment.

How will the economy be affected if the government raises taxes?

The government influences the disposable income of households by raising or lowering taxes (after-tax income). A tax increase reduces disposable income by taking money out of homes. A tax cut increases disposable income because it gives households more money.

Does raising taxes reduce GDP?

Tax changes have a significant impact: an exogenous tax increase of 1% of GDP reduces real GDP by 2% to 3%.

How does fiscal policy function?

Policymakers have two primary tools for influencing the economy: monetary policy and fiscal policy. By altering interest rates, bank reserve requirements, the purchase and sale of government securities, and foreign exchange, the Reserve Bank of India indirectly affects activity. In addition, governments impact the economy by altering the amount and nature of taxes, the scope and nature of spending, and the amount and nature of borrowing.

Governments impact how resources are used in the economy, both directly and indirectly. A basic national income accounting equation that measures an economy’s output (or GDP) about expenditures explains how this occurs:

GDP equals C + I + G + NX.

GDP is shown on the left as the total value of all final goods and services produced in the economy. On the right, the sources of aggregate spending or demand are:

-

Private consumption (C).

-

Private investment (I).

-

Government purchases of goods and services (G).

-

Exports minus imports (net exports, NX).

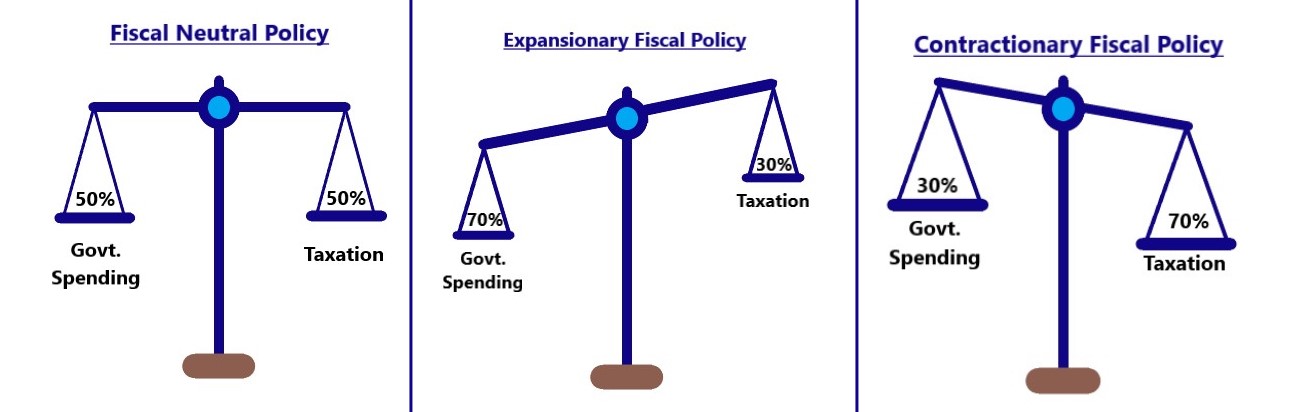

This equation demonstrates how governments influence economic activity (GDP), controlling G directly and indirectly, affecting C, I, and NX through changes in taxes, transfers, and spending. Fiscal policy that increases aggregate demand by increasing government spending is called expansionary or “loose.” On the other hand, fiscal policy is frequently regarded as contractionary or “tight” if it reduces demand through lower spending.

Why do tax increases slow down the economy?

In states where high earners are subject to higher taxes, migration increases the pretax real incomes of high earners while lowering the accurate pretax payments of lower earners. Instead of achieving long-term income redistribution, a more progressive tax structure distorts economic decision-making and reduces total real incomes.

The global financial crisis, which began first in the United States mortgage market in 2007, is an excellent case study of fiscal policy. The global economic crisis harmed economies worldwide, with financial sector difficulties and dwindling confidence influencing domestic spending, foreign investment, and trade (all of which affect output and GDP). Governments attempted a response to stimulate activity through two channels: automatic stabilizers and fiscal stimulus (new discretionary spending or tax cuts).

Stabilizers are not dependent on specific government actions and take effect as tax revenues, and expenditure levels change. They operate in sync with the business cycle. For example, as output slows or falls, the taxes collected fall because corporate profits and taxpayer incomes fall, particularly in progressive tax systems where higher-income earners are taxed at higher rates. During a recession, unemployment benefits and other forms of social spending are also expected to rise. Because of these cyclical changes, fiscal policy becomes expansionary during downturns and contractionary during upturns.

Automatic stabilizers are proportional to government size, which is more prominent in advanced economies. Because both approaches help to mitigate the effects of a downturn, there may be less need for stimulus where stabilizers are more vital (tax cuts, subsidies, or public works programs). Indeed, countries with larger stabilizers used discretionary measures less frequently during the recent crisis.

Furthermore, unlike discretionary actions, which can be tailored to specific stabilization needs, automatic stabilizers do not suffer from the implementation lags that discretionary measures frequently do. (For example, it can take time to design, obtain approval, and implement new road projects.) Furthermore, as conditions improve, automatic stabilizers and their effects are removed automatically.

The stimulus can be challenging to design and effectively implement and difficult to reverse when conditions improve. However, institutional constraints and narrow tax bases in many low-income and emerging market countries mean stabilizers are relatively weak. Even in countries with more muscular stabilizers, there may be a pressing need to compensate for lost economic activity and compelling reasons to direct the government’s crisis response to those in the greatest need.

Financial resources to respond on

The precise response ultimately depends on a government’s fiscal space for new spending initiatives or tax cuts, that is, access to additional financing at a reasonable cost or the ability to reorder existing expenditures. Some governments were unable to respond with stimulus because potential creditors feared that Inflation, foreign exchange reserves, and the exchange rate would be under too much pressure from increased spending and borrowing, or they would be delayed recovery by diverting too many resources away from the domestic private sector (also known as crowding out).

Creditors may also have questioned some governments’ ability to spend wisely, reverse stimulus once it has been implemented, or address long-standing concerns about underlying public systemic financial issues (such as chronically low tax revenues due to a poor tax structure or evasion, weak control over the finances of local governments or state-owned enterprises, or rising health costs and aging populations). Other governments have been forced to cut spending as revenues fall due to more severe financial constraints (stabilizers functioning). Fiscal stimulus is likely ineffective, if not undesirable, in nations with high inflation rates or external current account deficits.

The stimulus’s size, timing, composition, and duration are all critical factors to consider. The size of stimulus measures is generally tailored to policymakers’ estimates of the output gap—the difference between expected output and output if the economy were operating at total capacity. It is also necessary to calculate the stimulus’s effectiveness or, more precisely, how it affects output growth (also known as the multiplier).

The economic environment is accommodative (interest rates do not increase due to the fiscal expansion) if there is less leakage (for instance, only a tiny portion of the stimulus is saved or spent on imports). The country’s fiscal position following the stimulus is viewed as sustainable; multipliers tend to be larger. This cancels out its harsh effects. Suppose the expansion raises concerns about long-term sustainability.

In that case, multipliers can be small or even harmful. The private sector will likely respond to government intervention by increasing savings or moving money offshore rather than investing or consuming. Furthermore, multipliers for Spending levels are lower for small, open economies and higher than for tax cuts or transfers (in both cases, because of the extent of leakages).

In terms of composition, governments must choose between targeting stimulus to the poor, where full spending and a strong economic effect are more likely; funding capital investments, which may create jobs and help boost longer-term growth; and providing tax cuts, which may encourage firms to hire more workers or purchase new capital equipment. Governments have taken a “balanced” approach to all of these measures in practice.

In terms of timing, it is common for spending measures to take some time to implement (programme or project design, procurement, and execution), and once implemented, the measures may be in effect for a greater time period than necessary. On the other hand, the down turn is expected to last a long time (as it did during the recent crisis), concerns about lags may be less pressing: Some governments emphasized the execution of projects that were “shovel-ready,” or approved and prepared to go. For all of these reasons, stimulus measures should be targeted, timely, and temporary, with the goal of being quickly reversed once conditions improve.

Similarly, the responsiveness and scope of stabilisers can be improved, for example, by instituting a more progressive tax system that taxes high-income households more than low-income households. Transfer payments may also be explicitly linked to economic conditions (for instance, unemployment rates or other labour market triggers). Some countries’ fiscal rules aim to limit spending growth during boom times, when revenue growth is high, particularly from natural resources, and constraints appear less binding. Likewise, formal program review or expiration (“sunset”) mechanisms aid in ensuring that new initiatives do not outlive their initial purpose. Finally, medium-term frameworks that provide comprehensive coverage and assessment of revenues, expenditures, assets and liabilities, and risks help policymakers make decisions throughout the business cycle.

Large deficits and rising national debt

Fiscal deficits and public debt ratios (the debt-to-GDP ratio) in many countries have risen sharply as a result of the crisis’s effects on GDP and tax revenues, as well as the cost of the fiscal response to the crisis. Concerns about the fiscal stability of governments have been raised by support and guarantees provided to the financial and industrial sectors. Many nations can sustain modest fiscal deficits over long periods of time. Because domestic and international financial markets, as well as international and bilateral partners, believe they can meet current and future obligations.

Deficits that become excessively large and persist for an extended period of time, on the other hand, may undermine that confidence. Aware of these risks in the current crisis, the IMF urged governments in late 2008 and early 2009 to implement a four-pronged fiscal policy strategy to help ensure solvency: stimulus should not have long-term effects on deficits.

A commitment to fiscal correction once conditions improve should be included in medium-term frameworks, and structural reforms should be found and implemented to increase growth.; and countries facing medium and long-term demographic pressures should implement policies to address these pressures. Even as the worst effects of the crisis fade, and fiscal challenges persist, this approach is still effective, particularly in developed economies in Europe and North America.

edited and proofread by nikita sharma