The much-hyped Indian audio-tech brand boAt (Imagine Marketing Ltd.) is gearing up for a ₹1,500 crore IPO, but a deep dive into its Draft Red Herring Prospectus (DRHP) reveals alarming warning signs. A close reading of the Risk Factors and audited accounts shows inconsistent books, risky financing, and governance lapses that any prospective investor, or even a concerned customer should notice. Would it be wrong if we say boAt’s own auditors have documented a “parade of glaring red flags”?

Down the line, there is a scrutiny of boAt’s financial statements, highlighting the caveats flagged by its auditors, and question whether the company’s governance and culture are fit for public investment. is the picture that emerges is unsettling? Despite some recent profits, boAt’s foundation appears shaky, from the interpretation of the publicly available DRHP.

Red Flags in boAt’s Books: What the Auditors Found

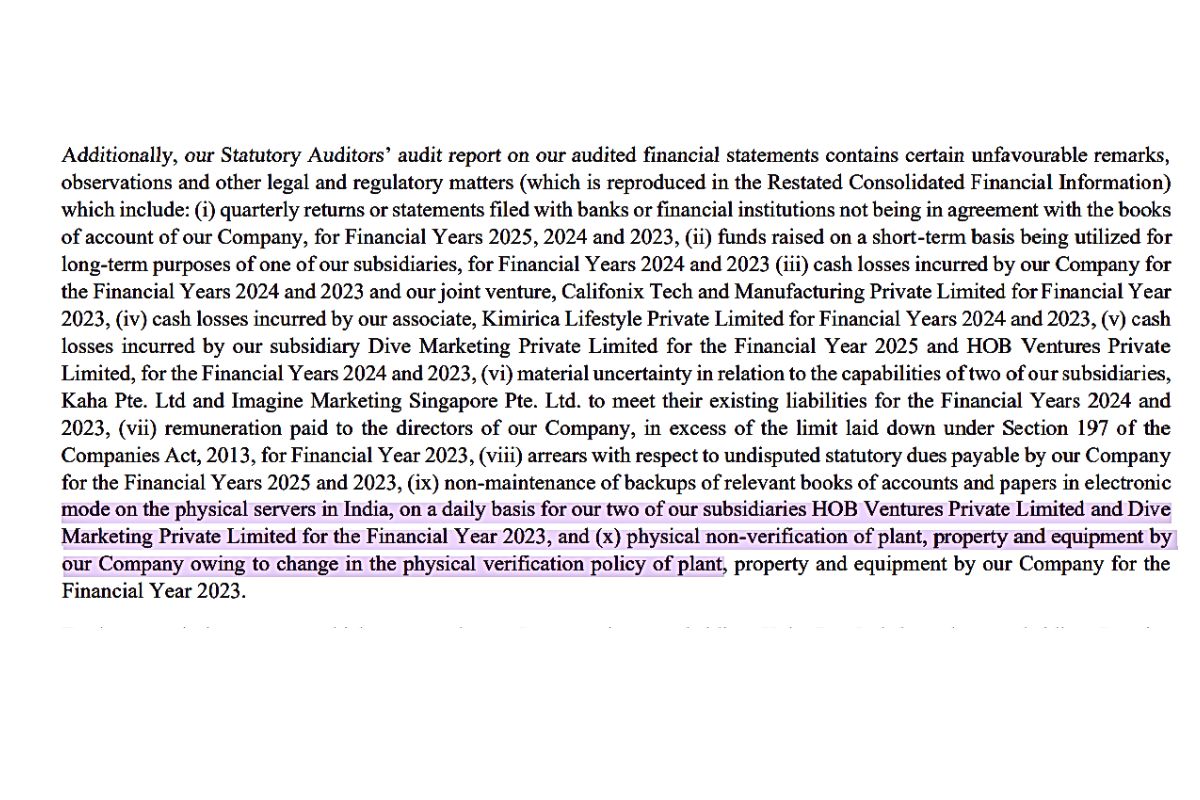

Imagine you’re considering buying into an IPO. You’d expect the books to be pristine. After all, the company is asking for public money. Instead, boAt’s DRHP shows serious mismatches and violations, all explicitly called out by the statutory auditors. In the Risk Factors section of the DRHP, boAt concedes the auditors have noted “unfavourable remarks” on its accounts. Key issues include:

- Accounts don’t match: For FY2023, FY2024, and FY2025, “quarterly returns or statements filed with banks or financial institutions [were] not in agreement with the books of account of our Company”. In plain terms, the company’s internal records differ from what it told its lenders. This is a basic control failure where your bank statements don’t agree with your books.

- Asset-Liability mismatch: In FY2023 and FY2024 the auditors found boAt used “funds raised on a short-term basis, for long-term purposes”. In other words, short-term loans or credit lines were channelled into long-term projects (like plant or equipment). This classic mismatch can trigger liquidity crunches, such as if short-term debts become due but assets take longer to produce returns, the company may face a cash squeeze.

- Excessive executive pay: The auditors flagged that FY2023 remuneration to directors exceeded the legal limits under India’s Companies Act. Simply put, the founders and top brass were paid more than allowed, which is a violation of corporate governance norms.

- Persistent losses in affiliates: The notes also reveal multiple companies in boAt’s orbit were burning cash. For example, the company itself had cash losses in FY2023–24, as did several subsidiaries and joint ventures. BoAt admits one JV (Califonix) lost money in FY2023, and even associates like Kimirica recorded losses. Two overseas arms (Singapore and Kaha Pte.) showed “material uncertainty” about meeting liabilities in FY2023–24. In short, across the group there were money-losing units dragging down overall results.

- Other lapses: Auditors noted lapses such as unpaid statutory dues and incomplete accounting backups in 2023. They even found that boAt had not physically verified all its fixed assets due to a policy change. These items hint at sloppy internal controls.

These revelations are startling. Auditors don’t list these items lightly. They signal weak internal controls and compliance issues. And they aren’t one-off: the same kinds of problems appear year after year. It seems that the entire IPO is built on a foundation that the company’s own auditors have called out as shaky. If the internal controls are this weak, how can anyone trust the financials?

As an investor, you’d expect all these issues to have been sorted out well before an IPO. Yet boAt is going public despite unresolved discrepancies. That suggests either mismanagement or an attempt to gloss over problems. Either way, it’s a red flag for anyone considering buying the stock.

Liquidity Crunch Ahead? Short-term Loans, Long-term Uses

One of the auditors’ biggest concerns is how boAt has been financing itself. The DRHP explicitly states boAt took short-term borrowing and tied it up in long-term investments. Why does this matter? Because it undermines basic financial prudence.

Typically, short-term loans (like bank working-capital limits or short-dated bonds) should be used to fund operations or inventory, aka the things that turn over quickly. Long-term projects (plant upgrades, R&D, new factories) should be funded with long-term capital (equity or long bonds). BoAt’s financiers instead see borrowing due soon being locked into assets or projects that won’t pay back for years.

This creates a maturity mismatch where liabilities are front-loaded, but the returns are back-loaded. If lenders demand payment before those long-term investments bear fruit, boAt might not have the cash to cover them. In the worst case, this is a classic recipe for a liquidity crisis. The auditors effectively warn, “Don’t be surprised if boAt has trouble servicing its debts if interest rates rise or if inventory doesn’t sell.”

In practical terms, it also means boAt’s cost of capital is high. Short-term rates tend to be higher and more volatile. BoAt has locked itself into that high-cost debt. If market conditions shift (as they often do), suddenly its financing costs can spike, squeezing margins. For investors, this is grave. An IPO should strengthen the balance sheet and fund growth safely. Instead, boAt’s books show fundamental misalignment of funding and spending. It sounds like there is “a deep misunderstanding of basic financial management, or worse, a reckless disregard for it.”

The DRHP gives an explicit example: it notes funds “raised on a short-term basis being utilised for long-term purposes” for two straight years. This isn’t a one-off hiccup; it’s a pattern. In a sensible company, the bankers’ quarterly statements would always tie out to the books, and long-term assets would be backed by long-term money. Neither was the case here. Instead, the mismatch remained uncorrected even as boAt prepared to go public.

Bottom line: boAt’s financing strategy looks fragile. If creditors get jittery, or if boAt’s growth slows, the company could face a funding crunch. That’s exactly the kind of risk an IPO prospectus should emphasize, yet it’s buried in the small print.

Breaking the Rules: Excessive Executive Pay and Governance Gaps

Another eyebrow-raising point in the DRHP is boAt’s own board breaking the rules on executive compensation. The auditors reported that in FY2023 the “remuneration paid to the directors was in excess of the limit laid down under Section 197 of the Companies Act, 2013”. In plain English, the founders and management were legally paid more than the cap on their salaries and benefits.

Indeed, boAt’s filings show the company had to pass a shareholders’ resolution to waive the excess payment. That means the excess pay was not a clerical error, but it was significant enough to catch attention and require correction. While boAt claims to have obtained a waiver by a shareholder vote, the fact it happened is worrying. Why? Because it suggests the company’s leadership was authorizing pay they shouldn’t have. If management is willing to flout laws on its own compensation, what does that say about their respect for other rules and controls?

To make matters more pointed, see how in FY2025 (the year before the IPO), each founder was still drawing hefty salaries. Disclosure in the DRHP (and media reports) show that Sameer Mehta and Aman Gupta each took home ₹2.5 crore in FY2025. Right after that, they abruptly resigned from executive roles and now take zero salary. This dramatic pay cut (from ₹2.5 crore to ₹0) happened just 29 days before the IPO filing.

From an investor’s standpoint, that reeks of convenient timing. It’s not uncommon for founders to step back before an IPO, but usually they hand off duties as part of a planned succession, often while still earning an appropriate director’s fee. Here, though, the timing is too precise and too abrupt as “the founders are distancing themselves from operational responsibility right before going public”. Isn’t it similar, how just before IPO, Bhavish Aggarwal started selling his own shares? It looks more like a “calculated pre-IPO pivot” than a genuine leadership transition.

Governance aside, consider the optics. The people running the show one day (and getting rich on the salaries) are gone the next, when public investors are asked to buy shares. And now both sit on the board with no pay. Does that inspire confidence? Or does it make you wonder why they felt the need to escape operational duty exactly now? The boAt DRHP doesn’t fully explain, other than to note the fact. But investors are perhaps on the mood of asking if the founders won’t steer the ship anymore, who will, and can we trust that those taking over (like the newly appointed CEO Gaurav Nayyar) can handle it?

Tiny Profits, Big Questions: Are the Financials Robust?

boAt often touts itself as a market leader and indeed the recent numbers show some return to profit. But the underlying story is still worrisome. After two years of losses, boAt swung to a net profit of roughly ₹61 crore in FY2025 on revenues of about ₹3,073 crore. That’s a profit margin of just 2% before tax, which is a razor-thin by consumer-goods standards. In FY2024, it lost ₹79.7 crore, and FY2023 it lost ₹129.5 crore.

So the turnaround, while real, is far from robust. It took a dramatic restructuring (cost cuts, Q4 expenses rejigged, etc.) just to eke out a quarter-percent EBITDA margin. Such narrow profits leave very little buffer for any hiccup- say a sudden raw material cost spike, a new competitor cutting prices, or a disrupted supply chain. And we know from the prospectus that boAt’s margins already depend heavily on aggressive marketing and promotions.

To add perspective, boAt’s FY2025 profit of ₹61 crore is smaller than many mid-size Indian companies report in a good quarter. For the hundreds of crores in sales, stakeholders might expect a stronger bottom line, especially when the founders are now pitching investors. Instead, almost all the growth to date came from increasing volume, not price or margin. In fact, boAt’s balance sheet shows debt still at around ₹565 crore as of FY2025(though reduced from prior year). It’s cutting leverage, but still carries substantial liability.

Given that context, other DRHP disclosures are ominous as boAt warns (quite properly) that future profits are not guaranteed. Even more, the Wearables segment, once expected to be a growth driver has seen revenue plunges, contributing to past losses. Approximately just a year before, it was reported that the number of active brands in India’s wearable market which includes smartwatches and audio wearables has fallen sharply, dropping by more than 30% in the July–September quarter of 2024. Only 52 brands are still operating, and experts say even more Indian brands may shut down soon.

The market is slowing down because people are taking longer to replace their old devices, there’s little new innovation in affordable products, and too many brands are offering similar, repetitive items. Experts say demand is falling and profit margins are very small. Many Indian companies depend on cheap, rebranded products made in China, and that’s making it hard for them to survive. Meanwhile, Chinese smartphone brands are returning to the market, using their strong ecosystems and focus on premium products to attract buyers again. “A confusing product portfolio has also left consumers dissatisfied, particularly after their first smartwatch purchase,” said Anshika Jain, senior research analyst at market tracker agency Counterpoint Research, regarding the above drop in sales.

The IPO proceeds themselves will largely go into working capital and marketing, not into eliminating legacy problems. In sum, the financials are a mixed bag. Yes, boAt has returned to profit, but it’s a precarious profit. The fundamentals like slim margins, heavy reliance on a few product lines, and a history of losses are not typical of a clean-ops IPO candidate. It raises the question that “is boAt being pushed public on momentum alone, without a truly sustainable underpinning?”

Founders Fleeing the Helm: Management Exodus Before IPO

A public-company IPO usually showcases continuity of leadership. Instead, boAt’s DRHP reveals a sudden brain drain at the top. Just 29 days before the IPO filing, both co-founders relinquished their day-to-day roles. Sameer Mehta resigned as CEO and became an Executive Director, and Aman Gupta quit as CMO to be a Non-Executive Director. Strikingly, neither now takes any salary or sitting fees, whereas each drew ₹2.5 crore in FY2025.

At the same time, a new CEO (Gaurav Nayyar) was appointed. The official explanation is usually something like “making way for fresh leadership before a new phase”. But the timing here screams unusual. A corporate transition of this scale would normally be announced with plenty of fanfare, showing investors a well-planned succession. Instead, it appears as a footnote in the DRHP. Multiple analysts have noted it looks more like the founders stepping back from risk while still cashing out a portion of their stakes in the IPO (selling shares worth hundreds of crores).

For the public, this sequence may not mean much at first glance. However, from an investment perspective it is unsettling. If the visionary founders aren’t running the show after the IPO, it begs many questions. Why? Do they not believe in boAt’s near-term prospects enough to stick around? And crucially, who is left to trust with execution? Gaurav Nayyar steps in on Day 1 of public life, but without any track record in the company or hype. This case is again similar to top level exodus in Ola, that signalled the problems in the company.

To sum it up, boAt is entering public markets under new management, orchestrated overnight. The founders won’t be at the operational wheel (even if they remain on the board), and this dramatic change was barely mentioned in PR. That’s enough to give investors pause. As one commentator bluntly put it, “it’s not just a management problem anymore, it’s a trust problem.”

Talent Exodus: A Revolving Door of Employees

Beyond the top brass, the DRHP reveals that boAt is losing staff at an alarming clip. The company’s full-time attrition rate, the percentage of employees leaving each year, has climbed into the 30–35% range. In FY2023 it was 27.09%, FY2024 28.14%, and FY2025 a staggering 34.18%. To put that in context, for every 3 employees at the start of FY2025, one left by year-end. In typical Indian corporate benchmarks (even in tech), attrition above 20-25% is considered high. BoAt’s 34% is extraordinary.

What’s more, this mass exodus happened despite boAt having a “massive ESOP program”, meaning employees held valuable stock options. If those options were truly worth something, they should have been incentives to stay. Instead, boAt notes itself that employees are either “miserable despite paper wealth” or “have zero faith in the future value of the stock”. In lay terms, people are quitting even though they have a stake in the company. That’s a huge red flag on morale and culture.

Imagine hiring dozens of engineers and marketers, only to see more than a third of them walk out the door every year. Projects get disrupted, costs for recruiting keep piling up, and organizational knowledge leaks out. Over time, this can cripple execution. In boAt’s case, it suggests the internal environment is toxic or pessimistic. Indeed, analysts interpreting the DRHP remark that boAt’s “internal culture is completely broken.” That aligns with the numbers where high attrition isn’t normal turnover, it’s a mass exodus.

A company whose own employees are fleeing can’t focus on growth. Yet boAt’s IPO pitch leans heavily on its brand and expansion plans. If the people building the brand are walking out in droves, the brand itself could suffer. And investors should know that when attrition spikes, often problems like mismanagement or missed targets follow. In sum, boAt is asking new shareholders to bet that this large-scale turnover is just a hiccup, not a chronic problem. Given the evidence, that’s a hard case to make.

Other Worrisome Internal Controls

The flagged issues go beyond pay and people. The auditors also pointed to more mundane but meaningful lapses:

- Backup & Records: Two key subsidiaries failed to maintain proper backup of electronic books and papers on a daily basis during FY2023. In simple terms, vital financial records weren’t consistently backed up. In today’s world of cyber risks and compliance, that’s a glaring oversight.

- Tax and Dues: There were “arrears with respect to undisputed statutory dues” for FY2023 and FY2025. This implies boAt fell behind on certain legal payments (like taxes, Provident Fund, etc.), at least temporarily. Any delay here can lead to penalties or legal trouble.

- Physical Verification: The auditors noted boAt “did not verify physical plant & equipment” in FY2023 due to an internal policy change. Verifying that factories and machinery exist and are accounted for is a basic audit requirement. Not doing so undermines confidence in the balance sheet.

- Frequent Audits: The very fact that such a long list of issues keeps showing up suggests boAt’s internal audit process is not working. Public companies usually have strong audits to catch these things early. Here, investors see year after year of the same kinds of comments. That persistence alone is a concern.

When put together, all these audit notes paint a picture of sloppy governance and control weaknesses. The DRHP even admits that these aren’t just one-offs. The company “took steps to rectify some observations” but “there can be no assurance that any such remarks will not form part of our financial statements in future years”. In other words, boAt is warning investors that problems could recur. That’s a chilling acknowledgement for anyone thinking about buying into the IPO.

The Public vs. The Private Story

To outsiders, boAt may just look like a popular earphone and speaker brand. But behind the scenes, the story is more troubling than many media reports suggest. Most press coverage highlights boAt’s comeback to profitability and its brand cachet. What gets much less attention are the auditor remarks and internal strife. In fact, industry commentators have accused mainstream media of “hiding” these red flags by focusing only on the favorable spin.

Contrast boAt with many high-flying Indian startups. Investors have become used to enterprises that burn cash for growth, like food-tech or ed-tech platforms, often with heavy venture funding and losses. BoAt is different as its business is hardware and consumer goods, with thin margins. Startups can justify losses on R&D or user acquisition; boAt has to show it can actually make money selling physical products at scale. Its slight profits of late barely cover interest costs, let alone build war chests for future competition.

Worse, the mix of issues at boAt suggests governance failure more than mere growth strategy. When a startup grows, one might excuse corners cut for the sake of speed. But boAt is an established company with audited financials and big-name backers (Warburg Pincus via South Lake Investment, Qualcomm Ventures, etc.). It’s supposed to operate with the rigor of a public firm already. Instead, its IPO filings expose a lack of financial discipline that even early-stage startups shouldn’t have.

Consider how IPO vetting works. Companies “clean up” their books before going public, resolving any mess. You’d expect boAt to have fixed misstatements, align its books with bank statements, and ensure compliance with the Companies Act before showing the DRHP to investors. Yet the opposite happened as the existing slip-ups were simply documented, not corrected. The filing even acknowledges that “when you go IPO, you clean the house… but digging into boAt’s ‘Risk Factors’ reveals disturbing things”. This contrast of public pride vs. private reality should set alarm bells ringing.

We speak of “weeding the garden” before sowing new crops. Similarly, in finance, you “pave the runway” for new investors. boAt didn’t do that. It’s pushing ahead with known issues front and center. “Is this the kind of governance you want to bet on?”. Given all the audit caveats, the prudent answer might well be “no.”

Are Investors Being Warned Enough?

It’s worth noting that boAt did disclose these problems in its DRHP. The issue is not concealment, but whether investors will dig for or recognize them. The prospectus’s “Risk Factors” section (nearly buried on page 28 of 493!) does list many standard cautions. But unless you read through the audit reports, you’d miss the explosive bullet points we’ve covered. Or else, if you follow certain analysts on Linkedin, perhaps you would know many things.

Some may argue the IPO is safe because boAt’s products have mass appeal, and the recent profits show things have turned around. That’s a fair point on one level, a ₹61 crore profit is real money. But when the fine print shows questionable bookkeeping, expensive internal turnover, and compliance breaches, it tempers that optimism.

Remember, the founders themselves will be walking away with a big chunk of proceeds through an offer-for-sale (Aman Gupta is selling up to ₹225 crore worth of shares, and Sameer Mehta up to ₹75 crore). They stand to profit regardless of the company’s long-term performance. Meanwhile, new investors get all the risks on their balance sheet.

How have other IPOs with similar issues fared? The recent history of Indian IPOs is littered with companies that looked good superficially but then disappointed after listing, often because of the same underlying problems. Buyers ultimately got spooked and stocks languished. It’s too early to say if boAt will join those ranks, but the parallels cannot be ignored.

From a public point of view, one might sympathize with boAt’s fans who want it to succeed and remain “Make in India” success story. But banks and regulators exist to protect small investors from this kind of scenario. The onus is on boAt to answer that “why should someone trust these financials? Why invest if internal records have been inconsistent? Why believe in growth if culture is in crisis?”

These concerns are grounded in the company’s own disclosures. It’s not mere speculation. Yet in marketing materials and interviews, boAt is selling a story of innovation and youthful energy.

At the end, isn’t this a Sinking Feeling?

These are not trivial issues you’d expect from a company about to invite retail investors to join its cap table. If anything, they scream for caution. The fact that boAt actually flagged these issues in its own documents (rather than sweeping them under the carpet) is a small mercy; it means potential investors can find the truth if they look. But in the frenzy of an IPO, do average investors really read the 500-page DRHP with such scrutiny?

For those who do, the verdict must be, beware. boAt’s products might be cool, but its financial house appears far from tidy. Let’s approach this IPO more warily than with fanfare. In a free market, investors ultimately decide. Any personal view is that unless boAt can convincingly clean up these red flags before the final prospectus, the company’s glide path looks bumpy.

It may well turn out profitable, but the high risk of a crash is plainly visible in these pages. We’ll have to see if others notice the same warning signs. In the meantime, anyone thinking of buying boAt shares would do well to remember: even shiny products can come from wobbly boats, as reflection of public documents and media reports.