Lavish Lease: SEBI’s Chairman Lives In Luxury While Investors Suffer In Silence!

SEBI’s Idea of Market Discipline Is a Luxury Tower in Prabhadevi...

On September 17, 2025, news broke that the Securities and Exchange Board of India (SEBI) leased a 5-BHK luxury apartment in Mumbai’s Prabhadevi for its new chairman, Tuhin Kanta Pandey, at a staggering ₹7 lakh per month. The three-year lease (with a 12-month lock-in) totals ₹2.65 crore in rent, with annual 5% escalations (₹7.35 lakh in year 2 and ₹7.71 lakh in year 3).

SEBI also paid a ₹42 lakh security deposit upfront. The apartment is 3,000 sq.ft. with 4 covered car parks in the high-rise Rustomjee Crown Tower, about 30 minutes from the SEBI office. SEBI’s public statement emphasizes that the deal is “within approved limits” and based on a valuer’s report. But to taxpayers and ordinary investors, this deal reads like government funds diverted to executive comfort.

Why Such An Exorbitant Cost For a Head of Public Market Regulator?

At ₹7 lakh per month, the chairman’s rent dwarfs his own salary and virtually every other official allowance. Under SEBI’s rules, a chairman can choose either (a) the government pay scale (equivalent to a Secretary to the Government of India) or (b) a consolidated salary. Reports confirm Pandey took the higher salary option, meaning SEBI must provide free housing.

In that case, his basic pay is capped at about ₹2.25 lakh per month. By comparison, the ₹7 lakh rent is three times his entire salary. Even under the consolidated-pay option, the maximum salary is ₹4.5 lakh (with no housing), so the rent still exceeds half his pay. In short, SEBI is spending more on rent for one person than the person earns.

For common SEBI employees, the gap is even more grotesque. A junior SEBI Grade A officer (assistant manager) in Mumbai has a gross salary of roughly ₹1.49 lakh and an in-hand take-home of about ₹1.10 lakh per month. In other words, the chairman’s apartment rent is over six times a mid-level officer’s entire salary! As an SEBI officer’s website candidly notes, “Gross salary ₹1,49,500, In-hand ₹1,10,500 per month”. This sharp disparity where millions of rupees on executive housing versus modest salaries for staff clashes badly with public perceptions of a regulator’s modesty. Ordinary citizens might reasonably ask that is it prudent for a watchdog of markets to indulge in executive luxury rather than saving funds for its own mission?

By any yardstick of Mumbai real estate, ₹7–8 lakh monthly rent is astronomical for an official residence. Even premium 5-BHK flats in good areas typically rent for much less. Industry reports show Mumbai’s central rents averaging ₹6–7 lakh for comparably sized luxury units. SEBI quietly points out that its lease aligns with a valuator’s estimate and an internal ceiling.

But this raises eyebrows that why should any valuation or internal policy allow triple or quadruple the chairman’s own salary? A recent media summary captures the public dismay: “SEBI has leased a five-bedroom apartment… at a starting monthly rent of ₹7 lakh. The lease spans three years, with a total rent of ₹2.65 crore”. To many taxpayers, those figures alone speak volumes.

Money is fungible. Every rupee SEBI spends on a plush apartment is a rupee not spent on its stated mission of investor protection, market regulation, and investor education. SEBI maintains the Investor Protection and Education Fund (IPEF), funded by fines and contributions, supposedly to educate and compensate small investors. But in practice, most of this fund sits unused.

According to SEBI’s own accounts, the IPEF corpus stood at ₹533 crore in March 2024 (and surged to ₹761 crore by FY25), yet SEBI spent only ₹2.8 crore in FY24 and about ₹2.7 crore in FY25 on investor awareness. That is well under 5% utilization of the fund in any year. In FY21 and FY23, spending peaked at ₹28.8 crore and ₹11.9 crore respectively, but still only a few per cent of the corpus.

Contrast that paltry spending with the ₹2.65 crore committed to the chairman’s rent alone. This one lease nearly equals the entire FY24 outlay on investor education. Investors and market watchers have long complained that SEBI’s awareness programmes are good on paper (tens of thousands of events) but fail to deliver real results. In fact, SEBI ran 43,826 investor-awareness events in FY24 and 50,789 events in FY25, a massive scale-up, yet its direct spending remained unchanged at roughly ₹2–3 crore per year. Economists say unused funds could instead bankroll targeted financial literacy, helplines, data-driven analysis tools, or technology to detect fraud. Instead, the regulator chose to dissipate resources on property rent.

The opportunity cost is stark. ₹2.65 crore could have paid the salary of dozens of market analysts or inspectors for several years, or built a modern digital surveillance unit. It is far more than enough to organize large-scale investor protection campaigns (seminars, websites, hotlines) nationwide. For context, one SSEB (stock exchange) official quipped that SEBI could have hired “200 new inspectors or invested in cutting-edge tech” with this money. (SEBI’s lack of manpower is frequently noted in parliamentary reports.) Instead of boosting core regulation, public funds are tied up in an opulent lease. A cynic might point out: SEBI was questioning executives for insider trading while paying its own boss insider prices.

SEBI’s defense is that the lease price was vetted by a “leading property valuer” and falls within board-approved limits. But none of the underlying details are public. The identity of the valuer, their comparative data, or any audit of the rental assessment has never been disclosed. The public only hears the regulator’s word that it seems fair. There is no independent proof that ₹7 lakh was the market rate or that the Board’s policy was scrupulously followed. Indeed, SEBI’s own website statement is bland that the property’s size and rent are “within the approved limit” and “determined in line with a valuation report of a leading property valuer”.

In the absence of transparency, such claims invite suspicion. Critics note that SEBI often resists revealing internal decisions. In a recent instance, the regulator refused an RTI request for details on when a chairperson recused herself from cases, invoking privacy and resource exemptions. SEBI has said that no such information on the matters in which Madhabi Puri Buch recused herself is “readily available”. The same SEBI said when an RTI asked ‘on what competencies Madhabi Puri Buch was choosen as the chair of SEBI”. If SEBI can claim secrecy over conflict disclosures, it can similarly resist disclosing details of expensive deals.

This is precisely why independent validation is needed. An official audit or RTI disclosure could confirm whether the lease terms were truly at market rates. So far, no such scrutiny has been applied. The only window was an RTI-accessed Portal Zapkey note, that revealed the ₹2.65 crore figure. But the actual valuation document and Board minutes remain hidden. Without them, the public must rely on SEBI’s assurances, which is hardly a reassuring prospect when large sums are at stake.

Observers argue that any premium paid (above, say, normal corporate rentals) should have to be justified in detail. Was the apartment fully furnished? What comparables were used? Were there any bids sought for alternate accommodation? The SEBI statement sidesteps all such questions. In effect, it asks investors to take its word. Given the premium on this deal, many ask bluntly that “Why not just lay out the report and policy in full?”

SEBI officials repeatedly cite a “Board-approved policy” governing official housing. Yet that policy itself is opaque to outsiders. Even basic questions that what is the allowable rent ceiling or house size? Why is a 5-BHK in Prabhadevi considered “within limit”?, go unanswered. The regulator’s formal line is simply that the accommodation “varies according to rank” and this particular case met the cap.

Some clues exist in law and models. The SEBI (Terms and Conditions) Rules, 1992 state that the Chairman is “entitled to rent free unfurnished house” with the Board approving its type or rent. In other words, by law the Chairman should get an official residence at no rent, not a private lease. Only if the Chairman opts out of a regular salary (choosing a consolidated pay of ₹4.5 lakh) would this rule not apply. Since Pandey took regular pay, the rules technically obliged SEBI to house him, rather than arrange a lease. Instead, SEBI treated it as a private lease with huge rent.

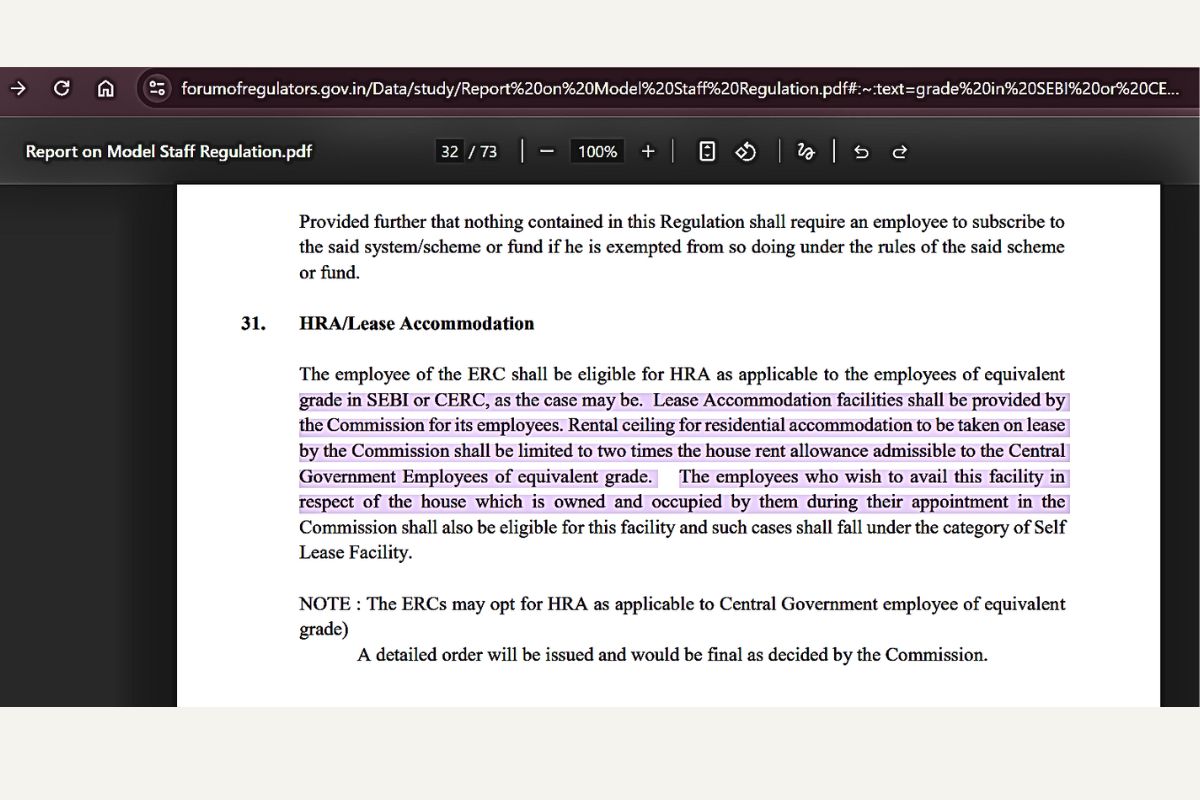

Likewise, a forum-of-regulators guideline (for generic commissions) states that “rental ceiling for residential accommodation to be taken on lease by the Commission shall be limited to two times the House Rent Allowance admissible to a Central Government employee of equivalent grade”. For a Secretary-level officer in Mumbai, CG HRA is around ₹24,000–30,000 per month, so 2× that is roughly ₹50–60,000 as a cap, far below ₹700,000. Even if SEBI’s internal policy were more generous, this model rule illustrates how unusually high the actual rent is.

In short, the lease appears to stretch (if not override) standard policy norms. SEBI says it was “within approved limit”, but the details of that approval (Board minutes or policy text) are unknown. Was there an explicit maximum rent or floor area? Did anyone question whether Mumbai’s luxury market is an appropriate benchmark for a regulator’s head? These questions remain unanswered, fueling skepticism that the “policy” was rubber-stamped after the fact.

How does this deal compare to past practice at SEBI or elsewhere in India? There is little direct precedent for a regulator head on this scale of rent. Earlier SEBI chairpersons (e.g. Ajay Tyagi, Madhabi Puri Buch) did not make headlines for palatial housing. When the BKC purchase was planned in 2018, SEBI talked of buying flats for its chairman and members, not leasing.

In fact, an internal note explained that official residences already existed in South Mumbai (allotted when the SEBI HQ was at Nariman Point) and proposed moving them to BKC for convenience. That report explicitly stated: “If the chairman… takes the normal pay scale, an official accommodation would have to be provided to him”. Thus, by SEBI’s own account, the expected solution was a provided flat, not an expensive market lease.

By breaking from that plan, SEBI has set a new high-water mark. Will future chairpersons get similar deals or even pricier ones (given inflation)? If other regulators take note, this could become a trend where a luxury apartment as standard benefit. For example, if SEBI’s board sees ₹7 lakh as acceptable for its chairman, why shouldn’t other agencies think likewise? There are hints of such an arms race. Opposition parties have pointed to past controversies in India involving public funds and housing for officials.

An often-cited example is the so-called “Sheesh Mahal” case in Delhi; an RTI revealed that ₹29.56 crore was spent on maintenance of then-Chief Minister Arvind Kejriwal’s official bungalow from 2015–2022 (an average of ₹3.69 crore per year). Even Delhi’s BJP leaders were aghast. They noted “on average, ₹31 lakh per month” was spent on upkeep. This suggests that lavish use of public money for official residences has precedent in India. SEBI’s transaction now places a market-rate rental on par with those scandals, albeit via regulatory funds.

However, housing costs at SEBI are a particularly sensitive benchmark. It is not a typical executive seeking comfort, but the head of the capital markets watchdog. When other institutions (like RBI, IRDAI, TRAI, etc.) allocate housing, they generally do so under strict limits or use existing government accommodations. SEBI’s shift to the top-tier real estate market of Mumbai is extraordinary and, some argue, damaging to institutional norms.

A regulator’s credibility rests on the perception that it is fair, transparent, and aligned with public interest, not that it treats its leadership as royalty. Questions are already being raised that “How can SEBI credibly lecture corporates on greed when it spends crores on executive housing?” For retail investors, already wary after various market scams, this lease can look like “more quid pro quo” and entitlement. The optics are bad.

SEBI insists it is protecting small shareholders, yet its own boss lives on the taxpayer dime in one of Mumbai’s priciest towers.

Investor-rights activists warn that such ostentation erodes trust. If the people who regulate market abuses are themselves seen as indulging in excess, suspicion of regulatory capture intensifies. A small investor denied relief might wonder, If SEBI’s leaders can claim crores, why do I have to fight so hard for a few thousand rupees? Credit rating agency and bank regulators have faced similar scrutiny; SEBI, as market guru, cannot avoid it. Even within SEBI’s ranks, seasoned officials may feel that spending on a luxury flat sends the wrong message. One SEBI staffer told a colleague off the record, “It’s like telling us to be frugal, while the boss goes shopping in the billionaire’s mall.”

At a minimum, the lease fuels political ammunition. Already, opposition politicians have blasted the expenditure as wasteful. Congress and other parties have demanded explanations, framing it as taxpayers subsidizing a “five-star life” for Pandey. SEBI’s brief statement that this is “within policy” looks like damage control rather than clarification. Ultimately, such episodes risk creating cynicism among market participants: faith in the regulator’s sincerity diminishes if its leadership appears indifferent to public perception.

The scandal is not only external. SEBI’s own employees, from research analysts to inspectors, are likely watching in disbelief. When the chairman’s rent alone exceeds what an entry-level officer earns in an entire year, morale can suffer. SEBI staff work long hours investigating fraud and educating traders, often with limited resources. They do so on salaries that, even with allowances, amount to barely ₹13–14 lakh per year. Meanwhile, one apartment lease is ₹9 lakh per year with an assured luxury lifestyle. Such disparities can breed resentment. If junior officers see the regulator pinching pennies on their travel and training, but happily shelling out rents akin to a corporate CEO’s villa, the internal culture of fairness is strained.

Moreover, SEBI’s own career charts show tight budgets. For instance, a Grade A officer receives around ₹1.5 lakh gross, including allowances, far less than the monthly rent of the chairman’s flat. Group allowances (petrol, housing aid, etc.) for staff are modest. Lower staff have sometimes complained of delayed promotions or frozen budgets in recent years. In that context, a lavish top-post perk feels especially tone-deaf. If the ruler lives in high style while soldiers scrimp, loyalty and motivation can erode.

Why lease a 5-BHK at such cost, instead of cheaper options? If SEBI was intent on providing housing, it could have considered purchasing a flat outright (as they contemplated in 2018) or using existing government facilities. Buying a comparable apartment (3,000 sq.ft.) in Prabhadevi would run into tens of crores, so leasing may save capital. But even a smaller 3-BHK in a less glitzy location could likely meet a chairman’s needs at far lower rent. SEBI could have justified a smaller or non-premium flat and still met policy.

Alternatively, SEBI could use a government guest house or an official bungalow. For example, the DGFT building or accommodations at Mumbai’s Fort/Worli area could have housed a senior official. (In fact, SEBI’s own past plan was to use flats in South Mumbai – now deemed too far, it seems no government alternative in Central Mumbai was sought.) Some have suggested even renting a furnished apartment on a shorter lease or using corporate housing networks when needed. Those choices might seem mundane, but they align with fiscal prudence. Instead, SEBI chose a trophy home.

Importantly, leasing gives no long-term asset to SEBI. After three years, the apartment reverts to the owner; the ₹42 lakh deposit is refundable, and the ₹2.65 crore rent is gone forever. Had SEBI purchased property, it might recoup some sale value later (albeit at enormous upfront cost). Here, once rented, SEBI gets nothing tangible from the expense. Critics ask: Why lock SEBI into a high lease instead of negotiating a purchase or exploring shared accommodation (for example, splitting a 5-BHK into two units for multiple officials)? The lack of such cost-saving creativity is conspicuous.

The lease’s built-in escalations also deserve scrutiny. Starting at ₹7 lakh, the rent rises to ₹7.35 lakh in year two and ₹7.71 lakh in year three, a 5% hike each year. Over three years, SEBI will pay ₹2.65 crore in rent plus ₹42 lakh deposit. That deposit (equivalent to six months’ rent) sits idle with the owner, yielding nothing. Worse, once the lease ends, SEBI will have to renegotiate in an even hotter market. If inflation and Mumbai rents continue climbing, the next lease could easily exceed ₹8 lakh per month. Thus the long-term financial burden is open-ended.

By comparison, had SEBI instead fixed a single 3-year rent with no escalation, it could cap the cost. Even better, outright ownership would eliminate such uncertainty (though at higher capital). We can only hope SEBI’s board negotiated an exit clause or renewal limit; otherwise, this flat is likely to become more expensive with each term. Given current trends (GST on luxury real estate, RBI raising rates), any renewal is likely to come with a rude shock.

This SEBI case may seem extreme, but it is part of a wider debate on public-sector perks in India. Across ministries and agencies, stories periodically emerge of ministers or officials living lavishly at taxpayer expense. Railways ministers were once criticized for building VIP trimmings, and state governments have spent on luxury retreats. Even regulatory bodies have had scrutiny: for instance, MPs questioned the Reserve Bank over its grand office renovation budget. These episodes fuel calls for reform.

Some analysts urge clear caps on perquisites for top regulators. They propose that boards annually disclose all benefit costs (housing, cars, travel) in detail. Others suggest tying official housing to mid-market rents or limiting floorspace. In fact, SEBI’s own policies seem at odds with such restraint. The Securities Appellate Tribunal (overseeing SEBI) has occasionally chided the regulator for lack of transparency. It remains to be seen whether the Pandey lease will spur new rules. At a minimum, parliamentarians may demand tighter oversight, perhaps even a Supreme Court or government audit of this transaction.

The Prabhadevi apartment lease for the SEBI chairman is a symbol of misplaced priorities. It epitomizes how public money intended for markets and investors can be diverted into high-luxury rather than core functions. By committing ₹2.65 crore in rent, plus ₹42 lakh deposit, SEBI has made a gift of massive sums to a property owner, while its own investor-education funds lie largely unused.

Critics will say that this deal sacrifices no hospital or pensioner’s money (SEBI is self-funded). But SEBI’s mission is to protect the public market, and it is funded by market participants and indirectly by all of society’s faith in fair markets. Every rupee wasted on perks is a rupee less for vigilance or compassion toward small investors.

SEBI’s reply (that it followed policy and market rates) will not quell concerns. Public perception is unforgiving: if regulators look lavish, public trust shrinks. Many will ask whether the era of frugality is truly over, and whether SEBI should reconsider this lavish lease.