Slower Growth, Bigger Ambitions. What China’s Two Sessions Reveal About Its Next Economic Phase

As China’s annual “Two Sessions” convene in Beijing, Premier Li Qiang has outlined a roadmap for the Chinese economy as it faces slower growth, structural headwinds and intensifying geopolitical rivalry. From artificial intelligence ambitions to military modernisation, the message from Beijing is clear: the next phase of China’s rise will look very different.

China’s annual “Two Sessions” gathering in Beijing has offered a revealing snapshot of how the country’s leadership sees the road ahead. In his government work report to the National People’s Congress, Premier Li Qiang laid out a set of priorities that reflect a leadership increasingly aware that the era of effortless high growth is fading.

Beijing set its GDP growth target for 2026 at between 4.5% and 5%, the lowest official target China has announced since the early 1990s, excluding the pandemic year when no goal was set. For a country that once routinely posted double-digit expansion, the new target is indicative of the economic challenges now facing the world’s second-largest economy.

The growth goal also represents a shift in philosophy. Chinese policymakers have increasingly emphasised “high-quality development” over simply chasing large headline numbers. The leadership is wary that aggressive growth targets can encourage excessive borrowing, unproductive investment and inflated local government statistics.

Fiscal policy will remain supportive but measured. The government maintained its budget deficit target at around 4% of GDP, a historically elevated level but unchanged from last year. Monetary policy is also expected to remain accommodative, with officials indicating that interest rate cuts and reductions in banks’ reserve requirement ratios remain possible if growth weakens further.

At the same time, Beijing has set several social stability targets alongside its economic goals. Authorities aim to keep the urban unemployment rate at roughly 5.5% while creating around 12 million new urban jobs during the year.

Inflation targets also reveal how policymakers view the current environment. China retained its 2% consumer inflation target, an unusually low threshold that reflects the country’s ongoing struggle with weak domestic demand and persistent deflationary pressures.

Taken together, the policy signals from the opening of the Two Sessions suggest Beijing is attempting to strike a careful balance – supporting economic activity while acknowledging that the structural forces shaping China’s economy are becoming increasingly difficult to ignore.

)

Structural Headwinds Weigh on China’s Growth

Behind China’s lowered growth target lies a set of structural challenges that have been building for several years. From the collapse of the property boom to weakening consumption and demographic pressures, the forces slowing the Chinese economy run far deeper than a typical cyclical downturn.

The most significant drag remains the property sector, which for decades functioned as one of the primary engines of China’s economic expansion. At its peak, real estate and related industries accounted for roughly a quarter of the country’s economic activity. That engine has now stalled.

A regulatory crackdown on excessive developer borrowing in 2020 exposed the fragile financial foundations of the sector, triggering a wave of defaults among property developers and leaving numerous housing projects unfinished. Since then, housing prices are estimated to have fallen around 30% from their 2021 peak, eroding household wealth and dampening consumer confidence.

Government efforts to stabilise the sector – including mortgage rate cuts, relaxed home purchase restrictions and tax incentives – have slowed the decline but have not yet revived demand in a meaningful way. For many Chinese households, property had long been the primary store of wealth. As prices fall, consumers have become more cautious with spending.

That caution has contributed to another worrying trend: persistent deflationary pressure. Prices across a wide range of goods and services have struggled to rise as companies slash prices to attract reluctant consumers. When households expect prices to fall further, they often postpone purchases, reinforcing downward pressure on demand.

Chinese policymakers have referred to this destructive price competition as “involution”, a cycle in which companies compete aggressively by lowering prices rather than expanding markets or improving productivity.

Adding to the challenge is China’s rapidly shifting demographic scene. The country’s population has begun to shrink, with births falling to their lowest level since at least 1949. The working-age population is also declining, while the proportion of elderly citizens continues to rise.

This demographic transition carries long-term implications for everything from consumer demand to labour availability. With fewer workers entering the workforce and more citizens retiring, China’s economic model – long powered by a vast labour supply – is undergoing a fundamental transformation.

Exports and the Trade War Cushion the Slowdown

Even as domestic demand remains weak, China’s export sector has provided a crucial buffer for the economy. In 2025, net exports accounted for roughly one-third of the country’s economic growth, the highest contribution in decades.

China’s exporters have managed to adapt to a more hostile global trade environment, particularly the ongoing tariff battle with the United States. At one point in early 2025, U.S. tariffs on certain Chinese goods reached as high as 145%, sharply restricting access to what was once China’s most important export market.

Yet Chinese manufacturers have responded by diversifying their export destinations. Shipments to Europe, Southeast Asia and emerging markets across the Global South have expanded, helping offset declining sales to the United States.

The shift has also coincided with China’s steady move up the industrial value chain. Instead of relying primarily on low-cost manufacturing, Chinese firms are increasingly exporting higher-value products such as electric vehicles, solar panels, industrial machinery and advanced manufacturing equipment.

This transition has helped China achieve a record trade surplus of around $1.2 trillion in 2025, underscoring the continued competitiveness of its manufacturing sector. However, relying heavily on exports to support economic growth carries its own risks.

Trade tensions between China and several major economies remain elevated, and protectionist measures against Chinese products are becoming more common across multiple regions.

For Beijing, the challenge is clear: while exports can cushion the slowdown in the short term, they are unlikely to serve as a permanent substitute for stronger domestic demand.

Military Modernisation and Taiwan Remain Central

While the economic outlook dominated much of the discussion at the Two Sessions, China’s leadership also used the platform to reaffirm its longer-term strategic ambitions, particularly in the realm of national security.

Beijing announced that it plans to increase defence spending by 7% in 2026, marking the slowest pace of growth in military expenditure since 2021 but still maintaining a steady upward trajectory. China’s official defence budget now stands at roughly 1.78 trillion yuan, making it the second-largest military spender in the world after the United States.

Despite the modest slowdown in spending growth, the government’s work report emphasised the need to accelerate the modernisation of the People’s Liberation Army (PLA), particularly in areas such as information warfare, advanced combat capabilities and strategic power projection.

The timeline for these ambitions remains clear. Chinese planners have set 2027 – the centenary of the PLA – as a major milestone for achieving significant improvements in military capability. By that point, Beijing hopes to field a force capable of operating effectively across multiple domains, including cyber, space and long-range precision strike.

Recent developments show how quickly China’s military capabilities are evolving. The government work report pointed to the commissioning of the Fujian, China’s first domestically built aircraft carrier equipped with advanced electromagnetic launch systems. The vessel represents a major step forward in China’s naval ambitions as it seeks to expand its presence in regional and potentially global waters.

At the same time, Beijing reiterated its uncompromising position on Taiwan. The report pledged that China would “resolutely oppose separatist forces advocating Taiwan independence and external interference.”

Tensions across the Taiwan Strait have remained elevated in recent years as military exercises, air patrols and naval deployments around the island have increased in frequency. For Chinese leadership, Taiwan remains both a sensitive political issue and a critical strategic objective.

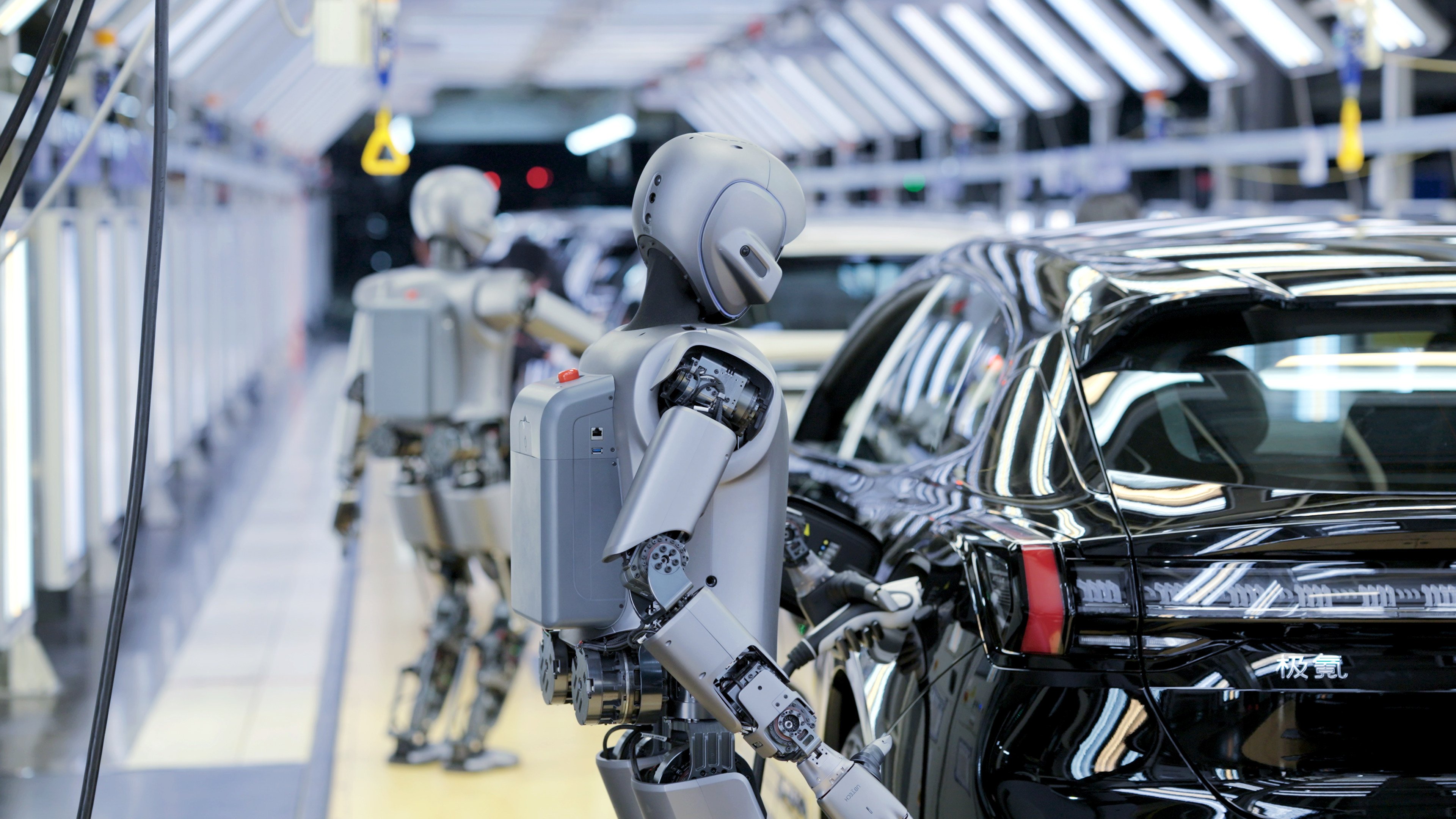

AI, Robotics and China’s Technological Bet

Beyond military modernisation, the Two Sessions also stressed what may be the most consequential pillar of China’s long-term strategy: an aggressive push into advanced technologies.

China’s new five-year development blueprint places artificial intelligence at the centre of its economic transformation. The 141-page plan references AI more than 50 times, underscoring how central the technology has become to Beijing’s future growth strategy.

The government has outlined an expansive “AI+ action plan” aimed at integrating artificial intelligence across nearly every sector of the economy – from manufacturing and logistics to healthcare, education and finance.

Chinese policymakers see technology not just as a tool for innovation but as a way to address the country’s structural challenges. Automation and robotics are expected to play a key role in compensating for China’s shrinking workforce, while AI-driven productivity gains could help sustain economic growth even as demographic pressures intensify.

The plan calls for major investments in quantum computing, 6G communications, embodied AI systems and humanoid robots, technologies that many experts believe could define the next industrial era.

Officials have also emphasised the development of open-source AI ecosystems, an approach that contrasts with the more proprietary models often pursued by Western technology firms. By encouraging open collaboration and rapid innovation, Beijing hopes to accelerate the deployment of AI applications across the economy.

China’s leadership believes the country is already making significant progress in several cutting-edge fields. According to a report by the state planning body, Chinese researchers and companies are increasingly competitive in areas such as biotechnology, robotics, advanced semiconductors and artificial intelligence.

For Beijing, technological self-reliance has become both an economic necessity and a strategic priority. Trade tensions with the United States have resulted in export restrictions on advanced semiconductor technology, forcing China to accelerate domestic innovation.

In the long run, Chinese policymakers appear to be betting that technological breakthroughs and automation will form the backbone of the country’s next phase of development.

Oil Shock and the Risk of Stagflation

Even as China struggles with deflation and weak demand at home, developments beyond its borders could complicate the economic outlook.

Rising oil prices driven by escalating tensions in the Middle East have begun to push global energy markets higher, raising the possibility of a new economic challenge: stagflation – a combination of slowing growth and rising prices.

Brent crude prices recently climbed above $84 per barrel, marking a sharp increase since the latest round of hostilities between Iran and U.S.-Israeli forces began. For China, which remains one of the world’s largest oil importers, sustained increases in energy prices could ripple through the broader economy.

Higher oil prices typically raise production costs for factories, increase transportation expenses and eventually push consumer prices upward. At the same time, rising costs can squeeze corporate margins and discourage investment, potentially slowing economic activity.

Economists often point to the oil shocks of the 1970s – including the energy crisis following the 1973 Yom Kippur War and the disruption triggered by the Iranian Revolution – as classic examples of how geopolitical conflicts can trigger stagflation in oil-importing economies.

For China, the situation is somewhat more complex. The country has spent years struggling with the opposite problem: persistent deflation and weak consumer demand. In theory, higher energy prices could help lift inflation closer to the government’s target.

But if oil prices rise too quickly or remain elevated for a prolonged period, the impact could instead weigh on economic growth while increasing inflationary pressures – precisely the combination policymakers are hoping to avoid.

China’s relatively diversified energy import network and state-managed fuel pricing system may provide some insulation from sudden shocks. Still, the unfolding geopolitical tensions in the Middle East serve as a reminder that external forces remain capable of shaping China’s economic trajectory.

A Strategic Transition for the World’s Second-Largest Economy

Taken together, the announcements emerging from this year’s Two Sessions reveal a country entering a new phase of economic and strategic transition.

For decades, China’s rise was powered by a combination of massive infrastructure investment, a booming property market and an abundant labour force. That model delivered extraordinary growth, transforming the country into the world’s manufacturing powerhouse and lifting hundreds of millions out of poverty.

Today, however, many of those engines are losing momentum. The property sector is no longer the reliable growth driver it once was, demographic shifts are shrinking the workforce, and geopolitical tensions are complicating trade relationships with major markets.

Faced with these realities, Beijing appears to be recalibrating its economic strategy rather than attempting to revive the old one.

The lowered growth target of 4.5% to 5% reflects a more pragmatic recognition of the constraints now facing the Chinese economy. Instead of chasing headline numbers, policymakers are focusing on stabilising employment, maintaining financial stability and gradually transitioning toward a more technologically driven model of growth.

At the same time, China’s leadership is clearly preparing for a more competitive and uncertain global environment. The steady expansion of defence spending, the emphasis on military modernisation and the continued focus on Taiwan all suggest that national security considerations are playing an increasingly prominent role in economic and technological planning.

Perhaps the most important signal from the Two Sessions lies in China’s massive push into emerging technologies. Artificial intelligence, robotics, quantum computing and advanced manufacturing are being positioned as the pillars of the country’s next development phase.

If Beijing’s strategy succeeds, technological productivity gains could offset some of the pressures created by demographic decline and slower traditional growth engines. But the path will not be without risks. Global competition in advanced technologies is intensifying, and trade frictions with the United States and other major economies show little sign of easing.

The Last Bit,