India’s small and medium enterprise sector is the backbone of the national economy — contributing over 30 percent of GDP and employing more than 110 million people. Yet one of the most persistent and damaging problems SMEs face is something deceptively mundane: waiting to get paid.

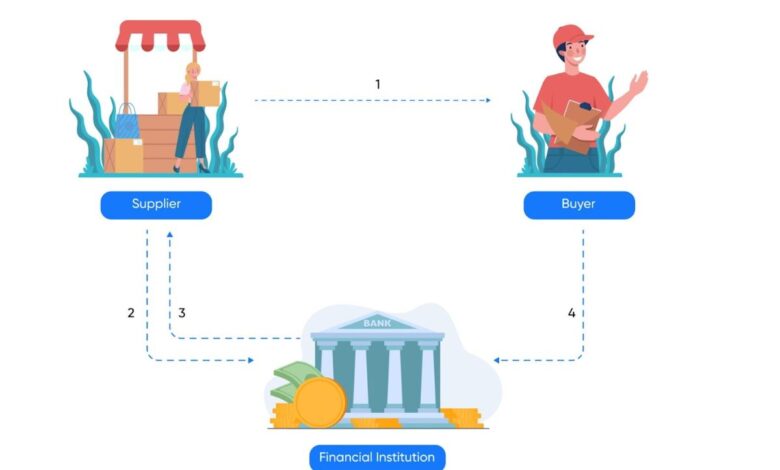

When a supplier delivers goods or services to a large corporate buyer, payment terms of 60, 90, or even 120 days are commonplace. During that waiting period, the supplier’s cash is locked inside a piece of paper — an invoice — while operational expenses, salaries, raw material purchases, and growth investments all continue to demand liquidity. This structural mismatch between when money is earned and when it actually arrives is what invoice financing was designed to solve.

Invoice financing — also called invoice discounting or receivables financing — allows businesses to unlock the value of their unpaid invoices immediately, receiving a large portion of the invoice value upfront from a financier, with the remainder (minus fees) paid when the buyer settles. In 2026, India’s invoice financing ecosystem is more developed, regulated, and technologically sophisticated than ever before, anchored by RBI-licensed Trade Receivables Discounting System (TReDS) platforms and supported by a growing range of fintech-led solutions. This article profiles the top 10 invoice financing platforms actively serving Indian businesses in 2026.

1. KredX

KredX is India’s most prominent and widely recognised invoice discounting platform outside the formal TReDS structure, and its name has become something of a category synonym in the early-stage and mid-market SME financing world. Founded in 2015 in Bengaluru by Manish Kumar and Anurag Jain, KredX operates a marketplace that connects businesses holding unpaid invoices from creditworthy corporate buyers with institutional and sophisticated individual investors willing to fund those invoices at a discount in exchange for short-term returns.

What makes KredX particularly compelling is its dual-sided value proposition. For the SME or vendor, it offers liquidity in as little as 24 to 72 hours against invoices that would otherwise sit idle for months. For investors, it offers access to short-tenure, relatively low-risk instruments — since repayment is contingent on the buyer (typically a large, rated corporate) rather than the SME itself. Over the years, KredX has expanded beyond invoice discounting into a broader supply chain finance platform, offering vendor financing, dealer financing, and dynamic discounting solutions to large enterprise anchors. Its growing enterprise client roster and consistent track record of investor returns make it one of the most trusted names in the Indian invoice financing landscape.

2. M1xchange

M1xchange, operated by Mynd Solutions, is one of India’s three RBI-licensed Trade Receivables Discounting System (TReDS) platforms — a category distinction that matters enormously. TReDS platforms are regulated market infrastructure institutions authorised by the Reserve Bank of India, designed specifically to facilitate the financing of trade receivables of MSMEs (Micro, Small and Medium Enterprises) through multiple financiers in a transparent, competitive, and standardised environment.

What this regulatory status means in practice is that M1xchange operates with a level of institutional credibility, participant oversight, and process transparency that non-licensed platforms simply cannot match. On M1xchange, an MSME seller uploads an invoice, the buyer (corporate anchor) accepts it on the platform, and multiple registered financiers — banks and NBFCs — bid competitively to fund the invoice, ensuring the MSME gets the most favourable discounting rate available in the market at that moment. M1xchange has consistently been among the highest-volume TReDS platforms in India, handling billions of rupees in invoice transactions annually, and its platform serves a wide range of sectors from manufacturing and logistics to healthcare and agribusiness.

3. RXIL (Receivables Exchange of India Ltd)

RXIL — the Receivables Exchange of India Limited — is the second of India’s three RBI-licensed TReDS platforms and is promoted jointly by the National Stock Exchange (NSE) and the Small Industries Development Bank of India (SIDBI). The institutional pedigree of its promoters alone gives RXIL a credibility and trust profile that distinguishes it in the market — both NSE and SIDBI are among the most respected financial institutions in the country, and their sponsorship signals a long-term, mission-aligned commitment to MSME financing.

RXIL operates on the same fundamental TReDS model as M1xchange — a three-party system involving MSME sellers, corporate buyers, and competing financiers — but has built particular strength in sectors where its promoters have deep existing relationships. SIDBI’s extensive MSME network and NSE’s institutional market infrastructure give RXIL natural distribution advantages when onboarding both sellers and financiers. For MSMEs that are already part of supply chains involving large public sector undertakings or NSE-listed companies, RXIL often provides the most direct and well-connected access to invoice discounting services.

4. Invoicemart (A.TREDS)

Invoicemart, operated by A.TREDS Limited, is the third RBI-licensed TReDS platform in India and was promoted by Axis Bank and mjunction Services Limited — a joint venture between SAIL (Steel Authority of India) and Tata Steel. This promoter combination gives Invoicemart distinctive sectoral strengths, particularly in steel, metals, and industrial manufacturing supply chains where mjunction’s deep buyer-seller network creates natural onboarding pathways.

Invoicemart has consistently focused on broadening its financier base — the platform has onboarded a large number of public and private sector banks as well as NBFCs, ensuring that MSME sellers benefit from competitive rate discovery. The Axis Bank backing also means Invoicemart enjoys strong connectivity with the bank’s large corporate client base, many of whom are natural anchor buyers on the platform. Together, India’s three TReDS platforms — M1xchange, RXIL, and Invoicemart — represent the formal, regulated backbone of the country’s invoice financing ecosystem, and every MSME exploring invoice financing should understand what the TReDS structure offers before looking at alternative platforms.

5. CredAble

CredAble is one of India’s most sophisticated and enterprise-focused supply chain finance and working capital platforms, founded in 2017 by Nirav Choksi and Ram Kewalramani. Unlike marketplace-style invoice discounting platforms, CredAble takes a technology-first, program-led approach — it works directly with large corporate anchors to design and deploy bespoke vendor financing, dealer financing, and dynamic discounting programs that are then made available to their entire supply chain ecosystem.

This anchor-centric model gives CredAble a distinctive footprint among India’s largest corporations, who use the platform to offer their vendors and dealers rapid access to working capital — simultaneously strengthening supply chain resilience while often generating early payment discounts that benefit the corporate’s own treasury. CredAble has built deep integrations with ERP systems like SAP and Oracle, enabling seamless data flow between corporate procurement systems and financing workflows. Its institutional backing, enterprise-grade technology, and growing balance of programs across sectors like retail, pharmaceuticals, and consumer goods have made it one of the most respected names in the Indian supply chain finance market.

6. Drip Capital

Drip Capital occupies a distinct and valuable niche in India’s invoice financing landscape — it specialises in trade finance for Indian exporters, providing invoice financing and purchase order financing to SMEs engaged in international trade. Founded in 2015 by Pushkar Mukewar and Neil Kothari, Drip Capital is backed by prominent venture capital investors including Accel, Wing VC, and Y Combinator, and operates across both India and the United States.

For an Indian SME exporter, getting paid on an international invoice is even more fraught than domestic receivables — payment cycles are longer, currency risk is present, and the complexity of cross-border documentation adds friction at every step. Drip Capital addresses this by providing financing against export invoices, purchase orders, and letters of credit, with a fully digital, paperless application process that can result in funding approval within 24 hours.

The platform’s AI-driven credit underwriting model assesses both the Indian exporter and the overseas buyer’s creditworthiness, enabling rapid decisions without the lengthy due diligence that traditional trade finance banks require. For India’s large and growing exporter community — particularly in textiles, chemicals, engineering goods, and agriculture — Drip Capital is one of the most purpose-built and effective financing solutions available.

7. C2FO

C2FO is a Kansas City-headquartered global working capital marketplace that has built a substantial and growing presence in India, working with large Indian corporates to deploy early payment and dynamic discounting programs for their supplier networks. Rather than the traditional debt-based invoice discounting model, C2FO’s primary product is dynamic discounting — where corporate buyers use their own surplus cash to pay suppliers early in exchange for a discount negotiated in real time on the platform.

This model is particularly powerful for large Indian conglomerates and MNC India subsidiaries with strong treasury positions, who can effectively earn a return on idle cash while simultaneously strengthening their supply chain by ensuring smaller vendors have healthy working capital. C2FO has partnered with major Indian corporations across FMCG, automotive, and industrial sectors, and its global network — which processes hundreds of billions of dollars in working capital annually — gives it a scale and institutional credibility that few domestic-only platforms can match. For suppliers to large C2FO-enrolled corporates, the platform offers a straightforward, low-friction route to early payment without the need for external financing.

8. Vayana Network

Vayana Network is one of India’s most experienced and deeply integrated supply chain finance technology companies, founded in 2017 and backed by investors including the International Finance Corporation (IFC) — the private lending arm of the World Bank Group. Vayana functions primarily as an enabler and network infrastructure provider for supply chain finance, working with banks, NBFCs, and corporates to digitise and scale their existing supply chain finance programs rather than positioning itself as a direct lender.

What makes Vayana particularly distinctive is its interoperability focus — the platform is designed to connect multiple financiers, ERP systems, and GST data sources into a unified, real-time finance workflow that significantly reduces the manual effort and data duplication that has historically made supply chain finance operationally expensive. Its GST-integrated invoice verification capability is especially relevant in India, where GST data provides a reliable, government-backed source of invoice authenticity. IFC’s backing is a strong signal of institutional quality, as IFC’s investment criteria include rigorous assessments of governance, risk management, and development impact. For banks and corporates looking to build scalable, compliant invoice financing programs on robust technology infrastructure, Vayana is one of the most credible partners available.

9. Cashinvoice

Cashinvoice is an Indian invoice financing platform that has built a focused and operationally mature product for SMEs in manufacturing and trading sectors that need fast, uncomplicated access to working capital against their trade receivables. Founded in 2016 and headquartered in Mumbai, Cashinvoice works with NBFC and bank partners to fund invoices, with the platform handling the technology layer — invoice upload, buyer verification, financier matching, and disbursement — while its lending partners provide the capital.

The platform has developed particular depth in sectors like steel, textiles, and food processing, where payment terms tend to be long and working capital cycles are financially punishing for smaller players. Cashinvoice’s ability to process invoices quickly, integrate with GST data for invoice verification, and work across multiple financier partners gives SMEs competitive rate options without requiring them to navigate complex applications with individual banks. For mid-sized manufacturing SMEs that have creditworthy corporate buyers but struggle to access bank financing directly, Cashinvoice provides a practical and well-tested alternative route to liquidity.

10. FlexiLoans

FlexiLoans is a Mumbai-based digital lending platform founded in 2016 that offers a broad range of business financing products, prominently including invoice financing and bill discounting among its working capital solutions. Backed by marquee investors including Sanjay Nayar’s family office, Maj Invest, and others, FlexiLoans has built its reputation on speed and accessibility — offering SMEs the ability to apply for and receive working capital financing with significantly less documentation and wait time than traditional banking channels require.

While FlexiLoans is not exclusively an invoice financing platform in the way that KredX or the TReDS players are, its invoice discounting product is a genuinely competitive and widely used component of its offering, particularly among smaller businesses with annual turnover between ₹50 lakh and ₹50 crore — a segment that is often too small for enterprise-focused platforms but too formal for informal credit. FlexiLoans’ integration with GST data, bank statements, and digital footprints allows it to underwrite SME credit risk quickly and at scale. For small businesses that need invoice financing as part of a broader working capital solution — one that might also include term loans or credit lines — FlexiLoans provides a convenient and accessible single-platform experience.

Understanding the Landscape: TReDS vs. Fintech Platforms

One of the most important distinctions for any business exploring invoice financing in India is the difference between RBI-licensed TReDS platforms and fintech-led invoice discounting platforms — and understanding this distinction can significantly affect the terms, cost, and suitability of the financing you access.

TReDS platforms (M1xchange, RXIL, and Invoicemart) are regulated market infrastructure institutions. They operate transparent, auction-based systems where multiple financiers compete to fund your invoice, which structurally drives rates down. They are specifically designed for MSME sellers, and participation by large corporate buyers in the TReDS ecosystem is increasingly mandated by government policy for companies above a certain size. If your business is an MSME and your buyers are large corporations, exploring TReDS should genuinely be your first step — the competitive rate discovery mechanism and regulatory oversight make it structurally advantageous.

Fintech-led platforms like KredX, CredAble, Drip Capital, and others offer greater flexibility — they can serve businesses that may not qualify under TReDS eligibility parameters, offer faster onboarding, and in some cases provide financing against international invoices or purchase orders. They are the right choice when TReDS is inaccessible or when the specific financing need (export finance, dealer finance, dynamic discounting) is outside the TReDS scope.

Conclusion

India’s invoice financing ecosystem in 2026 is sophisticated, well-regulated in its formal tier, and increasingly accessible even to smaller businesses across geographies and sectors. The platforms profiled here — from RBI-licensed TReDS infrastructure to AI-powered fintech lenders — collectively address the full spectrum of receivables financing needs that Indian businesses face. The challenge is no longer whether invoice financing exists; it is knowing which platform is structurally best suited to your business model, buyer profile, and financing requirement, and then moving quickly enough to let your receivables work as hard as the business that earned them.