In the grand tradition of Indian business scandals, a new chapter has been written. It’s not quite as dramatic as the Harshad Mehta securities scam of the 1990s, nor as internationally embarrassing as the Satyam Computer Services scam that rocked global markets in 2009. But what the Gensol-BluSmart saga lacks in historical significance, it makes up for with sheer audacity and a particularly contemporary flavor of hubris. The story unfolding before us reveals not just individual wrongdoing but a systemic cancer eating away at the heart of India’s startup ecosystem – the normalization of what can only be called “intentional misgovernance.”

The tale begins, as so many modern startup stories do, with a genuinely appealing premise. Who wouldn’t want to support an all-electric ride-hailing service promising to challenge the Ola-Uber duopoly while simultaneously saving the environment? It’s the perfect pitch for our climate-anxious, monopoly-wary times. The Jaggi brothers – Anmol and Puneet – launched BluSmart while already running Gensol Engineering, a listed company initially focused on solar energy. On paper, this was a natural extension of their green business portfolio. In reality, it appears to have been the beginning of an elaborate shell game played with investor money, government loans, and public trust.

Between 2023 and 2024, the Jaggi brothers managed to convince several government institutions – including the Indian Renewable Energy Development Agency (IREDA), Power Finance Corporation (PFC), and Rural Electrification Corporation (REC) – to hand over an astonishing ₹975 crore (approximately $130 million). The money was meant to finance the purchase of 6,400 electric vehicles to build out BluSmart’s fleet.

Only 4,704 vehicles were actually purchased. The remaining 1,696 phantom cars – and the substantial funds allocated for them – seemingly vanished into thin air. Or rather, as SEBI would later discover, they disappeared into the private coffers of the Jaggi family enterprises. “The company’s funds were routed to related parties and used for unconnected expenses, as if the company’s funds were promoters’ PIGGY BANK,” the regulatory body would later note with barely concealed disgust.

This pattern of treating public companies as private cash reserves is hardly new in India. In fact, it has a storied history dating back to the license-permit raj era when industrialists regularly siphoned money from their companies into personal accounts. What makes the Gensol-BluSmart case particularly noteworthy is how it combines old-school scam with new-age startup theatrics. The brothers weren’t content merely to divert funds; they had to construct an entire Potemkin village to maintain the illusion of success and innovation.

In early 2025, the Jaggi brothers made a grand announcement about their fully operational EV manufacturing plant in Chakan, Pune. They claimed to have 30,000 pre-orders for their new electric three-wheeler. Press releases were distributed, social media was flooded with carefully curated images, and investors were duly impressed. The stock price soared.

But when NSE officials conducted a surprise inspection in April, they discovered something that would be comical if it weren’t so outrageous – the much-vaunted factory was nothing more than an elaborate façade, a literal movie set designed to look like a manufacturing facility from the outside. Inside was no manufacturing setup, no workers, no assembly lines – just empty space decorated with a few props to fool visitors who might be given a carefully guided tour. It was corporate theater at its most audacious.

While this farce was playing out, Gensol’s stock price skyrocketed nearly 12 times in less than a year – a classic pump-and-dump scheme where insiders and their allies profit immensely while retail investors are left holding worthless shares. A key player in this drama was one Hari Shankar Tibrewal, a Dubai-based businessman with alleged connections to hawala operations (illegal money transfers), as per ED records. If his role was as significant as indicated by the press release issued by the ED, he was not only helping inflate the stock through questionable market tactics; he was also swaying strategic choices, such as starting BluSmart operations in Dubai; as these moves made minimal business sense but offered easy pathways for international money movement.

Why Tibrewal’s role cannot be ignored in Gensol-Blusmart-Jaggi Brothers Saga? The reason is the ongoing investigation by the ED (Enforcement Directorate), India’s premier investigative agency, which declared in one of it’s press releases that “The searches also revealed that Hari Shankar Tibrewal was also involved in manipulation of stock market in collusion with the promoters of the listed companies. Hari Shankar Tibrewal, using his immense capital, used to create temporary fluctuations in share prices, driving them upwards, and then withdraw funds once the prices reached a desirable level.” For context, the ED had frozen over 500,000 shares of Gensol Engineering. These shares were previously held by Dubai-based Zenith Multi Trading DMCC, an entity linked to allegedly accused Hari Shankar Tibrewal. Investigators suspected that the shares were part of a scheme involving artificial stock price manipulation using tainted funds routed through foreign portfolio investors (FPIs).

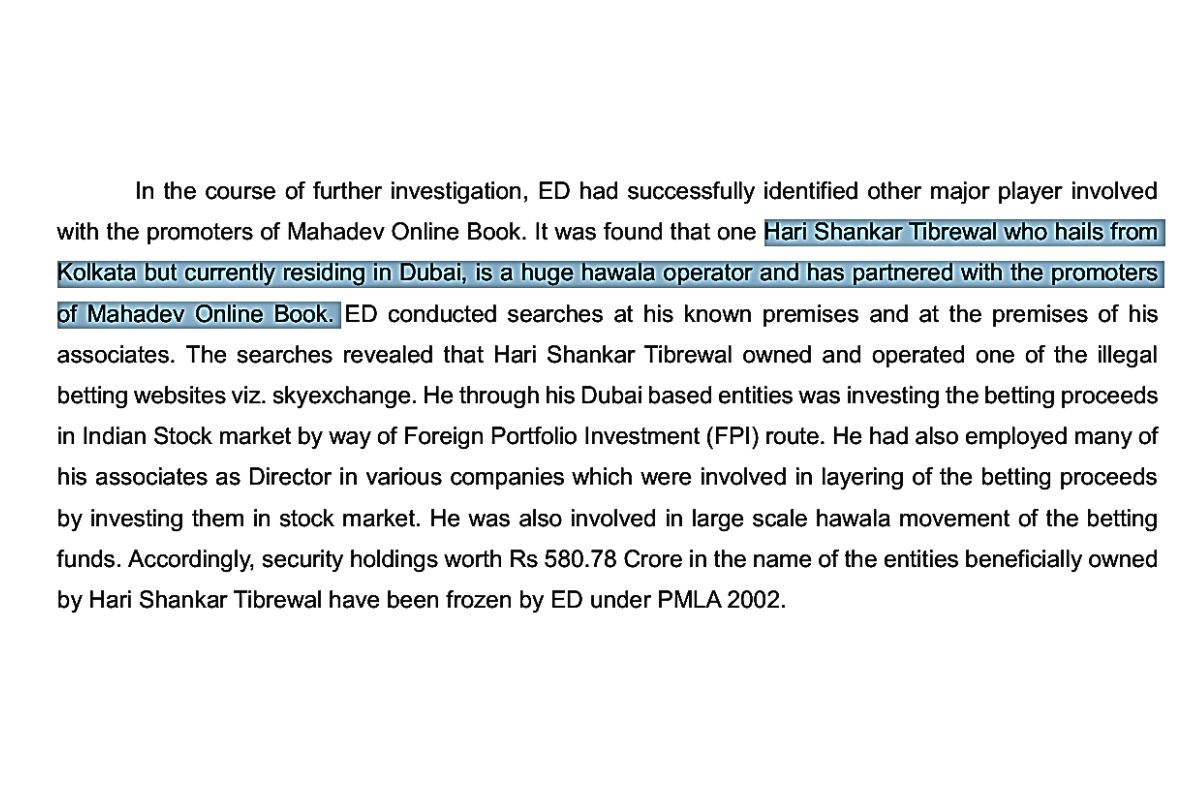

ED investigations had further revealed that one Hari Shankar Tibrewal had also partnered with the promoters of Mahadev Online Book in illegal betting operations for betting website “skyexchange”. Hari Shankar Tibrewal had laundered the proceeds of crime emanating from the betting operations through multiple companies operating both in India and outside India.

That Hari Shankar Tibrewal used Suraj Chokhani to launder and hide proceeds of crime under the guise of share investment for Indian companies. Searches u/s 17 of PMLA, 2002 conducted on 28/29.02.2024 at the premises of the associates of Hari Shankar Tibrewal including Mr Suraj Chokhani in Kolkata had revealed that the majority of source for these investments has been collected by way of receiving bank entries against cash in these companies and utilizing the proceeds for investment in share market. As on 29.02.2024, the Indian companies under control of associates of Hari Shankar Tibrewal held around securities worth Rs.580 Crore in stock portfolios . That the foreign entities also invested in India via FPI route and as on 29.02.2024 they were found to be holding securities worth Rs 606 Crore in stock portfolios.

A person against whom ED have taken actions under money laundering laws like PMLA, and have frozen assets, how can we say that his investments will not influence the decisions of the company that he is investing in? Also, if the proceeds of the crime is not suppose to have any connection with the investments in Gensol, then why, Bollywood stars, who attended the grand wedding of Mahadev Betting App owner Saurabh Chandrakar, were issued summons in Mahadev Betting App Case.

Similarly, not only Gensol, Dabur, an established name in India, was also alleged to have links as in late 2023, the Mumbai police, which was investigating the alleged ₹15,000-crore gambling and cyber fraud linked to Mahadev Book Online Betting App syndicate, registered a case against 32 persons, including Dabur Group director Gaurav Burman, company chairman Mohit Burman and actor Sahil Khan. So, we have enough ways to question whether Hari Shankar Tibrewal, who is a ‘hawala operator’ (as said by ED) do not have influence on decisions of Gensol-Blusmart-Jaggi Brothers saga???

Meanwhile, the actual BluSmart business was crumbling beneath the weight of this financial chicanery. Executives began quitting in droves, ride numbers were dropping precipitously as vehicles went unmaintained, and employees reported not receiving salaries for months. In perhaps the most telling indication of the company’s true trajectory, BluSmart – which had positioned itself as a disruptor to the ride-hailing industry – began quietly negotiating to partner with Uber, the very company it was supposedly “disrupting.”

When the house of cards finally collapsed, SEBI’s investigation revealed a pattern of systematic scam: Anmol Singh Jaggi had diverted Gensol funds to purchase a luxury apartment in The Camellias in DLF Gurgaon (one of India’s most expensive residential properties); ₹200 crore had been channeled to a car dealer that was merely a front for redirecting money back to private Jaggi-owned entities; forged documents had been submitted to banks and regulators; and a publicly listed company had been run like a family business with no regard for corporate governance or fiduciary responsibility.

The consequences were swift and severe – at least by Indian standards, where corporate wrongdoers often escape meaningful punishment. The Jaggi brothers were banned from the securities market and removed from management positions. Gensol’s stock crashed, employees lost jobs, and investors lost crores. Yet, despite this textbook scam, you can still find LinkedIn posts and Twitter threads hailing the Jaggis as “visionaries” who simply made “a few mistakes while scaling.” This phenomenon – the continued glorification of failed entrepreneurs despite clear evidence of malfeasance – is itself worth examining, as it points to deeper dysfunctions in how we assess business success in India.

There is a fascinating historical parallel in the case of Harshad Mehta. Mr. Mehta is still somewhat of a folk hero in some quarters, even though he masterminded one of the biggest securities scams in Indian history, manipulated the stock market using phony bank receipts, and caused a market meltdown that destroyed millions of investor fortunes.

The 2020 web series “Scam 1992” arguably lionized him further, portraying him as a bold outsider challenging a corrupt system rather than someone who inflicted enormous damage on that system and the ordinary investors who trusted in it. This cultural tendency to romanticize financial criminals as rebel heroes rather than recognizing the real harm they cause helps create an environment where the next generation of scamsters feels emboldened rather than deterred.

More recent examples abound. Consider the case of famous controversial shark Mr Ashneer Grover, co-founder of BharatPe, who was ousted amid allegations of financial irregularities and abusive leadership. Despite the scandal, Grover maintained a substantial public following and quickly rebranded himself as a startup guru and angel investor. Or think of Rahul Yadav, the Housing.com founder notorious for his unprofessional behavior, including publicly insulting investors and resigning in spectacular fashion. Rather than being shunned for his antics, Yadav became something of a cult figure in startup circles – the “bad boy” founder who wasn’t afraid to speak his mind.

These are not isolated events. They are signs of a widespread mindset in India’s startup ecosystem that prioritizes quick expansion and individual wealth acquisition over ethical leadership and sustainable business practices. The expression “fake it till you make it,” which has evolved from a harmless self-help maxim to a corporate tactic of purposeful deceit, nicely encapsulates this way of thinking. The underlying motivation for founders is to portray success at any costs, despite the fact that the truth is often less spectacular. The pressure to present a perfect narrative to investors, employees, and the public creates fertile ground for the kinds of misrepresentations and outright lies that characterized the Gensol-BluSmart saga.

This brings us to the deeper and more disturbing truth revealed by the BluSmart controversy: in India, companies are often poor, but promoters are rich. This paradox exposes a structural and moral flaw; a system where personal wealth accumulation by founders takes precedence over the health, sustainability, and even survival of the enterprise itself. When media and investors glamorize and pedestalize such promoters – often “preachers without morals” – the message being sent to an entire generation is deeply corrosive: that success is defined not by value creation or ethical leadership, but by the ability to raise funds, build hype, and cash out quickly.

The historical roots of this mindset can be traced back to the license-permit raj era when businesses often succeeded not through innovation or operational excellence but through political connections and regulatory arbitrage. While economic liberalization in 1991 was supposed to change this paradigm, old habits die hard. Many of the business practices that define today’s startup ecosystem – the preference for related-party transactions, the blurring of lines between company and promoter assets, the emphasis on valuations over profits – have their ancestry in the family business model that dominated Indian commerce for generations.

What’s changed is merely the packaging. Today’s startup founders speak the language of Silicon Valley – dropping terms like “disruption,” “scale,” and “hockey stick growth” – while often operating with the same old mindset that prioritizes insider wealth extraction over genuine value creation. They’ve traded the kurta-pajama for hoodies and sneakers, but the underlying approach remains distressingly similar.

Consider the case of Byju’s, once India’s most valuable startup, now mired in controversy over aggressive sales tactics, accounting irregularities, and a leadership style that many former employees describe as toxic. Despite mounting evidence of serious problems, founder Byju Raveendran was celebrated as a visionary entrepreneur right up until the moment the company began publicly imploding. Or take OYO, whose founder Ritesh Agarwal was praised for his aggressive expansion strategy even as hotel partners complained about unpaid dues and misleading business practices. Both companies saw their valuations soar while their business fundamentals remained questionable at best – a pattern that rewards hype over substance.

Such a setting makes moral action synonymous with failure or mediocrity. The current corporate narrative tends to marginalize or condemn founders who choose responsibility over ambition, openness over theatrics, and integrity over shortcuts as “too conservative.” They struggle to attract the same level of venture capital, media attention, or talent as their more flamboyant (if less scrupulous) counterparts. This creates a selection bias where the most visible “successful” founders are often those who have been most willing to bend or break the rules.

The damage extends beyond individual companies or investors. This breakdown of values vanishes public trust, poisons investor confidence, and ultimately weakens the foundation of a healthy entrepreneurial or startup ecosystem. Foreign investors, who have poured billions into Indian startups over the past decade, are increasingly wary of the governance standards (or lack thereof) they encounter. Domestic investors, particularly retail participants who often buy into IPOs with little understanding of the underlying business, repeatedly find themselves bearing the brunt of corporate misbehavior. And talented professionals who might otherwise contribute to building genuine value are either scared away from the startup ecosystem altogether or, worse, seduced into adopting the same problematic practices they see being rewarded around them.

Breaking this cycle requires more than just stronger regulatory enforcement, though that would certainly help. It demands a fundamental reimagining of what constitutes success in the business world. We need to celebrate companies that generate real profits, treat employees fairly, maintain ethical standards, and create genuine value for customers and not just those that raise the biggest funding rounds or achieve the highest paper valuations. We need media that questions the narrative rather than amplifying it, investors who perform genuine due diligence rather than following the herd, and a cultural shift that recognizes the difference between entrepreneurship and predatory behavior.

Some positive signs are emerging. The post-WeWork era has seen increased skepticism toward charismatic founders making grand promises without corresponding business results. The funding winter of 2022-2023 forced many startups to focus on fundamentals rather than growth at all costs. And a new generation of founders, witnessing the spectacular implosions of their predecessors, appears somewhat more inclined toward sustainable business practices.

Yet the Gensol-BluSmart saga reminds us how easily the lessons of the past are forgotten when temptation presents itself. The brothers Jaggi didn’t invent corporate scam; they merely adapted it for the electric vehicle era, dressing it up in the language of sustainability and innovation. Their methods were new, but the underlying philosophy – that rules are for others, that personal enrichment trumps corporate responsibility, that appearance matters more than reality – is depressingly familiar.

Until we realign our metrics of success and celebrate not just scale but substance, the cycle will repeat – companies will continue to bleed while promoters walk away wealthier than ever. The next generation of entrepreneurs is watching and learning, not just from what we say but from what we reward. If we continue to lionize those who treat public companies as personal piggy banks, we shouldn’t be surprised when more follow in their footsteps.

The Jaggi brothers may eventually face legal consequences for their actions, but the true test of whether we’ve learned anything from this episode will be whether we finally stop mistaking the accumulation of personal wealth for business success.

A healthy startup ecosystem requires more than just capital and talent; it needs integrity, transparency, and a shared understanding that the purpose of building a company extends beyond enriching its founders. Until we embrace these principles, we’ll continue to see more Scam 2025s – only the names and industries will change.

(Kindly refer to the ED press release on the below link https://enforcementdirectorate.gov.in/sites/default/files/latestnews/Press%20Release%20-%20Mahadev%20Online%20Book%20-1.3.2024.pdf)