The Haryana Real Estate Mirage: How BPTP, TDI Infrastructure, And India’s Most Controversial Builders Have Troubled Homebuyers For Decades — And Why SEBI Must Stop Their IPOs?

Introduction: The Broken Promise at the Heart of India’s Real Estate Boom

Somewhere in Faridabad, Haryana, a retired schoolteacher is paying EMIs on a flat she has never seen the inside of. In Gurugram’s Sector 85, a defence veteran holds a sale agreement stamped with promises of a handover date that passed eleven years ago. In Sonipat, 14,105 families who collectively paid Rs 4,619 crore to a single developer still have not received all the homes they were promised — nearly two decades after those projects were launched.

These are not outlier cases. They are the arithmetic reality of one of the most systematically broken industries in modern India: Haryana’s real estate sector. And at the centre of this crisis sit two companies that share more than geographical proximity or business similarity — they are bound by blood, by marriage, by a shared family network, and, by strikingly parallel patterns of financial fraud that the Enforcement Directorate is actively unwinding across Delhi-NCR and Sonipat.

Those two companies are BPTP Limited (Business Park Town Planners), chaired by the elusive Kabul Chawla, and TDI Infrastructure Limited, the flagship company of the Taneja family — Kabul Chawla’s in-laws. As of March 2026, both are under active Enforcement Directorate scrutiny. Both have had assets attached under the Prevention of Money Laundering Act. Both have accumulated mountains of criminal and civil complaints, FIRs registered in police stations across Delhi and Haryana, and court cases spanning nearly fifteen years. And yet both — astonishingly, almost incomprehensibly — are understood to be eyeing public market listings.

BPTP has been actively seeking to appoint merchant bankers for a mainboard IPO, with reports of a listing plan surfacing as recently as November 2025, just three months after the Enforcement Directorate raided its offices across Delhi-NCR in August of the same year (IPO Central, November 2025). M3M India, another Haryana builder whose promoters were arrested in 2023 under the PMLA, is similarly mentioned in industry circles as a potential FY26–FY27 listing candidate (StareEstate, 2025).

These plans must be examined with extreme seriousness by SEBI, especially in a 2026 geopolitical environment where the Iran–Israel–USA conflict has already injected profound volatility into global equity markets, and where the Indian retail investor, already exposed to bruising losses from the 2021 technology IPO wave, can least afford to absorb losses from domestically manufactured corporate fraud.

This article presents a meticulously sourced account of what BPTP and TDI Infrastructure have done to Indian homebuyers, how their family connection enabled a shared culture of impunity, and why their IPO ambitions should not be permitted to advance until every active enforcement proceeding is resolved, every homebuyer is made whole, and every court finds facts.

Part I: The Family Tie — How TDI and BPTP Are Connected Through Blood and Business

The connection between BPTP and TDI Infrastructure is not merely one of business rivals in the same market, or even of companies that share similar practices. It is familial. Kabul Chawla, the founder, chairman, and managing director of BPTP, is the son-in-law of the Taneja family — the promoter family of TDI Infrastructure. Ravinder Kumar Taneja is TDI’s managing director. By marriage, Chawla married into the Taneja business dynasty.

The significance of this family tie goes well beyond the personal. TDI Infrastructure Ltd is formally described as “the flagship company of Taneja Group,” with the senior Taneja having decades of prior experience in Haryana real estate before Kabul Chawla built BPTP from a 20-person operation in the early 2000s into a major Delhi-NCR developer.

Whether or not that specific assertion can be proved in court, the parallel structure of both companies’ legal troubles, revolving around the same pattern of FIRs, the same pattern of fund diversion, the same chronology of enforcement action, and the same political connections that allegedly enabled land acquisitions under the Bhupinder Hooda government in Haryana, makes the family connection a matter of acute public interest. The manner in which Haryana’s political patronage ecosystem fed raw land to connected developers, who then raised capital from buyers without delivering completed homes, is the foundational sin of the entire NCR real estate crisis, and both companies sit near its epicentre.

Part II: BPTP — A Chronicle of Fraud, Evasion, and Impunity

The Origin Story and the First FIR

Kabul Chawla, born in Karnal, Haryana, migrated to Delhi in the 1980s and built himself up as a property dealer in Faridabad before founding BPTP in 2003. The company grew rapidly through the mid-2000s real estate boom, launching projects including Freedom Park in Faridabad, The Park Serene in Gurgaon, Parklands, Discovery Park, and a range of township developments across Faridabad, Gurugram, and Noida. BPTP received SEBI approval in 2010 for an INR 1,500 crore IPO but deferred the plan amid weak market conditions, later buying back private equity stakes using asset sale proceeds in 2015 (IPO Central, November 2025). It is now preparing a second attempt.

What happened between that first IPO attempt and the current one is a story of catastrophic buyer betrayal compressed into fourteen years of court cases, police complaints, agency raids, and broken promises.

The first FIR against Kabul Chawla and BPTP was registered in January 2011 at a Faridabad police station. The allegation was stark and specific: BPTP had collected approximately Rs 400 crore from over 1,000 homebuyers in Sector 85’s Discovery Park project and had failed to deliver the promised flats and plots by the 2012 deadline committed in buyers’ agreements. The case fell under IPC Sections 420 (cheating) and 406 (criminal breach of trust). A Delhi court in December 2011 issued a non-bailable warrant against Kabul Chawla himself, not against a company employee, but against the chairman and managing director directly.

Chawla, by this point, had reportedly left India. Multiple publications document that he relocated to the United States, from where he has since managed BPTP’s operations via video calls and intermediaries, including his son Kabir who has handled day-to-day affairs. A Delhi court warrant was issued in December 2011. In 2026, fifteen years later, Kabul Chawla has not returned to face that warrant.

This is the most fundamental fact about BPTP’s governance:

BPTP is seeking a public listing; chaired by a man against whom a non-bailable warrant has been outstanding for over a decade, who has not presented himself before Indian courts to answer charges brought by over a thousand homebuyers, and who is alleged to be living in New York.

The Discovery Park and Park Serene Catastrophe

The scale of buyer betrayal at BPTP’s projects is documented in extraordinary detail across court records and media investigations. At Discovery Park in Sector 80, Faridabad, over 330 buyers fought for nine continuous years (2013–2022) for possession of flats they had fully paid for, with towers L and M — promised for completion by September 2020 — still incomplete as of 2022.

At Park Serene in Gurugram, approximately 400 buyers — including roughly 300 retired army officers and ex-servicemen — had paid 95 to 100 percent of the purchase price for luxury apartments. A decade after those payments, the towers remained largely unfinished and BPTP refused possession. The image of three hundred military veterans — men who served India, paid their life savings for retirement apartments, and received nothing — is among the most damning single facts in any investigation of India’s real estate sector.

In 2014, Chawla and BPTP executives were booked again, this time in Faridabad’s Sector 85 Parklands project, after buyers including Rohit and Mamta Kapoor received incomplete agreements with blank pages and still did not receive possession. In 2016, the Delhi High Court ordered FIRs after buyers sued over undelivered plots in BPTP’s SVP project in Gurgaon’s Sector 102, where each buyer had paid between Rs 86 lakh and Rs 110 lakh in 2010 — money that was taken and not returned, while the land remained undelivered six years later.

The cumulative grievance tally across all BPTP projects is documented at over 1,200 complaints since 2011. A report documented that 22 CBI-registered FIRs have been linked to BPTP’s ecosystem, including cases involving banker-builder collusion in loan fraud.

The Manhattan Penthouse and the Money Trail Abroad

Investigations into Kabul Chawla’s financial affairs have produced the kind of detail that makes the homebuyer’s plight all the more infuriating in its contrast. While buyers in Faridabad waited for flats they had paid Rs 40 lakh for, Chawla in 2012 purchased a 4,050-square-foot, five-bedroom luxury condominium on the 68th floor of the Time Warner Center in Manhattan, New York, for approximately $19.4 million (USD), using opaque Delaware-registered shell companies with a Singapore address. A New York Times investigation into foreign fund flows into top-end Manhattan real estate identified this purchase and linked it to Chawla, though Chawla denied ownership, claiming the property belonged to a cousin.

The Enforcement Directorate’s August 2025 probe has flagged this transaction as an undisclosed foreign asset — a potential violation of FEMA — and is examining whether the acquisition was funded through hawala-like mechanisms, with buyer funds from Indian real estate projects routed offshore. Reports note that the ED found evidence of “Rs 500 crore FDI routed via Mauritius shells, with put options masking hawala-like transfers”. A JPMorgan lawsuit in 2015 sought to block a transfer of this Manhattan property, an episode interpreted by observers as consistent with disputed fund flows from Indian operations.

The August 2025 ED Raids and FEMA Investigation

In August 2025, the Enforcement Directorate launched coordinated raids on BPTP’s corporate offices in Delhi, Noida, and Faridabad, as well as on the residences of Kabul Chawla and whole-time director Sudhanshu Tripathi. The raids targeted alleged violations of the Foreign Exchange Management Act (FEMA) involving over Rs 500 crore in Foreign Direct Investment (FDI) funnelled through Mauritius-based entities between 2007 and 2008. According to the ED, these funds were routed under the “automatic route” without requisite regulatory approvals and were allegedly used to acquire immovable assets abroad — including the Manhattan condominium — through anonymous foreign shell entities in which Chawla was identified as the “beneficial owner”.

Documents seized during the raids, the ED alleges, revealed a web of anonymous entities with Chawla’s fingerprints on transactions that bypassed Reserve Bank of India norms. BPTP’s spokesperson claimed full cooperation and insisted investments were made through legitimate ties to Citigroup and JPMorgan Chase entities. The ED is examining whether FEMA violations will escalate into a full Prevention of Money Laundering Act (PMLA) case — a far more serious legal jeopardy — if the offshore links and laundering mechanisms solidify sufficiently.

As of December 2025, despite being the subject of a non-bailable warrant, active FEMA proceedings, and the August 2025 raids, Kabul Chawla had not returned to India. The reason is outlined with clinical precision in reporting: US-India extradition treaties require “dual criminality” — the conduct must be criminal in both jurisdictions — and FEMA violations have historically been characterised as civil rather than criminal in US legal interpretations, making extradition difficult. His attorneys in India have filed anticipatory bails and stay petitions. A 2022 Supreme Court hearing on a related matter reportedly dissolved when Chawla’s lawyers cited “health grounds”.

Meanwhile, in a detail that encapsulates the gap between enforcement action and consequence, BPTP in early 2025 launched a new Rs 3,000 crore luxury housing project on Gurugram’s Dwarka Expressway, continuing to collect fresh capital from buyers, even as the chairman under whose oversight previous buyers’ funds were diverted remains abroad facing unexecuted warrants.

The Human Cost: Drowning Children and Suicides

No investigation of BPTP’s record can be complete without reference to the human consequences of its negligence beyond the purely financial. Elderly couples in Panchkula lost their retirement homes to failed projects and were forced into expensive rentals in their seventies.

In a May 2025 incident, residents of BPTP Park Prime and The Mansions in Sector 66 erupted in protest over what they described as a fraudulent overbuild scheme on their campus — BPTP allegedly constructing additional structures on common land that residents had paid for as open space.

Part III: TDI Infrastructure — Rs 4,619 Crore Collected, Rs 251.88 Crore Attached

The Company and Its Founding Family

TDI Infrastructure Limited, formerly registered as Intime Promoters Pvt. Ltd., is the flagship company of the Taneja Group and describes itself as having “carved a niche in self-integrated townships in prime locations across North India” (TDI official website). The company’s most prominent project is TDI City in Kundli, Sonipat — spread across 1,250 acres and described as one of North India’s largest residential developments. TDI Infrastructure has launched projects across Sonipat (Haryana), Panipat, Mohali, and Delhi, spanning residential townships, commercial malls including TDI Mall in Kundli, and mixed-use developments.

Under the leadership of the Taneja family — Ravinder Kumar Taneja as managing director, with Kamal Taneja and Akshay Taneja (the third generation, who majored in Economics from the University of Manchester) also involved in family entities — TDI expanded aggressively through the mid-2000s. Between 2005 and 2014, the company launched 23 commercial, residential, and housing projects in Sonipat alone and collected approximately Rs 4,619.43 crore in advance booking amounts from 14,105 customers across those projects.

That figure — Rs 4,619 crore from 14,105 customers — is the single most important number in understanding TDI’s record. It represents the life savings, home loans, and retirement funds of over fourteen thousand families, collected across a decade of sales. What happened to that money is the subject of the Enforcement Directorate’s current investigation.

The ED’s Finding: Funds Diverted, Homes Undelivered, 16–18 Years of Waiting

On March 6, 2026, the ED’s Gurugram Zonal Office issued a provisional attachment order under the Prevention of Money Laundering Act (PMLA) 2002, attaching immovable properties valued at approximately Rs 206.40 crore belonging to TDI Infrastructure Ltd. and its associated companies (The Tribune, March 2026; Social News XYZ, March 2026; Central Chronicle, March 2026; BizzBuzz, March 2026; DD News Government of India, March 2026). The attached assets consisted of approximately 8.3 acres of land and commercial units located in Kamaspur, Sonipat, Haryana.

This was not the ED’s first action against TDI in this investigation. Earlier in the same case, the agency had provisionally attached assets and properties worth Rs 45.48 crore belonging to TDI Infrastructure and its related entities. With the March 2026 attachment, the total value of attached assets in the TDI case reached Rs 251.88 crore (Central Chronicle, March 2026; DD News, March 2026).

The ED initiated this investigation on the basis of twenty-six FIRs registered and charge sheets filed by Delhi Police and the Economic Offences Wing (EOW), Delhi (The Tribune, March 2026). Those FIRs allege that TDI Infrastructure, its promoters, and key managerial personnel cheated and defrauded numerous homebuyers by failing to deliver promised flats and units within stipulated timelines. In one of the projects, the ED found that the delay in delivery extended to 16 to 18 years — meaning buyers who paid in 2005 or 2006 had still not received possession as of 2023 or 2024, nearly two decades later (The Tribune, March 2026; BizzBuzz, March 2026).

The ED’s investigation established the mechanism of fraud with forensic specificity. TDI’s promoters and directors diverted substantial funds collected from homebuyers to subsidiaries, erstwhile subsidiaries, and land-owning companies as advances for the purchase of land parcels and for other purposes — instead of using that money to build the homes buyers had paid for. The company also used customer funds to repay loans and make investments. This diversion of funds directly caused construction delays, preventing customers from receiving timely possession (The Tribune, March 2026; Central Chronicle, March 2026; Social News XYZ, March 2026).

As of March 2026, occupation certificates for four projects remain pending, and one project — “Park Street” — is still incomplete, its buyers waiting in a suspension of unresolved promises that has now entered its second decade (The Tribune, March 2026).

In March 2025, in a separate and remarkable enforcement action, the ED attached Rs 5.6 crore worth of shops in TDI Mall, Kundli, for environmental violations — specifically for violating the Water and Air Pollution Acts by dumping untreated sewage from projects including Kingsbury Apartments and Tuscan City onto open land.

The theory under which these environmental violations constituted money-laundering predicate offences was that the cost savings from non-compliance with environmental law constituted “proceeds of crime.” This creative but legally grounded use of PMLA to address environmental noncompliance represents an escalation in enforcement sophistication — and it speaks to the breadth of TDI’s alleged regulatory disregard, which extends beyond homebuyer fraud to the natural environment of Sonipat’s communities.

Part IV: The Wider Ecosystem — Other Haryana Builders Under Criminal and Regulatory Scrutiny

The scale of Haryana’s real estate fraud cannot be understood solely through the lens of BPTP and TDI. They are the most prominently investigated pair, but they operate within an ecosystem of similarly structured builders, several of whom have faced arrest, PMLA proceedings, or Supreme Court intervention for comparable conduct.

M3M India: Rs 400 Crore in Laundered Homebuyer Funds, Promoters Arrested

M3M India — whose promoters Basant Bansal, Roop Kumar Bansal, and Pankaj Bansal built the company into one of Gurugram’s largest luxury developers — became the subject of one of India’s most dramatic corporate arrest sequences in June 2023. On June 8, the ED arrested Roop Kumar Bansal under the PMLA, alleging that M3M had received approximately Rs 400 crore from the IREO Group through a layered network of shell companies in a transaction structured to disguise the movement of homebuyer funds between the two developer groups.

On June 14, the ED arrested Basant Bansal and Pankaj Bansal — a father and son, both directors of M3M — under a separate ECIR linked to an ACB FIR alleging that M3M’s promoters had bribed a special PMLA court judge, Sudhir Parmar, to receive favourable treatment in ongoing cases.

The IREO connection is central to the M3M story. The ED’s first prosecution complaint, filed in 2022, alleged that of 4,705 customers of IREO, almost 1,700 had not received flats or plots despite having made full payments (The Tribune, February 2025). The supplementary prosecution complaint filed in August 2023 arraigned the M3M promoters alongside 51 other managerial persons and entities of both the IREO Group and M3M Group.

The ED alleged that M3M received Rs 400 crore from IREO through shell companies, that the land notionally underlying the transaction had a market value of only Rs 4 crore, and that the balance was effectively a laundering mechanism — disguising IREO’s misappropriation of homebuyer funds as legitimate development rights payments.

The bribery dimension of the case is extraordinary even by the standards of Indian real estate fraud. The ACB FIR against special PMLA judge Sudhir Parmar alleged that he was showing “favouritism” to Lalit Goyal of IREO and to the Bansal brothers of M3M in criminal cases pending before him, in exchange for payments. Parmar was suspended by the Punjab and Haryana High Court.

His nephew Ajay Parmar was also arrested. The PMLA Adjudicating Authority in January 2024 confirmed the attachment of two immovable properties worth Rs 7.59 crore belonging to relatives and friends of the suspended judge. This is a case in which a sitting court judge hearing money-laundering cases against real estate developers was allegedly bribed by those very developers — a corruption of justice that extends the reach of Haryana’s real estate fraud into the judiciary itself.

The Supreme Court’s eventual ruling on the M3M arrests is essential context, however. The apex court, in a landmark October 2023 judgment, quashed the arrests of Basant Bansal and Pankaj Bansal in the second ECIR, finding that the ED had violated Section 19 of the PMLA in failing to communicate the grounds of arrest to the accused in a manner required by law.

The Supreme Court described the ED’s conduct as “clandestine” and said its “chronology of events speaks volumes and reflects rather poorly, if not negatively, the ED’s style of functioning”. This ruling is cited here not to vindicate the Bansals — the underlying IREO fraud investigation involving Rs 400 crore in diverted homebuyer funds continues — but because it represents the Supreme Court’s recognition that even in cases of genuine suspected fraud, the ED must follow due process. The merits of the underlying allegations remain contested and are being adjudicated.

IREO Group: Rs 1,376 Crore in Proceeds of Crime Identified

The IREO Group, whose alleged fraud was the predicate offence in the M3M case, presents perhaps the single largest homebuyer loss case in Haryana’s history. The ED identified proceeds of crime exceeding Rs 1,376 crore in the IREO investigation (Punjab and Haryana High Court, 2023 judgment — Roop Bansal v. Union of India). Lalit Goyal, owner and managing director of IREO, was arrested under the PMLA.

The FIRs against IREO alleged that the company’s directors and key managerial personnel were involved in “cheating and defrauding customers and investors against purchase of lands, plots, flats, etc.” and in “fudging of books of accounts to siphon off buyers’ money” — making false representations about possessing permissions to sell and develop the colonies while misappropriating the money collected (The Tribune, July 2023).

The IREO case has generated FIRs in 13 cases relating to two separate residential projects — “Skyon” and Floors, Plots, and Villas — and has fed into the broader Supreme Court proceedings in which over 1,200 homebuyers from NCR projects petitioned the apex court to order CBI investigation into the builder-bank nexus (The Tribune, September 2025).

Emaar MGF / Emaar India: Haryana RERA’s Most-Litigated Builder

The Haryana RERA Appellate Tribunal’s August 2025 cause list is perhaps the single most revealing document in understanding the breadth of builder-versus-buyer litigation in Haryana. The list shows “Emaar India Ltd. vs.” in dozens of consecutive entries — representing Emaar India (formerly Emaar MGF) appealing against RERA orders requiring it to refund homebuyers or pay interest for delayed possession across multiple projects (Haryana RERA Appellate Tribunal, August 2025).

The National Consumer Disputes Redressal Commission (NCDRC) case of Ramesh Malhotra versus Emaar MGF is cited in Haryana RERA jurisprudence as a benchmark for what constitutes permissible earnest money forfeiture (LiveLaw, November 2025). Haryana RERA directed Emaar MGF to refund homebuyers of its Palm Gardens project after a delay of nearly four years, with the authority noting consistent RERA norm violations.

Emaar MGF Land Limited — a joint venture between Dubai’s Emaar Properties and MGF Developments of India — operates at a different scale from BPTP or TDI and does not carry the same criminal enforcement record. However, the volume of litigation against it in Haryana’s consumer forums and RERA suggests a pattern of possession delays, unilateral maintenance charge hikes, and what the RERA authority has repeatedly described as RERA norm violations.

Ansal Townships Infrastructure: Another Chronic Offender

Haryana RERA directed Ansal Townships Infrastructure Private Limited in 2025 to hand over possession and pay interest for delay. Ansal Infrastructure has historically been among North India’s most complaint-heavy developers, with cases spanning multiple states and multiple product categories — a pattern consistent with systemic fund management failures rather than isolated project-level issues.

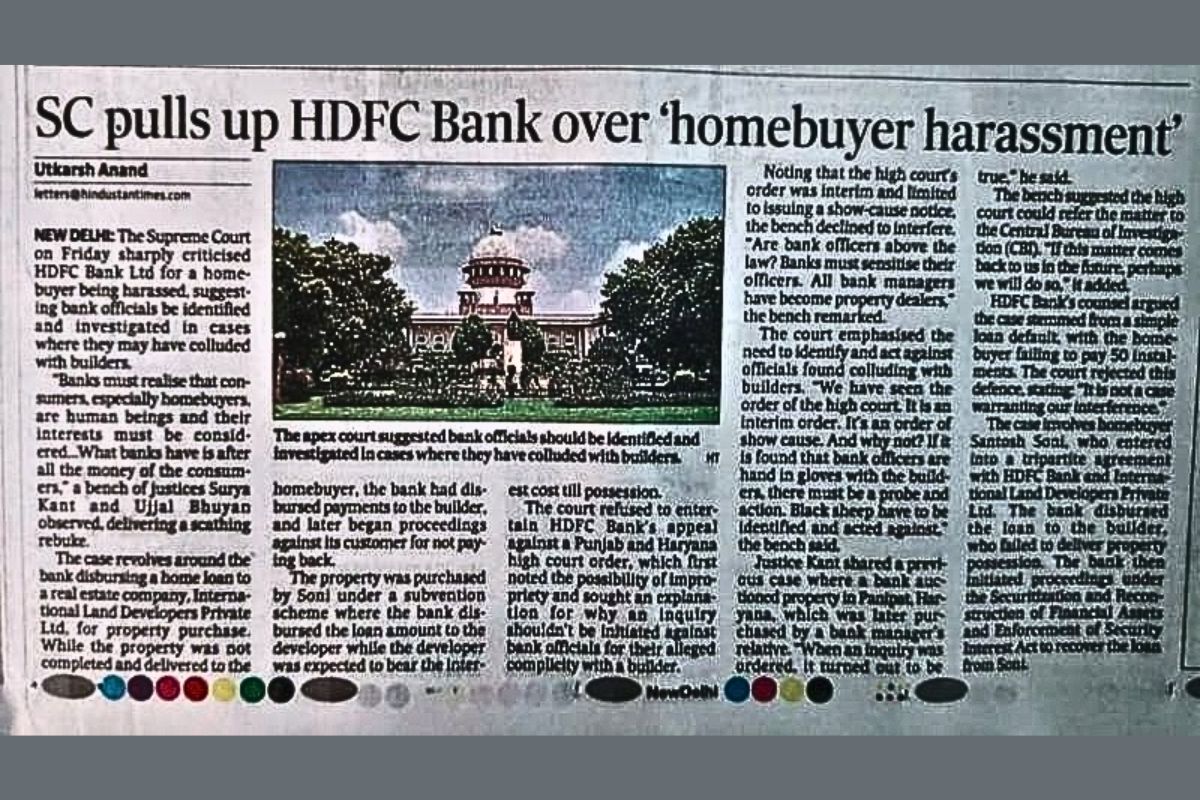

The Supreme Court’s Builder–Bank Nexus Investigation: A System-Wide Indictment

In September 2025, the Supreme Court allowed the CBI to register six additional regular cases — beyond the 22 already registered — into what the apex court described as the “unholy nexus between banks and developers” to defraud homebuyers. The court was hearing petitions from over 1,200 homebuyers who had booked flats under subvention plans in NCR projects and were being forced by banks to pay EMIs even though builders had never handed over flats.

The court found a prima facie nexus between renowned banks and builders in Noida, Gurugram, Yamuna Expressway, Greater Noida, Mohali, Mumbai, Kolkata, and Prayagraj. Under the subvention scheme, banks had disbursed sanctioned loan amounts directly to builders’ accounts — not to buyers — on the assurance that the builder would service the loan until possession. When builders defaulted, banks turned to the buyers, who had neither the homes nor any control over the money that had been disbursed to the builder. This is bank and developer fraud of a structural nature — not incidental misconduct.

The CBI had filed seven preliminary inquiries, with Supertech Ltd. described by the amicus curiae as the “main culprit” in this nexus. Corporation Bank had advanced over Rs 2,700 crore to builders through subvention schemes alone. Supertech alone had secured Rs 5,157.86 crore in loans since 1998 (The Tribune, September 2025).

Part V: Why SEBI Must Not Allow BPTP or Companies Under Active PMLA Investigation to Launch IPOs?

We arrive now at the question that gives this investigation its urgency in March 2026: why does any of this matter for India’s capital markets regulator, SEBI?

The answer has two distinct dimensions: the immediate and case-specific, and the systemic and structural.

The Immediate Case: BPTP’s IPO Plans Are Premature by Any Standard of Investor Protection

BPTP has been actively engaging merchant bankers to plan its mainboard listing, with reports from November 2025 noting that the company is “sitting on a 45–50 million sq ft land bank and plans to roll out projects worth about INR 10,000 crore annually” and has reported revenues of approximately Rs 3,000 crore in FY25 (IPO Central, November 2025). The CEO quoted in those reports spoke confidently of the company’s prospects, declining to comment on listing specifics.

What CEO Manik Malik did not address — and what any SEBI examiner of a prospective BPTP DRHP must address — is the following documented reality as of March 2026:

The company’s chairman and managing director, Kabul Chawla, is the subject of a non-bailable warrant issued by a Delhi court in December 2011, against which he has not appeared. The company is under active Enforcement Directorate investigation for alleged FEMA violations involving Rs 500 crore in improperly routed FDI, with raids having been executed in August 2025 and documents and lockers seized.

Multiple FIRs under IPC Sections 420 and 406 remain active against the company and its directors at police stations across Delhi-NCR. Over 1,200 homebuyer complaints since 2011 remain unresolved, with court cases pending across Delhi, Haryana, and Consumer Forums. The chairman is believed to be residing in the United States and has not appeared in Indian legal proceedings for over a decade.

Under SEBI’s ICDR Regulations, a company applying for a mainboard listing must make disclosures of outstanding litigations that could materially affect the business or represent a misappropriation of company assets. Active PMLA and FEMA investigations are categorically material — they directly threaten the company’s ability to operate, affect its asset base (as TDI’s Rs 251 crore in attachments demonstrate), and reveal the financial character of the promoter group.

SEBI’s observation letter process is not designed to certify the investment — but it is designed to ensure that buyers of shares in the public market are given full, complete, and honest information.

The question is whether BPTP’s DRHP, if filed, could honestly represent the full extent of its criminal and regulatory jeopardy, its promoter’s fugitive status, and its pending homebuyer liabilities, without that disclosure being so damning that the issue price would become impossible to sustain.

SEBI also has the power to reject or return a DRHP where active proceedings by regulatory or enforcement agencies are underway that could materially affect the issuer. PMLA proceedings — which can result in asset confiscation — represent exactly this category of existential financial risk. Allowing a company under active PMLA attachment to list creates a class of public shareholder who is, in effect, an unsecured creditor to homebuyer victims who have prior claims on the company’s assets.

The Geopolitical Context: March 2026 Is the Wrong Moment for High-Risk Listings

The Iran–Israel–USA conflict has, in early 2026, injected historic volatility into global equity markets. Indian equity markets have not been immune — the interconnection of global capital flows, oil price sensitivity (India imports approximately 85 percent of its crude oil requirements), and risk-off sentiment among foreign institutional investors has created a market environment in which retail participation is vulnerable to sharp downside moves in newly-listed, untested, or governance-challenged stocks. This is precisely the market environment in which promoter-driven IPOs with poor governance records inflict the greatest damage on retail investors — who are typically the last to receive information and the last to exit when things deteriorate.

The lesson of the 2021 technology IPO wave — where Paytm fell 27 percent on its listing day and never recovered to its issue price, where CarTrade Tech fell 76 percent from issue price and its 100 percent OFS structure meant not a single rupee went to the company — should not need to be learned again at the retail investor’s expense. In 2026, with additional geopolitical uncertainty layered on top of existing domestic governance failures, the case for SEBI to exercise its powers of scrutiny with maximum rigour is, if anything, stronger than it was in 2021.

The Structural Case: SEBI’s Obligation to Treat Pending Criminal Proceedings as Disqualifying, Not Merely Disclosable

The broader systemic argument is this: India’s SEBI ICDR framework treats pending criminal proceedings against promoters primarily as a disclosure obligation — the promoter must disclose the case in the DRHP, and the market can then price the risk. The implicit assumption is that the market’s information-processing capacity is sufficient to adjust valuations appropriately once the disclosure is made.

This assumption is empirically refuted by the Indian IPO market’s track record. Retail investors, who are allocated a substantial portion of every mainboard IPO, demonstrably do not process long-form risk disclosures in prospectuses with the sophistication that the disclosure model assumes.

The SEBI observation letter, as this publication has documented in earlier investigations, carries a halo of legitimacy with retail investors that it is not intended to carry. When BPTP’s eventual DRHP discloses — as it must — that its chairman has a non-bailable warrant outstanding, that the company is under FEMA investigation for Rs 500 crore, and that over 1,200 homebuyer complaints are pending, retail investors subscribing to its IPO in a bull run will not fully internalise these risks. They never have.

SEBI must evolve its framework to treat active PMLA and FEMA proceedings against promoters and companies as presumptive disqualifications pending their resolution — not merely as disclosures to be noted in fine print and forgotten by listing day. This is the structural reform that would protect retail investors not just from BPTP and TDI, but from the next generation of promoters who have learned from Kabul Chawla’s template that Indian capital markets are an exit vehicle available regardless of what you have done to your prior customers.

Conclusion: The Mirage Must Not Become a Listed Stock

In Haryana’s real estate market, between Faridabad’s Discovery Park and Sonipat’s TDI City and Gurugram’s Park Serene, there exists a geography of broken promises so extensive that it constitutes a social crisis, not merely a legal one. Tens of thousands of families — schoolteachers, army veterans, engineers, retired civil servants — have poured their life savings into homes that either don’t exist, were built without occupancy certificates, or were delivered decades late with none of the promised amenities. The money they paid built other things: Manhattan condominiums, diverted land acquisitions, loan repayments to banks, and the legal fees of attorneys fighting to keep promoters from accountability.

The Enforcement Directorate, in March 2026, provisionally attached Rs 251.88 crore of TDI Infrastructure’s assets. In August 2025, it raided BPTP for alleged violations worth Rs 500 crore. The Supreme Court has sanctioned CBI investigation into 22 cases of builder-bank nexus fraud across NCR. These are not peripheral or historic cases — they are live, current, and escalating.

Against this documented backdrop, the prospect of BPTP — and potentially M3M — launching IPOs to access India’s public markets in FY26–FY27, inviting retail investors to become shareholders in companies whose promoters are under active enforcement action, represents a risk to the Indian securities ecosystem that SEBI has both the legal authority and the moral obligation to prevent. The ICDR Regulations provide SEBI with sufficient tools: the power to scrutinise the basis-of-offer-price with genuine rigour, the power to return DRHPs pending resolution of material legal proceedings, and the power to require escrow arrangements protecting homebuyer claimants’ rights before any new capital is raised from the public.

The Haryana real estate mirage has cost Indian families incalculable amounts over two decades. The least that SEBI can do is ensure it does not also cost Indian retail investors their share market savings.

This article constitutes a public interest analysis. Nothing herein should be construed as investment advice, a determination of guilt in any criminal or civil proceeding, or a final finding of fact. All allegations against BPTP, TDI Infrastructure, M3M, IREO, Kabul Chawla, and their respective promoters and directors are allegations as investigated and reported by enforcement agencies and credible media — they remain subject to due process and legal adjudication.