How HDFC Bank Is Harassing The Homebuyers Over EMI Subvention Scheme? Historical Evidence Where HDFC Banks Were Caught In Harassment Of Their Customers.

The smell of fresh paint and the promise of new beginnings – this is what most Indians associate with buying their first home. But for thousands of homebuyers across the country, that dream has turned into a waking nightmare, and at the center of many of these stories sits one name: HDFC Bank. What emerges from court records, regulatory penalties, and consumer complaints is a disturbing pattern that raises fundamental questions about how one of India’s largest private banks treats the very people whose deposits fuel its operations.

The subvention scheme was supposed to be a bridge between dreams and reality. Under this arrangement, builders would pay the interest on home loans until they delivered possession, allowing buyers to move into completed homes without the burden of paying EMIs during construction delays. It sounded perfect, almost too good to be true. As it turns out, for many HDFC Bank customers, it was exactly that – too good to be true, and the consequences have been devastating.

This is where the Supreme Court marks its entry.

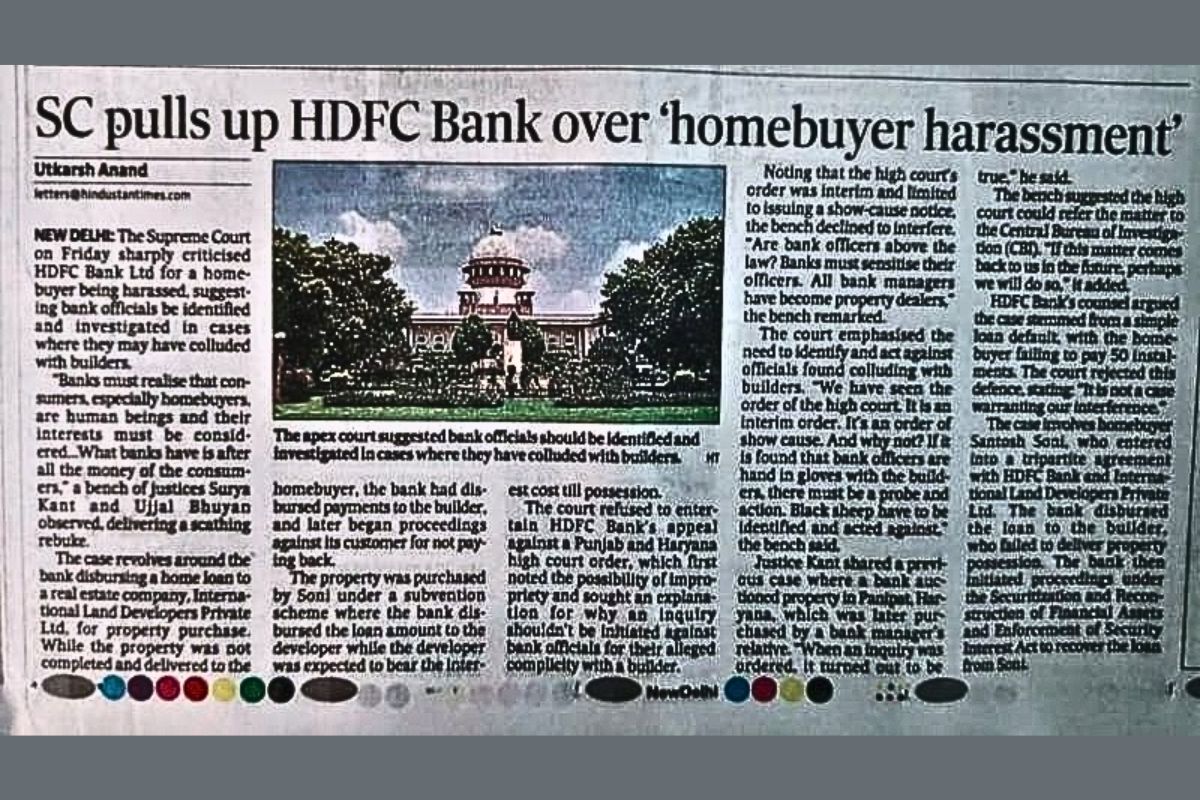

When the highest court in the land takes time to deliver what can only be described as a scathing rebuke to a major financial institution, it should make everyone sit up and take notice. In November of last year, the Supreme Court didn’t just criticize HDFC Bank; it essentially accused the bank of operating like a property dealing racket rather than a responsible financial entity. The words used by Justices Surya Kant and Ujjal Bhuyan were not the measured language typically associated with judicial pronouncements; they were the words of judges who had seen enough.

“Are bank officers above the law? Banks must sensitise their officers. All bank managers have become property dealers,” the bench remarked. This wasn’t casual criticism; this was a judicial body expressing deep concern about systemic corruption within one of India’s most trusted financial institutions. The case that prompted this response involved homebuyer Santosh Soni, whose experience with HDFC Bank‘s subvention scheme reveals the troubling mechanics of how these arrangements actually work in practice.

Soni had entered into what should have been a straightforward transaction. Under the subvention scheme, HDFC Bank disbursed loan amount directly to International Land Developers Private Ltd, while the developer was supposed to bear the interest cost until property possession. The developer failed to deliver the property, but the bank had already released the funds. When Soni found himself stuck with an undelivered property and mounting financial obligations, HDFC Bank’s response was to initiate recovery proceedings against him rather than the developer who had actually received the money.

The Punjab and Haryana High Court found prima facie evidence of collusion between bank officials and the builder, noting that “the officials of respondent No.1/Bank and respondent No.2/Builder seemed to be hand in glove, resulting in the property not having been handed over to the loanee and recovering the amount of loan from him while the amount having been paid to respondent No.2/Builder.” This judicial finding suggests something far more disturbing than simple negligence; it points to a deliberate scheme where bank officials may have been working with builders to defraud innocent homebuyers.

Justice Kant’s reference to a previous case where a bank manager’s relative purchased auctioned property, and subsequent inquiry confirmed the impropriety, is pressurising us to believe that this may not be an isolated incident where such malprices have taken place. The suggestion that the matter might be referred to the Central Bureau of Investigation indicates the court’s belief that what they were seeing might constitute criminal activity rather than mere civil disputes.

What We See When We Dig Deeper, Is A Pattern of Predatory Recovery Practices!

The subvention scheme debacle might be dismissed as an isolated problem if it weren’t for HDFC Bank’s documented history of aggressive and often illegal recovery practices. The Reserve Bank of India has repeatedly penalized the bank for violations that go far beyond technical non-compliance; but they represent a systematic disregard for customer rights and regulatory guidelines designed to protect vulnerable borrowers.

In September of the previous year, the RBI imposed a penalty of Rs 1 crore on HDFC Bank specifically for recovery agent violations. The central bank’s inspection revealed that the bank’s recovery agents were contacting customers outside the stipulated hours of 7 AM to 7 PM, disrupting their privacy and causing what the RBI termed “inconvenience” – a bureaucratic understatement for what many customers describe as harassment that affects their work, family relationships, and mental health.

The case of Yash Mehta, a Mumbai resident and business consultant with Ernst & Young, illustrates how HDFC Bank’s recovery practices can spiral into something resembling extortion. Mehta began receiving threatening calls from recovery agents over a relative’s Rs 3,500 EMI default, a relative he claimed never to have met. The agent, identifying herself as Neha, didn’t limit her harassment to Mehta but extended it to his father and grandfather, verbally abusing elderly family members over a debt they had no connection to. What made this disgustingly disturbing was the agent’s access to personal family details that should only have been available to the bank, suggesting either a serious data security breach or intentional misuse of customer details!

The psychological trauma of such malpractices and harassments by the HDFC bank cannot be ignored. When bank employees call customers’ elderly relatives, threatening and abusing them over debts they didn’t incur, it represents a form of financial terrorism that extends far beyond legitimate debt recovery. The fact that this happened over a relatively small amount of INR 3,500, suggests that HDFC Bank’s recovery machinery operates with little regard for proportionality or human dignity.

This fraud by HDFC bank is not only limited to Capital of India, but the impacts of malpractices and harassments of customers and homebuyers have taken a root to the Financial Capital of India as well.

Take Another Example- The Maharashtra RERA Ambernath Scandal: Forged Documents and Fraudulent Loans

Perhaps the most disturbing recent revelation came from the Maharashtra RERA investigation into the Ambernath scandal, where HDFC Bank allegedly emerged as a central figure in what investigators describe as systematic fraud. The accusations suggest that the private sector titan HDFC bank sanctioned home loans on the basis of forged documents, paving the way to raise fundamental questions about its due diligence processes and internal controls.

One of the homebuyer Palvinder Singh’s allegations paint an even more darker picture of institutional complicity that goes far beyond negligence! Singh claims that HDFC Bank officers Abdul Wahab Ahmed Usmani and Udaybhan Yadav facilitated fraudulent loans despite clear documentation issues. When Singh halted his EMI payments in August 2024 and demanded compensation for his financial losses, the bank’s response was brutally shameful; rather than investigating his concerns or addressing the alleged fraud, recovery agents Anthony Barneto, Mukesh Agarwal, and Siddharth Karnavat allegedly launched what Singh describes as an intimidation campaign.

The tactics employed like threatening property auctions and harassment through automated calls, suggest a bank more interested in silencing complaints than addressing legitimate grievances. Singh’s decision to give evidence to authorities and demand a full investigation has been met with “continued silence” from HDFC Bank, fueling suspicions that the banking titan has something significant to hide.

This case is particularly disturbing because it suggests that HDFC Bank’s problems with subvention schemes may be part of a larger pattern of fraudulent lending practices. If banks are sanctioning loans based on forged documents, it means that innocent buyers are being trapped in financial obligations for properties they may never receive, while developers and potentially corrupt bank officials profit from the scheme.

A Decade of Regulatory Violations: The KYC Harassment Campaign

HDFC Bank’s relationship with customer harassment extends back over a decade, revealing a consistent pattern of using bureaucratic processes as weapons against their own customers. In April 2013, the RBI had to specifically instruct HDFC Bank to stop creating its own “Know Your Customer”, KYC verification rules after the bank became the subject of “innumerable customer complaints about harassment to resubmit KYC documentation.”

The concept of harassment through paperwork might seem relatively benign, but for customers who have already completed proper documentation, being forced to repeatedly resubmit the same paperwork represents a form of bureaucratic torture. Customers reported being forced to visit branches multiple times, take time off work, and in some cases travel significant distances to resubmit documentation that the bank had no legitimate reason to request again.

What makes this particularly irritating is that more than a decade later, in March 2025, the RBI imposed another penalty of Rs 75 lakh on HDFC Bank for non-compliance with KYC master directions. This suggests that despite regulatory intervention, public criticism, and customer complaints, the bank has learned little and changed less. The persistence of these violations over more than a decade points to institutional culture problems rather than isolated incidents.

The Foreign Exchange Fraud Cover-Up

In 2019, the RBI fined HDFC Bank Rs 1 crore for failing to report frauds and non-compliance with other regulatory directions. The violation specifically pertained to forged bill of entries submitted by importers for foreign currency remittance – a serious matter involving potential money laundering and trade finance fraud. The fact that HDFC Bank failed to report these fraudulent submissions raises disturbing questions about whether the bank was complicit in the fraud or simply negligent to the point of enabling criminal activity.

Banking regulations require financial institutions to report suspected fraudulent activities not just to protect themselves, but to protect the integrity of the entire financial system. When banks fail to report fraud, they become unwitting (or willing) accomplices to criminal enterprises. The RBI’s penalty suggests that HDFC Bank’s failure to report these incidents was serious enough to warrant significant punishment, but it also raises questions about how many other fraudulent activities may have gone unreported.

The Car Loan Account Freeze: When Banks Become Judge and Jury!

The National Consumer Disputes Redressal Commission case from September 2024 shows another disturbing aspect of banking titan HDFC’s customer treatment. The commission found the bank responsible for deficiency in service by placing a hold on a customer’s savings account funds, which resulted in his car loan installment bouncing. The bank’s response to what may have been a simple administrative issue was to essentially freeze the customer’s access to his own money, creating a cascade of financial problems.

The commission’s decision to award INR 50,000 in compensation for “mental agony and harassment,” along with INR 5,000 in litigation costs, suggests that the customer’s suffering was significant and that the bank’s actions were found to be deliberately punitive rather than administratively necessary. When banks start using customers’ own deposits as cushion in disputes, it displays a disgusting breach of the trust relationship that banking depends, opeartes and exists upon.

What Is The Human Cost of Institutional Callousness?

Behind each regulatory penalty and court case lies a human story of broken dreams, financial stress, and psychological trauma. When banks like HDFC use their institutional power to harass customers, the impact extends far beyond the immediate financial consequences. Families are torn apart by financial stress, elderly relatives are subjected to verbal abuse, and young homebuyers find their dreams of homeownership transformed into legal nightmares.

The particularly disturbing aspect of HDFC Bank’s pattern is how it seems to target the most vulnerable moments in people’s lives. Homebuying represents one of the most significant financial decisions most people ever make, often involving life savings and decades of future earnings. When banks exploit this vulnerability through schemes that benefit builders and bank officials at the expense of innocent buyers, they are essentially profiting from people’s dreams and desperation.

The recovery practices documented in various cases suggest a bank that views its customers as adversaries to be conquered rather than clients to be served. When recovery agents call elderly relatives, when banks freeze accounts to force compliance, when customers are pursued for money that was disbursed to defaulting builders, it reveals an institutional mindset that prioritizes short-term profit over long-term customer relationships and ethical business practices.

Regulatory Response: Isn’t This Too Little, And, Too Late?

While the RBI has imposed multiple penalties on HDFC Bank over the years, the persistence of similar violations suggests that these punitive measures may be insufficient to change this harassing institutional behavior of HDFC. The amounts involved typically ranging from Rs 75 lakh to Rs 1 crore may represent little more than a cost of doing business for an institution of HDFC Bank’s size and profitability.

The real question is whether regulatory authorities are prepared to take more serious action when banks repeatedly violate consumer protection guidelines. The Supreme Court’s suggestion that matters might be referred to the CBI indicates that judicial authorities may be losing patience with regulatory approaches that seem to have little deterrent effect.

Consumer protection in banking cannot be achieved through periodic fines alone. It requires institutional accountability, changes in corporate culture, and consequences significant enough to make banks think twice before engaging in practices that harm their customers. The pattern of violations at HDFC Bank suggests that current regulatory frameworks may be inadequate to protect consumers from institutional bad actors.

The Broader Implications for Indian Banking

HDFC Bank’s troubles with consumer harassment and regulatory violations cannot be dismissed as the problems of a single institution. As one of India’s largest private sector banks, HDFC’s practices influence industry standards and customer expectations across the banking sector. When such a prominent institution repeatedly violates consumer protection guidelines, it sends a message to other banks about what they can get away with.

The subvention scheme problems highlighted in recent court cases point to systemic issues in how banks and builders cooperate in real estate financing. If banks are more interested in maintaining compromising relationships with builders than protecting the interests of individual homebuyers and customers, it suggests that current regulatory frameworks may be inadequate to address conflicts of interest in real estate finance, which is giving birth to builder-bank nexus.

The international reputation of Indian banking also suffers when major institutions are found to be engaging in practices that would be considered unacceptable in more mature financial markets. Foreign investors and international partners evaluate Indian banks not just on their financial performance, but on their governance standards and customer treatment practices.

At The End, What We Need Is The Need For Institutional Accountability.

The documented pattern of consumer harassment, regulatory violations, and questionable business practices at HDFC Bank represents more than isolated incidents or administrative failures. It suggests institutional problems that require more than cosmetic fixes or periodic regulatory penalties to address effectively.

The human cost of these practices, broken dreams, financial stress, family trauma, and lost trust in the banking system cannot be measured simply in rupees and regulatory penalties. When banks forget that they exist to serve customers rather than exploit them, they undermine the social contract that makes modern banking possible.

The Supreme Court’s harsh criticism, multiple RBI penalties, and growing number of consumer complaints tells us that HDFC Bank stands at a junction of industry titan and ethical standards. This forces us to ask will the bank continue with business practices that prioritize short-term profits over customer welfare, and will be facing increasing regulatory scrutiny and potential criminal investigation? Or it can undertake the fundamental cultural and operational changes necessary to restore customer trust and regulatory confidence.

For Indian homebuyers and banking customers more generally, the HDFC Bank case gives a cautionary tale that consumers must remain vigilant even when dealing with seemingly reputable institutions. The dream of homeownership should not become a nightmare of harassment, fraud, and institutional indifference. But until banks face consequences serious enough to change their behavior, customers must protect themselves through careful documentation, persistent advocacy, and willingness to seek legal redress when their rights are violated.

The story of HDFC Bank’s consumer practices is still being written. Whether it becomes a cautionary tale of institutional accountability or continues as a saga of regulatory ineffectiveness will depend largely on how seriously authorities take the mounting evidence of systematic customer abuse. For the thousands of customers who have suffered under these practices, justice delayed has already become justice denied. The question now is whether institutional accountability will follow, or whether the pattern of harassment and exploitation will continue under the protective umbrella of regulatory tolerance.