Urban Company: An Unprecedented Success Story in Home Services

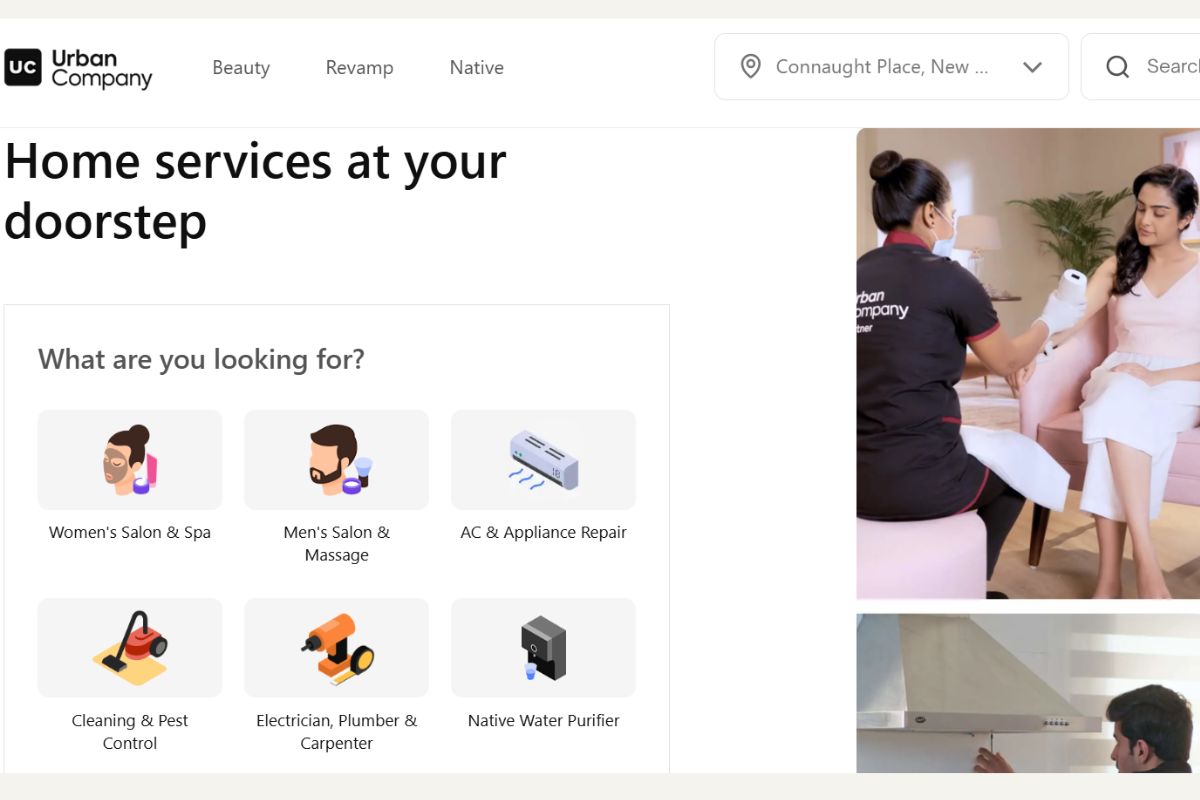

In India’s vibrant startup ecosystem, Urban Company has emerged as a shining example of how to build a venture-backed business with grace, class, and sustainable fundamentals. Founded in 2014 (as UrbanClap) by Abhiraj Singh Bhal, Varun Khaitan, and Raghav Chandra, Urban Company is a technology-driven marketplace for at-home services ranging from beauty and spa treatments to appliance repairs and home cleaning. Over the past decade, it has grown from a scrappy Gurgaon startup into Asia’s largest home services platform, all while navigating challenges that few companies anywhere in the world have managed to overcome.

Now, with its recent IPO filing, Urban Company has once again proven why it deserves a round of applause. The company not only delivered robust growth and its first full-year profit in FY2025, but also chose to value itself conservatively for its public debut, signaling a rare commitment to investor fairness.

At a time when many high-profile startups chase growth at the expense of profitability, Urban Company stands out for achieving both scale and profits. In the fiscal year ended March 2025 (FY25), the company recorded operating revenues of ₹1,144 crore, marking a 38% year-on-year growth. More importantly, it swung to profitability posting a net profit after tax of ₹240 crore for FY25, a dramatic turnaround from a loss in the previous year.

Lets see why Urban Company’s IPO plans have been met with excitement, and even veteran investors are lauding it as perhaps “the best VC-funded company to have come out of India” in recent years.

Strong Financial Performance in FY25

Urban Company’s financial results for FY25 reveal a business firing on all cylinders. The company’s operating revenue jumped 38.2% year-on-year to reach ₹1,144 crore. This growth was broad-based, driven by a post-pandemic surge in demand for home services and the company’s expansion into new categories and geographies. Urban Company operates in 48 Indian cities and has also ventured into international markets like the UAE, Singapore, and Saudi Arabia. Notably, Indian operations contributed ₹997 crore to the FY25 topline, while international markets brought in ₹147 crore, showing that the company’s core market is still India, but with a promising ~13% of revenue now coming from abroad.

What truly sets FY25 apart is that Urban Company turned profitable for the first time. According to the annual report and IPO filings, the company reported a net profit of ₹239.8 crore in FY25. This profit figure was bolstered by a deferred tax credit of about ₹211 crore, which the company booked due to accumulated past losses now turning into future tax assets. Even without this one-time tax gain, Urban Company achieved a pre-tax profit of roughly ₹28 crore, a testament to improved operational efficiency and cost discipline.

In other words, the core business itself moved into the black, after years of investments and refinement. For context, in FY24 the company had posted a net loss of ₹92.7 crore; thus, FY25’s profit marks a significant milestone. This makes Urban Company one of the very few Indian unicorn startups to become profitable before its IPO, bucking the trend of cash-burning tech IPOs.

A closer look at the revenue streams shows a well-diversified business model beyond just matchmaking consumers with service professionals. About 65% of the operating revenue in FY25 came from what Urban Company calls “platform services”, essentially the commissions or marketplace revenue from facilitating home service transactions.

This core segment contributed ₹742 crore in FY25, up 32.5% from the previous year. Urban Company’s platform oversaw 6.8 million service orders during the year across 17 categories ranging from salon treatments to pest control. The total gross transaction value of services rendered via the platform was an impressive ₹3,115 crore in FY25, highlighting how much business flows through its ecosystem. The company earns a cut of these transactions, and with scale, that has become a healthy revenue engine.

In addition to the core platform fees, Urban Company has built ancillary revenue streams that are growing rapidly. One such stream is its “UC Plus” annual membership program for customers, which provides benefits like discounted visits and priority bookings. Membership fees brought in ₹98 crore in FY25, a modest 7.7% rise from the previous year, indicating a steady base of loyal customers willing to pay for the subscription service. Another area is product commerce where Urban Company sells various tools, consumables, and products both to its network of service professionals and directly to customers.

For example, beauticians and handymen on the platform buy supplies (like beauty kits or hardware tools) through Urban Company’s supply chain. These B2B product sales to service partners contributed ₹188 crore in revenue in FY25. Meanwhile, Urban Company has also started developing its own consumer durables under the “Native” brand, most notably, a line of smart water purifiers that it markets to homeowners via its platform. Sales of Native water purifiers surged more than threefold to ₹116 crore in FY25, up from just ₹29 crore in FY24.

This indicates strong early traction for Urban Company’s foray into branded products, which leverage the company’s direct access to customers’ homes. Together, these product-related revenues (to partners and consumers) accounted for roughly ₹304 crore, or over a quarter of the total operating income, providing a nice boost to the top line and diversifying the business beyond pure services.

Urban Company’s total income was further augmented by ₹117 crore of other income (primarily interest on funds and gains from mutual fund investments). Including this, the total income for FY25 came to ₹1,261 crore. This additional income reflects prudent cash management by the company, essentially earning returns on the venture capital funds raised in prior years. The presence of non-operating income also helped Urban Company’s bottom line.

On the cost side, Urban Company demonstrated remarkable discipline, which is a key reason it could turn profitable even as it grew 38%. Total expenses in FY25 were ₹1,223 crore, up only about 20% from ₹1,021 crore in FY24, a much slower growth in costs compared to the 38% jump in revenue. Two of the largest expense heads, employee benefits and advertising/promotions, were flat or unchanged year-on-year. Employee expenses stood at ₹350 crore, almost identical to the previous year’s spend.

This figure includes a substantial non-cash component of ₹72.5 crore in ESOP (employee stock option) costs, indicating the company continued to reward employees with stock without ballooning cash salaries. Marketing and business promotion expenses were ₹207 crore, the same as FY24, despite the sizeable growth in business. In effect, Urban Company managed to support 38% revenue growth with no increase in headcount costs or ad spend, showcasing significant improvements in productivity and perhaps benefiting from word-of-mouth and repeat usage by existing customers.

This is an incredible feat in the services domain, where scaling up usually entails proportional increases in workforce and marketing. Urban Company’s ability to hold these costs steady implies that past investments in brand and tech are paying off. The platform is now running more efficiently, and the company didn’t need to throw money at customer acquisition or hiring to drive growth in FY25.

The result of rising revenues and controlled costs was a turnaround in profitability. Urban Company’s operating profit (EBITDA-level) became positive, and its India consumer services segment, essentially the domestic marketplace business, generated ₹113 crore in profit during FY25. This core segment’s ~15% profit margin demonstrates that the unit economics of the home services marketplace have matured nicely in India. Not all parts of the business are profitable yet (the newer initiatives are still in investment mode).

The company did incur losses in certain segments. The “Native” water purifier and smart devices vertical had a ₹38.7 crore loss in FY25, and the international operations recorded a ₹33.7 crore loss. These losses were more than offset by the domestic services profit engine, but they highlight where Urban Company is still building for future growth. The management appears comfortable investing in these areas (global expansion and new products) given the robust profits from the core business.

In summary, FY25 was a breakout year financially for Urban Company having strong double-digit growth, first-ever full-year profit, and healthy contributions from new revenue streams. It’s a financial profile that many startups would envy, which is a 38% growth rate with improving margins is a rare combination. As we’ll see, this solid financial footing provided a great backdrop for the company’s IPO plans and also serves to validate the resilience of its business model in a tough sector.

An IPO Filing Marked by Grace: Leaving Money on the Table

While Urban Company’s financials are impressive, what has really set tongues wagging in investment circles is the manner in which the company is approaching its initial public offering (IPO). In April 2025, Urban Company filed its Draft Red Herring Prospectus (DRHP) for a public issue of about ₹1,900 crore. According to the DRHP, only ₹429 crore of this will be a fresh issue (new capital for the company), and the remaining ₹1,471 crore will be an offer-for-sale, allowing existing shareholders to partially exit.

Notably, the founders themselves are not selling any shares in the IPO. The shares in the OFS come from early venture backers like Accel and Tiger Global, which are trimming their stakes after 8-9 years of investment. This structure sends a positive signal that the founders and management are holding onto their equity, indicating confidence in the company’s future prospects, while also providing liquidity to early investors in a controlled manner.

The real class act, however, lies in how Urban Company decided to price its IPO. The company set a price band of ₹98–103 per share for the issue. At the upper end (₹103), this implies a post-issue market capitalization in the range of ₹14,000–15,000 crore. In dollar terms, that’s roughly $1.7–1.8 billion, the valuation Urban Company is seeking from public market investors. Observers were quick to note that this figure is significantly lower than Urban Company’s valuation in its last private funding rounds. In June 2021, Urban Company had raised $255 million in a Series F round led by Prosus (Naspers) and others, at a post-money valuation of $2.1 billion.

Later, in December 2021, the company facilitated an employee stock sale (ESOP liquidity program) in which shares were transacted at an even higher $2.8 billion valuation. In other words, the private markets considered Urban Company to be worth nearly $2–3 billion four years ago, when it was still unprofitable and smaller.

Fast forward to 2025. The company has grown substantially (revenues have more than doubled since then, and profitability has been achieved) and yet the IPO is being priced at below the last private valuation. By one estimate, the IPO pricing corresponds to roughly 13 times FY25 revenues, i.e. a Price-to-Sales ratio of ~13x, which for a profitable, high-growth tech-enabled services firm is actually quite reasonable, if not modest, in the current market.

This deliberate under-valuation (relative to expectations) is virtually unheard of in the Indian startup scene, where IPOs in recent years often sought aggressive price tags. Companies like Paytm, Zomato, and Nykaa went public at rich valuations that arguably left little on the table for new investors, leading to post-listing stock corrections in some cases. Urban Company, by contrast, appears to be “keeping money on the table” for retail investors, essentially offering them a chance to partake in the future growth of the company at a fair entry price. It reflects an attitude of taking public shareholders along for the next phase, rather than squeezing out maximum valuation on Day 1.

This move has earned Urban Company a lot of goodwill. Commentators have called it a special kind of respect for retail investors, a sign of grace and class from the founders in not letting ego or short-term gains dictate the IPO pricing. It’s worth noting that the company likely could have justified a higher valuation, given its unique market position and the fact that profitable, category-leading tech companies often command premium multiples.

The choice to self-impose a lower valuation speaks to a long-term mindset. Urban Company’s leadership would rather see a strong post-listing performance and leave upside for new shareholders than grab the last dollar on the table. As one analyst quipped, “This kind of class is basically unheard of” in IPO launches.

The IPO’s valuation also underscores Urban Company’s confidence in its fundamentals. At ₹15,000 crore (~$1.8B), public investors are being offered a piece of a company that has no direct comparables and is a clear market leader in a potentially massive space. The implied 13x revenue multiple might seem high if one looks at traditional services businesses, but Urban Company is anything but a traditional services business. It’s a platform business with network effects, a strong brand, and multiple revenue levers (services, products, subscriptions) are more akin to a consumer tech company.

Moreover, given the company’s growth and profitability trajectory, that multiple can quickly be justified. Urban Company’s consolidated revenues (₹1,144 Cr in FY25) are growing ~38% YoY; if this pace (or anything close to it) continues into FY26 and beyond, the forward revenue multiple drops rapidly. Investors are essentially valuing not just the present earnings, but the future potential of Urban Company scaling across India and perhaps other emerging markets.

For context, India’s home services market was valued at around $60 billion in 2024 and is projected to reach nearly $100 billion by 2029. Crucially, only about 1% of this market is online so far. Urban Company, as the category pioneer, stands to benefit immensely from the secular trend of services moving from unorganized offline providers to organized online platforms. The headroom for growth is enormous, which is a fact likely not lost on investors who see the ₹15k crore valuation as just a starting point for a long-term growth story.

Another noteworthy aspect is how marquee investors have responded during the IPO process. We saw significant institutional interest even before the IPO opened. In early September 2025, Urban Company executed nearly ₹500 crore worth of secondary share sales to anchor investors at ₹103 per share (the top of the price band). Global funds like Permira and Prosus, as well as India’s SBI Mutual Fund, bought shares from Tiger Global and Accel in these pre-IPO transactions. The fact that such respected investors are stepping in at the IPO price, effectively endorsing that valuation is a strong vote of confidence.

These deals, done at a ~₹15,000 crore valuation, closely match the IPO’s projected market capitalization. It tells us that informed, long-term capital sees value in Urban Company at this pricing. The IPO is not about cashing out for founders (who, as mentioned, aren’t selling); it’s about bringing in new partners for growth.

By valuing itself a touch lower than its last private round, Urban Company ensured that those new partners, including retail investors in India’s market, have a reason to cheer. As the IPO opens (on September 10, 2025, per the RHP) and Urban Company transitions to a publicly listed company, it will do so with a solid base of goodwill and arguably undersold stock, which bodes well for post-listing performance.

In sum, Urban Company’s IPO approach exemplifies maturity and integrity in capital markets. At a time when startup valuations can swing wildly and public market debuts have seen both euphoria and disappointment, Urban Company’s measured strategy is refreshing. It’s the mark of a company that is confident in the long run, inviting others to join the journey on fair terms, rather than demanding a king’s ransom upfront. For this, the company has rightly earned applause. As we continue, we will examine how Urban Company’s underlying business model and market position actually justify the optimism and perhaps even suggest that the best is yet to come.

No Parallel in the Market: A Category of One

One reason investors are bullish on Urban Company, even at a billion-dollar scale, is that the company virtually has no direct competitor in India, or even globally at comparable scale. Urban Company pioneered the on-demand home services aggregation model in India, and it has maintained a leadership position for years with surprisingly little serious competition nipping at its heels. This is not for lack of trying from others; rather, it speaks to how extraordinarily hard this business is to execute, and how far ahead Urban Company is in terms of operational know-how and brand trust.

In India, several startups launched in the mid-2010s aiming to do what Urban Company (then UrbanClap) was doing, like making platforms to hire plumbers, electricians, cleaners, etc. The most notable early rival was Housejoy, which started around the same time and even secured major funding (including from Amazon). However, Housejoy struggled to find a sustainable model and eventually imploded due to various reasons (strategic missteps, cash burn, perhaps the challenge of quality control at scale). By the late 2010s, Urban Company had clearly pulled ahead, and Housejoy’s presence faded.

Other local competitors like Timesaverz, Mr. Right, Zimmber and so on either remained niche or got acquired. (Zimmber, for instance, was acquired by Quikr in 2017 but never became a national player.) Even the big horizontal tech companies sensed the opportunity but couldn’t crack it. Notably, Flipkart, India’s e-commerce giant tried to enter the at-home services space. In late 2022, Flipkart announced it would offer appliance installation and repairs via its app, leveraging its Jeeves after-sales service arm. While Flipkart’s move made headlines and certainly poses competition in the appliance servicing niche, it is largely an adjunct to their product sales (limited to services for appliances bought on Flipkart).

It does not replicate the broad, standalone service marketplace that Urban Company built. As of 2025, no one in India offers the breadth of services, geographic reach, and depth of platform integration that Urban Company does. The company provides a one-stop app to book anything from a haircut at home to a pest control visit, with standardized pricing, vetted professionals, and a satisfaction guarantee.

The trust and convenience Urban Company has cultivated among urban Indian households is a formidable moat. It’s telling that even years after Urban Company’s rise, one can hardly name a “number two” player in the organized home services space in India. The company’s name itself has become synonymous with getting a reliable service professional at your doorstep.

Globally, home services is often described as the “holy grail” of consumer tech – many have attempted it, but few have succeeded profitably. In the U.S., startups like Handy and Thumbtack tried to build similar platforms. Handy was eventually acquired by Angi (formerly Angie’s List/HomeAdvisor), and Thumbtack remains private but regionally focused. Angi Inc., which is perhaps the closest analogue to Urban Company in concept, operates the largest home services platforms in the U.S. (it connects homeowners with contractors and service pros).

However, Angi’s model is more of a lead-generation marketplace (with advertising and leads sold to contractors) rather than the full-stack, end-to-end managed service model Urban Company employs. Moreover, Angi has had a turbulent journey as it reported over $1.1 billion in revenue in 2024 but has struggled with profitability, even showing net losses in recent years. The challenges of ensuring quality and consistency in home services are universal; even in developed markets, maintaining a profitable marketplace for plumbers and handymen is tough.

That Urban Company achieved what many Western and Chinese startups couldn’t, a scaled, profitable home services platform that puts it in a league of its own. There really isn’t a direct comparison for Urban Company anywhere in the world; no other company has built this kind of services marketplace with similar scale and financial profile.

So, what has Urban Company done differently that sets it apart? The company’s approach has been extremely hands-on and operationally intensive, something many pure tech-focused founders avoid. Urban Company realized early that just aggregating supply (listing lots of service providers) wasn’t enough; it had to deeply involve itself in training, standardization, and quality control to deliver a reliable experience. The company established training centers for service professionals, created standardized menus of services and prices, and enforced quality checks. It even helped service partners with access to genuine spare parts and products (hence the ₹188 Cr sales to partners in FY25).

Essentially, Urban Company built its own “service force” where thousands of gig workers who, while not employees, are vetted and in some ways nurtured by the platform. This high degree of operational control is costly and complex, but it ensures that when a customer books a service, the experience is consistent. Compare this to something like cab aggregation where an Uber or Ola primarily just needs to onboard drivers and their cars, and then manage dispatch algorithms. Even that relatively simpler service saw huge quality variations and operational issues in India.

In home services, the variables multiply, Each service category is different, tools and training are needed, the work happens inside customers’ homes (so trust and safety are paramount), and the duration and nature of each job can vary widely. It’s a logistical and managerial nightmare to coordinate thousands of independent service professionals across dozens of service types, ensure they arrive on time with the right equipment, do a quality job, and behave courteously, all in a country as chaotic as India. This is why many who attempted it failed or stayed small. Urban Company not only survived, but has excelled at this execution-heavy model.

Industry insiders often quip that “aggregation of services is infinitely harder than aggregation of anything else”. To illustrate this, think about ride-hailing (cabs). How many moving parts are involved in delivering a taxi ride? Essentially, a driver with a car, the condition of the car, and the driver’s basic professionalism (often just measured in being a safe driver and perhaps not engaging in unwanted small talk). Despite this relatively limited scope, cab companies in India had a harrowing time where service quality issues were rampant, driver churn was high, and collectively over ₹35,000 crore was burned in the ride-hailing wars with Ola, Uber, and others over the past decade.

Yet, customer complaints about rude drivers or unclean cars remained common, and profitability was elusive. Now take home services, where the “moving parts” are far more complex. For a salon-at-home service, the beautician needs to be trained in multiple treatments, carry a kit of dozens of products, maintain hygiene, manage waste, and also deliver a friendly personal experience. For a plumber or electrician, troubleshooting skills are key, as is carrying the right spare parts; plus there’s the challenge of old buildings and unpredictable repair scenarios.

And unlike cab rides, these jobs can easily go awry if the person is even slightly negligent or unskilled, leading to property damage or safety hazards. Coordinating all this at scale is like operational hell. This is why, after Housejoy’s decline, no major tech player successfully replicated Urban Company’s model despite the clear market need. Flipkart’s cautious entry only into appliance services (where they have an existing foothold via Jeeves) underscores that even giants are wary of the full-spectrum services game.

Urban Company, therefore, finds itself in a rarefied position where it has the first-mover advantage, the largest network of trained service professionals (over 50,000 by some counts), and years of data and learnings that new entrants simply don’t have. Its brand stands for trust in a sector traditionally plagued by mistrust of local handymen. Customers know they can turn to Urban Company and expect a baseline level of professionalism.

This brand reputation is gold in a word-of-mouth driven market. In many Indian cities today, when someone needs a plumber or a home cleaning, the default suggestion is “just book it on Urban Company.” That kind of mindshare is extremely hard to dislodge, especially now that Urban Company has reached critical mass. It’s telling that the company could grow 38% in FY25 without increasing marketing spend, which is a sign that repeat usage and organic referrals are driving growth. It’s effectively the category creator and the category leader, with network effects that make it stronger as it gets larger (more professionals join because that’s where customers are; more customers download the app because that’s where the pros are).

From an investor’s perspective, this “winner-takes-most” dynamic in a huge addressable market is very attractive. Urban Company’s Service Addressable Market is roughly 35% of that $60+ billion home services market (since not all services can be organized), but even that subset is multi-billion dollars in potential. With only ~1% online penetration so far, Urban Company has a long runway just in India, not to mention its international forays. Importantly, it has shown that it can make money in this business, which is a feat others haven’t managed. “What Urban Company has achieved is a result of pure grit, for all practical purposes, is not a replicable business strategy.”

In other words, you can’t simply throw money or code at this problem; you need years of slog, fine-tuning operations, and weathering storms. That makes Urban Company’s lead very defensible. It also explains why the company can command a double-digit revenue multiple, because it’s not just another services company, it’s the services company that cracked a code where others failed. There is only one Urban Company, much like there is only one iconic Saravana Bhavan restaurant or one Ferns N Petals (to borrow analogies of unique businesses).

The absence of a comparable peer means investors are valuing Urban Company on its own merits, and if anything, some believe that the IPO valuation doesn’t fully price in certain hidden strengths, such as its budding consumer products arm and the quasi “salesforce” it has in its army of gig partners which it could leverage for more product offerings. Those could open additional revenue streams in the future (imagine Urban Company selling home warranties, insurance, or fintech products to homeowners through its trusted professionals as the possibilities are many). Such angles are hard to value now, which is why some argue that even 13x revenue might prove to be modest once these play out.

In summary, Urban Company stands in a category of its own, with no like-for-like rival in India and arguably worldwide. The combination of its operational excellence, scale, brand trust, and head start makes it a formidable player that is reaping the rewards of being a pioneer. The market, both customers and investors, recognizes this uniqueness, which is a big part of why the company’s story is so compelling and deserving of admiration.

Grit, Execution, and the “Dignity of Labour” Revolution

Urban Company’s journey has not just been about business success; it has also been a story of empowering workers and changing societal perceptions. In India, blue-collar service jobs (like cleaning, plumbing, beauty services) traditionally did not enjoy much respect or dignity. Workers in these fields were often informal, underpaid, and had to deal with unreliable demand and middlemen who took large cuts. Urban Company set out to change that by bringing what one might call “dignity of labour” to the forefront in this segment.

The company treated service professionals not as some anonymous gig workers, but as “partners”, providing them training, uniforms, ID badges, safety equipment, and a steady flow of clients. By aggregating demand, Urban Company enabled these individuals to dramatically increase their earnings and reliability of income. According to the company’s disclosures, an average active service professional on the Urban Company platform earned around ₹26,000 per month (as of 2024).

That is a substantial income in India for semi-skilled work, which is often higher than what an entry-level white-collar worker might make. Top performers earn even more. This income uplift has been life-changing for many barbers, beauticians, electricians and cleaners who partnered with UC, allowing them to join the formal economy and plan their finances better.

Urban Company also introduced features like insurance for service professionals, zero-interest loans for buying equipment, and skill upgradation programs. By investing in their workforce (even though they are not employees, but independent contractors), Urban Company essentially professionalized the gig work. Customers, in turn, began to value these services more and treat the visiting workers with more respect, seeing them as part of a reputable company’s network rather than random “unreliable” labour.

This is a subtle but powerful shift where one could argue that Urban Company has pioneered a cultural change in how urban Indians perceive and engage with domestic help and technicians. The term “dignity of labour” isn’t just a slogan; the platform actively highlighted success stories of its service partners, celebrating them in marketing campaigns and on social media to showcase the human side of this workforce. By doing so, they’ve helped chip away at the class divide stigma associated with such jobs.

The company’s fairness extends internally as well. Urban Company became known for its employee-friendly policies, especially regarding ESOPs (employee stock ownership plans). Over the years, it facilitated multiple ESOP buyback rounds, allowing employees to liquidate stock options and create wealth. In fact, Urban Company has enabled around ₹100 crore worth of ESOP liquidity for its team between 2017 and 2021.

In its fourth ESOP sale program in Dec 2021, valued at a $2.8B company valuation, over 940 current and former employees were eligible and many participated. The founders proudly noted that only a small percentage chose to sell (indicating employees’ faith in the company’s future), but regardless, those who did sell reaped substantial rewards. The culture of ownership and wealth-sharing at Urban Company has been cited as exemplary.

ESOPs were granted with friendly terms (like a nominal ₹1 exercise price and no expiry for exercised options), underscoring the leadership’s intent to genuinely make employees partners in success. This stands out in an environment where many startups offer ESOPs but often with onerous conditions that make them hard to realize value from.

Urban Company’s ethos of fairness also extends to how it deals with customers and service quality issues. The platform has a clear policy for reworks or refunds if a customer is dissatisfied. By standing behind the service, it built trust. It also, reportedly, has structured commission rates such that service partners take home the lion’s share of the job’s fee (often 75-80% to the worker, 20-25% to UC as commission).

This is unlike some gig platforms that have been accused of squeezing worker earnings. There have been occasional protests or discontent from service partners. For instance, some beauticians struck work in 2021 asking for better terms, but Urban Company engaged in dialogue and addressed many of those concerns, maintaining an overall positive relationship with its partner network. In an industry known for exploitation (either of workers or customers, or both), Urban Company’s reputation for playing fair with all stakeholders is a breath of fresh air.

All these initiatives have cemented Urban Company’s image as a startup that “helps everyone along the way” whether its employees, its gig partners, its customers, and even early investors (through timely exits and now a reasonable IPO price). The company seems intent on creating what Info Edge founder Sanjeev Bikhchandani might call a “lasting institution” of a company that endures and benefits society, not just a flash-in-the-pan startup. It is fitting that as Urban Company goes public, it does so with good karma accumulated over years. The goodwill among its workforce and user base is likely to translate into sustained business momentum.

Yet, amidst all this praise, it’s also important to acknowledge the challenges and risks ahead. The biggest risk arguably is that Urban Company’s success has been so tightly interwoven with the vision and grit of its founding team. Abhiraj Bhal (CEO), Varun Khaitan, and Raghav Chandra have steered the ship through tumultuous waters for over a decade, through the early struggles of scaling, the demonetization in India (which impacted cash-based local services), the pandemic (when home services were paused entirely during lockdowns), and now into profitability. Their leadership is seen as irreplaceable in the near term.

As Urban Company grows further and becomes answerable to public shareholders, the role of this founding trio will remain crucial. They have been the chief architects of the playbook that’s working. The company will need to ensure it builds a strong second line of leadership and a culture that can sustain beyond the founders’ daily involvement. This is a common concern for founder-led companies, but perhaps more pronounced here because of the sheer complexity of the business as the founders carry a lot of tacit knowledge and have been the driving force holding the complex pieces together.

Any transition or dilution of their roles would have to be very carefully managed to avoid disruptions. The good news is the IPO will bring additional capital and possibly allow the company to attract top managerial talent (with the cachet of being a listed firm). The founders have also shown foresight in many decisions so far, so one can expect them to tackle succession planning prudently. Nonetheless, investors will keenly watch how Urban Company evolves from a scrappy startup culture to a mature public company without losing its agility and customer focus.

Another challenge is continuing to balance growth with profitability. FY25’s numbers were stellar, but as a public company there will be pressure every quarter to keep improving margins and revenues. Urban Company may choose to reinvest heavily for growth (e.g., rapid international expansion or new product lines) which could dampen short-term profits. It will have to manage market expectations and communication expertly. Moreover, any major quality lapse or safety incident in its services could hurt its brand. Operating in people’s homes is a sensitive domain where trust once broken could be hard to rebuild. So far, Urban Company has managed incidents well and kept a generally clean record, but scale brings more unpredictability.

Lastly, while no formidable competitor exists today, success could yet breed competition. It wouldn’t be surprising if, seeing Urban Company’s IPO success, new ventures (perhaps started by alumni or deep-pocketed corporate houses) try to enter the fray with niche angles (say, focusing on one category like home cleaning with a twist, or trying a franchised model). Urban Company will need to stay innovative and customer-obsessed to fend off any future challengers. The introduction of InstaHelp (a quick 25-minute fulfillment for on-demand domestic help launched in March 2025) is an example of how the company keeps pushing the envelope in service convenience. It must continue such innovation to maintain its edge.

Conclusion: A Rare Gem in the Startup Ecosystem

Urban Company’s impending IPO is more than just another startup success story. It’s a watershed moment for India’s tech ecosystem. Here we have a company that ticked all the right boxes of identified a massive unorganized market and organized it, scaled rapidly yet sustainably, reached profitability before IPO, and chose an IPO path that respects new investors and long-term value creation.

Urban Company has set a precedent that high-growth startups can achieve operational excellence and need not indulge in exorbitant pricing or hype. It exemplifies building with a long-term vision and empathy for all stakeholders, be it the beautician earning her livelihood through the platform, or the customer whose life is a tad easier thanks to a reliable home service, or the investor who trusts the founders with their capital.

As Urban Company transitions into a public company, it carries with it the hopes of many. Customers hope it will expand to more cities and services; service professionals hope it will further elevate their profession; and investors hope it will become one of those “lastingly great institutions” that define their era. The company has already joined the elite club of Indian startups that have delivered both impact and returns.

In an environment where much of the narrative around startups is about skyrocketing valuations and the subsequent crashes, Urban Company’s story is refreshingly about values and value creation going hand in hand. It’s no wonder that industry observers are rooting for them. The sentiment on the street (and on social media) has been overwhelmingly positive, which is a mix of national pride (an Indian startup achieving something globally rare) and personal appreciation (countless individuals have positive anecdotes of using Urban Company’s services).

Moving forward, Urban Company will face the scrutiny that all listed companies do, but if it continues on its current trajectory, focusing on customer delight, partner welfare, and sustainable growth, it could very well become one of India’s “last institutions” in the consumer tech space, as people like Sanjeev Bikhchandani have envisioned for the ecosystem. That means a company that endures for decades, continually innovates, and becomes a household name not just for this generation but the next. The foundation has been laid with grit and grace; now it’s about scaling new heights. Given its track record, betting on Urban Company to achieve those heights doesn’t seem far-fetched at all.

In the grand tapestry of India’s startup saga, Urban Company’s tale will likely be remembered as a turning point; a point where doing good and doing well converged. As we applaud the company for what it has achieved so far, we also look ahead with optimism.

Here’s wishing Team Urban Company all the luck for the next phase of their journey. If the past is any indicator, they will approach it with the same humility, resilience, and clarity of purpose that got them here. And if they do, not only will their investors prosper, but so will millions of Indians whose lives are touched by Urban Company’s services. Hats off to that, and may the applause only grow louder in the years to come.