Banks Have Rules. So How Did Customer Data End Up On A Street Food Plate? If India’s Most Regulated Institutions Can’t Protect Data, Who Will?

A viral image of a roadside food plate allegedly made from discarded bank documents has exposed an uncomfortable truth about data privacy in India. If confidential financial records can slip so easily into public circulation, the question isn’t about rules but why they keep failing.

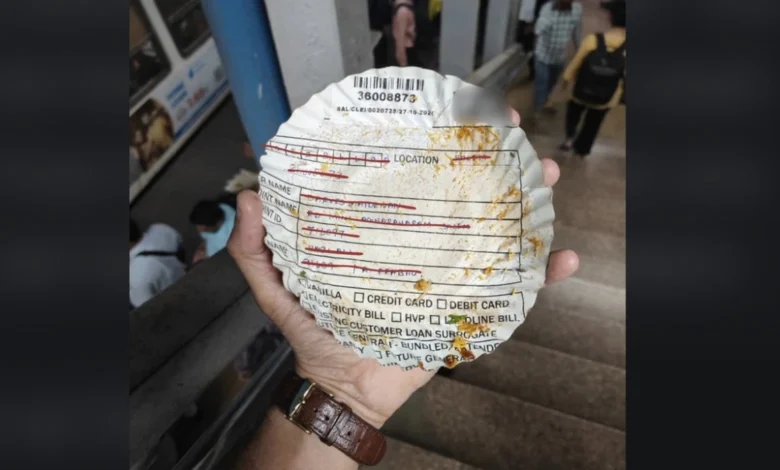

A viral image circulating on social media has reignited uncomfortable questions about data privacy in India and this time, the evidence is disturbingly tangible.

The image, shared on X by an account shows a roadside food plate allegedly fashioned from a discarded bank or financial document. The paper plate appears to still carry printed customer information, including fields showing names, locations, and payment-related details. Although some portions are scribbled out, several entries remain clearly legible.

The bottom line is this: what once appears to have been a formal financial document has found its way into everyday street commerce, stripped of dignity, safeguards, and confidentiality.

Irrespective that attempts to identify the originating bank from the viral image based on a visible number, is unlikely to yield any conclusive answer. (Indian banks do not follow a publicly traceable, standardised numbering system for internal documents and such numeric sequences are typically branch-specific or system-generated references used for file tracking, vouchers, or transaction batches).

More importantly, the larger issue is not which bank the document belonged to, but how any banking or financial record containing customer-linked information escaped mandated destruction and entered public circulation.

Once confidential data leaks into the informal economy, its provenance becomes nearly impossible to trace, yet the potential harm to individuals remains very real, illustrating a systemic breakdown in data-handling accountability rather than an isolated lapse by a single institution.

Unsurprisingly, the image triggered a wave of reactions online, ranging from shock and anger to dark humour. But beneath the sarcasm lay a serious and recurring concern – how did a document containing sensitive customer data end up being sold as recyclable paper and repurposed by a roadside food vendor?

What The Rules Say

On paper, such an incident should be nearly impossible.

Most banks in India follow structured and regulator-approved processes for handling, storing, and ultimately destroying physical records. These tasks are typically outsourced to specialised “writer companies” – empanelled vendors approved by senior bank authorities, not informal or local operators.

If documents are old but still operationally or legally relevant, they are stored in sealed boxes, categorised by date, account number, or document type. When required, banks retrieve specific files by coordinating with these writer companies, which are responsible for secure storage and controlled delivery.

If documents are deemed obsolete and fall outside mandated retention periods, the same empanelled vendors are tasked with their destruction. Shredding is often carried out on-site, in the presence of bank officials, using industrial shredders. In theory, customer confidentiality is protected at every stage.

These processes are not discretionary. They are governed by policies framed in line with Reserve Bank of India (RBI) guidelines, which clearly define how long different categories of banking records must be retained and how they should be destroyed once they outlive their utility.

Some records must be preserved permanently. Others can be destroyed after a specified number of years (often ten or more) subject to approvals and exclusions for documents linked to legal proceedings or matters that may require future reference. Banks are also required to maintain detailed records of what has been destroyed, when, and through which authorised process.

In many cases, tenders are issued to paper mills or recycling firms that meet eligibility criteria. These firms must provide formal undertakings guaranteeing confidentiality and certifying that records will be fully pulped or destroyed beyond recovery. In smaller towns, records are sometimes incinerated under supervision; in larger cities, professional destruction services convert documents into pulp using high-capacity shredders.

A Controlled Process – In Theory

Large public-sector banks, including institutions such as State Bank of India and Punjab National Bank, formally classify record disposal as a controlled activity. Internal policies, statutory retention schedules, and regulatory guidance dictate every step, from segregation and authorisation to destruction and audit verification.

RBI circulars on information security, operational risk, outsourcing, and cyber fraud explicitly require banks to protect the confidentiality, integrity, and availability of customer data throughout its lifecycle, including disposal. Internal audits, regulator inspections, CCTV monitoring, chain-of-custody documentation, and certificates of destruction are meant to ensure there are no blind spots.

For electronic records, the expectations are even stricter: secure wiping, degaussing, or physical destruction of storage media to ensure data is irrecoverable.

Yet, despite this dense web of controls, the viral image suggests a reality that contradicts the rulebook.

When Compliance Breaks Down

If even a fraction of what the image suggests is accurate, it points to a failure not of regulation, but of enforcement and accountability somewhere along the chain – be it within a bank branch, a records centre, a disposal vendor, or the recycling ecosystem.

Once sensitive documents enter informal recycling channels, audit trails collapse. Provenance becomes untraceable. Responsibility becomes fragmented. And customer data – meant to be protected under layers of policy – becomes just another raw material.

The inability to identify the originating bank from the document is itself telling. It shows how easily data, once leaked, slips beyond institutional control, even when it originates from one of the country’s most regulated sectors.

This is also where the popular assumption about “dark web data leaks” begins to fall apart. Contrary to perception, most personal data misuse in India does not originate from sophisticated hacks or shadowy online marketplaces. It begins far earlier and far closer to home – through negligent disposal, informal resale, and poorly monitored vendor chains. Once documents or databases exit formal custody, they often enter a grey market that operates openly and cheaply, long before any organised cybercrime network gets involved.

Personal Data

Now let us talk about the much larger data economy. The same systemic weaknesses that allow confidential paper records to slip into informal recycling channels also enable personal information to circulate digitally, traded casually and cheaply across India’s booming lead-generation market.

If you’ve ever wondered why your phone starts ringing the moment you buy a house, change jobs, or enquire about a loan, the answer lies in a shadowy but thriving ecosystem quietly operating across India, an informal market where personal data is bought, sold, and recycled with alarming ease.

In this market, your phone number, address, profession, income bracket, and recent purchases can be packaged and sold for as little as ₹150 to ₹300. The buyers are typically telemarketing firms, BPOs, call centres, and lead-generation agencies. The sellers range from loosely organised middlemen to individuals with access to databases that were never meant to be monetised.

At the heart of this trade is one simple truth: personal data has become cheap, abundant, and dangerously accessible.

How The Data Trail Begins

Consider the case of a young telemarketer; armed with a list of residents who had recently purchased or rented apartments in a particular housing complex. He began calling them with offers for loans, interiors, insurance, and investment products. The list wasn’t compiled through market research, it was bought.

Such lists are widely available and often categorised with striking specificity: “new homebuyers,” “recent car owners,” “parents of school-going children,” or “people who have applied for personal loans.” The more targeted the data, the higher its value – though even the most detailed information rarely costs more than a few hundred rupees.

This data doesn’t come from a single source. It flows from real estate brokers, retail stores, delivery platforms, educational institutions, hospitals, fintech apps, and even government-linked databases. In many cases, it is siphoned off by employees or vendors who see an opportunity to make quick money by selling access they were trusted with.

India’s Informal Data Economy

What has emerged is an unregulated and largely invisible “lead generation” industry. Data is collected, repackaged, and resold multiple times, often without the knowledge or consent of the individuals concerned. By the time a consumer receives their tenth unsolicited call of the day, their information may have passed through half a dozen hands.

Telemarketers admit that fresh data is the lifeblood of their business. Old lists quickly lose value as consumers block numbers or opt out. This constant demand fuels a supply chain where privacy is treated as a disposable commodity.

The consequences extend far beyond annoyance.

From Marketing To Fraud

Experts warn that the same data fuelling telemarketing is also feeding India’s rapidly growing scam economy. Fraudsters use leaked personal information to impersonate bank officials, company executives, or even family members. With the rise of AI tools such as voice cloning and deepfake videos, the risks have multiplied.

Only at this later stage does leaked data sometimes migrate into more overtly criminal ecosystems, including organised fraud rings and encrypted online marketplaces. By then, however, the damage has already been done. The original failure is rarely a dramatic breach – it is the quiet normalisation of data leakage, where information is treated as expendable and accountability dissolves across multiple hands.

A scammer armed with a victim’s name, recent transactions, employer details, and phone number can craft an alarmingly convincing plan. WhatsApp impersonation scams, fake customer-care calls, and targeted phishing attacks thrive on precisely this kind of leaked data.

In many cases, victims are left wondering how strangers knew so much about them. The answer often lies in databases that were sold cheaply and carelessly.

The Law Is Catching Up – Slowly

India’s Digital Personal Data Protection (DPDP) Act promises to change this scenario by placing stricter obligations on entities that collect and process personal data. Under the law, organisations are expected to obtain clear consent, limit data usage, and ensure secure storage. Heavy penalties have been framed for violations.

However, privacy experts caution that enforcement will take time. Many companies are still unaware of their responsibilities under the new regime, while smaller players in the data resale chain operate far below the regulatory radar. Realistically, it may take two to three years before compliance becomes widespread and meaningful.

Until then, the data trade continues largely unchecked.

The Cost of Convenience

India’s digital boom has made everyday life easier – from instant loans and doorstep deliveries to online education and healthcare. But this convenience has come at a steep cost. Personal information is routinely shared, often with little scrutiny of how it will be stored or who it might eventually reach.

In a country where data literacy remains low and accountability even lower, individuals are left exposed. Blocking numbers and opting out of calls offers only temporary relief. Once data is leaked, it cannot be recalled.

The uncomfortable reality is this: in today’s India, you are not just a consumer, you are a data point. And until stronger enforcement, corporate responsibility, and public awareness converge, your personal information will remain a tradable asset in a market that values profit over privacy.

The Last Bit, What Customers Are Left With

For customers, the implications are deeply unsettling. Banks are legally obligated to safeguard personal and financial data until its final destruction. Any loss or improper disposal of confidential records is reportable and can attract regulatory action.

In practice, however, customers often learn of such lapses only after damage has already been done – through spam, fraud, impersonation scams, or, in this case, a viral image that lays bare the fragility of data protection on the ground.

If regulated banks, armed with RBI mandates, audits, and approved vendors, cannot fully guarantee secure disposal of customer records, the question becomes unavoidable: where does accountability truly begin—and where does it end?