59 % Annual Growth In Ghost Shopping Malls: A Reminder Of Changing Customer Buying Behaviour And Need For Satisfactory Mall Experience.

India’s retail scene is a medley of different pictures, mixing the energy of high streets with the grandeur of shopping complexes. However, behind these sparkles is a story of resilience and reinvention. The industry, or at least a few poorly built and managed malls, is dealing with changing customer patterns and economic challenges. The retail sector’s issues, notably the rise of ghost malls, signify a sharp reminder of the ever-changing nature of consumer behaviour and market pressures.

As per a new study by real estate firm Knight Frank India, the number of ghost retail malls in India is rapidly increasing. According to the ‘Think India Think Retail 2024’ research, there were 13.3 million square feet of ‘ghost shopping infrastructure’ across 29 cities in 2023, resulting in a $798 million loss. A ghost shopping mall is an infrastructure with a retail vacancy rate of more than 40%. Considering the eight Tier 1 cities, the pan-India vacancy rate across all mall types was 15.7%. Furthermore, although Tier 1 cities had 271 shopping malls in 2022, the number decreased to 263 (77% of all retail centres) in 2023.

The startling 59% year-on-year growth in underperforming retail properties, culminating in over 13.3 million square feet of unoccupied space called ‘Ghost Malls,’ provides a gloomy picture of the environment.

These barren enclaves, with vacancy rates above 40%, represent a gap between established retail formats and changing customer habits. The consequences are severe, with a projected loss of value of INR 6,700 crore in 2023 alone. Unsurprisingly, India’s biggest cities face the most severe effects of this retail reckoning, with the National Capital Region (NCR), Mumbai, and Bengaluru emerging as hotspots for ghost shopping malls.

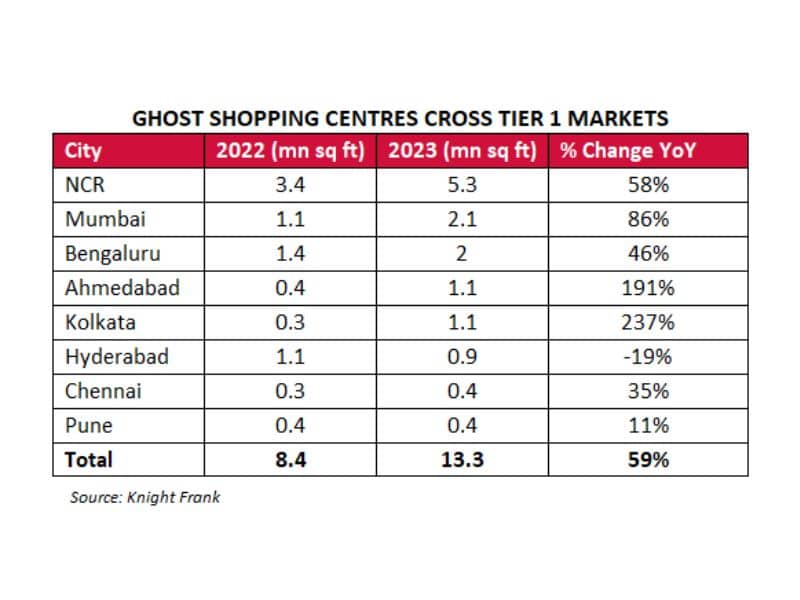

What cities have the most ghost malls?

According to Knight Frank statistics, 64 abandoned malls in eight cities include 75% of the total 125.1 million square feet of gross leasable area, GLA. According to the survey, Delhi-NCR has the highest concentration with 21 ghost shopping centres (5.3 million sq ft), followed by Bengaluru with 12 (2 million sq ft), Mumbai with 10 (2.1 million sq ft), Kolkata with 6 (1.1 million sq ft), Hyderabad with 5 (0.9 million sq ft), Ahmedabad with 4 (1.1 million sq ft), and Chennai and Pune with three each (0.4 million sq ft).

Interestingly, the number of empty commercial complexes in Hyderabad decreased by 19%. Despite eight new additions, the total number of retail centres in tier 1 cities fell year on year, with a total of 263 complexes by 2023. According to the assessment, underperforming malls were either destroyed for residential or commercial projects, permanently shuttered, or auctioned off.

Lucknow, Kochi, and Jaipur were the top three tier II cities in terms of available Gross Leasable Area in shopping malls, with 5.7 million square feet, 2.3 million square feet, and 2.1 million square feet, respectively. Lucknow is a critical participant, accounting for 18% of the total GLA in Tier II cities.

Overall, retail centre vacancies in India’s top eight cities have improved from 16.6% in 2022 to 15.7% in 2023, a drop of 87 basis points. Ghost retail Centres make up a part of the total retail mall vacancies. However, when Ghost Shopping Centres are removed from the stock in the top eight cities, shopping centre health in India improves from 7.4% in 2023, owing to the exceptional performance of Grade A assets and optimum occupancy in Grade B assets.

So, what is causing this problem of ghost retail malls and high vacancy rates? Is it because offline buying is making way for online shopping? Is it due to decreased customer demand? Or are there other industry-specific factors at play?

The need and aura of Grade A malls can be seen as one of the reasons customers prefer visiting them.

Since the 1990s, India’s mall culture has thrived, resulting in an increase in the number of shopping centre buildings. By 2023, Grade A malls accounted for 47% of the total shopping area in the country, 31% in Grade B, and 22% in Grade C. Some Grade C malls in Tier 1 cities like NCR, Mumbai, and Pune were demolished for residential construction due to increased housing demand post-pandemic.

Grade A malls continue to prosper, with strong occupancy rates and footfalls, thanks to their strategy of the proper tenant and brand mix, location, revenue share, innovation, and events that continue to entice customers. Without a mix of these qualities, Grade C assets stagnate, requiring landlords to consider options for rejuvenation or divestment.

Shishir Baijal, MD and chairman of Knight Frank India has emphasised the disparities in mall performance across grade levels. “Grade A malls have flourished, maintaining high occupancy, foot traffic, and conversion rates while providing value to their customers. In contrast, Grade C assets and ghost shopping centres are underperforming, compelling landlords to make efforts to revitalise or dispose of such buildings,” he added. The current retail trend of premiumisation, also spreading through malls, may explain why high-end shopping malls are booming. Another factor driving lower-grade malls’ demise and high-grade ones’ emergence might be a focus on consumer experience.

Another reason is the space of the infrastructure that can be magnate for the shoppers.

Retailers across categories are establishing larger brick-and-mortar locations and expanding existing ones as consumers demand a better physical shopping experience. According to Anarock statistics, the percentage of retailers smaller than 2,000 sq feet fell to 52% in the first half of 2023-24, down from 61% the previous year. During this time, the proportion of stores sized 2,000-5,000 sq ft climbed from 19% to 21%, as did those sized 5,000-10,000 sq ft (11% from 9%) and 10,000-15,000 sq ft (13% from 9%).

“The store now focuses on experience rather than merchandising. Brands have understood this, and by growing the shop, they are expanding their offering,” Pankaj Renjhen, COO and joint MD of Anarock Retail, explained.

Mall developers are increasingly focused on creating bigger malls to provide a better shopping experience. Rahul Arora, Head of Office Leasing Advisory and Retail Services, India, JLL, told a media outlet that the average size of mall developments completed in 2023 jumped by 41% from 276,800 sq ft in 2022 to 389,900 sq ft. Developers are building larger malls to provide a better shopping experience, whether for entertainment, food and drinks (F&B), or fashion.

The entry of new players can be a bit challenging.

In India, a new sort of mall is on the rise. At least half a dozen factory outlet malls are planned in India, similar to those in the USA and the UK, as retail developers try to compete with online competitors in a market increasingly driven by significant discounts. While such retail locations, where brands are given discounts throughout the year, are popular worldwide, the market remains unorganised in India. Retail will expand beyond malls and high streets, moving to highways as additional infrastructure is created.

On highways, a factory outlet mall with food and beverage options and leisure areas makes sense. Susil S. Dungarwal, creator of Beyond Squarefeet, a shopping mall specialist firm, predicts that this concept will become widespread in the next years.

Despite this instability, do estimates for the future business landscape provide a ray of hope?

Malls are anticipated to draw more than Rs 20,000 crore in investment over the next 3-4 years, with the country’s largest mall developers, DLF, Prestige, and Phoenix, entering the next phase of growth as practically all prominent retailers increase their store count, according to industry officials. As part of its development strategy, real estate giant DLF has begun building a new 26-27 lakh square feet retail mall in Gurugram at a cost of roughly Rs 2,200 crore, according to PTI in April. It is also developing a luxury mall in Goa that would be around 6 lakh square feet in size.

With potential revenues for shopping centres estimated to exceed USD14 billion by 2024-25, there is a tangible feeling of confidence about the industry’s endurance and flexibility. However, achieving this potential necessitates a deliberate effort to reinvent the role of shopping malls in the retail ecosystem. Recognising shopping malls as more than just commercial environments is critical to their evolution. They are, at their core, experiencing places that must change to satisfy customers’ shifting wants and desires.

The conclusion.

An improved shopping experience is critical in an era of increased disposable incomes and urbanisation. “The momentum of consumer demand, fueled by increased disposable incomes, a young populace, and urbanisation, favours the organised retail sector. An improved retail experience is critical for customers, emphasising the importance of physical retail locations,” says Shishir Baijal.

Furthermore, the increase in research emphasises the significance of taking proactive actions to solve the difficulties confronting India’s retail industry. This includes adopting adaptable tactics to manage the changing terrain and seize fresh possibilities. From adapting abandoned shopping malls to revitalising high streets, stakeholders must work together to create innovation and resilience in the retail sector.

Brands play an important part in this reinvention process. As customers choose experiences over transactions, marketers must take advantage of the controlled atmosphere of shopping malls to create immersive, interactive locations that appeal to their target demographic. Brands can carve themselves a distinct identity in an increasingly competitive environment by embracing innovation and putting consumer engagement first.

Finally, the future of shopping malls in India depends on their capacity to adapt, develop, and reinvent themselves as dynamic centres of commerce and experience. With proactive steps and a shared commitment to excellence, India’s retail industry can meet today’s difficulties and emerge more robust, more resilient, and more vibrant than ever before.