Given the need for faster, accessible, and easy credit in the economy, it is quite right that the digital banking sector or the credit sector is on an emphatic rise. Given the level of convenience that is being offered by the online credit industry in India, it is quite understandable that why is the industry on an emphatic rise.

In addition to the convenience and faster service, such services are also being offered cheap and are proving to be quite economical for the users. Paying an interest rate of 2.25 percent is sitting quite well with users especially when a comparison is laid between the online credit industry and the traditional banking sector.

According to the reports, many Indians are significantly turning to the burgeoning online lending sector. A major reason for the same is the immediate and significant need for cash in the economy due to the financial havoc that was wreaked by the pandemic on the individuals. According to a nationwide survey, there are effectively more than 1,200 digital lending start-ups that have cropped up across India. The high drive of the startup culture is mainly due to the burgeoning lucrativeness and share of the online credit market in India.

Factors fueling the rise of the online credit system in India

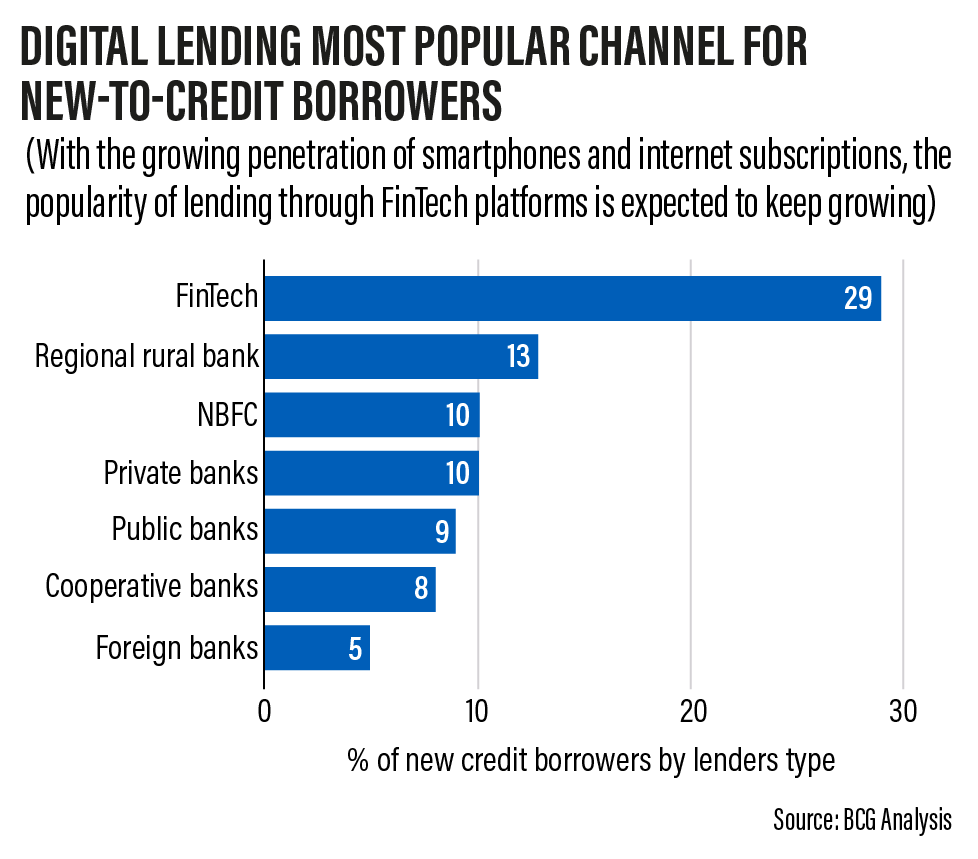

Various factors have contributed to the rise of the credit sector in India. First and foremost is the increasing smartphone ownership in India that has led to rapid digitalization not only in the urban but also rural areas of India. Secondly, the fall of the traditional banking archaic system has contributed to such a rise. It is due to the low credit card penetration in India that has led to a lesser impact on the individuals that are migrating towards the online credit industry. If statics are to be scrutinized, there are roughly about 120 million employed people in India that do not effectively own credit cards in the economy. This report was published by Inc42.

Digital India

Prime Minister Narendra Modi’s government’s policies for an emphatic push for a “digital India” have contributed towards the growth of the online credit industry in India. This necessarily isn’t such an enticing situation for Indian banks that are heavily burdened with high loan losses. This in fact is one of the contributing reasons for the increase in popularity of the online credit industry.

With high NPA loans that plague the mighty banking sector, banks have remained cautious of extending loans invariably. Given the already crippled financial situation of the nation, extending loans can be risky. Thus, taking the viewpoint into consideration, easy credit has plummeted in recent years. This has effectively opened up the various avenue for online credit start-ups. The uptick in the same has also been due to India’s online transaction boom that had materialized during the pandemic.

According to Boston Consulting Group, India’s digital retail loans market has been significantly projected to reach $1 trillion by the financial year 2024. The market will reach the value of $1 trillion in terms of total disbursements in the country.

Given all the aforementioned circumstances, the situation has effectively softened for lenders who are desperately looking to build consumer bases for their startups in the economy.

According to various analysts and experts, India is significantly poised at this point to be the leader in terms of credit pick-up. According to them, this has been accelerated by the pandemic and strong fundamentals that are driving demand and consumption in the economy.

A lucrative opportunity for international conglomerates

It is to be noted that given the humungous momentum that online credit platforms are witnessing, the sector has effectively grabbed the attention of technology companies. These technology companies include companies like Xiaomi and Facebook that are looking for opportunities to expand in the sector. According to recent trends and reports, regional, international and local conglomerates have been effectively and emphatically trying to establish a foothold in the niche market.

Amongst all other companies interested in the sector, Facebook had made its move the last month when it had joined with online lender Indifi. The association that was formed was commenced to launch a small business loans initiative in India. The small loans initiative in India effectively offered companies the liberty to advertise on social media platforms for marketing purposes. The range of the loan had roughly stretched from 5 lakh to 5 million.

In addition to Facebook, Chinese electronics maker Xiaomi is also highly interested to venture out into the online credit sector in India. It highly plans to foray into the credit cards and loans sector in India through various effective partnerships with online lenders and banks and online lenders.

According to Utkarsh Sinha who is the managing director at Mumbai-based Bexley Advisors, the online credit sector in many ways has served as an extension of the banking industry. Through its efforts, it has emphatically regularized the non-formal credit infrastructure in the country. This has been due to the extension of loans to the unbanked sectors that have been marginalized in the growth story of India.

Though, here it is to be noted that all is not as rosy as it might sound. There are some added risks that come with cheaper and flexible digital lending. Given that the digital lending space offers easy credit, background checks are usually not carried out thoroughly. This can effectively lead to the formation of the credit bubble in the economy which can wreak havoc once busted. To encapsulate the matter, it can be stated that the risk of digital lending is collateral-free, which is highly risky.

Thus, what will be the future of lending space in India is highly contentious.

Edited by Sanjana Simlai.