Agritech in India: An Overview of the Industry and Investment Opportunities

In this article, we look at the agriculture sector in India and how technological interventions by the agritech industry are increasing efficiencies and overall productivity, resulting in investment potential.

Food security has been a top worry around the world as the global population exceeds 7.9 billion in November and is expected to reach 9.8 billion by 2050. The urgency for action must also address resource shortages, distribution and access distortions, and the need to increase agricultural outputs. Policymakers around the world are increasingly looking for long-term solutions to the dilemma by leveraging technology in agricultural operations.

It has heightened interest in new agriculture technology (agritech), with agritech entrepreneurs earning $26.1 billion in funding globally by 2020. This was a 35.4 per cent increase from the last year. Between 2020 and 2027, the global agritech industry is expected to develop at a compound annual growth rate (CAGR) of 12.1%. Like China and the United States, India is a competitor.

Agritech developments are crucial to India’s economy. Its agriculture sector, valued at US$370 billion, continues to be the primary source of income for almost 40% of the population and provides 19.9% of the national GDP (FY 2021). However, despite its contribution, the sector continues to be plagued by structural flaws that stifle growth and productivity. To address these issues and increase farmer incomes, Indian agriculture requires technology-assisted modernisation backed by strong reforms – and this is where agritech is likely to play a key role.

About Agritech

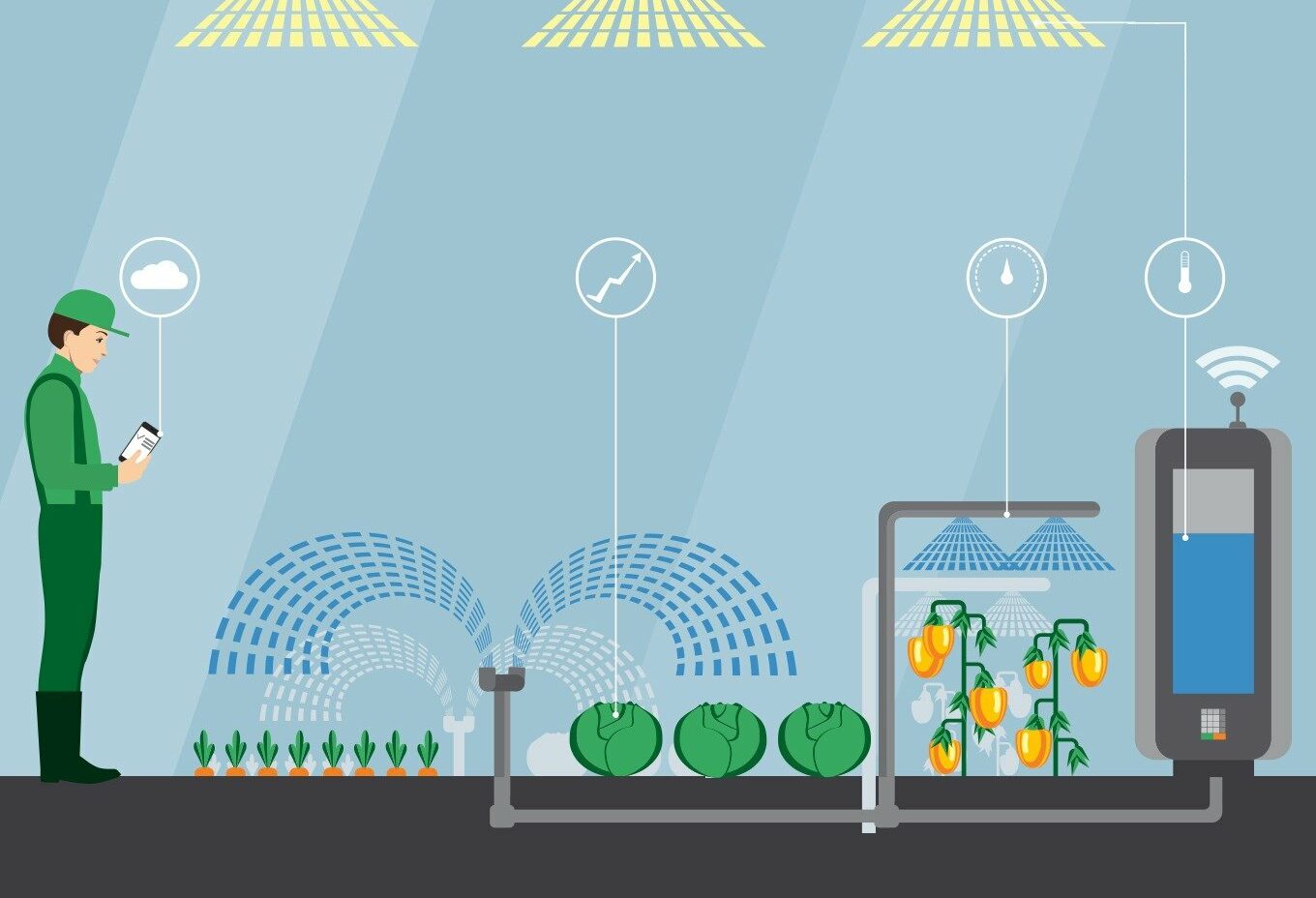

Agri-tech is the application of technology to farming to increase efficiency and profitability. Agri-tech is utilised in forestry, aquaculture, and viticulture and is most typically used in horticulture and agriculture.

Agri-tech improves agriculture by monitoring and analysing weather, pests, soil, and air temperature information. Automation is also used in agri-tech, like managing heating and irrigation and distributing aerosol pheromone for insect control.

Agri-tech technologies and applications include:

- Drones

- Satellite photography and sensors

- IoT-based sensor networks

- Phase tracking

- Weather forecasts

- Automated watering

- Light and heat control

Over 1300 agriculture startups operate in India, using artificial intelligence (AI), machine learning (ML), the internet of things (IoT), and other technologies to boost efficiency and productivity. They are presently on an upward growth trajectory due to the COVID pandemic. Agri-startups in India are concentrated in Karnataka, Maharashtra and the Delhi National Capital Region (NCR).

While the three farm bills that the agritech industry praised are being rolled back this month due to concerns raised by non-corporate stakeholders, agritech players in India will continue to push forward, aided by the pace of innovation and diverse funding, as technology solutions to long-standing challenges are urgently sought.

The Farmers’ Produce Trade and Commerce Bill, 2020; The Farmers Agreement of Price Assurance and Farm Services Bill, 2020; and The Essential Commodities Bill, 2020 – intended to help the Indian agriculture sector undergo structural change. As any Indian government will attest, policy changes with such broad repercussions necessitate long-term negotiation and co-opting of several parties. At times, political expediency can work in India, especially given Prime Minister Modi’s BJP government’s large mandate. Still, farm reforms are an electoral wedge issue, and concerns about forthcoming state elections in Uttar Pradesh have stopped his ambitious programme.

In this article, we look at India’s agriculture sector and how agritech interventions increase efficiencies and overall productivity, resulting in investment potential.

The agricultural sector’s contribution to India’s GDP:

Farming (crops and horticulture), forestry, animals (milk, eggs, and meat), and fisheries are part of the Indian agricultural economy. It holds for 11.9 per cent of worldwide agriculture gross value added (GVA) of US$3,320.4 billion and contributes 12 per cent to India’s exports, ranking second after China. Non-agricultural segments such as consumer items, retail, chemicals, and e-commerce are also affected by the sector’s consumption and production dynamics.

Due to economic interconnections, the agriculture industry is critical to India’s economic output and growth potential. It’s also why sector reforms are desperately needed. Long-term issues are broken down below.

India’s agribusiness economy is fragmented and disorganised.

From the provision of agricultural inputs to the manufacturing and transformation of agricultural goods and their distribution to final customers, the agribusiness ecosystem encompasses all business activities from farm to fork. Factors such as rapid urbanisation, diet diversification, altering customer preferences, and the expansion of food markets have moved this ecosystem to new segments like e-commerce and hyperlocal.

However, the agriculture value chain remains mainly unstructured and fragmented, with many tiers of intermediaries and middlemen. While 86 per cent of India’s small and marginal farmers continue to provide the majority of the country’s food and nutrition, they face challenges like landholdings of less than two hectares and restricted access to technology, inputs, financing, money, and markets.

Agritech innovation can address a lack of infrastructure, inefficient supply chains, and poor digital adoption that has historically prevented the sector from reaching its full potential.

How does agritech help India’s agriculture sector increase productivity and efficiency?

Agritech is a phrase that refers to a group of organisations and startups that use technological breakthroughs to develop goods or services that help farmers increase production, efficiency (both in terms of time and cost), and profitability across the agriculture value chain.

The following are the various segments of the agritech industry that support the whole value chain:

Farm inputs market linkage: A digital marketplace and physical infrastructure connect farmers to inputs.

Biotech: It research on plant and animal life sciences and genomics.

Farming as a service: Renting farm equipment on a per-use basis.

Precision agriculture and farm management: Increasing productivity through geospatial or weather data, IoT, sensors, robotics, and other technologies; farm management solutions for resource and field management, among other things.

Farm mechanisation and automation: Seeding, material handling, harvesting, and other automated tasks utilise machinery, tools, and robots.

Farm infrastructure: Farm infrastructure includes greenhouse systems, indoor-outdoor farming, drip irrigation, and environmental control systems like heating and ventilation, among other things.

Quality management and traceability: It includes post-harvest produce handling, quality check and analysis, production monitoring, and storage and transit traceability are all examples of quality management and traceability.

Supply chain technology and output market linkage: A digital platform and physical infrastructure to manage the post-harvest supply chain and connect farm output to customers is being developed.

Financial services: It include credit lines for input purchases, equipment purchases, and crop insurance or reinsurance.

Advisory/Content: Online information systems for agronomic, price, and market data.

Agritech provides the opportunity to address a variety of present pain points in the agriculture sector across the value chain, therefore expanding the market potential.

Using technology to modernise and introduce systemic efficiency in India’s agriculture sector can open up investment prospects.

This can be accomplished in a variety of ways, including:

- Facilitating input market linkages, underpinned by a solid physical infrastructure network, can address current concerns such as input price volatility and sub-optimal input selection.

- Precision agriculture can boost yield by as much as 30%.

- Farm management can increase operational efficiencies and reduce expenses by digitising documents.

- Quality management and traceability will assist farmers in achieving greater results in high-quality food, further motivating them to use new methods.

- Facilitating output market linkages through an efficient post-harvest supply chain eliminates inefficiencies like high farm food wastage, resulting in a win-win situation for farmers and consumers.

- Better financial services might benefit 30 per cent of farmer households with credit and 65 per cent of farmer households with crop insurance.

Business models in India’s agritech sector

The following are the several types of business models in the agritech industry:

- Margin-based model: This model operates in market linkage – farm inputs, supply chain technology, and output market linkage, where the agritech operator gets a margin by developing marketplace linkages on the information or output side and by delivering the promised services.

- Subscription-based model: Agritech players in areas like precision agriculture and farm management and quality management and traceability use a subscription-based model to offer a mix of hardware, software, and services-based solutions throughout the year and collect monthly or annual subscription fees from their customers.

- Transaction-based model: This is used by agritech firms that provide financial services. It is based on the number of loans or insurance policies offered.

Overview of agritech in India

During FY 2019-20, the agritech industry saw a revenue increase of around 85 per cent. According to an Ernst & Young 2020 report, the Indian agritech market has a potential worth of US$24 billion by 2025, of which only 1% has been realised thus far. This potential is estimated to be worth US$35 billion by 2025, according to another analysis by Bain & Company.

With India’s ever-increasing internet penetration and rural areas as the critical engine of this growth, the country is well-positioned to adapt to changing agricultural techniques and move from traditional business models to new innovative business models powered by agritech.

Investing in India’s agritech space

EM3, Cropin, Jumbotail, Ninjacart, DeHaat, AgroStar, Farmbee, Licious, and Zappfresh are the most prominent firms getting funding in the Indian agritech landscape.

Since 2015, investments in Indian agritech have increased by a factor of ten, with a total investment of US$242 million in 2020 (through October). The meat delivery segment of startups attracted the most funding in the agritech industry in 2020, with US$124 million, followed by the marketplace and e-distribution businesses (US$83 million).

The results for 2020 are a major departure from previous years when marketplace and e-distribution firms garnered the lion’s share of investment ($203 million out of a total of $257 million). In contrast, meat delivery businesses received only US$20 million.

Growing segments within agritech in India

Supply chain technology and output markets have the highest potential in India, worth US$12.1 billion, followed by financial services, precision agriculture and farm management, quality management and traceability, and market linkages-farm inputs (US$1.5 billion) out of a total projected agritech market potential of US$24 billion.

The following are some of the most well-known companies active in various agritech segments:

- Fasa, Bitmantis, Agronxt, and Soilsens are examples of IoT-powered agriculture and drones.

- DeHaat, Ninjacart, Jumbotail, Bijak, Farmzen are marketplaces and e-distributors.

- DeHaat, AgriBegri, AgroStar, BigHaat, Gramophone are some farm inputs available.

- Cropin, FarmERP, AgNext, and BharatAgri Precision agriculture and farm management

- AgroStar, IFFCO Kisan, RML, Farmbee, and Fasal Salah are the farmers’ advisories.

- Aggois, Niruthi, Weather Risk, Jai Kisan, Aggois, Niruthi, Weather Risk, Jai Kisan, Aggois, Niruthi, Niruthi

- Equipment leasing companies include EM3, Agri Bolo, and Tractor Bazaar.

- Licious, Zappfresh, and Pesca are some of the meat delivery services available. To Your House, Fresh

- Nebulaa, AgricX, and Intello Labs are the companies that measure crop quality.

- Drip Tech, Netafim, Cultyvate, and Soilsens are examples of intelligent farm equipment.

- Mahyco, Nu-genes, and Nuziveedu seeds are hybrid seeds.

- Fresco, Triton Foodworks, and Junga are all hydroponics companies. Absolute Foods are fresh and green.

Input market linkage and farming as a service (FaaS) segment:

In India, major players include AgroStar and BigHaat, which provide farmers with a missed call-based service for ordering inputs and equipment and a cash-on-delivery service. By collaborating directly with the producers, these companies have eliminated many intermediaries. As part of farming-as-a-service, several organisations provide services like on-demand machinery leasing, field levelling, and pesticide spraying.

Supply chain, post-harvest management, and output market linkage segment: This segment contributed the most to the agritech industry’s revenue in FY 2020 and also grew the fastest among all segments during the same year. Collection, processing, storage, logistics, and distribution of agricultural produce from farmers to end customers or merchants are all part of the segment’s activities. Inadequate rural infrastructure and a lack of traceability throughout the supply chain have pushed agritech companies to enter the market. This area is dominated by startups like Ninjacart, Waycool, and Samunnati.

Precision farming, analytics, and advisory segment: During FY 2020, this segment, which provides precision farming solutions and advisory services, grew by roughly 17%. This segment’s companies address structural difficulties caused by farmers’ lack of awareness about scientific farming practices. These companies employ IoT sensors or GIS technology to collect farm-specific data like soil, weather conditions, humidity, pests, and so on and then use their analytical capabilities to deliver timely insights to farmers. These firms are also developing quality evaluation and grading solutions for large agribusinesses and traders. In India, roughly 200-250 startups are providing similar services. Clover, Cropin, KhetiNext, Zentron, and other notable startups.

Agri fintech

Agritech startups in this area provide services including credit, insurance, warehouse receipt financing, trade financing, and so on. Farmers’ largest problem is a lack of access to organised loans, collateral, and official documentation. Agritech companies use technology like geotagging farmland and remote crop monitoring to create risk profiles for farmers and assess their creditworthiness. Agritech companies work with banks, NBFCs, and input suppliers to give loans at lower interest rates than unorganised lenders. This industry is still emerging in India, with roughly 20-40 companies now operating, with notable firms being payAgri, Jai Kisan, Aggois, and others.

Edited and published by Ashlyn Joy