Top 10 Finance Mobile Apps in India in 2022

As individuals struggle with the financial uncertainty brought on by more than a year of catastrophic economic shocks, budgeting has been front of mind for many. While a handwritten budget is entirely acceptable, budgeting apps have become a popular tool to track spending and savings habits.

Sorting through the many budgeting apps available may be difficult, especially since each has various features. Forbes Advisor has selected the best budgeting apps to help you find one right for you and your needs.

Managing your money is a challenging task. Tracking expenses and keeping track of the bank balance can be difficult now that many of us no longer balance a check. Apps for personal finance can link to your bank account and help you keep track of your expenditures. Individual finance apps can also help you track upcoming bill payments (some allow you to pay bills directly on the app), monitor your credit score, and keep track of your investment portfolio.

The top personal finance apps include various features for managing your entire finances (email reminders, bill due dates, subscription tracking, shared wallets, and so on). All of the applications on our list are compatible with iOS and Android, so you may enjoy them no matter which smartphone giant you favour.

1.Acorns App

Acorns is a computer-managed investment portfolio that regularly rounds up your purchases on linked credit or debit cards and returns the change. Call it a virtual piggy bank. College students, unassociated investors, and people who struggle to save money are Acorns’ target audiences. When it comes to selecting young, would-be investors, Acorns concentrates on college students, particularly those without earned income who cannot contribute to tax-advantaged retirement plans.

There’s always a nice chunk of money seeking for a new home after four years of “rounding up.” It might be the startup capital for your venture!

You have had the option of automatically or manually transferring your change into an investment portfolio. Acorns also have a lot of partners who offer 10% cashback when you use a linked payment method with them, like Jet, Blue Apron, Airbnb, Boxed, and Hulu. Unlike IRA and 401(k) accounts, Acorns only provides personal taxable accounts. It’s one thing to find the money. Free money, such as an employer match, is another entirely. Consequently, don’t put all your acorns in one basket — something along those lines.

2.Pocket Guard

This programme budgets how much spendable money you have after accounting for the fundamentals like payments, debt, and long-term financial goals. Pocket Guard offers tools to help you monitor your income and expenses, so you can take control of your money and even expand your savings account. It links all your accounts in one spot, giving you a complete picture of your balances and net worth.

Pocket Guard can send you offers for lower rates on financial services when you build a profile and fill out basic personal information. Based on previous purchases, the products are tailored to your preferences. Because many of our transactions are now conducted online, it can be challenging to decide how much money you have available to spend. This ambiguity can lead to overdrafts or late fees, hindering us from getting the most out of our money. Pocket Guard keeps you informed about your existing and future economic status.

It even includes visually appealing graphs that simplify identifying the areas where you overpay. You may also add hashtags to the categories to customize them. The free version should do for those searching for a simple way to keep track of their expenditures. More customization possibilities and thorough reports are available in the premium version.

3.You Need A Budget

YNAB (the app’s acronym) excels at advising users to manage their money wisely and ethically. The tutorials and educational materials are outstanding and highly beneficial. It’s designed for low-income families that only need the basics, and it’s not a tool for savvy personal finance.

Every dollar you’re expected to earn has a job assigned to it. You may either spend it or preserve it. YNAB connects to your financial accounts directly to get real-time account balances and other information. It’s a more traditional approach to budgeting, and it works well for folks who are serious about managing money.

YNAB explains its principles using tutorials and pop-up windows, as well as a checklist to the left that will help you get started. Some issues arise as you go through the process. Creating all of the unique categories required to direct your money flow is the moment. You may switch types, and YNAB has a function called “Stuff I Forgot To Budget For,” which is very useful.

4. Digit App

![]()

Digit is intended for those who wish to save money without putting forth much effort. Digit monitors your spending habits and sends money from your linked bank account to your Digit account, almost like Big Brother. What is the process behind it? Digit makes a transfer every two or three days, usually after evaluating your bank balance, anticipated income, upcoming expenses, and current spending patterns.

Digit calculates a non-essential sum based on these variables that you won’t notice based on your spending patterns. “Wait, can’t I do this on my own?” you might ask. Possibly. On the other hand, Digit is targeted at a generation that places a high value on technology and trusts it implicitly. For those people, the fee and convenience are well worth it.

In fact, for every three months that clients save with Digit, they receive a 1% yearly Savings Bonus. You’ll earn a $5 incentive if you introduce a friend to the service. Customers can use Digit’s text service, which uses SMS texting, to do routine banking transactions (such as monitoring their balance, initiating withdrawals, and viewing upcoming bills) without having to use a computer. Digit was made to create smaller savings for the tech-savvy millennial population.

5.GoodBudget App

An ancient savings approach involves physically dividing all of your cash into separate envelopes. There’s an envelope for groceries, another one for your phone bill, the other for gas, and so on. Take Goodbudget to be a collection of virtual “envelopes.” It gives the option of deciding how you want to spend and save your money. The free membership gives you a simple way of managing and tracking your money. The paid membership is best suited to those with bigger budgets.

For regular expenses like rent, groceries, and entertainment, Goodbudget gives “regular” envelopes. For annual costs, vacations, Christmas gifts, and an emergency fund, there are “more” envelopes.

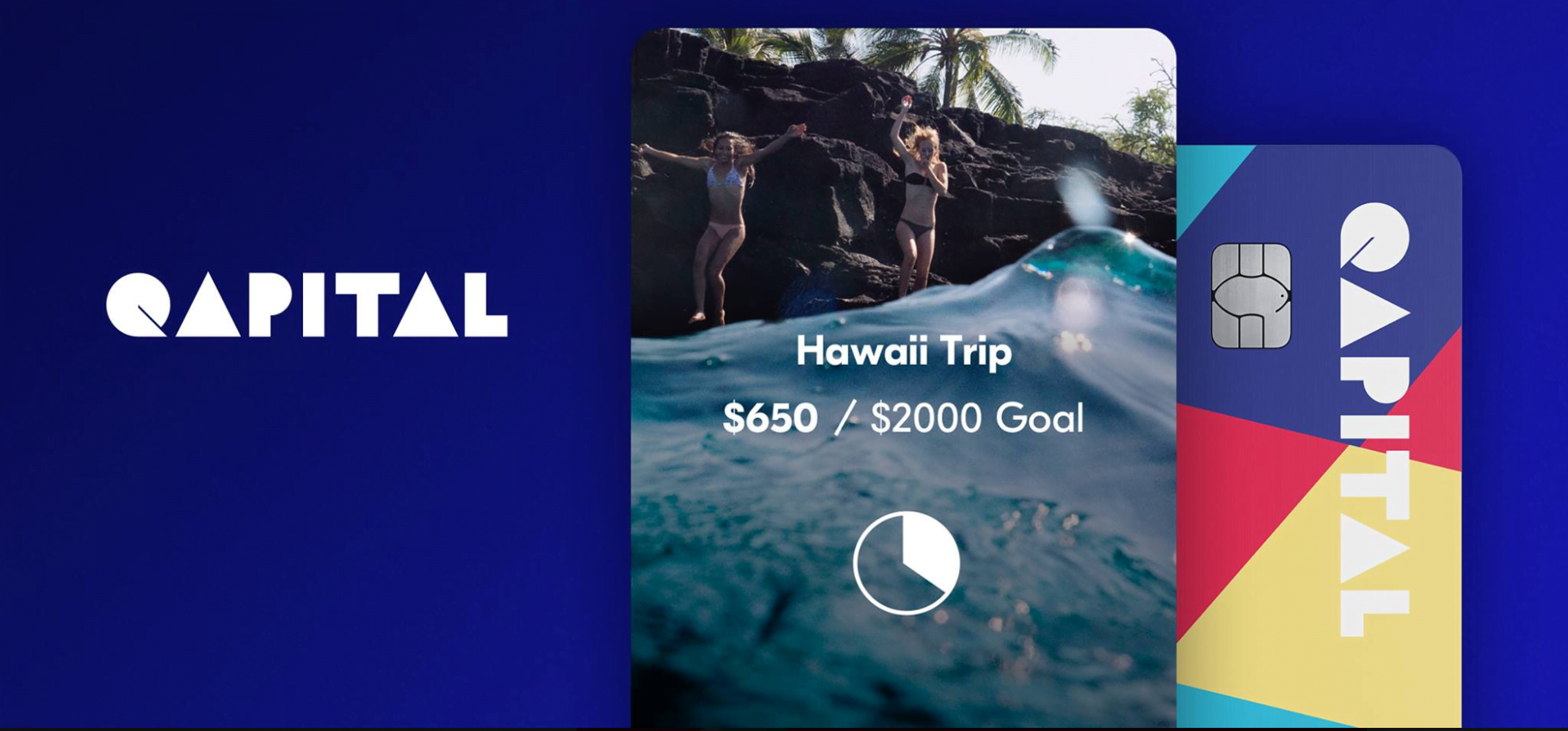

6. Qapital App

Through gamification and modest acts in everyday life, Qapital makes it very simple to save money. It does require the establishment of a new FDIC-insured account (no minimum balance or monthly service fee). And what’s the procedure? If you buy coffee every morning, Qapital rounds up the price and saves the extra. If you go over budget on something, such as food or commuting expenses, you can put the difference toward something else, like a vacation fund. You’ll be saving money in ways you never thought almost invisibly before you know it. It also synchronizes with IFTT (“If this, then that”), suggesting more ways to save.

Qapital also includes exciting features, such as asking if you want to acquire new talents, such as cooking or photography. If that’s the case, you’ll be asked to estimate how much money you’ll need, and then you’ll be led through a process that will help you find out how to save that money.

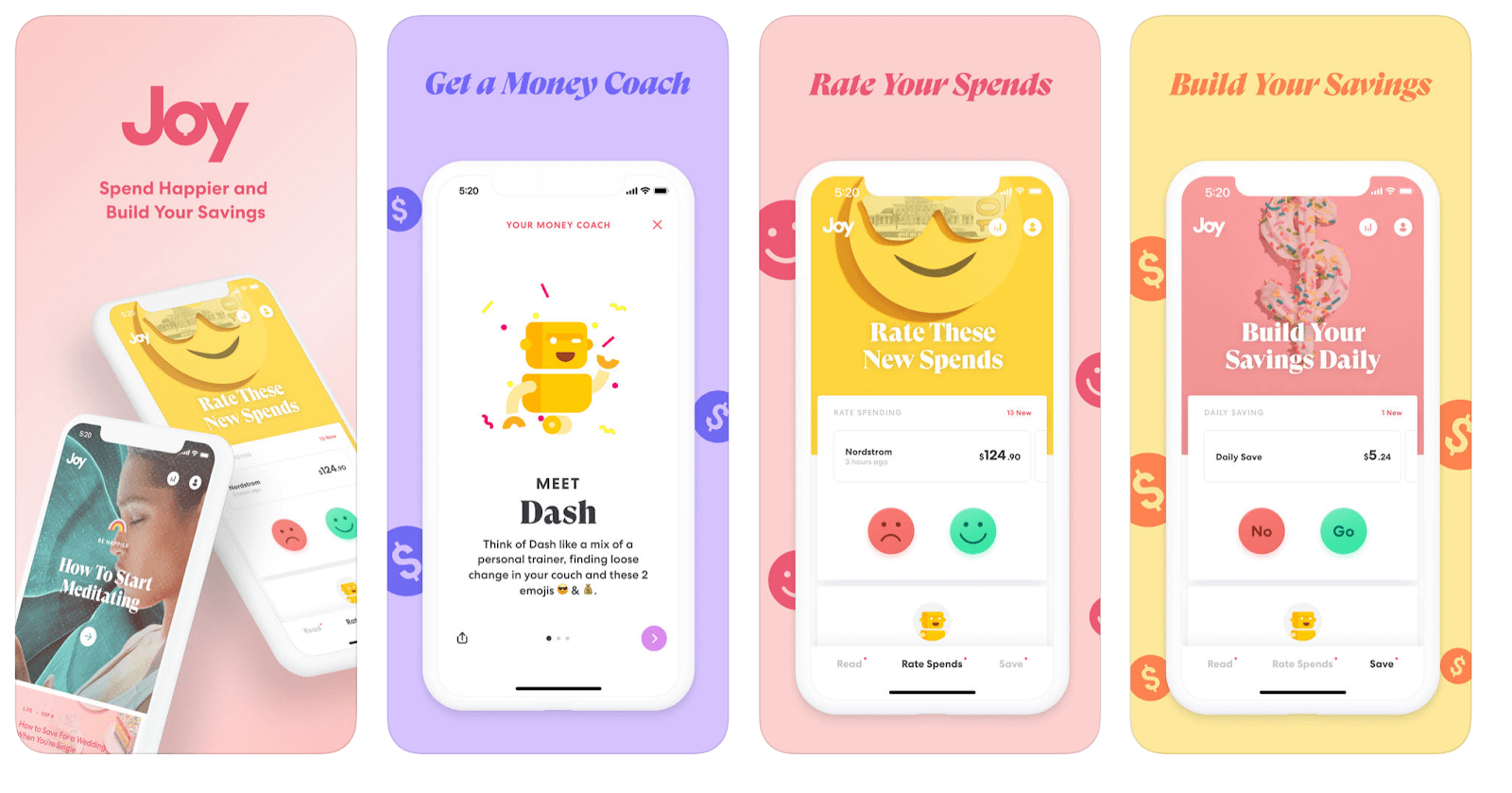

7. Joy

Joy is a savings and financial coaching app that focuses on the user’s happiness regarding purchases. After creating a profile (a checking account or credit card), the user is asked to link their spending account to the app after creating profile (a checking account or credit card). The user is then required to report on their recent spending. Joy guides how dollars and cents relate to satisfaction by asking users to rank their purchases as “happy” or “sad.” Purchases of low value (or “sad”) should be avoided, whereas purchases of high value (“happy”) are allowed.

The application seeks to assist the user in connecting spending that adds value to one’s life and spending that adds little or no value by standardizing reflection on expenditures. Joy also publishes a steady flow of up-to-date, simple financial articles. This collection of tools can assist spark savings motivation and keeping one’s goals in the front of one’s mind.

Joy users open a Joy Savings account. The app identifies savings opportunities and then sends money to the account with the user’s consent. The savings account is FDIC-insured, and customers can withdraw cash or terminate it at any moment.

8.Honeydue

Honeydue is for couples that want more honesty in their relationship, especially when it comes to money. The app is free and may be used by teams at any stage of their relationship as long as it satisfies to share financial data.

The app allows you to keep track of your money across various financial institutions, such as bank accounts, loans, and investments. Notifications and bill reminders sent at the correct time keep you on track with your payments and help you avoid late fees. Honeydue can establish a joint bank account for you and your counterpart, but this is an optional service.

With Sutton Bank, the account is FDIC-insured, comes with a free debit card, and has no minimum balance or annual fees. The app can be used without having a Honeydue bank account. You may even talk with your lover using the app, but some people would instead do it in person.

9. Personal Capital

![]()

Personal Capital is a comprehensive tool that allows users to track their spending and evaluate their investment portfolio. Like many of the other applications on our list, Personal Capital allows you to integrate all of your accounts in one place for easy administration and viewing.

You may use it to calculate your net worth, which will give you a good idea of where you stand economically and allow you to set a clear goal for where you want to be in the future. The app provides you with a personalized financial plan based on adviser analysis.

Compared to other apps, Personal Capital stands out for offering high-quality mobile apps and superior, easy-to-navigate desktop interfaces. It also contributes to examining your accounts and finding any hidden costs that may be hindering your portfolio from reaching its maximum earning potential. Anybody can utilize Personal Capital’s managing money tools for free. To be eligible for its advising services, you must first open an account with a required reserve of $100,000.

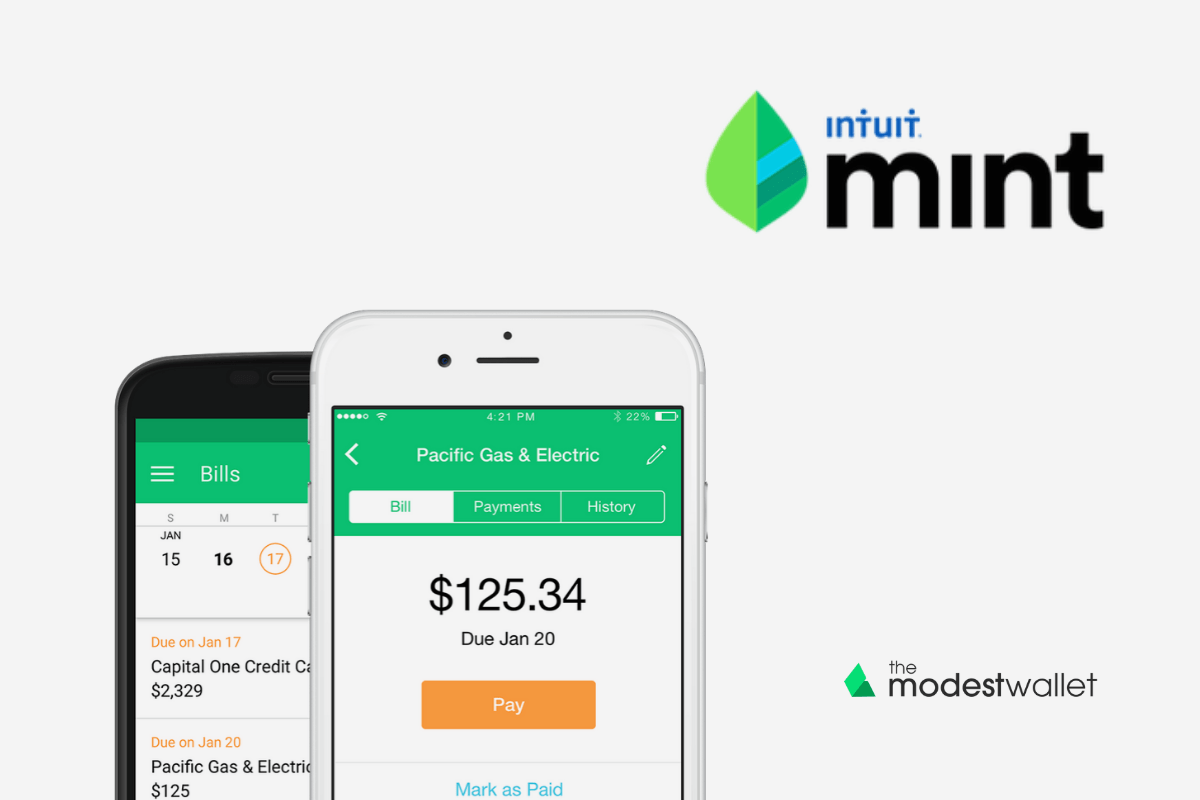

10. Mint App

Mint is quick and reliable, giving detailed and in-depth views of personal finance in the U.s. It has simple functionality. You may use the mobile app or the website (mint.com) to sign up. Mint uses configurable alerts to analyze your spending habits, income, and other financial transactions.

If you click the plus symbol and choose “Create Budget,” you’ll be sent to a page with a list of spending categories (such as groceries or movies). It recommends a monthly spending limit based on your spending history and data collected over several months. A simple line graph represents your monthly budget, giving both a short-term and long-term perspective.

It’s not an app for reconciling transactions or accounting software; it’s more about spending and overall financial health. Mint can not only calculate your net worth, but it can also give you lots a detailed breakdown of your spending habits. It’s also helpful in setting financial goals, such as breaking out of credit card debt or purchasing a home. Bills will be sent as push notifications. You’ll get a warning if you’re getting close to your budget limit in your given categories – too many lattes this week?

Advertising helps raise Mint, but the ads are more beneficial than annoying. Mint understands precisely how much interest you’re earning and paying on your mortgage, loans, and credit cards because of its all-knowing, all-seeing approach to your financial accounts.

Edited and Proofread by Ashlyn