Why Softbank Said A Near ‘Good-Bye’ To India?

Is it wrong if we say “India is too risky” from a governance perspective? That may be hyperbole where thousands of honest founders are building great companies, but high-profile bad apples tainted the well. The credibility of Indian startups took a hit every time a scandal splashed across headlines. SoftBank’s near-goodbye to India wasn’t just about macroeconomics or portfolio losses; it was also a reaction to this credibility crisis. Money can price in risk, but it flees uncertainty, and nothing breeds uncertainty like not knowing if a startup’s numbers are real.

India’s startup party had a larger-than-life DJ in SoftBank. For years, Masayoshi Son’s billions blasted through Bangalore and Gurgaon, minting unicorns at a heady pace. But when the music stopped, the Japanese investment giant quietly slipped out the back door, leaving the founders in a funding hangover. Why did SoftBank say a near “goodbye” to India’s startups, and what does it reveal about the credibility crisis facing the ecosystem? The story of SoftBank’s retreat can be a saga of exuberant bets, sobering losses, governance debacles, and a belated return to business fundamentals. It reads like a subcontinental cautionary tale – equal parts dramatic and data-driven – of how hype met reality in India’s tech dream.

From the frozen deal-making and global losses to imploding unicorns, frenzied exits, fraud scandals, mass shutdowns, and the reckoning that followed, we follow SoftBank’s footsteps as it tiptoed away from the wreckage. Along the way, we unearth example after example of Indian startups that went from billion-dollar darlings to cautionary tales, each adding to SoftBank’s skepticism. And we ask: was this downfall fuelled by a startup culture imitating Silicon Valley’s playbook without solving India’s real problems?

SoftBank’s near-withdrawal is not the end of India’s startup story; but it is the end of an era. The question is whether founders and investors will learn the hard lessons of these tumultuous years. Here is the story of how SoftBank’s India euphoria turned into an 18-month silent exit, and what it means for the future of Indian innovation.

The Dramatic Investment Freeze: Understanding SoftBank’s 18-Month Pause

In 2021, SoftBank was the life of the Indian startup party, writing enormous checks as if there were no tomorrow. That year alone, it deployed roughly $3 billion in India, fuelling high-profile companies like Paytm, Zomato, and Unacademy during the pandemic boom. Come 2022, however, SoftBank slammed on the brakes. Its investments in India plummeted by 84%, from over $3.2 billion in 2021 to about $500 million in 2022. By early 2023, the once-prolific dealmaker had virtually halted new deals for about 18 months, an extraordinary pause for a firm synonymous with aggressive growth funding.

This dramatic freeze was not just a dip in volume, but it was a strategic U-turn. For years, SoftBank’s mantra under Masayoshi Son had been “growth at all costs,” gladly bankrolling cash-guzzling startups to grab market share. But as 2022 unfolded, the calculus changed. Investors across the board grew skittish; late-stage backers like Tiger Global, Prosus, and Alpha Wave also retreated to the sidelines. SoftBank’s India head, Sumer Juneja, described a “wait-and-watch” strategy, focusing on portfolio preservation rather than new bets. Simply put, SoftBank had shifted from blitzscaling to survival mode in India!

By mid-2023, SoftBank’s deal pipeline in India was a trickle. It participated in only about six deals in 2022, down from 17 the year before. In 2023, it remained largely inactive, making almost no new investments. The conglomerate that once mused about plowing $5–10 billion a year into India was now content to sit on the sidelines. Insiders describe SoftBank’s India team as spending more time managing existing stakes (and fretting over them) than chasing the next big thing. The 18-month hiatus was so stark that when SoftBank signalled it might “hit the restart button” in 2024, it made headlines.

This freeze has been one of the most striking shifts in venture capital behaviour in recent years. It wasn’t triggered by a lack of promising startups – plenty still courted capital – but by a fundamental loss of confidence. As we’ll read, that loss of confidence had deep roots: some in SoftBank’s global troubles, and some in very local Indian messes. The funding winter that descended in 2022 was not just an India story but part of a worldwide chill.

Yet, its effects in India were especially pronounced, given how reliant the ecosystem had become on a handful of big-pocketed investors like SoftBank. Founders who once bragged about SoftBank term sheets in record time were suddenly left waiting by silent phones. For roughly a year and a half, SoftBank essentially told India’s startups that “We’re on a break.” And like a jilted partner, the ecosystem was left to wonder what went wrong.

The Global Context: SoftBank’s Massive Losses and Strategic Recalibration

To understand SoftBank’s India retreat, one must zoom out to the global carnage unfolding in Masayoshi Son’s empire. Simply put, SoftBank was (perhaps) bleeding, and badly, on the world stage. Its Vision Fund 1 and 2 had bet big on high-growth tech companies, and by 2022 those bets were imploding en masse.

Across four consecutive quarters in 2022, the Vision Funds racked up staggering losses, each on the order of $5–6 billion. This was unprecedented. SoftBank’s investment unit had never seen a losing streak like that. In one infamous quarter (Q2 2022), SoftBank reported a record investment loss of over $24 billion – yes, in just three months. It was a global bloodbath fuelled by plunging tech valuations, rising interest rates, and some truly disastrous bets (like, WeWork).

The man who once fancied himself a tech-soothsayer had a come-to-Jesus moment. Son’s hyper-aggressive strategy may be termed as flopped. “My investment judgment was poor,” he admitted after WeWork failure, effectively eating crow for the WeWork debacle and others. With SoftBank Group posting the largest losses in its history, Son publicly vowed to “play defense” instead of offense. The company shifted into what its CFO called a “defensive” stance, hoarding cash and slashing headcount on the investing teams. In short, SoftBank was in survival mode globally, and that meant no more billion-dollar moonshots for a while.

India, which had been SoftBank’s third-largest market after the U.S. and China, could not escape this global pullback. When your parent fund loses a hefty amount like trillions in a quarter, even the most promising Indian startups start to look like luxuries you can’t afford. The logic was painfully simple. Every new dollar into an Indian venture was a dollar not shoring up SoftBank’s balance sheet or backing safer bets like Arm (the chip designer Son was desperate to IPO to raise cash).

SoftBank’s retreat from India was thus part of a worldwide venture capital contraction. As inflation spiked and interest rates rose, frothy tech valuations were marked down across the board. The free money era ended, and with it ended SoftBank’s freewheeling ways.

It wasn’t just WeWork’s ghost haunting SoftBank. The Vision Fund portfolio was littered with misadventures: Didi in China got hammered by regulators, Coupang’s stock in Korea sagged, and closer to home, flagship investments like Oyo and Paytm were struggling. SoftBank lost confidence that pouring more fuel would rekindle these flames. In mid-2022, Son’s lieutenants like Rajeev Misra (who spearheaded many India deals) began stepping back, further signalling a strategic cooldown.

By late 2022, SoftBank “virtually halted new funding” globally, as one Reddit memo quipped. The firm focused on raising liquidity, selling off chunks of Alibaba, T-Mobile, etc. to fortify itself. This global defensive crouch meant that India’s funding winter was, in large part, an import from SoftBank’s winter. The meteoric losses forced a rethink: no more chasing growth without profitability, no more being the last greater fool in the valuation game. SoftBank would bide its time until sanity (and lower prices) prevailed.

To Indian founders used to Son’s grandiose promises, this strategic recalibration felt like whiplash. Not long ago, SoftBank’s Vision Fund chiefs were touring Bangalore, tossing out term sheets with minimal diligence. Suddenly, those same chiefs were telling founders to cut burn, focus on cash flow, and forget about $5 billion valuations. It was as if the big bad wolf of venture capital had morphed into a penny-pinching uncle overnight. But after a $50+ billion drubbing over two years, even SoftBank had to concede as the party was over, and the cleanup had to begin.

The Portfolio Problem: When Unicorns Become Liabilities

If SoftBank’s global losses set the stage, the actual play in India was performed by its portfolio – a cast of unicorns that were supposed to be stars but turned into millstones. SoftBank had pumped roughly $15 billion into Indian startups over the years, helping to birth about a fifth of India’s 100-plus unicorns. But by 2022–23, many of those unicorns looked less like thoroughbreds and more like limp ponies. The difference between valuation and value hit home with a vengeance.

Take Paytm, once SoftBank’s crown jewel in India. In 2021, Paytm went public amid great fanfare, reaching a lofty $20 billion+ valuation at IPO. SoftBank had poured hundreds of millions into Paytm, expecting a windfall. Instead, Paytm’s post-IPO performance was a train wreck. The stock lost over 60% of its value from the issue price, eroding billions in market cap. For SoftBank, Paytm became “a drag on returns”. By mid-2023, SoftBank started unloading its Paytm shares at a loss, selling a 2% stake for about $300 million in a desperate attempt to recoup cash. It was a bitter pill: a marquee investment turning into an albatross.

Then there’s OYO Rooms, the once high-flying hotel aggregator often touted as India’s Airbnb. SoftBank was OYO’s largest backer, valuing it near $10 billion at one point. OYO raised a whopping $3+ billion in funding and expanded globally, but later, the company struggled with profitability, burning cash to subsidize hotel partners and customers.

By 2022 OYO was grappling with corporate governance issues and repeated layoffs. SoftBank quietly slashed OYO’s valuation on its books to just $2.7 billion, a 75% markdown essentially acknowledging that much of its investment had vaporized. An IPO plan has been repeatedly delayed. OYO’s tale for SoftBank is cautionary, as a startup can grow fast and still lose its way, becoming a liability that needs constant triage.

Another instructive case was Meesho, the social commerce platform once heralded as the next big e-commerce disruptor. SoftBank joined a $570 million funding round for Meesho in 2021 at a lofty valuation. But as capital tightened, Meesho had to make a stark choice as it has to slash its cash burn or die trying. Until early 2022, Meesho was burning an eye-watering $40 million per month in a blitz to outgrow competitors. Over the course of the year, Meesho’s leadership (prodded by investors like SoftBank) cut that burn by 90%, down to around $4–5 million a month.

This radical diet saved Meesho from an immediate crash, but it came at a price; where growth slowed dramatically, and ambitions had to be reined in. Meesho’s founders admitted they’d settle for 30–50% growth instead of doubling every year, essentially understanding that the prior growth was unsustainable without endless cash infusions. For SoftBank, which had bet on Meesho’s meteoric rise, this was a sobering reset. A company they valued as a unicorn was now focused on surviving rather than dominating, its trajectory clipped.

Patterns emerged across SoftBank’s India portfolio. High valuations had been propped up by easy money, and when that evaporated, so did the lofty price tags. Many unicorns SoftBank backed, from ed-tech players like Unacademy to mobility firms like Ola Electric, faced harsh questions about when (if ever) they’d turn a profit. Unsustainable unit economics were exposed. Companies like Meesho and Unacademy slashed headcount and marketing spend, essentially rewriting their playbooks from “growth-first” to “efficiency-first.” The implicit promise SoftBank had made, that it would keep funding these losses until scale magically led to profits, was broken. And so the unicorns, left to survive in the wild without infinite capital, began bleeding.

In stark terms, SoftBank realized that many of its Indian unicorns were overvalued and underperforming. A senior SoftBank executive reportedly quipped that in India, “we funded too many features, not enough real businesses.” Startups had focused on blitzscaling a proven Western concept (food delivery, ride-hailing, quick commerce, etc.), hoping to win a winner-takes-all market in India. But often they misjudged the market size, or the competition, or the customer’s willingness to pay without subsidies. When reality set in, SoftBank was left holding equity in companies whose notional values far exceeded their actual worth or prospects.

By early 2024, SoftBank’s internal calculus for India became clear, which says “No more chasing the next unicorn until the current stable stops bucking”. Why write new checks when the old ones were bouncing? SoftBank’s near-term strategy shifted to damage control, trying to steer portfolio companies toward sustainability, and, as we’ll explore next, even looking to exit some investments entirely rather than double down.

The Exit Strategy: Liquidation Over Investment

Perhaps the most telling sign of SoftBank’s changed relationship with India is this. Rather than pumping money into Indian startups, SoftBank spent the last couple of years pulling money out. The investor famous for never seeing a round it didn’t want to lead suddenly became a net seller in India. Between 2021 and 2024, SoftBank liquidated roughly $7 billion worth of its holdings in Indian companies; through IPOs, block trades, and secondary sales. This was an extraordinary reversal. The same SoftBank that once spoke of “doubling down” on India was now busy cashing out of India.

The hit list of exits is remarkable. SoftBank sold significant stakes in Zomato, the food delivery giant, and Policybazaar (PB Fintech), the insurance marketplace, soon after they went public. It offloaded shares of Delhivery, the logistics startup, at IPO. It fully exited e-commerce baby retailer FirstCry and eyewear retailer Lenskart, both via secondary sales to other investors or IPO offer-for-sale tranches.

SoftBank even did a rare founder buyback deal to partially exit InMobi, one of the earliest Indian unicorns, with the founder taking back shares. And when it came to Ola Electric, SoftBank quietly pared down its stake as well. In one fell swoop, SoftBank was monetizing a big chunk of the portfolio it had built over nearly a decade.

To observers, it was clear what was happening. SoftBank was prioritizing liquidity and “return of capital” over the long-term “build for the future” talk. In public, SoftBank executives tried to put a positive spin. Sumer Juneja, for example, insisted that SoftBank was not fleeing India but merely “competing with IPOs for capital allocation”, as if selling in IPOs was a tough-but-necessary choice. He argued these exits were good for the ecosystem – proof that Indian startups could deliver returns. But that narrative fooled few. The reality was that SoftBank’s trust in the Indian growth story had been shaken so much that it was willing to lock in losses or modest gains and walk away.

Consider the numbers. SoftBank invested about $2.3–2.4 billion in four Indian tech companies that IPO’ed in 2021–22 (Paytm, Zomato, PB Fintech, Delhivery). By late 2023, it had sold chunks of those holdings for only $1.8–1.9 billion, effectively acknowledging that even the public markets didn’t value them at what SoftBank had paid. In Paytm’s case, SoftBank’s average investment cost was well above the IPO price; every sale booked a loss.

In the private domain, SoftBank’s exit of FirstCry reportedly valued the company at far less than the once-hyped $2 billion valuation. Dunzo, the hyperlocal delivery startup which SoftBank didn’t directly invest in but was emblematic of the sector, became nearly worthless – Reliance, a major backer, wrote off its entire investment of ₹1,645 crore (~$200 million) when Dunzo collapsed in 2025. These kinds of outcomes no doubt reinforced SoftBank’s urge to get whatever cash it could while the getting was good.

By 2024, SoftBank’s India portfolio strategy looked like, prune and pivot. Prune the dead branches (sell off losers, take losses if needed) and pivot to a few sectors that still held promise (more on that in the Path Forward). The numbers bear repeating: SoftBank clocked over $7.2 billion from India exits up to 2025, a figure that would have been unthinkable during the bull run when the last thing on Son’s mind was selling early. This great Indian sell-off signalled a deep lack of faith. It was as if SoftBank looked at its roster of Indian unicorns and decided that many wouldn’t be “roaring lions” in the future, but rather paper tigers that it was better off without.

One could argue, of course, that SoftBank was simply cycling out capital to recycle into new bets. But did we see SoftBank redeploying massively in new Indian startups during this period? No, we saw the opposite. The proceeds from these India sales likely went to plug holes elsewhere (or to stockpile cash). Indeed, SoftBank’s new investments in India during 2022–23 were minimal, as we discussed – effectively near zero outside follow-ons. If SoftBank truly believed these exits were healthy churn, it would have concurrently been making new bets. But, it wasn’t.

Founders and observers in India got the message loud and clear, that the SoftBank was in retreat mode. The days of the $100 million term sheet over coffee were gone. Now SoftBank was the one dumping shares, not accumulating them. This exodus had ripple effects. Other global investors like Tiger Global and Prosus also started trimming their India exposure, partly in response to the same macro factors, but also because once SoftBank turned cautious, the “greater fool” chain in late-stage funding broke. The result was a hard funding winter where even good companies struggled to raise money at sensible terms.

SoftBank may not publicly admit to “exiting India”, and indeed it hasn’t shut down offices or anything that dramatic. But the shift from being a net investor to a net seller speaks louder than any PR statement. It represents a stark reversal from the heady optimism of 2021. The Vision Fund had once dreamed of IPO riches in India; by 2023 it was more interested in how quickly it could unload shares after IPO. For the ecosystem, this was a reality check: if the biggest believer is cashing out, perhaps the emperor (the startup story) indeed had no clothes.

The Governance Crisis: Why Trust Collapsed

Even as SoftBank grappled with numbers and valuations, a more insidious force was eroding its confidence (and that of many other investors) in India. A spate of corporate governance scandals that rocked Indian startups in 2022 and 2023. It was as if every few weeks, a new scandal hit the headlines, each unveiling some combination of cooked books, internal fraud, or founder misconduct. For an investor already on edge, this was gasoline on the fire of skepticism. Trust, the basic fiber that holds the investor-founder relationship, was collapsing.

The most dramatic example was GoMechanic, a Sequoia and Tiger-backed car repair startup that had been in talks with SoftBank for a sizable investment. In January 2023, GoMechanic’s founder admitted to wide-scale financial misreporting, which was essentially fraud. The startup had inflated revenues, possibly by creating fictitious garages/customers and tweaking the accounts, all in a bid to show growth. This confession came only after due diligence by SoftBank’s team (and co-investor Khazanah) uncovered serious “discrepancies”.

The fallout was swift and brutal. GoMechanic’s investors (including top VCs) were “deeply distressed” at being misled, an EY forensic audit was launched, and the company laid off 70% of its staff overnight. A startup valued at around $300 million just months prior effectively imploded due to greed and deceit. SoftBank, needless to say, walked away from the potential deal in horror, likely thanking its lucky stars for discovering the rot just in time.

Not long before, another SoftBank suitor, Trell, had imploded in similar fashion. Trell, a social commerce startup, was in late-stage talks to raise over $100 million (reportedly with Amazon in the mix) when an investigation found serious financial irregularities. It appeared Trell’s founders had vastly overstated revenues and possibly engaged in related-party transactions to siphon funds. The funding round collapsed, and Trell ended up laying off more than half its employees in 2022. Once again, due diligence saved investors from throwing good money after bad; but it also served up another cautionary tale of lax governance.

And who can forget the BharatPe saga? While not a SoftBank portfolio company, BharatPe was a high-profile fintech where the founder, Ashneer Grover, was accused of egregious misconduct; from siphoning money via fake vendor invoices to abusive behaviour. In early 2022, BharatPe’s board (which included Sequoia’s rep) ousted Grover after an audit found “recruitment irregularities and non-existent vendors” draining company funds. The public mud-slinging that followed, with Grover insulting investors and the company suing him for ₹88 crore, became a soap opera that did little to inspire confidence in Indian startup governance.

Then came Zilingo (though based in Singapore, it had Indian founders and was part of the Sequoia India portfolio). In 2022, an anonymous whistleblower tip led to an investigation that found Zilingo’s CEO Ankiti Bose had misreported financials; she was suspended and eventually fired. Although not directly tied to SoftBank’s India investments, these incidents contributed to a narrative that something was rotten in the state of Startup-land.

By mid-2023, it felt like a pattern. GoMechanic, Trell, BharatPe, Zilingo, and later ZestMoney, all facing accusations of fraud or serious governance lapses. ZestMoney, a buy-now-pay-later fintech, nearly got acquired by PhonePe in 2023, but the deal was called off after due diligence reportedly raised concerns over its books and compliance. The founders of ZestMoney then resigned and the company all but collapsed, laying off 20% of staff and leaving its future in limbo. It emerged that the deal fell through due to lapses in due diligence, valuation disagreements, and questions about business sustainability – polite wording that often includes governance and data accuracy issues.

From SoftBank’s vantage point, these episodes painted a troubling picture. Indian startups not only had risky business models, some couldn’t even be trusted with basic honesty. It’s one thing to lose money chasing growth; it’s another to lose money because a founder lied or hid the truth. The latter leaves a far deeper scar. Indeed, after GoMechanic, Sequoia India’s managing director wrote a rare public blog, decrying the frauds and promising stricter oversight, practically begging founders to not “misuse trust”. When a top VC feels compelled to lecture founders on not committing fraud, you know trust is in the gutter.

SoftBank itself isn’t new to governance crises (WeWork’s Neumann era), but facing a cluster of them in an emerging market likely made it far more cautious. Reports suggest SoftBank and others increased diligence steps, including more forensic audits, deeper background checks for any India deals. This slower, more careful approach is the antithesis of the “move fast” ethos that had fuelled the 2016–2021 funding surge. And it undoubtedly contributed to SoftBank simply opting out of new deals – the hassle and risk of finding the next GoMechanic lurking in a data room was just too high.

In conversation, some insiders even whispered that “India is too risky” from a governance perspective. That may be hyperbole where thousands of honest founders are building great companies, but high-profile bad apples tainted the well. The credibility of Indian startups took a hit every time a scandal splashed across headlines. SoftBank’s near-goodbye to India wasn’t just about macroeconomics or portfolio losses; it was also a reaction to this credibility crisis. Money can price in risk, but it flees uncertainty, and nothing breeds uncertainty like not knowing if a startup’s numbers are real.

The Great Shutdown Wave: Startup Failures from 2020 to 2025

While SoftBank was busy selling stakes and sidestepping frauds, another drama was unfolding on the ground: an unprecedented wave of startup failures in India. The years 2022 through 2025 saw thousands of ventures shut their doors, from tiny three-person outfits to once high-flying funded companies.

By some estimates, over 53,000 tech startups in India have folded over the past decade, with a sharp spike in 2022–2023. One LinkedIn analysis noted that just in 2023 and 2024, around 28,000 startups shut operations, an astonishing bloodletting, compared to only ~2,300 recorded closures in the entire period from 2019 to 2021. In 2025 alone, at least 11,000 more startups died (as of October that year), though the silver lining is that the pace of failures was slightly lower than 2023’s peak.

For SoftBank and other investors, these statistics weren’t abstract, as they hit close to home, as many portfolio companies were among the casualties. Let’s enumerate some of the prominent failures and near-failures that have characterized this “funding winter” massacre:

- Dunzo: Once a poster child of hyperlocal delivery (Google’s first direct India investment) and later quick commerce, Dunzo spiraled out in dramatic fashion. It had raised around $450 million (from the likes of Reliance and others) at its peak, swelling to a valuation over ₹6,000 crore. But by late 2024, Dunzo was unable to pay salaries or vendors; it shuttered most operations. Reliance wrote off its entire stake as worthless. The company that popularized “get it delivered in 19 minutes” couldn’t find a path to profitability and became one of the most expensive write-offs in Indian startup history. SoftBank wasn’t an investor, but Dunzo’s collapse sent a chill through the market – if even big-pocket backers like Reliance and Google couldn’t save a top startup, who could?

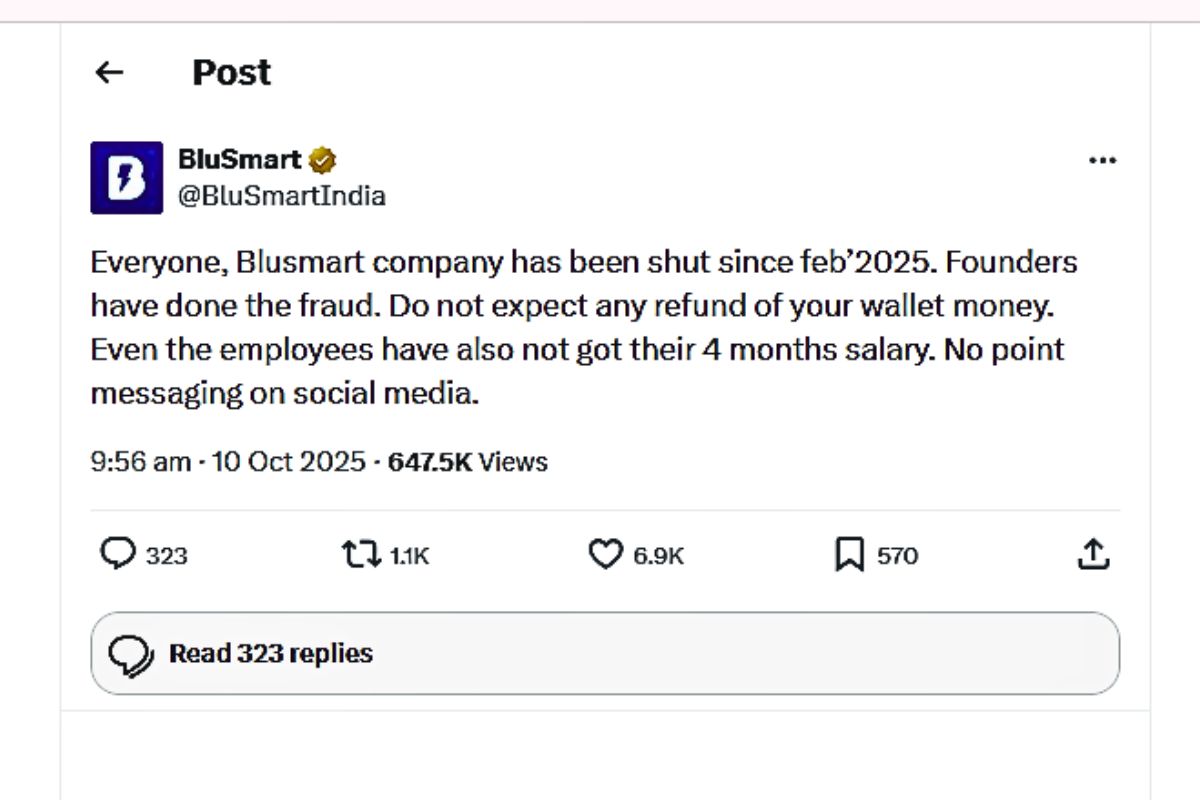

- BluSmart: India’s first all-electric ride-hailing startup, BluSmart was on a promising track, offering a cleaner Uber alternative. It raised heavy funding, reportedly over $50 million, including investments from BP and celebrity backers. But in 2025, BluSmart suddenly shut down amid scandal. Its official X account posted a bombshell message claiming “founders have done the fraud… company has been shut since Feb 2025… no salaries for 4 months”. Subsequent investigation by SEBI (the regulator) suggested that around ₹262 crore meant for EV purchases was diverted by the promoters for personal luxuries, such as buying a high-end apartment and funnelling money to related firms. BluSmart’s app went dark, and lenders began legal action. This saga, involving Deepika Padukone and MS Dhoni as brand ambassadors who were left embarrassed, reinforced fears that even the “good for environment” startups were not immune to old-fashioned corruption. Thousands of drivers and staff were left in the lurch. For investors like BP, it was a rude awakening to India’s governance realities.

- The Good Glamm Group: A roll-up of D2C beauty and media brands (MyGlamm, POPxo, Mamaearth’s rival, etc.), Good Glamm was nearly a unicorn, valued around $1.2 billion at its peak. It went on an acquisition spree, gobbling up smaller brands to build a beauty empire. But by 2023, the strategy unraveled. Integration of diverse brands proved difficult; synergies didn’t materialize. The group’s revenue grew, but so did losses, and cash started running out. In mid-2023, Good Glamm delayed payments to employees and vendors, signalling distress. Finally, its lenders lost patience and enforced their rights on the assets. In a LinkedIn post in July 2023, CEO Darpan Sanghvi admitted defeat, as the lenders would break up and sell the group’s brands one by one to recover loans. Essentially, Good Glamm was being liquidated piecewise; a dramatic fall for a would-be unicorn. SoftBank wasn’t directly involved, but this high-profile collapse of a near-unicorn was yet another black mark on the ecosystem’s report card.

- Otipy: A farm-to-fork grocery startup backed by WestBridge, Otipy grew fast during the pandemic delivering fresh produce to urban consumers. It even piloted electric vegetable carts in 2023. But when a crucial $10 million funding round fell through in 2025, Otipy ran out of cash and shut operations overnight, laying off ~300 employees. In a somber town hall in May 2025, the CEO told employees the company couldn’t go on and would try to liquidate assets to pay salaries. Otipy’s FY24 revenue had grown 68% to ₹160 crore, but it still lost ₹52 crore – an unsustainable model without fresh funding. Its collapse left farmers, vendors, and customers in the lurch (many had unrefunded wallet balances). The quick commerce winter spared few, and Otipy became another data point showing growth alone isn’t enough.

- Koo: Billed as “India’s Twitter,” Koo shot to fame during 2021’s Twitter vs. Government tussle. It amassed ~10 million users and raised over $65 million from Tiger Global, Accel, and others. But by 2023, Koo struggled to keep users engaged and burn under control. It tried to find a buyer (DailyHunt and ShareChat were courted) but failed. In July 2024, Koo’s founders announced that without more capital or an acquisition, they had to shut the app down. Running a social network turned out to be extremely costly as Koo was spending over ₹10 crore a month even after cuts. The co-founders even dipped into personal funds to pay salaries, but that wasn’t sustainable. They poignantly noted that Koo needed “5–6 years of patient capital” which never materialized. By mid-2024, Koo went into hibernation, proving that desi clones of global platforms face an uphill battle. The episode also carried political undertones (Koo had government support initially), adding to the drama. For SoftBank, Koo’s fate underscored why it avoids Indian consumer internet fads that don’t have clear monetization.

- Other notable shutdowns read like an obituary of the pandemic-era startup frenzy. Lido Learning, a well-funded ed-tech startup, shut abruptly in 2022 after it couldn’t raise more capital, stranding employees and students. FrontRow, focused on celebrity-taught courses, folded when demand vanished post-pandemic. Vedantu Superkids, a subsidiary of Vedantu, also closed as the online tutoring boom went bust. BeepKart, a used two-wheeler marketplace that raised $18M, scaled back drastically – its FY24 revenue jumped to ₹100 crore but losses doubled to ₹66 crore, forcing it to shut operations in some cities and fire staff. Ohm Mobility (EV financing), Log9 Materials (battery tech), Hike (once a messaging unicorn that pivoted to crypto gaming) – all either shut down or shrank to shadows of their former selves. Hike’s pivot into a crypto-powered gaming platform was effectively killed when India’s regulations and a steep crypto downturn hit; by 2023 Hike had shut its social app and its “Rush” gaming service struggled after a real-money gaming ban, leading founder Kavin Mittal to wind down operations.

- Even legacy names from an earlier era finally threw in the towel: TinyOwl, a foodtech startup that had melted down in 2015, formally shuttered in 2022 after languishing. Furlenco, a once-promising furniture rental startup, collapsed under debt in 2023, with assets sold in a fire sale.

The scale of failures was staggering, but it also had a cleansing effect. Observers noted that by 2025, the shutdown rate began to slow, possibly indicating the worst had passed. In 2025, fewer startups shut compared to 2024, suggesting the ecosystem was shedding its weakest links and stabilizing. But from SoftBank’s perspective, the damage was done, as the go-go years had created a startup bubble where too many companies with flawed models got funded.

When the bubble burst, it wiped out tens of thousands of ventures, including several that SoftBank had either invested in or considered investing in. This failure wave certainly fed into SoftBank’s decision to freeze new bets. After all, why rush to invest in the next startup when the mortality rate had spiked so alarmingly?

For India’s reputation, these numbers were a double-edged sword. On one hand, a high failure rate is normal in a maturing ecosystem, as it shows experimentation and creative destruction. On the other hand, the sheer magnitude raised questions. Were many of these Indian startups ever truly viable, or were they built on vapor? SoftBank likely asked itself that unkind question about some of its own portfolio: if a company needed endless capital to live, maybe it wasn’t alive in the first place. The failure of so many ventures, big and small, became a collective referendum on the excesses of the 2018–2021 funding mania.

Autopsy of a Boom: Why So Many Startups Imploded

The post-mortem of India’s startup boom isn’t pretty, but it’s illuminating. Several recurring root causes explain why so many ventures, including those SoftBank loved – failed at such alarming rates. These aren’t just individual stories of bad luck; they are systemic issues that undercut the credibility of the whole ecosystem:

(i) Growth-at-All-Costs & Vanity Metrics: During the boom, startups were conditioned to “grow, grow, grow” by any means. Customer acquisition, GMV, MAUs – these numbers mattered more than profits or even unit economics. Founders responded by blitzscaling unprofitably. Think of food delivery apps offering meals cheaper than raw groceries (to boost order counts), or e-commerce platforms giving massive cashbacks to show GMV growth.

It was a classic case of vanity over sanity. For a while, as long as new funding came in, this could continue. But when the funding music stopped, these startups found themselves with high costs and customers unwilling to pay full price. As an example, online grocers that were giving 10-minute deliveries at near-zero fees simply couldn’t sustain operations when investors no longer subsidized each order. Many, like Zepto’s early competitors, shut down or retrenched heavily. The excessive burn in pursuit of growth essentially dug a grave that these companies fell into when cash ran dry.

(ii) Pandemic Bubble & False Market Signals: The pandemic provided a once-in-a-lifetime surge for certain digital businesses – ed-tech, gaming, online groceries, remote work tools, etc. Many startups mistook these temporary spikes for permanent shifts. Ed-tech firms like Byju’s, Unacademy, Vedantu assumed that online learning had changed forever, so they scaled up wildly in 2020–21 (hiring thousands of tutors, spending on ads, acquiring peers). But once schools and coaching centers reopened, demand reverted sharply.

By 2022–23, these companies had to lay off hundreds and acknowledge grossly overestimating the market. Lido Learning went bust when students flocked back to physical tuitions. Similarly, quick-commerce (10-minute grocery) saw insane growth during lockdowns, leading firms like Dunzo and Zepto to invest in dozens of “dark stores.” Post-pandemic, growth slowed and economics remained terrible (who pays delivery fees for a ₹50 order?). The crash of Dunzo underscored that building a business on an exceptional event (Covid) is dangerous. Many Indian startups learned this too late.

(iii) Financial Mismanagement & Fraud: We’ve covered the headline frauds, but even beyond those, there was widespread financial indiscipline. Loose internal controls, inexperienced CFOs, founders treating company accounts as personal ATMs – these issues plagued numerous startups. Even some not accused of fraud found that their accounting was aggressive (capitalizing expenses, recognizing revenue too early, etc.) to impress investors. When investors started scrutinizing more closely in 2022, a lot of creative accounting was exposed.

Furthermore, startups often diversified into unrelated businesses using surplus funds from a boom cycle – money that evaporated when focus returned to core business. There’s also the element of plain incompetence: some founders just didn’t manage cash flow or compliance well, leading to crises that needn’t have happened. A telling stat: in late 2023, the Ministry of Corporate Affairs reported over 6,300 DPIIT-registered startups as ‘closed’ (dissolved/struck-off) since the government recognition program began. Not all closures are due to mismanagement, but it’s a safe bet that a good chunk could have been avoided with better financial planning and governance.

(iv) Winner-Takes-All Myths & Overcompetition: Many Indian startups operated in winner-takes-all markets – or so they thought. Food delivery, ride-hailing, e-commerce, payments: in each, a belief that only 2–3 players would survive led to an arms race of spending. SoftBank itself fueled some of these fights (e.g., funding Ola to fight Uber, or Flipkart to fight Amazon back in the day). But what if the market couldn’t sustain even one player profitably, let alone two? That seems to be the case in quick commerce – it’s debatable if any company can make money delivering ₹100 orders in 10 minutes regularly.

Also, some markets had incumbents with deep pockets entering, crushing the newcomers. Reliance’s entry into grocery and e-commerce, for example, squeezed startups like Grofers (Blinkit), Zepto and pushed others to sell or shut. Global giants like Amazon and Walmart (via Flipkart) meant India’s e-commerce startups had virtually no chance unless they found niche angles (Myntra survived by focusing on fashion and being acquired, smaller ones perished).

The intense competition, often funded by venture capital’s own doing, ensured that customer acquisition costs stayed high and profit remained elusive. Many startups were essentially in a game of chicken, hoping competitors would fold first. When the funding cycle turned, several all crashed at once (as seen in online learning and quick grocery, where multiple players failed nearly together).

(v) Regulatory and Policy Shocks: Some startups were victims of external policy changes. India’s regulatory environment can be unpredictable, and a few sectors saw the rug pulled out from under them. Crypto exchanges and crypto-tech startups boomed in 2021, but in 2022 the government imposed steep taxes and an effective ban via banking channels, decimating trading volumes. Startups in that space either pivoted or died. Real-money gaming (like fantasy sports, rummy, etc.) was another rollercoaster: initially a gold rush, then multiple state bans and a dramatic new tax in 2023 (28% GST on entry fees) made many gaming startups nonviable overnight.

Hike’s pivot to a gaming platform, which involved real-money tournaments, got nuked by these rules; Hike effectively shut that venture. Fintech lenders and neo-banks faced an RBI crackdown on digital lending practices and data storage norms – some folded because they couldn’t adapt. Zoplar was reportedly hit by restrictions on importing refurbished medical equipment, gutting its business model (if you can’t source devices, you can’t lease them). While good startups navigate regulation proactively, many younger ones were caught off-guard, and their investors perhaps didn’t price in this substantial India risk.

(vi) The Funding Dependency: Finally, the overarching cause: too many startups were built to run only on continuous funding injections, not on sustainable revenue. This was fine in a bull market – one could always raise the next round at a higher valuation. But the moment the music stopped, those dependent on investor cash (rather than customer cash) hit a wall. When SoftBank and others retreated, startups that hadn’t charted a path to break-even had no plan B. It’s telling that in the frigid funding winter of 2023, even fundamentally decent startups had to close shop simply because their “lead investor” ghosted them or term sheets got delayed.

An example is LiftO – a well-liked startup that shut down because a committed Series A fell through at the last minute, leaving it stranded. This dependency syndrome was perhaps the biggest systemic flaw, where companies prioritized pleasing investors over pleasing customers for far too long. Startups rarely die because the idea is bad; they die because fundamentals were imaginary; momentum was mistaken for sustainability. A brutal assessment, but not inaccurate for the 2020–2022 vintage of startups.

For SoftBank, each of these root causes served as a post-facto justification for its pullback. Son might have thought: “Perhaps we rushed in without understanding the market.” When SoftBank first poured billions into India, it assumed Indian startups would replicate Chinese or American ones and ride the same curves. But structural differences of economic, cultural, regulatory meant the Silicon Valley copy-paste model often failed in India. Many Indian startups were solving problems that, frankly, weren’t top priorities for the average Indian, or they were solving a real problem in an inherently unprofitable way. The reckoning of 2022–2025 taught everyone that no amount of funding can fix a fundamentally broken model.

In the end, SoftBank’s hesitation to invest further wasn’t just fear or financial prudence; it was also a reflection of learning. They had touched the stove and been burned. The next time (if ever) SoftBank returns with big checks, one can be sure they will be asking: Show me your path to profit. Show me your governance is clean. Show me you’re not just aping a Silicon Valley idea but truly solving an Indian problem. Until then, caution prevails.

The Capital Efficiency Myth: High Burn, Low Return

One phrase that kept coming up in board meetings during this era was “capital efficiency”, which is essentially, how well a startup turns each dollar of investment into value. In India’s boom, capital efficiency went out the window. Startups raised record sums (over $20 billion of funding flowed into India in 2021 alone), but the output in terms of sustainable businesses was dismal. It became painfully clear that many Indian startups were extremely inefficient in their use of capital, burning huge amounts to produce relatively modest results.

Consider some emblematic cases:

- Dunzo, as mentioned, raised about $449 million in its lifetime. What did that buy? A recognizable brand, yes, and a user base in a few cities ordering groceries and errands. But not a profitable engine. By late 2022, Dunzo’s core business of 15-minute groceries was leaking money with every order. Instead of pivoting in time or slowing down, Dunzo kept trying to spend its way to victory, until the cash ran out. When it shut down, hundreds of millions had effectively gone up in smoke, with no profitable business to show. If one were to compute the return on invested capital for Dunzo’s investors, it would be deeply negative. Reliance’s write-off of ₹1,645 crore speaks volumes.

- Otipy was actually relatively efficient by some startup standards as it grew revenue 68% in a year with moderate funding. Yet even there, ₹160 crore in revenue came with ₹52 crore in losses in FY24. That means for every ₹3 earned, ₹1 was lost. The improvement from the previous year (losses were ₹72 crore on ₹95 crore revenue in FY23) suggests Otipy was trying to fix its economics, but it wasn’t enough. When the crunch hit, that inefficiency, needing ₹1.52 to generate ₹1 of revenue, proved fatal. Essentially, Otipy needed continued infusions to subsidize the losses; without them, even its growth became irrelevant.

- BeepKart is a stark illustration. The used two-wheeler marketplace managed to double its revenue to ₹100 crore in FY24, a commendable growth. However, its losses also more than doubled to ₹66 crore. So despite 2.5x revenue growth, it actually became more unprofitable in absolute terms. The company tried to scale in multiple cities simultaneously, which ballooned costs (inventory, storefronts, staff) faster than revenue. The result was a classic “growth and losses both rising in tandem” scenario. When it attempted to cut costs later, quality and customer satisfaction fell, as described by insiders, further hurting the business. In an efficient market, one might expect losses to decrease as revenue scales (economies of scale). But here, losses kept up, indicating the model itself had thin margins and scaling just amplified the burn. For SoftBank or any late-stage investor, these dynamics are red flags – it implies no matter how much money you pour in for growth, profitability remains a mirage.

SoftBank had several such cases in its own portfolio too: Ola Electric, for instance, raised over $800 million by 2022 to set up its EV scooter factory and operations. Yet, even after delivering scooters, Ola Electric was reportedly nowhere near profitable per unit, and quality issues led to recalls. Each scooter sold was likely at a loss initially (subsidies, manufacturing hiccups).

If an investor looked at how many dollars went in vs. how much sustainable profit came out, the ratio was atrocious. Similarly, Unacademy raised hundreds of millions, but by 2022 had to acknowledge that much of that had been squandered on user growth that didn’t convert to paying customers. It famously started a programme to become revenue-positive, but only after laying off 1,000+ employees and cutting all “frivolous” costs (like free snacks for staff). That such drastic measures were needed suggests the earlier spending was hugely inefficient relative to output.

Why were Indian startups so capital-inefficient? A few reasons: artificially low pricing (to undercut competitors and lure price-sensitive Indian consumers) meant companies were effectively buying revenues. High operational costs in a challenging infrastructure environment meant it took more effort/money to deliver services (think delivery drivers in chaotic cities – you need more riders per order volume than in a dense city like Shanghai). And many startups overbuilt teams and products – flush with cash, they would hire ahead of need, build fancy tech that wasn’t required at their stage, or expand to too many cities at once. All that burned cash quickly without commensurate returns.

SoftBank, after a point, likely ran the numbers and realized that the Internal Rate of Return (IRR) on its India portfolio was far below projections. In venture, you accept many losses for a few mega-wins. But what if even the “wins” (the unicorns) yield low or no returns? By early 2023, SoftBank’s few Indian stars that had seen liquidity – like Zomato, Policybazaar – were lukewarm.

For instance, SoftBank sold its stake in Policybazaar at a valuation not far from what it invested, meaning after years the return was negligible. Its sale of part of its Zomato stake post-IPO was also at a modest gain at best, given Zomato’s stock volatility. Meanwhile, others like Paytm and OYO were underwater. So the overall portfolio math looked ugly.

One could almost hear SoftBank’s investment committee asking: “Why double down in a market where our dollars seem to evaporate into losses and markdowns? Until we see evidence of genuine capital efficiency, let’s hold off.” This sentiment is supported by how SoftBank’s new India bets (in 2024–25) are shaping up; as they are focusing on enterprise and B2B startups that have clearer revenue models, rather than consumer unicorns that guzzle cash. We see SoftBank sniffing around AI startups, cloud infrastructure plays, SaaS companies; the very domains where typically unit economics are better and $1 of investment can create more intrinsic value.

In summary, the myth during the boom was that one could spend one’s way into building a lasting company – that if you captured the market, profits would magically follow. The bust revealed the folly: many startups spent tons and still couldn’t find profit.

SoftBank’s exit from the feeding frenzy was in part a realization that capital is not a commodity to be sprayed around but a precious resource that needs to yield returns. If Indian startups wanted more of SoftBank’s money in the future, they’d have to show they could do more with less. As harsh as it sounds, the era of “more funds = more growth” died, and with it died many startups that were running on fumes of that philosophy.

The Valuation Reality Check: From Unicorn Dreams to Distress Sales

For years, Indian startups (aided by investors like SoftBank) chased the coveted “unicorn” status – a billion-dollar valuation – as if it were a merit badge. By 2021, India had over 100 unicorns, many turbocharged by late-stage funding rounds that assumed future growth and monopolistic markets. But in the cold light of 2023–2024, those valuations underwent a brutal reality check. As the saying goes, valuation is not value. SoftBank learned this in perhaps the most painful way.

All these make one thing clear, that the unicorn bubble is busted, and SoftBank’s India portfolio is deeply underwater. SoftBank had poured money at the top of the market. Now the market reset and those investments were worth a fraction of cost. Psychologically and practically, this would deter anyone from pouring more in. Why invest a fresh $100 million at a $1B valuation when your previous $100 million is now worth $30 million? You’d rather wait until the dust settles, maybe even buy back in at the bottom if you still believe – or just cut your losses and walk.

Another angle: SoftBank likely faced pressure from its own backers (LPs). The Vision Fund had Saudi and Abu Dhabi money, among others. Consecutive loss quarters and high-profile flops would have made those LPs question further high-risk bets. The prudent course was to shore up what’s left, not double down on a sinking ship. India, unfortunately, fell in the category of sinking (or at least taking on water) in SoftBank’s global view.

In essence, the once lavish spender had turned into a value investor scouring for bargains – a different persona entirely. The writedowns and distress sales taught SoftBank a lesson: India’s unicorn valuations were often built on hope, and hope is not a strategy. Going forward, any resurgence of SoftBank in India would be on far more conservative terms. The era of unicorn-minting at the flick of a pen ended in a heap of “decacorn” dreams crashing to earth.

The Path Forward: Lessons and the Road Ahead for Indian Startups

SoftBank’s quasi-departure from India is not just an anecdote in venture circles; it’s a pivotal chapter in the story of India’s startup ecosystem. It marks the end of the Wild West era and the beginning of a more sober, pragmatic phase. As we step forward, the question isn’t simply whether SoftBank will come back (odds are, it eventually will in some fashion). The deeper question is: what changes now for Indian startups? And can they rebuild credibility to entice big capital again?

In conclusion, SoftBank’s retreat was both a cause and effect of India’s startup winter. It symbolized the end of an age of innocence (or ignorance, one might say) for venture investing in India. Credibility took a hit, yes, but credibility can be rebuilt with consistent, solid performance over time. The onus is now on Indian startups to prove their mettle – to show that they can be as innovative and resilient as any in the world, and not just beneficiaries of a temporary capital glut.

Will SoftBank return in full force? Probably, someday – as soon as the pendulum swings and they see multi-bagger returns being likely again. Masayoshi Son loves a good story, and India’s long-term growth story is still compelling. But the next time he comes knocking, founders and investors will both remember the lessons of this chapter.

The hope is that the ecosystem will by then have shed the dubious reputation of being a copycat, cash-burning, governance-ignoring wild west, and transformed into a place where big visions can be backed by big funds responsibly. In a way, the SoftBank saga could be the tough love that propels Indian startups into a more credible, globally respected era – once they pick themselves up from the humbling crash and get back to building, one prudent step at a time.