5 Indian Company That Must Be Precautionary Investigated Amid PayTM & Byjus Fiasco.

Given the worrisome findings affecting certain well-known Indian companies, it is becoming increasingly evident that a thorough audit of firm funds and activities is not just warranted but absolutely necessary. The startup ecosystem, once praised as a sign of innovation and expansion, now urgently requires scrutiny and accountability of every individual company. Growing concerns about valuation anomalies, false financial statements, and prioritising profits over conscience raises severe questions about these companies' reliability.

Innovation and aspiration have found fertile ground for success in India’s startup ecosystem. We’ve seen a historical growth in entrepreneurial accomplishments over the last decade, thanks to a variety of variables. Factors include increased technology accessibility, a bigger consumer market, and a growing hunger for exploring the unknown. However, in this evolving company culture, a clear tendency has emerged: massive capital outflows, which frequently outstrip the revenues earned by these companies.

The recent performance of new-age businesses such as Paytm and Byjus has raised worries about their long-term viability. Following are the companies that can be investigated in the aftermath of the Paytm and Byju fiascos in order to avoid any potential mishaps, as indicated by distinct red flags.

Today, we’ll tell you about five Indian company that seem to appear at an alarming rate.

Their climb from humble origins to billion-dollar values may appear to be a success story, but behind the scenes, things are not so rosy. A closer look at their financial documents uncovers some startling figures. These companies are investing extensively in marketing, expansion, and staff compensation. This is resulting in a massive cash burn rate.

Traditional business knowledge holds that companies should prioritise profitability and efficient resource management. However, these start-ups appear to be pursuing a different strategy. They prioritise expansion at all costs. This method may be effective in the short term but is unsustainable in the long run. If these companies do not begin to generate profits quickly, they will eventually run out of money.

Flipkart.

Flipkart, India’s largest e-commerce company, is spending money at an alarming rate. Flipkart’s cash burn rate for the fiscal year ended September 2022 was US$3.7 billion, the highest of any Indian company, not alone in the e-commerce market. Flipkart’s investors are concerned that the company would run out of money due to its rapid cash burn rate. Flipkart has already raised more than $10 billion in capital, but it is unclear how much more the company will need to raise to stay viable.

Several reasons contribute to Flipkart’s substantial cash burn rate. One factor is the company’s ambitious expansion strategy. Flipkart had raised US$3.6 billion in July 2021. Later in August 2021, right before the forthcoming holiday season, it invested $1.42 billion in many of its expansions.

According to the filing with the registrar of companies, US$ 589 million was invested in Flipkart India Private Limited, US$ 353 million in its B2C segment Flipkart Internet Private Ltd, another US$ 412 million in Instakart, the logistics arm of the business, and another US$ 66 million in Myntra Designs and Myntra Jabong India. Flipkart is also expanding into new areas, such as grocery and fashion, as well as investing in cutting-edge technology like AI and machine learning. These expenditures are costly, and they contribute significantly to Flipkart’s high cash burn rate.

Not to forget the company’s competitive environment. The Indian e-commerce business is highly competitive, and Flipkart is up against Amazon and other players. To compete, Flipkart offers steep discounts and cashback, which contributes to its cash burn rate. At this pace, if Flipkart is unable to limit its cash burn, it may be obliged to raise further funds or perhaps sell itself. This would be a significant setback for the Indian e-commerce business and a blow to Flipkart’s customers, who have grown to rely on the company for online shopping needs.

According to the report, the net loss for FY23 was ₹4,846 crore, up from ₹3,404 crore in FY22. This is a 44% increase year-on-year. Even after that, the recent news around the e-commerce giant says that Flipkart aims to buy Dunzo. It is strange to understand how a company with a high cash burn rate and substantial losses aims to buy another loss-making firm. Isn’t this can be a point of investigation?

Firstcry.

In August 2023, the tax department was seen probing an alleged tax evasion by the founder of FirstCry, Supam Maheshwari, for possible tax fraud of more than $50 million. After years of losses, FirstCry turned profitable in the financial year ending March 31, 2021. It is one of the few companies in our country seeking to tap the IPO market after being profitable at an operational level.

FirstCry is one of the handful of e-commerce companies that have managed to cross the Rs 5,000 crore revenue threshold. The Pune-based unicorn has recorded around 2.4X growth in revenue in the financial year ending 03.2023, but its losses blew 6X during the same period. Losses for the SoftBank-backed firm spiked 6.15X to Rs 486 crore in FY23 as compared to Rs 79 crore in FY22. Its ROCE and EBITDA margins stood at -7 % and 2%, respectively. On a unit level, it spent Rs 1.12 to earn a rupee in FY23.

Supam Maheshwari is recognised for launching three Indian unicorn companies: FirstCry, Globalbees Brands, and Xpressbees. The case emphasises the importance of rigorous financial audits and investigations, particularly in high-value stock transactions, in ensuring tax compliance.

Many media outlets describe Mr Maheshwari as an Indian version of Elon Musk for his visionary efforts, resilience, and unwavering dedication to launching three businesses. No doubt, one can have such great vision, but history has shown that such great vision often comes with its own hidden secrets. The allegation of tax evasion can be one of them, which categories this company to be a point of investigation.

Ola.

Ola, a trailblazing ride-hailing behemoth that transformed urban commuting, is one of the most sought-after companies in the Indian startup scene. Ola began its journey to revolutionise urban transportation through a dependable ride-hailing platform. Since its inception, the company’s trajectory has been defined by rapid growth and innovation.

From providing unique mobility alternatives such as electric vehicles and bike taxis to expanding into worldwide markets, Ola has constantly demonstrated a commitment to defining the future of transportation. However, underlying its phenomenal success lies an intriguing aspect: Ola’s high cash burn rate, which has piqued the interest of industry analysts and investors alike.

After raising billions of dollars in capital from investors, including SoftBank, Tiger Global, and Sequoia Capital, investors had high hopes for Ola. In FY21, Ola’s revenue decreased by 63%, resulting in losses of ₹174.5 billion. Ola has been running through funds at an alarming rate. Ola’s cash burn rate for the fiscal year ending March 2023 was a stunning $1.3 billion.

As with any other company, one of the primary causes of this cash burn was considerable marketing spending to gain both consumers and drivers. Huge discounts for customers, combined with large incentives for drivers, did little to benefit Ola. Aside from that, Ola expanded into other verticals, where it invested heavily, like Ola Money and Ola Electric.

Ola Electric alone lost ₹3.7 billion in FY22. In FY22, Ola’s operating revenue was ₹19.7 billion, with total expenses of ₹33.6 billion. This led to a loss of ₹15.2 billion. Ola Electric intends to raise roughly a billion dollars in 2024 through a public offering, which will be key to securing the company’s ambitious goals to disrupt the vehicle industry. According to analysts, the value of the business might be around $7 billion, with an issue price range of INR 130 to INR 150. However, Ola Electric has so far failed to impress the grey market participants, and there are many uncertainties about its capabilities to accomplish its gigantic EV goals, making the prospective pricing a little too rich.

With Ola Cabs still struggling to become profitable, founder and CEO Bhavish Aggarwal have shifted his focus entirely to Ola Electric. Now, the stage is set for a historic event in India’s automobile industry: the first initial public offering (IPO) by an Indian pure-play electric vehicle (EV) company and the first auto stock debut in two decades. Ola Electric boosted its goals by submitting its Draft Red Herring Prospectus (DRHP), hoping to raise $1 billion through pre-IPO placements and an IPO in 2024. It seems that Ola is trying to become the poster boy of the EV sector, as aimed once by ed-tech Byju, which is a triggering alarm.

However, the path ahead is far from smooth. Ola Electric, which has sold over 3.5 lakh electric two-wheelers and has an omnichannel network, is also under fire for its overdependence on government subsidies, high valuation, and uncertainty about future product launches, including its ambitious foray into car manufacturing. Will Ola’s sparkling growth story and ambitious infrastructure deployment impress the public markets, or will this IPO fail, leaving investors stuck at the charging station?

There have been a significant amount of service and quality complaints concerning Ola electric scooters on social media channels. Given these concerns, as well as the EV market’s slow growth in the first nine months of FY24 due to a lower FAME II incentive, Ola Electric’s valuation may appear overly high.

Also, the company was under scanner in May last year when the government initiated an investigation into FAME scheme irregularities after whistleblowers raised apprehensions. As part of the investigation, the Commerce Ministry and the Directorate of Revenue were approached to cross-check customs records and determine whether there had been any deviation from the staged manufacturing programme. The company was discovered to be charging clients more than the Rs 1.5 lakh level set by the central government’s FAME initiative in order to receive subsidies.

The company had previously stated that the increased expense was for additional software features and off-board charging. Later, the company announced in their letter to ARAI dated April 30, 2023, that, on their own volition, they would reimburse the price (approx Rs 130 crore) of the off-board charger to all customers who have purchased the off-board charger as an accessory when purchasing an Ola S1Pro model scooter from FY 2019-20 until March 30, 2023.

So, the past attempts to mislead customers and the overpriced valuation of IPOs can be points of concern that regulatory bodies should be vigilant about.

BharatPe.

This name on the list has been making headlines since the beginning of 2022. Its founder, Ashneer Grover, caused a lot of buzz with his appearance on the reality show Shark Tank. BharatPe is a Tiger Global-backed company that offers merchant and business aggregator services. The company provides a universal QR code that shops may use to accept push payments via third-party UPI apps.

It also serves as a conduit for lending partners to make small-ticket loans to merchants to meet their daily working capital requirements. The company collect commissions on these loans.

BharatPe’s revenue from POS machines increased from ₹441 million in FY21 to ₹1.26 billion in FY22. In FY22, commission income increased from ₹720 million to ₹1.52 billion, more than doubling from FY21. In FY22, revenue from loyalty points and related services increased from zero in FY21 to ₹1.08 billion. The company generated ₹6,960 million from advertising, membership, and other services.

Now, let’s look at the expenses to obtain a better perspective.

BharatPe’s losses increased threefold from ₹27.7 bn in FY21 to ₹82.8 bn in FY22. In FY22, BharatPe spent ₹14.83 billion and earned ₹4.57 billion. To make matters worse, its co-founder Ashneer Grover and his wife, Madhuri Jain, were allegedly involved in financial irregularities and fraud. They had to resign for this reason because the case is still pending. Following their resignation, the firm’s board filed several court lawsuits against them, and vice versa.

A preliminary assessment by multinational consulting firm Alvarez and Marsal (A&M), which was recruited to investigate charges of financial impropriety by co-founder and managing director Ashneer Grover and his wife Madhuri Jain Grover, has thrown BharatPe’s operations into doubt. The audit revealed financial irregularities, showing that the firm was paying numerous ‘consultants’ for individuals gained through them. These facts provide a picture of problematic organisational methods, throwing doubt on both the Company’s financial and operational transparency.

According to the investigation, employees reported joining dates that corresponded to vendor bills while remaining unaware of any recruitment via these ‘consultants.’ The involvement of Madhuri Jain Grover, who received and transferred invoices from merchants, many of which originated with her brother Shwetank Jain, is particularly concerning. These bills shared fonts, email addresses, and physical addresses. The research also revealed a clustering of bills from suppliers in Madhuri Grover’s birthplace of Panipat.

Following these revelations, the BharatPe board asked Alvarez & Marsal to perform an independent audit of the company’s internal systems and processes. Ashneer Grover refuted the claims, claiming that he was under pressure to leave the company, which exacerbated the situation. A staggering loss of Rs 5,594 crore was reported during the upheaval, and CEO Suhail Sameer quit. The unexpected departure of high-profile executives raised concerns about the firm’s stability.

Recently, BharatPe has received another notification from the Ministry of Corporate Affairs (MCA) demanding information about its operations and actions taken against co-founder Ashneer Grover. The MCA has also questioned the conclusions of a status report produced by the Delhi Police’s Economic Offences Wing, which looked into claims of financial irregularities at BharatPe. So this makes Bharatpe a point of investigation.

Pristyn Care.

Pristyn Care, a healthcare business, is making waves in the industry by offering elective procedures at reasonable prices and attractive discounts. Recent events raise serious concerns about the company’s aims and procedures, emphasising the necessity for a thorough investigation into its finances and activities.

Pristyn Care’s dubious business practices are highlighted by its relentless pursuit of money, which usually comes at the price of patients’ safety. According to investigations, sales executives are under pressure to hit revenue targets, which might lead patients to undergo procedures that may not be required or in their best interests. There have been instances where patients who preferred non-surgical treatments were repeatedly persuaded to have procedures instead.

Pristyn Care works with hospitals to rent critical infrastructure such as operating theatres. It uses digital marketing and a large sales force to convert web search inquiries into consultations and surgeries in a variety of medical disciplines, including gynaecology, ENT, urology, orthopaedics, dentistry, and others. It is critical to understand that elective procedures are pre-planned and distinct from emergency surgery. Patients frequently seek advice from many doctors before continuing.

At the centre of these worries is a terrible episode involving the unexpected death of a patient, Amita Panchal, a 47-year-old bank employee with mobility issues. Panchal received surgery at a Pristyn Care-affiliated facility. In a terrible turn of events, her condition deteriorated substantially following surgery. Family members, concerned about her deteriorating condition, appealed for the removal of a balloon implanted during the treatment. However, there was a two-day wait before the balloon was extracted. Panchal died tragically, raising concerns about the quality of care and the impact of Pristyn Care’s approach on patient outcomes.

These concerns indicate deeper flaws with Pristyn Care’s operating model. The company’s business model is primarily based on a combination of digital advertising, well-organized sales staff, and inexpensive surgical services. This aggressive expansion strategy has raised concerns that sales executives and medical experts may prioritise surgical treatments to meet financial targets, potentially at the expense of patients’ best interests.

Pristyn Care has categorically disputed allegations of undue pressure for surgery and emphasised its unwavering commitment to preserving the highest levels of patient safety. Nonetheless, sources within the company, who requested anonymity, revealed that doctors’ performance is evaluated based on their conversion rates from outpatient consultations to inpatient surgeries (OPD to IPD ratio), implying that financial incentives may influence medical decisions.

However, this is not the only area of concern. The company’s internal work climate, characterised by significant attrition rates—particularly in departments responsible for patient care coordination and finance—has sparked concerns about its impact on overall care quality.

Pristyn Care’s financial audit from last year revealed “material weaknesses” in its internal controls. In its qualified opinion on Pristyn Care’s internal controls, the auditor identified substantial shortcomings in three areas: hospital and patient price, doctor agreements, and vendor selection.

First, the auditor found that Pristyn Care lacked internal procedures for accurately determining fees invoiced to patients or hospitals. Second, a Pristyn employee presented the auditor with “some documentary material in regard to agreements with doctors that were not real.”The auditor stated that internal controls for “review and authorization of the calculation of doctor expenses” partially relied on “unsigned agreements.” Third, Pristyn’s vendor selection procedure, which involved competitive price analysis, was not running well.

All of these problems may result in an overstatement or understatement of recognised revenue, as well as an overstatement or understatement of expenses associated with surgeries, doctors, or patients on the books. According to the auditor, it might also result in improper disbursements for doctors and negative marketing for vendors.

To be true, numerous high-profile businesses have sparked auditors’ concern about internal controls. The auditor for edtech major Byju’s expressed an ‘adverse view’ on its internal controls relating to customer collections and revenue recognition in FY21, while auto service company GoMechanic was found to have failed to implement internal controls despite being obligated to do so. Later, the founders of Gomechanic openly admitted to the company’s financial irregularities, and you are familiar with Byju’s past and present.

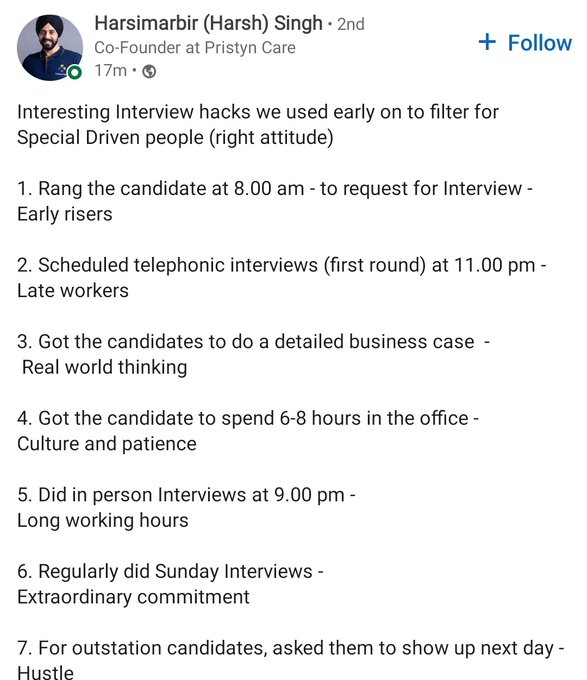

Also, if you are worried about how unusual targets might have been given to the salesperson, then this post of one of their co-founders, Mr Harsimarbir Singh, will blow your mind in anger; he elucidated at length about the so-called “interview hacks” used at the health-tech company to screen out candidates. Despite the fact that Harsimarbir Singh appears to have removed his offending LinkedIn post, screenshots of it have been extensively shared and heavily attacked on Twitter and other social media sites.

Singh’s tactics included making applicants wait six to eight hours to test their patience, scheduling interviews in the early morning or late at night, scheduling interviews on Sunday, and requiring outstation candidates to show up to the office the following day.

“I have worked in this company for three months. And this person seriously wants everyone to work at least 12 hours a day in the office. He even used to scold/shout at the employees in front of 60-70 people. I have witnessed some of them crying, too. Sometimes, I have seen him checking on employees. who is leaving early? And early se, I mean before 7 pm,” commented a Twitter user. “If you work in Pristyn, get in touch with me, and I’ll happily help you get jobs at companies with a better culture,” wrote another Twitter user.

A significant portion of the professional workforce has criticised these practices as outdated and toxic, particularly during the ‘Quiet Quitting’ movement, in which workers refuse to work unpaid overtime or take calls after work hours – in other words, do the bare minimum required of them at their jobs.

This is not the end. Recently, last month, it was hospitals vs. Pristyn Care again. One of India’s most valuable health IT businesses has faced criticism for providing “false, fraudulent, and misleading statements” to patients. In January 2024, Pristyn Care received a legal letter last month from a group of 24 hospitals about two of the company’s websites, Medifee.com and Healthprice.in. All the contact numbers on these websites are directed to Pristyn Care and not the hospitals. In fact, the website features few options to get in touch with hospitals, but the numbers again redirect one to Pristyn representatives.

The bottom line.

Given the worrisome findings affecting certain well-known Indian companies, it is becoming increasingly evident that a thorough audit of firm funds and activities is not just warranted but absolutely necessary. The startup ecosystem, once praised as a sign of innovation and expansion, now urgently requires scrutiny and accountability of every individual company. Growing concerns about valuation anomalies, false financial statements, and prioritising profits over conscience raises severe questions about these companies’ reliability.

Investigations into these companies seek to protect not only the interests of investors but also the reputation of the Indian startup community. It is critical that businesses adhere to moral standards, keep financial transactions transparent, and prioritise the interests of their customers. India’s startup scene’s future is dependent on its ability to confront these difficulties head-on, fostering accountability and moral behaviour. The only option for these companies to regain lost confidence and pave the road for a stronger, more dependable startup environment is to implement tight oversight and corrective actions.