Mamaearth IPO: How Startups Like Mamaearth Are Making Fools Of Indians By Their Marketing Tactics!

Did Mamaearth bought something toxin-free in the market for the first time, or were there already toxin-free products, and Mamaearth just played their parent-child bonding card to lure and fool the customers?

So, in less than or about 24 hours, we are going to see the much-waited, hyped and somewhere criticised video of the last 365 days, the IPO of Honasa Consumer Limited, aka the Mamaearth IPO. Before you make up your mind to invest or not invest in the Mamaearth IPO, read this piece of essay on whether the startup Mamaearth is really such a great company or just a fantastic case of ‘Marketing Goodness’ that has successfully gimmicked the Indian customers?

Did Mamaearth really innovate something new to the market?

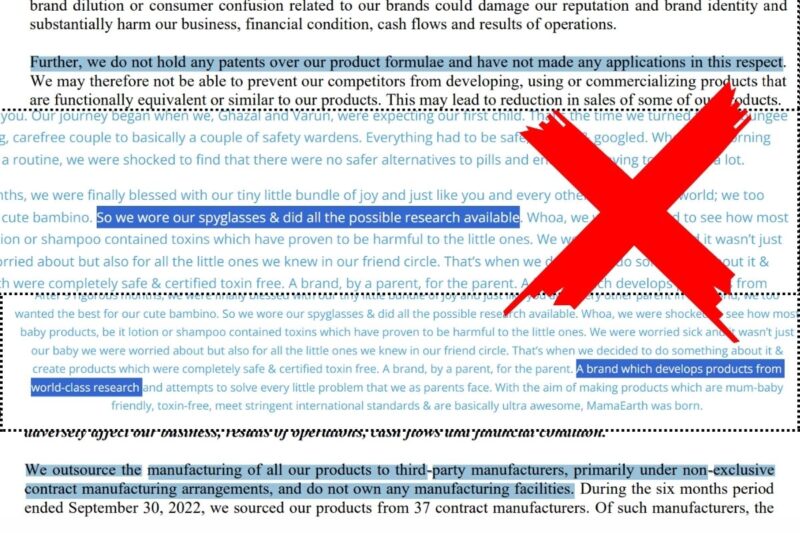

The ‘https://mamaearth.in/our-story’ section of Mamaearth page says, ‘So we wore our spyglasses & did all the possible research available’. However, the DRHP of Mamaearth ‘https://www.bseindia.com/corporates/download/332525/DRHP_20221229142958.pdf’ mentions something contradictory. Page 48 says, ‘We do not hold any patents over our product formulae and have not made any applications in this respect’. So my question is, if Mamaearth doesn’t have any patents, then how could they mention on their website that they have researched something? Isn’t that misleading to the customers?

How could a company claim that there were no better products in the market, and they bought something new that anyone else hasn’t? That’s where the question arises: there may be many other good baby care products in the market. It’s just that Mamaearth used the concept of parental emotions to connect with the people without actually doing something new?

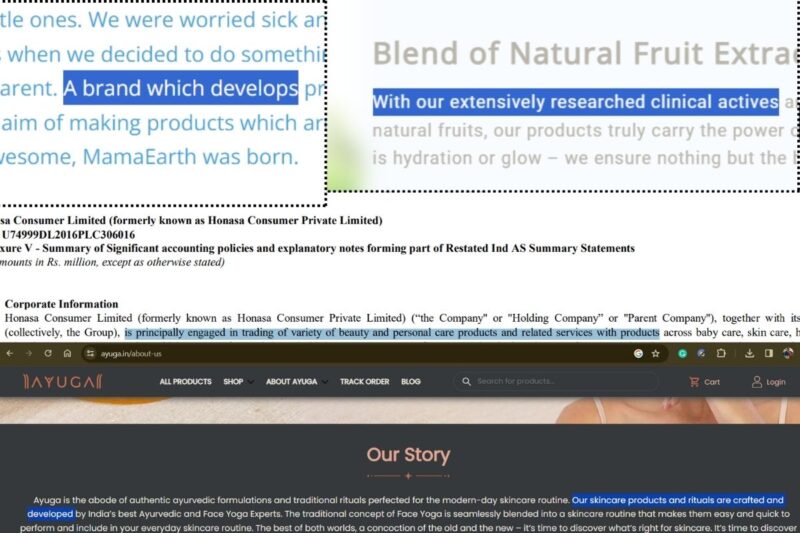

Also, as one moves ahead on the same page, you can see the lines that means that it is a brand that develops the products from world-class, extensive research and attempts to solve every little problem that parents face. But the DRHP (Page 42) says, ‘We outsource the manufacturing of all our products to third-party manufacturers’, which means Mamaearth has no in-house manufacturing unit; then how are they developing their own products? Again, a question on innovating their own products!

The paragraph in DRHP further reads, ‘We outsource the manufacturing of all our products to third-party manufacturers, primarily under non-exclusive contract manufacturing arrangements, and do not own any manufacturing facilities’. Now, a non-exclusive contract allows the contracting parties to contract with any other party, which means they can enter into another contract with anyone apart from each other for the same service or transaction of goods.

That means any other company can use the same formula or sell the product in a different packaging. Also, Mamaearth can use someone else’s formula, put them under their bottles and sell into the market! That’s raising questions about the authenticity of their products? Did Mamaearth bought something toxin-free in the market for the first time, or were there already toxin-free products, and Mamaearth just played their parent-child bonding card to lure and fool the customers?

Moreover, the Corporate Information in DRHP, Page 221, says that the company ‘ is principally engaged in trading of a variety of beauty and personal care products and related services with products’ instead of developing, creating, crafting, designing formulations, as mentioned in their various websites. Then how can one get convinced that they are actually getting something new on the table and not just trading the Beauty and Personal Care (BPC) products?

On page 316 of DRHP, it is mentioned that ‘Expenses include purchases of traded goods, increase in inventories of traded goods, employee benefits expenses, depreciation and amortisation expenses, finance costs, other expenses and change in fair valuation of preference shares’. In the entire section, there is ‘no expense for the purchase of raw materials’, which raises eyebrows: where is the innovation?

Page 142 of DRHP mentions that ‘Honasa launched at least 2.6 times higher number of new SKUs than the BPC industry median during Financial Year 2022’. Also, Page 146 says that the company introduced 159 and 225 new SKUs (Stock-keeping units) in the BPC market in India during FY2022 and during the 6 months period ended 30.09.2022, respectively. How is it possible that a 7-year-old company with no in-house manufacturing facility and no patent could launch such a great variety of products that they claim to be an outcome of their ‘special formulation’?

It again points out that they do not have any unique formula for their products, and there are similar products on the market; however, they took the opportunity to ‘become first and not become best’! There is no problem in contract manufacturing, but under a non-exclusive format, it seems that Mamaearth does not care about their ‘special toxin-free formulations.’ So, what is the point of being a toxin-free market leader? It’s just a game of marketing!

Moreover, Honasa Consumer Limited acquired a content platform, ‘Momspresso’, on which they suffered a giant loss, just in an attempt to promote the products. Their other acquisitions, like Dr Sheth’s and BBlunt, have individual items on them, while Momspresso was just there as an advocate of Honasa Products, comprising of working or non-working women who are supposed to give positive reviews about their products. It seems that brand awareness is more important for Mamearth than the individuality of the product.

This again can be witnessed in the DRHP that mentions the money generated from the IPO will be used for ‘Advertisement expenses towards enhancing the awareness and visibility of our brands; Capital expenses to be incurred by our Company for setting up new EBOs (Exclusive Brand Outlets); Investment in our Subsidiary, Bhabani Blunt Hairdressing Private Limited (“BBlunt”) for setting up new salons; and General corporate purposes and unidentified inorganic acquisition.

It is nowhere mentioned that the company wants to invest more in the ‘specialised toxin-free formula’ that they even hadn’t patented. Seems like Mamaearth is more towards ‘creating brand empire’ rather than ‘creating toxin-free product’.

Now, let’s leave DRHP; let’s talk about the usage of products. Are they really toxin-free?

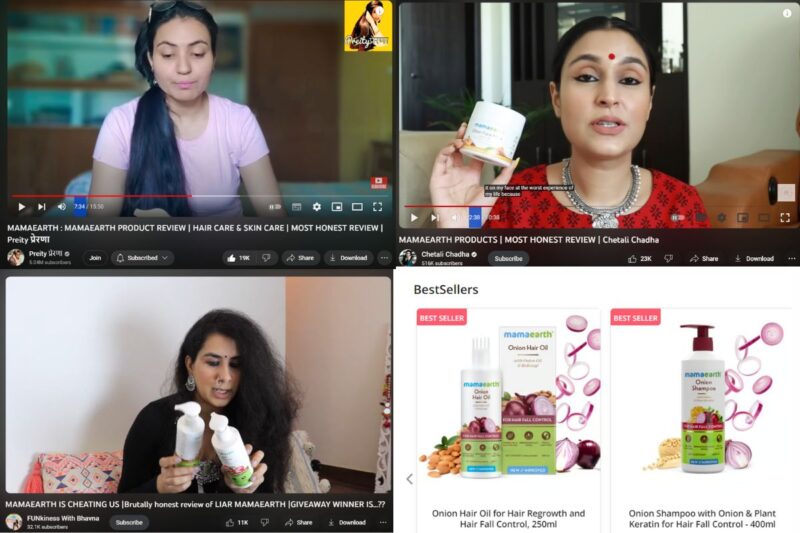

The first one, Mamaearth’s ‘Onion Shampoo with Onion & Plant Keratin for Hair Fall Control’, happens to be one of the best-sellers on their website. However, a YouTuber with a channel name ‘Preity प्रेरणा’ mentions how this product was a disaster not only for her but for many in her circle, having different skin types. Not only that, but the customers also commented how this product discouraged them from being toxin-free. A similar kind of unacceptable experience occurred with Conditioner as well. And the list add more products like the same, which were not toxin free.

Not only one YouTuber but another one with the name ‘Chetali Chadha’, also argued that the products were disappointing. Moreover, she voiced out that no celebrities have spoken about it. The next one who mentioned that Mamaearth cheated her is ‘FUNkiness With Bhavna’.

So, one thing is for sure. If you are thinking that they are completely natural, then just wait. So many negative comments show that not everyone can be wrong. Mamaearth may have used artificial, synthetic chemicals in their products, haven’t mentioned them in their ingredients, and have fooled consumers on the name of toxin-free products!

Is it worth investing in Mamaearth IPO if you are a retail investor?

Well, there is no sure ‘Yes’ or ‘No’ for this question. What we are trying to decode are some meaningful insights that can help you take your call.

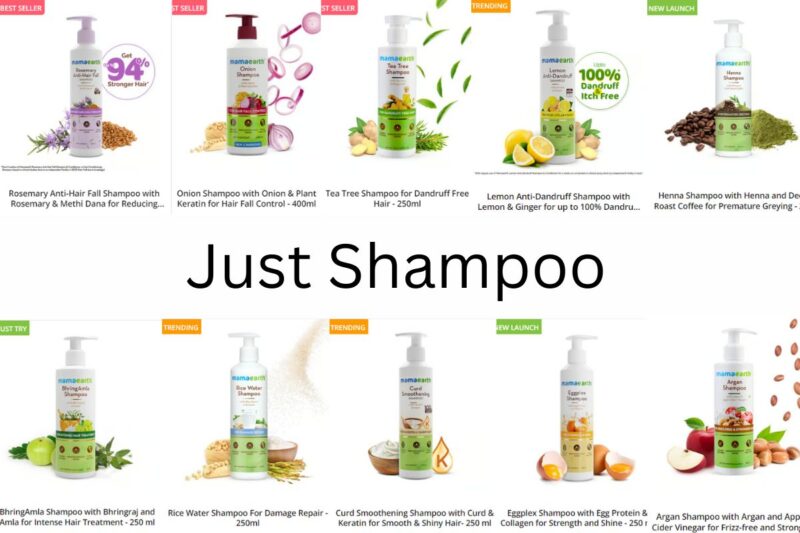

The first one. From all the above-mentioned data about launching new SKUs, it seems that Mamaearth is more into marketing its brands, acquiring new brands and adding them under its ‘House of Brands’ rather than innovating or improving their product. There is nothing wrong with acquiring new brands and adding them under their own umbrella. But this has to stop somewhere. In the race to be first, Mamaearth is continuously running behind, launching and acquiring more and more and more.

For example, check out the Mamaearth website; they have 10 variants of just Shampoo. Oh My God, to capture the market, they have taken every possible thing under their name. This needs to stop somewhere. Moreover, if they are supposed to spend such a huge amount on marketing, then where is the margin going to come from? Even if they make a margin, it would amount to be relatively small. Then why should I, acting as a retail investor, should put my funds into the company?

Another point till now is that Mamaearth has positioned themselves as ‘Digital First’, an online D2C brand, where they are selling directly to their customers, and hence, in this way, it can increase its commissions and earn a great margin. But this is not totally correct. The revenue from offline channels across all brands of Honasa Consumer Limited stood at 35.39% of the revenue from operations during the six-month period ending September 30, 2022. So, offline has many middlemen who are engulfing the margins, and hence, what the retail investor will get?

Moreover, Mamaearth, as said earlier, has positioned itself as an online brand and has generated millions of funds through investors and consumers by promising that they are a digital-first brand. Now, suddenly going public, they are mentioning in their DRHP that being offline is more profitable. Why this 180-degree shift? Will the retail investors are going to pay for this experiment?

It can happen that the market for the BPC industry in the coming years will explode, and Mamaearth can be a leader in the market; hence, infusing your money into this company is worth it. But do you think other traditional players will sit ideally in the market? The answer is NO. So if Mamaearth enters into a new ball game of offline channels, they will get aggressive competition from the traditional players who are already having their lands embarked in the offline market. In such a situation, Mamaearth may have to compromise on its margins. So the question remains the same: where will that margins come from? So think judiciously if you are a retail investor!

And now the giant enemy marks their entry, the hurdle of VALUATION that everybody is worrying about. If the valuations don’t improve in a couple or triplet of years, then……what is the justified valuation of the company? Recall the Nykaa IPO, which gave a huge amount of return to one of the major film actresses. It seems like Mamaearth also wants to replicate the same.

There are a plethora of articles circulating on the internet that Shilpa Shetty Kundra, one of the early investors of Mamaearth, is expected to make an 8X return from this bumper IPO. Also, Snapdeal co-founders Kunal Bahl and Rohit Bansal, who were the first supporters of Mamaearth, are expected to make 108 times their initial investments.

It seems that this IPO is not for the innovation of better products in the company, not for the consumers, not for the retail investors, but a Diwali Bumper Bonanza for the early-stage investors so that they can say goodbye to the company. Well, there is no problem in gifting the early-stage investors, as they were the first ones to support, but gifting them at the cost of retail investors’s money may not be justified!