There is a particular kind of corporate audacity that announces itself not through secrecy but through sheer repetition — a developer that launches project after project, collects crore after crore from trusting homebuyers, fails to deliver, offers excuses, fights legal battles through every available forum, and then, having exhausted the patience of buyers, regulators, and courts alike, turns confidently to the capital markets and says, “invest in us” or “give me more money so that we can betray you”…

That developer is BPTP Ltd — Business Park Town Planners — a Gurugram-based real estate company that has spent the better part of two decades building one of the most documented records of project delays, homebuyer harassment, fund diversion allegations, and regulatory non-compliance in India’s National Capital Region. And as of late 2025, BPTP is actively preparing an Initial Public Offering, appointing merchant bankers, projecting revenues of ₹5,500 crore for FY2025-26, and presenting itself to retail investors as a growth story worth backing.

This article argues, with detailed evidence drawn from court judgments, regulatory orders, enforcement agency actions, and documented buyer testimonies, that SEBI has a compelling public interest obligation to conduct the most rigorous possible scrutiny of BPTP’s IPO before a single retail rupee is committed — and that based on the record currently in the public domain, there are serious grounds to question whether that IPO should proceed at all in its current form.

Section I: The Company and Its Land Bank — Understanding the Scale of the Claim

BPTP Ltd was incorporated and began active real estate development in the mid-2000s, positioning itself as a large-scale township developer in the Delhi NCR region, with its primary operations concentrated in Gurugram and Faridabad. The company’s promoters built the enterprise around a straightforward proposition: acquire large land parcels in high-growth corridors, launch residential and commercial projects at scale, collect buyer advances, and complete delivery over a 3–5 year horizon.

On paper, the land bank has always looked impressive. As the Economic Times reported in November 2025, BPTP is touting a land bank of 45 to 50 million square feet and claims to have ₹6,000 crore worth of projects under active development on the Dwarka Expressway corridor alone, with new project launches planned at a rate of approximately ₹10,000 crore annually going forward. The company claims revenues of ₹3,000 crore for FY2024-25, with a stated target of ₹5,500 crore for FY2025-26. The July 2025 launch of Gaia Residences — a 1,600-unit luxury complex on Dwarka Expressway marketed as a ₹3,000 crore investment — was positioned as evidence of BPTP’s continued market relevance and ambition.

These are the numbers that will appear on the front pages of the IPO prospectus. They are not false numbers — but they are dangerously incomplete ones. And the incompleteness is not accidental.

Section II: The Projects — A Graveyard of Broken Promises

To understand the full weight of BPTP’s legacy liabilities, one must go project by project. This is not an exercise in cherry-picking failure; it is the comprehensive picture that emerges when you examine RERA filings, court records, and buyer testimonies across the company’s entire portfolio.

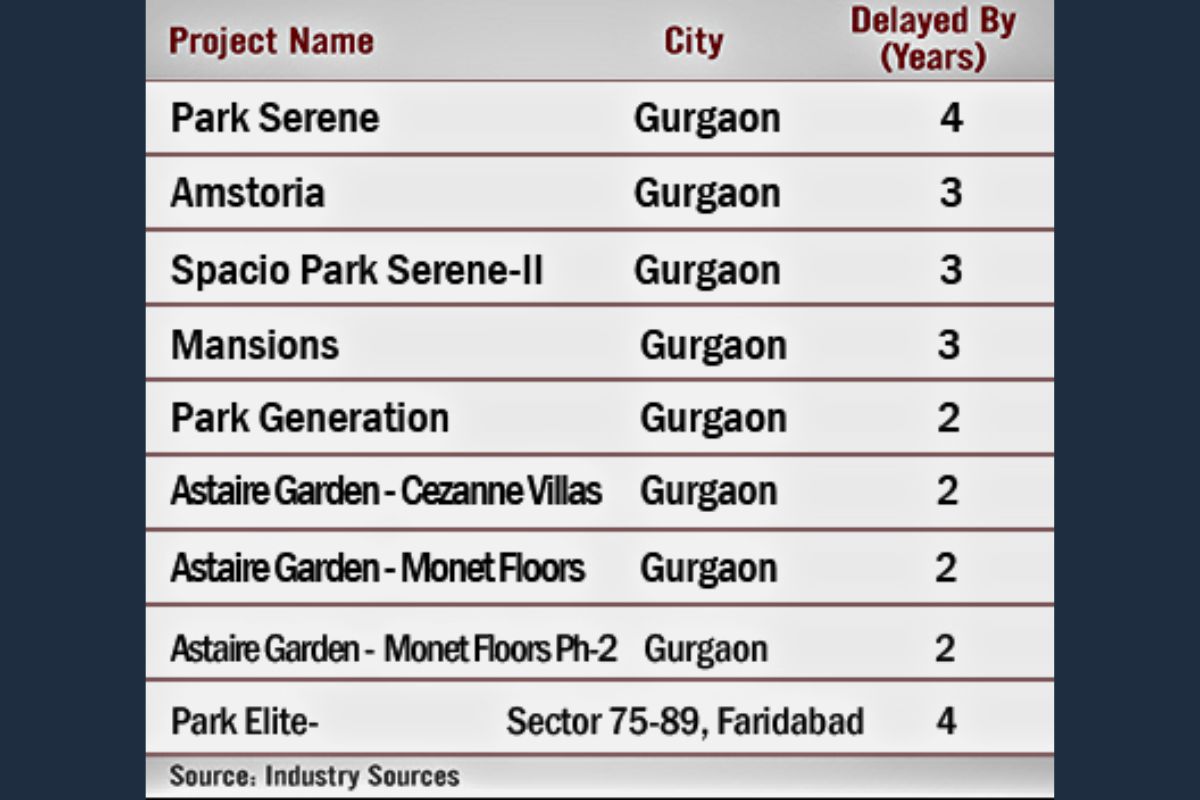

BPTP Spacio, Sector 37D, Gurugram

Spacio was launched approximately in 2010 as a mid-to-premium residential project in Gurugram’s rapidly developing Sector 37D. The promised possession date given to buyers was 2014 — a standard four-year delivery timeline for a project of its scale. Buyers paid large proportions of the total purchase price upfront, relying on that timeline for their financial planning.

Possession was not offered until mid-2021 — nearly a decade after launch and seven years after the promised handover. But the delay itself was not the end of the harassment. As the Times of India reported in 2021, buyers who had already paid approximately 95% of the flat’s total cost were then presented with demands for an additional ₹15 to ₹20 lakh in what BPTP called “escalation charges.”

Buyers described a situation where the company had obtained an Occupancy Certificate for select towers and then used that certificate as leverage — sending possession offer letters that were conditioned on payment of these additional charges. Refuse, and possession would be withheld indefinitely. Comply, and you validated charges that buyers argued were entirely unilateral and legally indefensible.

One buyer’s account, captures the human texture of this experience: having paid the near-entirety of a flat’s cost over seven years, maintaining EMI payments to a home loan account, and simultaneously paying rent because the promised home did not exist, they were then confronted with an escalation demand equivalent to 25 to 30% of the original flat cost. Appeals to the Chief Minister’s grievance cell and the Prime Minister’s Office yielded, in the buyer’s words, no relief whatsoever.

Park 81, Sectors 81–82, Faridabad

The Park 81 project — a villa and group housing development in Faridabad’s Sector 81 — represents one of the clearest documented cases of BPTP’s delay pattern. Buyers booked villas between 2009 and 2011 on the explicit promise of possession by July 2014. That promise was not kept. Possession was not offered until June 2023 — nine years after the promised date and, in some cases, twelve years after booking.

But even the June 2023 possession offer came with conditions. BPTP demanded extra payments from buyers before handing over the properties — payments that buyers, having already waited nearly a decade beyond the contractual deadline, were understandably unwilling to treat as legitimate. In litigation before Haryana RERA (HARERA), one buyer challenged both the delay and the extra-payment demands.

On December 16, 2024, HARERA ruled decisively in the buyer’s favour. The regulator found that the delays were the builder’s fault and ordered BPTP’s relevant entity to pay approximately ₹39.6 lakh in delay interest to the buyer. Critically, HARERA explicitly rejected BPTP’s force majeure arguments — arguments that had invoked COVID-19 and environmental clearance delays as justification for the non-delivery. The regulator’s reasoning was blunt: the promised handover date was July 2014. COVID-19 occurred in 2020. A six-year delay that predated the cited force majeure event by six years cannot be attributed to that event.

The HARERA judgment also addressed a procedural manoeuvre that BPTP had attempted in that case: the company argued that a “full and final settlement” agreement purportedly signed in June 2023 extinguished the buyer’s right to claim delay interest. HARERA found that the alleged settlement had been signed by only one allottee and was not binding, stripping BPTP of this procedural shield and allowing the interest claim to proceed.

Parklands and Parklands Pride, Sectors 77–85, Faridabad

The Parklands family of projects — covering multiple phases across Faridabad’s Sectors 77 through 85 — represents the largest-scale delayed delivery situation in BPTP’s Faridabad portfolio. RERA filings show these projects were registered between 2011 and 2024, with official completion dates now extending into March 2029 in some cases — a registered completion timeline that, given BPTP’s track record, should itself raise serious questions.

One documented case from the Parklands project provides particularly instructive data. A buyer booked a plot in 2006 and paid approximately ₹43.13 lakh by 2015. Despite this nine-year payment history, the buyer did not receive possession of the originally allotted plot. BPTP eventually offered possession of an alternate plot in 2018 — twelve years after the original booking. The buyer refused and sought a refund with interest through legal channels.

The case eventually reached the Supreme Court of India. In September 2025, the Supreme Court directed BPTP to refund the buyer’s money with 18% annual interest. The reasoning of the Court is worth examining carefully because it reveals the Supreme Court’s assessment of BPTP’s conduct. Lower forums had awarded 9% interest on the refund. BPTP had, in its own buyer agreements, charged 18% per annum interest on buyers who made late payments.

The Supreme Court’s logic was elegant and cutting: if BPTP considers 18% the appropriate rate of return on delayed money when buyers are late, then 18% is the appropriate rate when BPTP is late. The differential treatment — 18% for BPTP’s benefit, 9% for the buyer’s benefit — was precisely the asymmetry the Supreme Court corrected. (Supreme Court, Parklands judgment, September 2025.)

Terra Flat Buyers Association v. BPTP

Another Supreme Court case, decided in November 2024, involved the Terra Flat Buyers Association — a collective of BPTP flat buyers who had organized to pursue their claims jointly. The Supreme Court, in this matter, ordered BPTP to refund money to the flat buyers with 9% interest. In February 2025, BPTP appealed on the question of interest rates, and the Supreme Court partly allowed that appeal on the specific interest rate issue — but the core finding of BPTP’s liability for refunds to buyers was not disturbed. (Terra Flat Buyers Assn v. BPTP, Supreme Court, November 2024; February 2025 modification order.)

This order is one of several Supreme Court rulings against BPTP, and it is significant because it confirms a pattern — a consumer court found BPTP guilty, BPTP appealed to the Supreme Court hoping to reduce or escape liability, and the Supreme Court largely upheld the buyers’ rights.

Other Faridabad Projects: Park Elite Premium, Park Arena, Discovery Park, Princess Park

BPTP’s Faridabad portfolio extends across Park Elite Premium (Sector 84), Park Arena (Sector 80), Discovery Park (Sector 80), Princess Park (Sector 86), and the Deck and EWS schemes in Sector 82. Across all of these, RERA registration records and buyer complaints reflect a consistent pattern: launch dates in the 2009–2015 range, promised completion dates that were never met, and buyers who have spent years navigating a labyrinth of demands, partial possessions, and legal proceedings.

A buyer of a Park Elite property described to a particularly egregious practice: BPTP had billed the buyer for a “super-area” increase — essentially charging the buyer for additional square footage that the buyer had not agreed to in the original contract. When the buyer complained, their flat was, in the buyer’s account, effectively “blocked” by the developer for a year — meaning that possession was withheld as a form of economic coercion against a buyer who had dared to question an illegitimate charge.

Now, this is an ironically interesting part of the story. This tricky idea of BPTP using ‘super-area’ to harass the homebuyers is (perhaps) taken from their familiar roots, another giant builder of Haryana, TDI Infrastructure, who is known to have notorious background in making the roads to Haryana. If you are wondering how TDI and BPTP is connected, then follow this article to know the family ties of homebuyers harassment.

A brief about this case is- TDI Infrastructure lost a RERA complaint filed by a homebuyer in January 2019. For the next four and a half years, instead of complying with the order and paying the buyer his due compensation, TDI used a series of legal applications — each one slightly differently framed — to avoid paying and to delay the matter. Every single attempt failed because TDI kept refusing to do the one thing the law required: deposit the money while the appeal is pending.

TDI Infrastructure refused to accept the loss and kept fighting — not on the merits of the case, but through procedural tricks. What follows is essentially a story of TDI repeatedly trying to reopen a closed door, and the Tribunal repeatedly shutting it.

This case is a textbook example of how a resourced developer can use procedural litigation — filing one application after another, each with a slightly different legal argument — to delay compliance with a homebuyer’s legitimate order for years, even when the legal grounds for each application are weak or nonexistent. The buyer won in January 2019. Four and a half years later, in July 2023, the buyer is still in proceedings because the developer kept the legal machinery running. That gap between winning on paper and receiving money in hand is one of the most significant practical failures of the homebuyer protection system in India.

Gurugram Projects: Amstoria, Verti Greens, The Amaario

In Gurugram, BPTP’s township development at Sector 102 — marketed under the “Amstoria” brand and including phases called Verti Greens and The Amaario — represents another tranche of delayed high-value developments. These are positioned in marketing materials as premium residential offerings in one of Gurugram’s most sought-after corridors. RERA registration records confirm these projects were registered in the post-2017 RERA era, which means their timelines are legally enforceable in ways that pre-RERA projects were not.

The July 2025 launch of Gaia Residences — also in Sector 102 on the Dwarka Expressway — as a 1,600-unit complex with a ₹3,000 crore investment announcement was positioned by BPTP as a statement of confidence and growth momentum. But buyers of earlier Amstoria phases who are still waiting for possession see it differently: as evidence that BPTP’s capital and management attention are being directed toward new launches and new revenue collection rather than toward completing commitments already made to existing buyers.

Section III: The Human Cost — Years of EMI, Rent, and Waiting

The financial and human impact of BPTP’s delays cannot be adequately conveyed through legal citations alone. Behind every court case and RERA order is a family whose life plan was built around a home that did not come.

The most common financial consequence is what buyers describe as “double burden”: paying a home loan EMI every month on a flat that does not exist while simultaneously paying rent for the accommodation they must actually live in. In a market like Delhi NCR, this double burden — over seven, nine, or twelve years — can amount to tens of lakhs in additional expenditure that was never budgeted for, and which the legal system’s compensation mechanisms have only partially addressed.

NDTV’s 2016 investigative report — titled “Big Developers, Big Delays: BPTP” — documented approximately 15 BPTP projects that were delayed by more than three years at that time, with an estimated 5,000 homebuyers described as being “stuck in limbo.” That figure — 5,000 buyers in 2016 — does not account for the many additional buyers who booked in projects launched or expanded after 2016, nor for the buyers of projects that were supposed to have been resolved by 2016 but were not. The actual number of BPTP homebuyers affected by significant delays across the full project portfolio is almost certainly several times that figure.

Buyers reported to NDTV that they had written to “all administrative levels” — including the CM’s office and PM’s grievance cell — without result. Some organized protests at Jantar Mantar in New Delhi, demanding government intervention. As ET Realty reported in 2016, these protests reflected a community that had exhausted patience with both the developer and the regulatory system that was supposed to protect them.

Perhaps the most corrosive aspect of the experience, as reported consistently by buyers across multiple projects and multiple years, is the systematic use of possession as a bargaining chip. BPTP’s pattern — obtaining Occupancy Certificates and then using the possession offer as leverage to extract additional, uncontracted payments — is not incidental misconduct. It is a business practice that converts the buyer’s natural eagerness to finally receive their home into a mechanism for extracting additional revenue from people who have already paid the full contracted price and waited years beyond the promised date.

Section IV: Legal Evasion — How BPTP Has Tried to Cover Its Tracks

BPTP’s legal strategy across consumer forums, RERA, NCDRC, and the Supreme Court reveals a consistent pattern: use every procedural tool available to delay, reduce, or eliminate liability, regardless of the underlying merits.

The most common technique has been the invocation of force majeure — environmental clearances, NGT (National Green Tribunal) orders, and most recently the COVID-19 pandemic — as justification for delays that, as regulators have repeatedly found, substantially predated those events. In the Park 81 case, HARERA explicitly rejected this argument because the promised 2014 delivery could not plausibly be attributed to a 2020 pandemic. Yet BPTP has deployed the same argument across multiple proceedings, in what appears to be a standard template response rather than a case-specific factual defence.

The “full and final settlement” manoeuvre — seen in the Park 81 HARERA case — is another technique. Here, BPTP attempts to extinguish a buyer’s claim by producing a settlement document, sometimes signed by only one of multiple allottees, and arguing that it bars further compensation claims. HARERA saw through this in December 2024, finding the purported settlement invalid and allowing the delay-interest claim to proceed. But the existence of the manoeuvre — and the resources BPTP devotes to constructing it — is itself instructive.

BPTP has also deployed unilateral contractual provisions to defend its practices. For instance, agreements that granted BPTP the right to increase the “super-area” of a flat — and charge buyers accordingly — were invoked to justify what buyers experienced as arbitrary post-sale price increases. Consumer forums and HARERA have generally found such provisions to be unreasonable and unenforceable against buyers who had no meaningful bargaining power at the time of signing. But fighting those provisions costs buyers legal fees, time, and emotional energy.

BPTP’s 2016 public statement to NDTV — in which the company claimed to have reduced its debt from ₹900 crore to ₹300 crore and said it was selling land to fund construction — is worth examining in retrospect. If the debt reduction was genuine and the land sale proceeds were directed to construction, the delays that continued for years after 2016 become even harder to explain on purely operational grounds. What the statement reveals, however, is that BPTP’s primary financial management priority at the time was balance sheet repair through asset sales, not the completion of homes that buyers had already paid for.

Section V: The Enforcement Directorate’s Investigation — Allegations of Fund Diversion and FEMA Violations

The most serious institutional action against BPTP to date has come from the Enforcement Directorate, India’s financial crimes investigation agency.

In August 2025, the ED conducted raids on BPTP’s offices and the residences of its directors across the NCR, acting under the provisions of the Foreign Exchange Management Act (FEMA). The ED’s press release, which followed the raids, contained allegations of significant gravity.

According to the ED’s findings, BPTP received foreign direct investment exceeding ₹500 crore between 2007 and 2008 through entities incorporated in Mauritius. The violation alleged by the ED is that this FDI was structured with illegal “put option” and “swap” clauses — contractual provisions that guaranteed foreign investors a specific return on their investment regardless of BPTP’s actual business performance.

Such clauses are prohibited under FEMA’s FDI regulations because they effectively convert an equity investment (which is supposed to carry market risk) into a guaranteed-return instrument, which has different and more restrictive regulatory treatment. The Reserve Bank of India had specifically directed BPTP to remove these impermissible provisions, and the ED alleges that BPTP failed to comply with those directions.

The ED’s investigation is ongoing. The investigation has the potential to segue into a Prohibition of Money Laundering Act (PMLA) investigation if the alleged FEMA violations are found to constitute predicate offences — a development that would dramatically escalate the legal jeopardy facing the company and its promoters.

Perhaps equally significant is what the ED said beyond the FEMA allegations. The agency noted in its communications that it had uncovered “multiple FIRs” registered against BPTP and its directors across various Delhi-NCR police stations, specifically in connection with “non-completion of various projects for a long period of time and diversion of funds.” The existence of these FIRs — which the ED’s investigation is examining as part of the broader financial probe — is a detail that appears nowhere in BPTP’s public communications and promotional materials around its IPO plans.

It is worth pausing here to appreciate the full weight of what the ED’s statement implies. The allegation is not merely that BPTP was a developer that ran into construction delays due to market conditions or regulatory complications. The allegation is that funds collected from homebuyers were diverted — meaning that money paid by buyers for specific projects was not used for those projects. If that allegation is sustained, it explains the persistent gap between the money collected and the construction completed in a way that no force majeure argument, no pandemic, and no environmental clearance delay can account for.

It has reported that, years earlier that buyers had filed complaints at “all administrative levels” but that the administration had “failed to file an FIR” against BPTP. The ED’s August 2025 disclosure suggests that FIRs have in fact been registered at local police stations — but that their investigation has not progressed to prosecution. This is consistent with a pattern, well-documented across Indian real estate fraud cases, where well-resourced developers use their connections and legal resources to delay police investigations indefinitely while buyers exhaust themselves in consumer forums.

Section VI: The IPO — Retail Investors as the Final Exit

It is against this backdrop — delayed projects numbering in the dozens, an estimated thousands of unpaid buyers, multiple Supreme Court orders against the company, active RERA enforcement proceedings, an ongoing ED investigation into FEMA violations, and multiple FIRs for fund diversion — that BPTP has decided that 2026 is the moment to approach India’s public capital markets for an IPO.

It was reported in November 2025 that BPTP was in the process of appointing a merchant banker to manage the listing. The company’s pitch to potential investors centres on its land bank of 45 to 50 million square feet, its revenue trajectory (₹3,000 crore in FY2024-25, targeting ₹5,500 crore in FY2025-26), and its strategic position on the Dwarka Expressway — one of the NCR’s most active residential corridors. The July 2025 launch of Gaia Residences is cited as evidence of product pipeline and demand. The ₹6,000 crore claimed to be under development on Dwarka Expressway is presumably intended to convey scale and momentum.

There is a historical footnote that the reporting does not emphasize but that investors deserve to know. BPTP attempted an IPO before. It was reported in 2011 that BPTP had received an earlier IPO approval that ultimately lapsed without being used. The reasons for that lapse were not definitively reported, but the timing — coinciding with the early years of the very project delays that have since become BPTP’s defining legacy — is worth noting.

The fundamental question for SEBI and for retail investors is this: what exactly will the proceeds of this IPO be used for, and who benefits from it?

In a real estate developer IPO, one of the most critical questions is whether the IPO proceeds are intended to fund genuine new development — creating new value — or whether they are being used to resolve legacy liabilities, settle ongoing legal judgments, fund working capital shortfalls created by fund diversion, or provide an exit to promoters and early investors who have been holding illiquid positions in a company with a deeply troubled record.

The ₹500 crore FDI from Mauritius — which the ED alleges came with illegal put/swap clauses — effectively means that early foreign investors in BPTP were promised a guaranteed exit. If those clauses are ultimately found to be enforceable (or if BPTP settles with those investors to resolve the ED case), the money to fund those exits has to come from somewhere. An IPO is a remarkably efficient mechanism for transferring that obligation onto retail investors who have no knowledge of the underlying structural problems.

The dozens of court cases — Supreme Court orders, HARERA orders, NCDRC decisions, ongoing RERA complaints — represent financial liabilities that, in many cases, have not yet been fully quantified or provisioned. When a buyer wins a Supreme Court order for a refund at 18% per annum on a ₹43 lakh booking, the liability is specific. But across hundreds or thousands of such cases, the aggregate liability is enormous — and how it is presented, if at all, in the IPO’s financial disclosures will be one of the most important questions SEBI must press on.

Then there is the matter of the ongoing ED investigation. Any SEBI due diligence process worthy of the name must grapple with the fact that at the time of this IPO’s preparation, the company is the subject of an active FEMA investigation by the country’s primary financial crimes enforcement agency, with seized documents, alleged violations running to ₹500 crore in FDI, and a press release from the ED that explicitly connects the BPTP investigation to homebuyer fund diversion allegations and multiple FIRs across Delhi-NCR police stations.

Indian securities regulations require that material pending litigation be disclosed in IPO prospectuses. The question is not whether these matters will appear in the prospectus at all — the legal requirement is clear. The questions are: how are they characterised, how are the financial provisions quantified, what worst-case scenarios are disclosed, and whether the overall presentation gives a retail investor a genuine understanding of the risk profile they are assuming. Experience with Indian real estate developer IPOs suggests that the answer to these questions is rarely as complete as the public interest requires.

Section VII: The Pattern of Launching New Projects While Old Ones Lie Unfinished

One of the most persistent and documented criticisms of BPTP from its own homebuyers is the juxtaposition between the company’s enthusiasm for new launches and its indifference to completing existing commitments.

In 2016, at a time when NDTV documented 15 BPTP projects with delays of more than three years and approximately 5,000 buyers in distress, BPTP was simultaneously marketing new phases and new projects in the same corridors. In 2021, when Spacio buyers were reporting a decade of waiting and demands for escalation charges, BPTP was expanding its project pipeline. In July 2025, when the ED had just conducted raids on BPTP’s offices and Gaia Residences buyers from earlier phases were still waiting, BPTP launched an entirely new 1,600-unit luxury complex on Dwarka Expressway with a ₹3,000 crore headline.

This pattern — new launches generating fresh revenue through advance collection while old projects languish — is precisely the mechanism that consumer forum regulators, RERA authorities, and the Supreme Court have repeatedly identified as the structural driver of real estate developer misconduct in India. A developer that collects advances on Project B while using those funds to partially finish Project A (or not finish it at all) is not simply a disorganised developer. It is a developer whose business model depends on an ever-expanding pool of new buyer money to service the obligations it has already incurred — a structure that is, at its logical end, a Ponzi-adjacent scheme.

The ED’s allegation of fund diversion — if sustained — would confirm what BPTP’s own project delivery record strongly implies: that money collected for specific projects was not ringfenced for and deployed toward those projects in the manner that buyers understood when they made their payments.

Under RERA, enacted in 2016, developers are required to deposit 70% of collected amounts in a dedicated escrow account that can only be withdrawn for construction of the specific project for which the money was collected. This requirement was specifically designed to prevent the kind of fund commingling and diversion that characterised pre-RERA developer misconduct. How rigorously BPTP has complied with RERA’s escrow requirements — across all its RERA-registered projects — is a question that SEBI’s IPO due diligence should be pressing urgently.

Section VIII: The Regulator’s Responsibility — What SEBI Must Do

SEBI’s mandate, as stated in its founding statute, includes the protection of investor interests and the promotion of the development of, and the regulation of, the securities market. These twin obligations — investor protection and market integrity — converge in the BPTP IPO with unusual force.

The case for enhanced SEBI scrutiny rests on several distinct grounds. First, there is an active investigation by a sister enforcement agency — the ED — into financial violations at BPTP under FEMA, with allegations of fund diversion and multiple FIRs at Delhi-NCR police stations. An IPO that proceeds while that investigation is active exposes retail investors to outcome risks that have not been definitively quantified and may not be fully disclosable under current norms.

Second, there is an extensive record of Supreme Court judgments, NCDRC orders, and HARERA decisions against BPTP — creating quantifiable legal liabilities that must be honestly provisioned in the IPO’s financial statements and risk disclosures. SEBI must verify that these liabilities are not being obscured through creative provisioning or downplayed through aggressive optimistic assumptions.

Third, the pattern of launching new projects while completing old ones is a structural business risk for the post-IPO company. Retail shareholders in a listed BPTP will be exposed to whatever liability emerges from the current portfolio of delayed projects, which includes projects with registered completion dates as far out as March 2029. Given BPTP’s historical delivery record, the probability that all of those projects are delivered on the RERA-registered timeline is not a question of optimism versus pessimism. It is a question of evidence — and the evidence does not support the optimistic scenario.

Fourth, the history of the prior BPTP IPO approval that lapsed in 2011 — without the underlying project delivery problems that have since accumulated — should serve as a caution that market timing and promotional momentum do not substitute for the kind of structural reform and liability resolution that a company with BPTP’s record requires before it is a suitable vehicle for retail investor capital.

Concretely, SEBI should require BPTP to provide a complete, project-by-project disclosure of all delayed projects, the current status of construction, the outstanding delivery obligations, and the timeline for completion with specific milestones. SEBI should require the prospectus to disclose the aggregate estimated liability from all pending legal cases — consumer forum, RERA, NCDRC, and Supreme Court — with realistic worst-case as well as central-case estimates. SEBI should require a complete disclosure of the ED FEMA investigation, including the specific nature of the allegations, the ₹500 crore FDI in question, and the potential outcomes of the investigation including PMLA implications.

SEBI should require that the IPO proceeds be allocated with clear ringfencing toward completion of existing delayed projects before any allocation to new project launches or promoter exit. And SEBI should consider whether, given the active ED investigation, the BPTP IPO should be held in abeyance until the investigation reaches a stage where its financial implications can be reliably disclosed.

Section IX: The Systemic Argument — Allowing This IPO Sets a Dangerous Precedent

There is an argument beyond BPTP’s specific case that this article asks SEBI to consider.

India’s real estate sector has, over the past decade, produced an extraordinary number of cases in which developers collected large advance sums from homebuyers, diverted those funds, failed to complete projects, and then — rather than facing consequences — used their remaining assets and brand value to continue attracting fresh capital while legacy buyers waited in courts and in rented accommodation. The RERA framework, enacted in 2016, was specifically designed to discipline this pattern at the project level. SEBI’s IPO scrutiny process is the corresponding discipline at the capital markets level.

If a developer with BPTP’s documented record — multiple Supreme Court orders for refunds, an active ED investigation, an industry-wide reputation for delay and escalation charges, and dozens of projects with buyers still waiting — can successfully execute an IPO and transfer its liabilities onto retail shareholders, then the message to every real estate developer in India is clear: build whatever record you like at the project level, because the capital markets will always provide an exit on the other end. Retail investors, who lack the institutional due diligence capacity of sophisticated PE or institutional investors, will bear the resulting losses.

SEBI’s role in preventing that outcome is not a peripheral regulatory nicety. It is the central function the institution exists to perform.

Section X: The Homebuyers’ Voice — What They Want the Retail Investor to Know

In the course of the research behind this article, across multiple published accounts in NDTV, the Times of India, Economic Times, ET Realty, and regulatory orders, a consistent message emerges from BPTP’s homebuyers to anyone considering investing in BPTP’s IPO.

They want retail investors to know that the glossy presentations — the Gaia Residences launch event, the ₹10,000 crore annual project pipeline, the land bank statistics — conceal a reality in which thousands of families across Delhi NCR are still waiting for homes they paid for between five and fifteen years ago. They want retail investors to know that the same management that sent them escalation charge letters after decade-long delays, that invoked COVID as the excuse for a delay that predated COVID by six years, and that allegedly structured its foreign investment with illegal guaranteed-return clauses, is now asking the public markets to trust it with more money.

They want retail investors to know that every rupee BPTP collects in an IPO is a rupee in the hands of a management whose primary documented skill is not building homes but managing — through legal loopholes, procedural delays, and financial engineering — the gap between what it promised and what it delivered.

And they want SEBI to know that the housing market’s credibility as a destination for middle-class savings in India depends on the capital markets refusing to become an exit mechanism for developers who have spent a decade and a half breaking the promises they made to the very market segment whose trust they are now asking SEBI to help them access again.

Conclusion: The Public Interest Case Is Overwhelming

BPTP is not a company that made isolated mistakes. It is a company whose documented record — across its own project portfolio, across its regulatory history, and now in the offices of the Enforcement Directorate — reflects a systemic pattern of collecting money, failing to deliver, and deploying every available legal and procedural tool to minimize the consequences of that failure.

The Supreme Court has ordered it to pay buyers with 18% interest, using BPTP’s own penalty rate as the benchmark for what accountability looks like. Haryana RERA has rejected its force majeure defences in terms that leave no doubt about what the regulator thinks of those arguments. The Enforcement Directorate has raided its offices, seized its documents, and alleged violations totalling ₹500 crore in FDI structured with illegal guarantees. Multiple FIRs for project delays and fund diversion sit in Delhi-NCR police stations. Thousands of buyers have spent years in courts and consumer forums — and thousands more are presumably still waiting for homes without the resources or awareness to pursue legal remedies at all.

This is the company that wants India’s retail investors to buy its shares.

SEBI’s answer must be informed by the complete record — not the prospectus that BPTP’s merchant bankers will craft to highlight the land bank and suppress the liabilities, but the full documented history that courts, regulators, enforcement agencies, and investigative journalists have assembled over fifteen years of watching BPTP operate.

Investor protection is not an abstract principle. It is the protection of the retired government employee in Faridabad who has ₹2 lakh in a DMAT account and who has no way of knowing, without SEBI’s intervention, that the “exciting real estate IPO” being marketed on television is the company that left his neighbour waiting twelve years for a plot of land and then demanded extra money when it finally appeared.

SEBI must act. The record demands it. The public interest requires it. And the homebuyers of Delhi NCR — who have already paid an enormous price for BPTP’s pattern of conduct — deserve to know that at least one regulator will draw the line before retail investors are handed the bill.