Kotak Mahinda Bank Cum Municipal Corporation Panchkula Fraud Case: When Private Government Partnership Fools The Citizens Of The Nation!

On the morning of March 25, 2026, officials of the Municipal Corporation (MC) Panchkula walked into the Sector 11 branch of Kotak Mahindra Bank to initiate a routine transfer from a maturing Fixed Deposit. What they discovered instead was a nightmare; one that would blow open a multi-crore financial conspiracy involving bank insiders, a rogue government official, shadowy financiers, and significantly, real estate firms that appear to have served as the final destination for public money that was never meant to leave the civic body’s coffers.

The Municipal Corporation had believed it was sitting on 16 Fixed Deposits amounting to ₹145.03 crore, with a maturity value of ₹158.02 crore, safely parked in Kotak Mahindra Bank. Every single one of those FD receipts, it turned out, was a forgery. The money had long been siphoned. The bank’s own officials had been complicit, not merely negligent. And as the Enforcement Directorate’s press release of April 23, 2026 now confirms, the siphoned funds were transferred not just to individual bank accounts, but to real estate firms and private persons — a detail that opens a far larger and more disturbing question about what kind of cartel was operating in the shadows of Panchkula’s financial system.

This is not a story about a single rogue employee or an isolated lapse of oversight. This is a story about the systemic failure of India’s private banking sector, the chronic corruption within municipal bodies, and the now-familiar builder-bank nexus that the country’s investigative agencies — including the CBI itself — have been circling for years. The Panchkula fraud is not the beginning of a new chapter. It is the most visible headline yet in a long, sordid story that has been written in the ink of taxpayer money.

How the Conspiracy Was Engineered: Inside the Kotak-MC Nexus

According to the ED’s PMLA investigation and the findings of Haryana’s State Vigilance and Anti-Corruption Bureau (SV&ACB), the criminal architecture of this fraud was built carefully, over years, by a closed nexus of three types of actors: a corrupt Municipal Corporation official, compliant bank insiders, and a web of private financiers.

The key individuals named are Dileep Kumar Raghav, who served as Customer Relationship Manager at Kotak Mahindra Bank’s Panchkula branch; Pushpinder Singh, the bank’s Deputy Vice President at the same branch; and Vikas Kaushik, the former Senior Accounts Officer of Municipal Corporation Panchkula. Together, this trio formed the operational heart of the conspiracy.

Their method was as brazen as it was sophisticated. Beginning in May 2020, Kaushik and Pushpinder Singh allegedly opened a fraudulent bank account (Account No. 2015073031) in the name of the Municipal Corporation using forged seals and signatures, including those of the then-Commissioner of MC Panchkula, IAS Sumedha Kataria, and the then-Senior Accounts Officer, Sushil Kumar. Neither of those officials had any knowledge of this account. In June 2022, they opened a second fraudulent account (Account No. 2046279112), this time forging the signature of the then Deputy Municipal Commissioner, Deepak Sura.

Having created fake institutional identities within Kotak Mahindra Bank’s own system — a process that should have been caught by the bank’s Know Your Customer (KYC) and account-opening protocols — the conspirators then forged debit notes and fund migration authorisation letters in the name of MC Panchkula. Critically, the bank officials processing these instructions used unauthorised email IDs to seek and grant authorisation, deliberately bypassing the official email communication channels that the Municipal Corporation had registered with the bank. This means that somewhere within Kotak Mahindra Bank’s internal systems, not one but multiple compliance checks were either circumvented or deliberately ignored.

The real MC Panchkula, meanwhile, received fabricated FD advice notes — forged documents showing it held 16 healthy Fixed Deposits worth ₹145 crore. The civic body’s records showed everything was in order. In reality, the money had already been drained.

Pushpinder Singh has since surrendered and been arrested, the sixth person taken into custody in the case. According to the SV&ACB, the conspirators then transferred these funds to private financiers including Rajat Dahra, Swati Tomar, Kapil Kumar, and Vinod Kumar. Rajat Dahra alone allegedly received ₹70 crore of the stolen public money. These funds were then routed back to Pushpinder Singh and his wife Preeti Thakur — and in the most damning thread of all — forwarded onward to real estate builders, who allegedly received the money as high-interest loans, enriching the network further.

The entire scheme sustained itself on a basic exploitation of institutional trust: the Municipal Corporation trusted the bank to hold its public money safely, and that trust was used as a weapon against it.

Kotak Mahindra Bank: A History That Should Have Sounded Alarm Bells

The outrage of the Panchkula fraud multiplies exponentially when one examines Kotak Mahindra Bank’s documented track record of internal compliance failures, fraud cases, and regulatory violations — a record that stretches back years and raises serious questions about whether this bank’s institutional culture has ever been seriously interrogated.

According to parliamentary data cited in multiple published reports, Kotak Mahindra Bank topped the list of private banks in India for reported fraud cases in recent years. This is not a distinction that any responsible financial institution should want, yet there has been no sustained public reckoning with what this figure represents in terms of systemic rot.

In Gurugram in 2024, three Kotak Mahindra Bank executives, two deputy managers and an assistant manager were arrested for opening more than 2,000 fake accounts, which were then used to aid cybercriminals in facilitating crores in nationwide scams. This was not a case of external hackers penetrating the bank’s systems. These were insiders, with institutional access, using their positions to build an industrial-scale fraud pipeline from within.

A similar pattern emerged in Hyderabad, where a bank sales manager colluded in a ₹2.06 crore trading fraud. In Mumbai, a relationship manager, the same designation as Dileep Kumar Raghav in the Panchkula case allegedly defrauded a 75-year-old American citizen of ₹2.7 crore by misusing blank documents and One Time Passwords (OTPs) that had been trusted to him. The Panchkula Relationship Manager Raghav allegedly did something structurally identical: he used his position of institutional trust to provide false verification of fake FDs to the Municipal Corporation when they came asking uncomfortable questions in July 2025 and February 2026.

The Reserve Bank of India has penalised Kotak Mahindra Bank on multiple occasions. In April 2024, the RBI took the extraordinary step of barring Kotak Mahindra Bank from onboarding new customers via mobile and online banking channels and from issuing new credit cards — a punishment it reserved after conducting two consecutive years of IT audits in 2022 and 2023, finding serious and unresolved deficiencies in the bank’s information technology systems. For a bank whose business model was heavily dependent on digital channels and new-age customer acquisition, this was a regulatory earthquake. Yet the bank managed to navigate it without any serious structural overhaul becoming publicly visible.

In December 2025, the RBI imposed a further penalty of ₹61.95 lakh on Kotak Mahindra Bank after an inspection of its March 2024 financial position revealed three specific lapses: the opening of multiple Basic Savings Bank Deposit (BSBD) accounts for individuals who already held such accounts in violation of the one-per-person rule; allowing its business correspondents in rural areas to perform tasks outside their regulated scope; and — most damaging of all — submitting false information regarding borrowers to Credit Information Companies (CICs).

Incorrect credit reporting directly harms citizens by distorting their credit scores, affecting their ability to access loans for years. In November 2023, the RBI had already imposed a ₹4 crore penalty on Kotak Mahindra Bank for regulatory violations. These are not isolated incidents. They form a pattern of a bank that operates at the edge of regulatory compliance, retreating only when the regulator’s foot comes down — and then resuming business as usual.

There are also the allegations, deeply uncomfortable in a democratic society, surrounding the bank’s electoral bond contributions. Reports published by investigative outlets indicate that Infina Finance, a group entity associated with Uday Kotak, donated ₹60 crore exclusively to the Bharatiya Janata Party via electoral bonds between 2019 and 2021. Critics and analysts have noted that this period coincided with favourable regulatory outcomes for the bank, including a 2020 arrangement that allowed Uday Kotak to retain a 26% stake in the bank despite earlier RBI pressure to reduce it to 10%.

While no direct quid pro quo has been established in a court of law, the opacity of the electoral bond mechanism, which the Supreme Court of India has since struck down as unconstitutional, means that such questions cannot be cleanly resolved. What is clear is that the largest private bank in India, with a documented record of insider frauds and regulatory violations, has operated in an environment where the political and regulatory pressure on it has remained conspicuously muted.

The Panchkula fraud must therefore be read not as an aberration, but as the natural fruit of a tree that has never been pruned with sufficient force.

Municipal Corporations: India’s Most Unaccountable Repositories of Public Money

If the bank side of this fraud represents a failure of private-sector compliance, the municipal corporation side represents something arguably more corrosive: the corruption of the institution that is most directly supposed to serve the ordinary citizen.

Municipal corporations across India manage enormous sums of public money — funds collected through property taxes, professional taxes, water charges, and central and state government grants. These are, in the most literal sense, the people’s money. The citizens of Panchkula paid their taxes expecting those funds to be used for roads, drainage systems, parks, garbage disposal, and public health. Instead, ₹145 crore of those funds sat in fabricated FD accounts while the real money was being loaned to builders at profit.

The Panchkula case is far from unique. Across India, municipal bodies have been implicated in fund embezzlement of varying scales and mechanisms. In many cases, the fraud follows the same structural blueprint: a corrupt insider with access to the institution’s financial accounts collaborates with either a private bank official or an external financier to siphon funds, using forged documents to maintain the appearance of legitimacy in the municipal corporation’s own records.

The pattern of municipal fund fraud in India has been documented at alarming scale. Investigators and auditors across state governments have repeatedly flagged the ease with which municipal financial systems can be exploited when internal audits are weak, when fund reconciliation happens only on paper rather than through direct bank verification, and when the relationship between a specific bank branch and a specific civic official becomes too personal and too comfortable.

The Panchkula case illustrates precisely this dynamic: Dileep Raghav and Pushpinder Singh were not strangers who approached a random civic official. The conspiracy was built on a sustained relationship between bank officials and an insider within the municipal corporation’s accounts department — a relationship that appears to have operated for years without triggering any institutional alarm.

The Comptroller and Auditor General (CAG) of India has, in multiple reports spanning the 2018–2024 period, flagged serious deficiencies in the financial management of municipal bodies across states including Haryana, Uttar Pradesh, Maharashtra, and Rajasthan. These include failure to reconcile bank balances, reliance on self-certification of funds by single officials without secondary verification, and the absence of third-party audits of investment instruments like FDs. The Panchkula fraud exploited exactly these structural gaps — the Municipal Corporation had no independent mechanism to verify that its FDs actually existed in the bank’s system. It simply trusted the forged documents provided by Raghav.

The question that must be asked loudly is this: why does India’s municipal governance system still permit individual officials to manage hundreds of crores of public money in FDs without mandatory, real-time digital reconciliation with the bank? The Reserve Bank of India has digital infrastructure capable of making such verification instantaneous. The failure to mandate it represents a policy choice that, in cities and towns across India, has created conditions in which the Panchkula fraud can be replicated with minimal effort.

The Real Estate Connection: Who Are the Builders in This Story?

Perhaps the most consequential, and least discussed, element of the ED’s press release is a single, carefully worded sentence: “Such illegal funds were also transferred to real estate firms and private persons.”

The Enforcement Directorate’s search operations on April 22, 2026 covered not just the bank officials and their personal financiers, but also the premises of a real estate firm called Sanat Realtors and an individual named Sunny Garg. The inclusion of a real estate entity in the ED’s search list is not incidental. It is the investigative thread that connects the Panchkula fraud to a much larger and more systemic pathology in India’s economy: the builder-bank nexus.

SV&ACB’s investigation has already disclosed that the funds ultimately transferred to builders were framed as loans meant to earn “more profit” for the conspirators. Rajat Dahra, who allegedly received ₹70 crore of stolen MC Panchkula funds, appears to have been a conduit — a financier who sat between the bank officials and the real estate entities that were the final recipients. The money moved through a layered network of individual accounts, personal relationships, and private entities — a classic structuring technique designed to break the paper trail and make forensic tracing difficult.

This raises the central interrogative question that “Is the CBI’s recent probe into the builder-bank nexus in subvention schemes pointing at the same cartel that the ED has now identified in the Panchkula case?“

The CBI, the Supreme Court, and the Builder-Bank Cartel

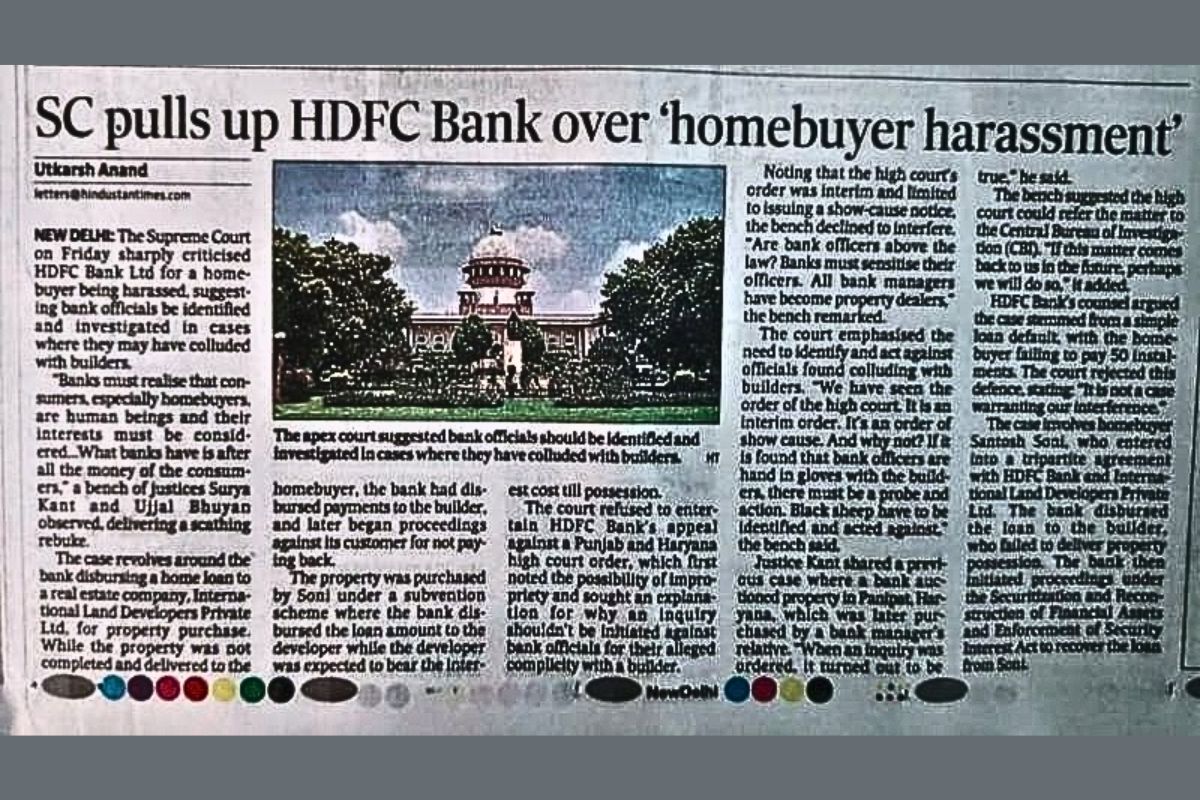

In a different but structurally parallel investigation, the Supreme Court of India has directly confronted the builder-bank nexus in the context of EMI subvention schemes — a financial product that, on paper, was designed to protect homebuyers but was systematically weaponised against them by an axis of builders and banks operating in bad faith.

Under EMI subvention schemes, builders advertised to homebuyers that they would pay the EMI or pre-EMI interest on the buyer’s home loan until possession was handed over. Banks eagerly participated, disbursing 70–80% of sanctioned loan amounts often without verifying whether construction milestones had actually been achieved — a direct violation of the 2013 RBI guidelines on housing loans.

When the builders defaulted on their EMI obligations in 2018 and 2019, the banks turned to the homebuyers and demanded payments on loans for apartments that had never been completed, or in some cases, never even been commenced. The Supreme Court, in its hearing of this matter, described what it heard in scathing terms, expressing alarm at how banks had disbursed enormous sums without conducting basic due diligence on construction progress.

The CBI has been investigating specific instances of this builder-bank collusion, with cases like the Ozone Metrozone fraud in Chennai, where the developer, using subvention scheme loans, effectively converted individual homebuyers into unknowing financiers of a stalled real estate project. The loans were taken in buyers’ names. The money went to the developer. The developer failed to honour its EMI obligations. And the banks pursued the buyers for recovery, even though the buyers were victims. In effect, a tripartite conspiracy between builders, banks, and their own institutional incentives had transformed the life savings of middle-class homebuyers into an unsecured, zero-recovery loan to a real estate developer.

The structural question that the Panchkula fraud now sharpens to a point is this: when the ED says that illegally transferred municipal funds went to “real estate firms,” is it describing a similar dynamic? Were the builders who received these funds; whether through Rajat Dahra or through the network of private persons named in the investigation, part of the same network of real estate entities that have routinely used politically-connected financial intermediaries to access cheap, unaccountable capital? Are these the builders whose projects have been sold to ordinary homebuyers on the strength of loans from banks whose officials were simultaneously siphoning public money into those very same real estate ventures?

The answer, at this stage, is that investigators do not yet know — or have not yet said. But the architecture of the fraud, as described by both the ED and the SV&ACB, bears strong resemblance to the builder-bank-financier triangles that the CBI and the Supreme Court have already identified in the housing loan subvention cases. Rajat Dahra is not named as a homebuyer or a common citizen.

He is named as a private financier who received ₹70 crore of stolen public money. Sanat Realtors is not a random search target — it is a real estate entity whose premises the ED chose to raid in the context of a civic body’s stolen funds. Sunny Garg is not a municipal official. He is a private individual whose properties were searched in connection with money that began its journey in the public coffers of a Haryana city.

The question of whether this builder-bank nexus — the cartel of bank insiders, real estate developers, and financial intermediaries — is the same one that the CBI has been tracking in the subvention scheme cases is not merely academic. If it is the same cartel, or even an overlapping one, then the Panchkula fraud is not just a local financial crime. It is a node in a national network of actors who have found a way to systematically convert both public money and private savings into private real estate capital, using banks as the mechanism of transfer and forged documents as the instrument of concealment.

The Citizen Pays: Who Bears the Cost?

The moral weight of this story ultimately rests on a simple, devastating truth: every rupee that Pushpinder Singh, Vikas Kaushik, Dileep Kumar Raghav, Rajat Dahra, and their associates extracted from the Municipal Corporation Panchkula’s accounts was a rupee that belonged to the people of Panchkula. It was tax money. It was the savings of salaried workers, shopkeepers, small businesspeople, and residents who pay their municipal taxes with the expectation — the entirely reasonable expectation — that this money will be spent on their city.

Roads not repaired. Drainage systems not maintained. Parks not built. Healthcare centres not funded. Every one of these failures is not just a governance shortfall — it is the direct downstream consequence of a ₹145 crore theft from the civic body that was meant to deliver these services.

The homebuyers in the subvention scheme cases have already paid with years of their lives — paying EMIs on properties they cannot live in, fighting in RERA tribunals and consumer courts, watching their life savings drain into legal fees while builders and banks continue operations with minimal disruption. The taxpayers of Panchkula are now in a comparable position: they will bear the cost of a theft they had no way of detecting, engineered by people in whom they had placed institutional trust.

This is the fundamental violence of white-collar crime in India’s banking and municipal systems. It does not come at you with a weapon. It comes wearing a tie and carrying forged documents, operating from behind a bank counter and a municipal office desk, protected by institutional opacity and regulatory delay. By the time the Enforcement Directorate’s search teams arrive at the premises of a real estate firm called Sanat Realtors in Panchkula, the money has already been layered, laundered, and potentially invested in assets whose appreciation will further reward those who stole it.

What Must Change: The Accountability Deficit

The Panchkula fraud, the Kotak Mahindra Bank regulatory violations, the Supreme Court’s indictment of the builder-bank EMI nexus, and the CBI’s ongoing investigations into real estate subvention schemes are not separate stories. They are chapters of the same story: the story of how India’s financial institutions and civic bodies have been systematically hollowed out by a class of insiders who exploit the gap between the letter of regulation and the reality of enforcement.

The path forward requires mandatory real-time digital reconciliation between municipal corporation accounts and bank systems — no civic body of Panchkula’s scale should be able to hold over ₹100 crore in FDs without a verifiable, independently accessible digital trail. It requires multiple-signatory, multi-channel verification for all fund migration instructions above a threshold — no single official, whether inside the bank or the civic body, should have the unilateral power to move hundreds of crores without independent real-time confirmation.

It requires the whistleblower protection mechanisms within banks to be genuinely functional — if any employee within Kotak Mahindra Bank’s Panchkula branch was aware of the fraudulent accounts, their silence was purchased or compelled, and the system provides them no safe path to come forward.

Above all, it requires that the investigation now underway does not stop at the individuals already arrested. The ED’s probe into Sanat Realtors, Sunny Garg, and the flow of funds into real estate firms must be pursued to its conclusion — publicly, transparently, and without the kind of regulatory deference that has, for too long, allowed India’s largest private bank to accumulate fraud headlines without facing the full force of accountability.

The people of Panchkula paid their taxes. They are owed an answer. The people of India, whose homebuying savings have been weaponised by the builder-bank cartel in city after city, are owed an answer. The Supreme Court has demanded one. The CBI is searching for one. The ED has begun to knock on the right doors.

The question is whether those doors will finally be opened all the way — or whether the same nexus of political connection, institutional opacity, and regulatory lethargy that allowed this fraud to run for six years will once again muffle the sound of justice.