You must have heard a lot about how you should invest your wealth for your financial security and how investment is an asset. Isn’t it? Hearing people say all this around you might tempt you into investing a part of your money that fetches significant returns over time. But, are you aware of the different kinds of investment tools available in the market? Do you have proper knowledge about what are the prevailing interest rates on different investments? Can you name the type of investment that fetches guaranteed returns if locked in for a certain amount of time?

Whether or not you were able to answer the questions above, here is an investment guide that’ll help you make an informed decision before you decide to invest your money.

Financially speaking, investments are made for various purposes. The different objectives can be meeting shortages in your income, saving up for your retirement or daughter’s marriage or even for the purchase of other assets to name a few. Investments are made with a view of earning returns. Apart from that, putting your money into an investment scheme makes sure that you set apart a sum at regular intervals. This practice helps you instil a sense of financial discipline in the long run.

What are the different areas of investment?

- Bonds

- Mutual funds

- Fixed deposits

- Provident funds

- Stocks and equities

Let’s take a look at which of these investment areas is the safest and guarantees you significant returns. Without a doubt, FD investment tops the list. Fixed deposits are the most popular investment tool in India. Because of the financial safety, guaranteed returns and flexible tenures, investing has been synonymous with FDs big time!

What exactly is a fixed deposit?

An FD is an investment instrument provided by banks and Non-banking Financial Companies (NBFCs) to their customers. A certain sum of money is locked in for a fixed period at a pre-determined rate of interest. Although this rate of interest is higher than that offered on a savings account, it differs from one financial institution to another. Ranging from tenures as short as 7-14 days, FDs can be locked in for a maximum of 10 years at a stretch.

Working mechanism of fixed deposits

You might think of making an FD as lending money to a bank or an NBFC. What happens is when you invest in an FD, the financial institution guarantees to return you the invested sum, along with the interest amount earned for the tenure. This period is also known as the maturity period. While your money is locked in, the banks might use it to lend their borrowers, for which interest is charged from them. A portion of this interest is passed on to you according to the interest rates at which you invested your money in the FD. The interest rate depends upon the tenure for which you’ve invested your money with the bank.

After a fixed deposit matures, you have two options at your disposal. You can either withdraw the entire amount (along with the interest earned) or reinvest the interest amount. If you choose to reinvest, there are two ways to go about it:

Cumulative FDs

- Interest and principal amount paid at maturity

- Interest reinvested every year

- You don’t receive regular interest payouts

- A lump sum amount received at the end of FD tenure

This option will be suitable for you if you’re not looking for a regular stream of income. Here, you’ll benefit from the power of compounding because next year’s interest is calculated on the principal plus interest of the previous year.

Non-cumulative FDs

- Interest paid at fixed intervals

- Monthly, quarterly, half-yearly or annual interest paid as per your convenience

- Gives you a regular stream of income

While this sounds like a better investment option, the downside to it is that you lose out on earning the interest amount.

How do you invest in an FD?

With the advent of technology, opening a fixed deposit account no longer requires going to the bank. Online FDs can be opened within minutes and with just a few clicks! Follow these 3 simple steps for opening an online FD with your preferred financial institution.

- Step 1: Fill in your FD details (including tenure, amount and interest payout method)

- Step 2: Set up your investment account by answering a few very easy questions that follow

- Step 3: Make the payment on your FD

And, you’re done! What can be easier and more time-saving than this simple process?

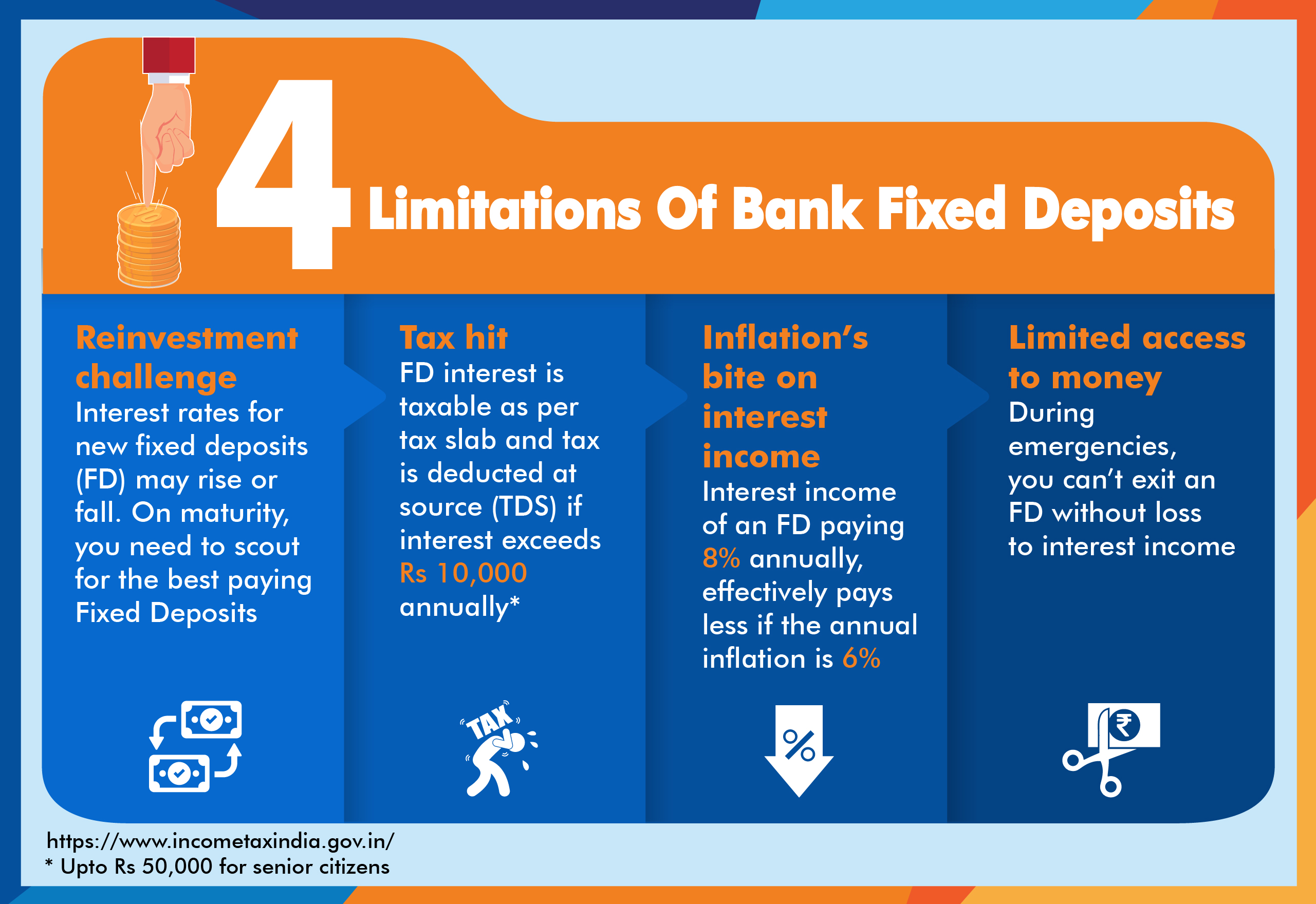

Taxation on fixed deposits

Just like you have to pay taxes on your incomes from various sources, the interest you receive on your FDs is also taxable. The Government charges this tax at your applicable tax slab under the head “Income from Other Sources”. Banks deduct TDS (Tax Deducted at Source) at 10% per annum from your interest. TDS on the interest income is eligible for deduction only if the total interest amounts to Rs. 40,000 per annum. For senior citizens, this limit is Rs. 50,000.

The significant role of FDs in your portfolio

Market-linked instruments such as mutual funds and equities carry an associated risk factor. Fixed deposits do not. Investing in FDs is safe and provides you with an assured return once the maturity period is over.

A positive net value of your portfolio

Market fluctuation is an inevitable phenomenon. During market lows, fixed deposit returns ensure that the net value of your portfolio still remains positive. This happens because the interest that you earn from FDs can compensate for any losses incurred out of other market-linked investments.

Short-term goal appropriate

Investing in fixed deposits is a wise investment choice for meeting goals where you can’t afford to lose the capital investment you made.

Benefits of an FD investment

- Your capital remains safe

- Premature withdrawal facility available

- Higher returns in comparison to a savings account

- A higher rate of interest permissible for senior citizens

- You can earn interest on interest (benefit of compounding)

- You can easily open an online FD account from the comfort of your home

Various online investment platforms provide you with the knowledge you need before putting your money in any investment scheme. Conduct thorough research before you opt for investing in a fixed deposit account. Whether you’re a high-risk investor or have a low-risk appetite, fixed deposit investment is the safest way of earning more returns.