Russia-Ukraine war to lower growth, increase inflationary pressures globally: KPMG

Russia-Ukraine war to lower growth, increase inflationary pressures globally: KPMG

According to a new global economic perspective from global consulting firm KPMG, an extended state of emergency in Ukraine will reduce global monetary opportunities and trigger inflationary tensions around the world.

Monthly reports include monetary forecasts and studies by an association team of market analysts in various fields and regions around the world.![]()

The study warns that progress on global issues such as public welfare and environmental change is stalling as political and monetary pioneers adjust to the general outcome of the dispute in Ukraine.

The global economy has improved with expanded sovereign debt as a result of the COVID-19 downturn, and as central banks increased borrowing costs, so have sovereign debt collection costs, making it particularly challenging for emerging markets with US money. He concluded that professionals and many organizations, still dumbfounded by the effects of the epidemic, were poorly prepared to deal with another major financial disruption.

He said the global monetary picture for the next two years had not been fully clarified by the outcome of the Russia-Ukraine conflict. A review by our chief economist reveals that different regions and locations were at different rates of monetary recovery post-COVID-19 before the conflict in Ukraine, a review by our chief economist reveals. While GDP figures suggest otherwise, the world faces clear and recurring themes and threats. Armed conflict may be confined to Eastern Europe today, but it is currently having a tremendous impact on all countries.

global economy

As KPMG points out, world development forecasts for the next two years are not entirely determined by the outcome of the Russo-Ukrainian war. He created three situations to examine the outlook for the world economy.

Figures for the next two years remain unclear due to the outcome of the Russo-Ukrainian war. Looking at the current vulnerability, KPMG’s Global Economic Outlook formulates three situations to assess global economic performance:

- Significant circumstances predict that global oil prices will be $30 higher than before the state of emergency escalated, with gas costs in Europe halving. It also means a 5% increase in the cost of food worldwide.

- A more extreme situation examines the possible impact of a $40 increase in global oil costs, as well as a 100% increase in gas costs for Europe and a 50% increase for the rest of the world. The 10% increase in the cost of food worldwide will also be remembered for the direst results imaginable.

- A 23% increase in the cost of normal metals and a 4% increase in the cost of rural information resources were recalled for both situations. In Europe, this also means higher subsidies and higher government spending.

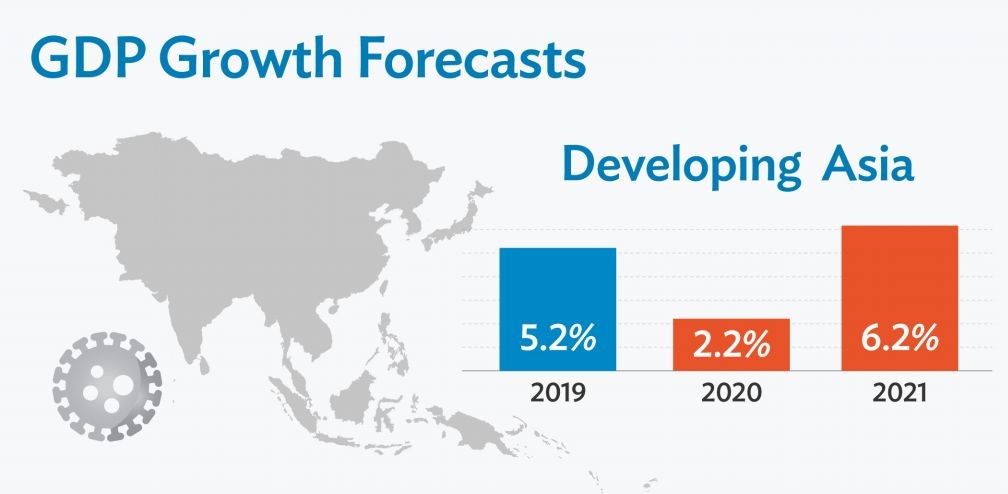

According to the report’s study, global GDP growth could range from 3.3% to 4% this year and 2.5% to 3.2% in 2023, depending on the scenario. The current risk to KPMG’s forecasts is on the downside. It is possible that a confrontation between Russia and Ukraine will develop beyond the report’s worst-case scenario, in which, for example, an energy supply disruption causes serious industrial disruption in parts of Europe.

The report’s bullish scenario examines what will happen if the war ends earlier than expected, prices return to early February levels, and production and trade flows are restored.

It is possible that a confrontation between Russia and Ukraine will develop beyond the report’s worst-case scenario, in which, for example, an energy supply disruption causes serious industrial disruption in parts of Europe. A new wave of the COVID-19 pandemic is still disrupting supply chains in major economies like China, and a new wave could undo recent improvements.

ASEAN Growth Prospects

Inflation in ASEAN is rising, partly due to monetary easing during the epidemic. However, compared to other regions of the world, price dynamics are still very moderate; consumer price inflation in Indonesia, Malaysia, Thailand, and Vietnam currently hovers between 2% and 3%. Domestic demand typically recovers more slowly during a pandemic, leading to a longer recovery in domestic demand and lower local inflationary pressures. Singapore, on the other hand, where government aid is higher, is an exception, with inflation currently at 4%, the highest level since 2013.

The region will be affected by the recent increase in food and gas prices. Russia and Ukraine supply large quantities of wheat imports (mainly to Indonesia and the Philippines). In addition, potash fertilizers in the agriculture of the region are heavily dependent on Russia and Belarus.

The increase in government revenues has partially offset the negative impact of higher fuel costs in commodity-producing countries such as Indonesia and Malaysia. Shortages of key raw materials such as neon and semi-finished iron and steel products needed for the production of chips (neon), vehicles, machinery, and electronics are expected to disrupt supply chains due to the Russo-Ukrainian (steel) war.

As several countries, such as Indonesia and Singapore, are showing signs of economic recovery, the focus has shifted to fiscal consolidation with the announcement of tax hikes. This, coupled with an easy run of wins from reopening, will dampen economic momentum in the second half of 2022 and 2023, returning growth rates to long-term trends in many countries.

The Indian economy

According to the study, variables such as increased mobility, increased consumer confidence, and the spread of high-performing industries indicate India’s economic recovery. In addition, according to CMIE statistics, increased government investment plans as well as investments in infrastructure and the industrial sector are likely to reduce unemployment, which hit a six-month high of 8.1 percent in February of 2022.

While the Indian economy is expected to maintain its strong growth trajectory, recent geopolitical developments have hurt local equity indices and led to volatility in crude oil and currency prices, the study said.

According to the study, the Indian economy is expected to continue its strong growth trajectory, although recent geopolitical developments have damaged local stock indices and led to volatility in crude oil prices and exchange rates.

Given India’s dependence on crude oil, natural gas, and other imported commodities, rising inflation and widening current account deficits need to be closely monitored, especially given the country’s changing geopolitical environment. Moreover, the fourth wave of COVID-19 infections and the changing virus pose a major risk to India’s future economic growth.

Inflation on a high exacerbates central banks’ dilemma.

The global economy has emerged from the COVID-19 recession with sovereign debt rising, and as central banks have raised interest rates, so have the costs of servicing sovereign debt, making it difficult for emerging markets whose debt is denominated in the US currency that they value. Politicians and many businesses are still suffering from the effects of the epidemic, making them less prepared for another major economic shock.

economic consequences

The escalation of the war between Russia and Ukraine as a result of the massive invasion of Russia in late February will result in higher prices and also add to supply chain concerns. Despite the deteriorating relations between the West and Russia since Russia’s invasion of Crimea in 2014, recent sanctions and uncertainty over supplies of some important commodities will be felt most strongly in Europe, where Russia still enjoys some of the best trading relations.

If the situation worsens, the market may experience greater volatility as investors seek safe havens and some trades are delayed. As military activity continues, geopolitical and economic instability are expected to remain high.

Despite rising inflationary pressures, both the European Central Bank and, to a lesser extent, the US Federal Reserve could adopt a more cohesive monetary policy with slightly smoother interest rates this year. The Bank of England, on the other hand, could maintain its plan for two further rate hikes in the summer.

The supply system is up for grabs.

Prior to the invasion, bottlenecks in the supply chains of the UK, US, and China began to ease while they were still growing in the euro zone. Some of those gains are likely to be reversed due to recent events.

Base metals such as nickel, aluminum, and palladium are produced in large quantities in Russia and Ukraine. Delays in purchasing can have a negative impact on industrial production and the entire supply chain. Further problems are expected to arise from the scarcity of components imported from the region, especially in sectors such as automotives.

Due to the lack of a cable system from Ukraine, several German car manufacturers have suspended production. The region’s significant share of global fertilizer production has the potential to impact agricultural production and disrupt global food supply chains.

Inflation will remain higher for longer.

Russia’s main exports, oil and gas, experienced significant price increases. Gas prices have more than doubled since the conflict began, and oil prices have risen by more than $125 a barrel. Energy costs are expected to rise in the near term if gas prices remain unchanged, adding to the strain on consumer incomes.

After a planned 54% increase next month, the cap on gas prices for UK households could rise by around 50% in October, with some of the gains underpinned by a £200 cut in the bailout provided by the Treasury.

The cost of nickel has risen, as have the prices of fertilizers and staple foods such as wheat and vegetable oil, with food prices expected to be affected overall. Russia and Ukraine account for 25–30% of world wheat exports and the bulk of sunflower seed exports. Wheat prices, up more than 50% since early March, could add more than a percentage point to UK inflation. Gradual increases in commodity and energy prices will lead to higher inflation rates.

Due to the need to reduce dependence on Russian energy, energy prices are expected to remain high for a long time. All European economies are expected to be affected, which could lead to faster inflation in the coming years.

Weak economic growth

Lithuania, whose exports to Russia account for 6% of its GDP, is perhaps the most vulnerable to trade tensions as a result of the crisis. According to IfW, trade restrictions with Russia could reduce Lithuania’s GDP by 2.5% in the long term, while the economies of Latvia and Estonia could shrink by 2% in the long term.

According to an analysis by the Kiel Institute, the larger European economies in Germany, Italy, and France are significantly less dependent on Russia, with exports to Russia accounting for between 1 and 2 percent of total exports and the long-term impact of trade restrictions on them. The decline in the economy ranged from 0.4% to 0.16% of GDP, with Poland registering a slightly larger decline of 0.78%.

In addition to the trade disruption challenges, higher inflation will weigh on demand negatively. In our estimation, a 10% increase in oil prices combined with a 50% increase in gas prices could result in a 0.5% decline in GDP in some of Europe’s largest economies. According to market statistics from early March, this simulation captures about half of the impact of rising energy costs on GDP growth.

Rising prices and the side effects of trade tensions will have an impact on economies outside Europe. According to the IMF, a 10% increase in oil prices, purely due to supply, would reduce global GDP by 0.1% to 0.2%. If this trend continues, a shift in income from oil-consuming countries to less spending-friendly oil-producing countries can be expected.

This could affect investment in oil-importing countries due to reduced profitability. As trade with Russia shifts from the West to other destinations, some countries may enjoy a short-term export boost.

Risks of further escalation

The potential decrease in gas availability, in addition to the increase in gas prices, is an option that can increase the impact of the crisis on several European economies. Given that Russia supplies 30–40% of the region’s gas, the region is very vulnerable to gas supply disruptions. While not our main scenario, eurozone GDP could fall by around 2% if it loses access to Russian gas.

It will also have a significant indirect impact on economies such as the UK, which imports only 5% of its gas from Russia due to falling export demand and further disruptions in supply chains.

KPMG’s Global Economic Outlook:

The Global Economic Outlook is a biennial economic forecast prepared by the macroeconomic team at KPMG’s global network using a variety of external and internal models that capture key relationships in the global economy. As with all predictions, there is a lot of room for error, and results can vary widely.

About KPMG International

KPMG is a global network of independent professional services organizations specializing in assurance, tax, and consulting services. KPMG is the brand under which KPMG International Limited (“KPMG International”) and its member companies operate and provide professional services. An individual KPMG member company and one or more member companies are collectively referred to as “KPMG”.

With more than 236,000 partners and employees working in member companies worldwide, KPMG operates in 145 countries and territories. Each KPMG company is a legally separate and distinct entity that identifies itself as such. Each KPMG member company is responsible for its commitments and commitments.

KPMG International Limited is a limited liability company based in the UK. Customer service is not provided by KPMG International Limited or its affiliates.

edited and proofread by nikita sharma