The latest World Economic Report from the IMF raises red flags for India

The main takeaway from the World Economic Outlook released by the International Monetary Fund is that “the worst is yet to come.” India has valid concerns.

The International Monetary Fund (IMF) sends two World Economic Outlooks (WEO) and two updates every year, in April and October and January and July, respectively, with the main message to decision-makers throughout the world that “the worst is yet to come” for the global economy. Although it is not a portmanteau of the dreaded word “stagflation,” it describes a state of economic stagnation (or contraction) despite high inflation.

In a separate statement, the IMF states that the three largest economies—the United States, the European Union, and China—will continue to stall, while “more than a third of the global economy will contract this year or next.” The most immediate threat to current and future prosperity is increasing price pressures, which squeeze incomes and threaten macroeconomic stability.

The hardest policy task at hand may be dealing with persistently high inflation and stagnant GDP. This is because policies intended to control inflation frequently lead growth to decline more, whilst those intended to promote growth frequently cause inflation to rise. Perhaps, for this reason, Pierre-Olivier Gourinchas, the Economic Counsellor, begins his introduction to the most recent WEO by saying, “As storm clouds gather, policymakers need to retain a firm hand.”

Prospects for growth

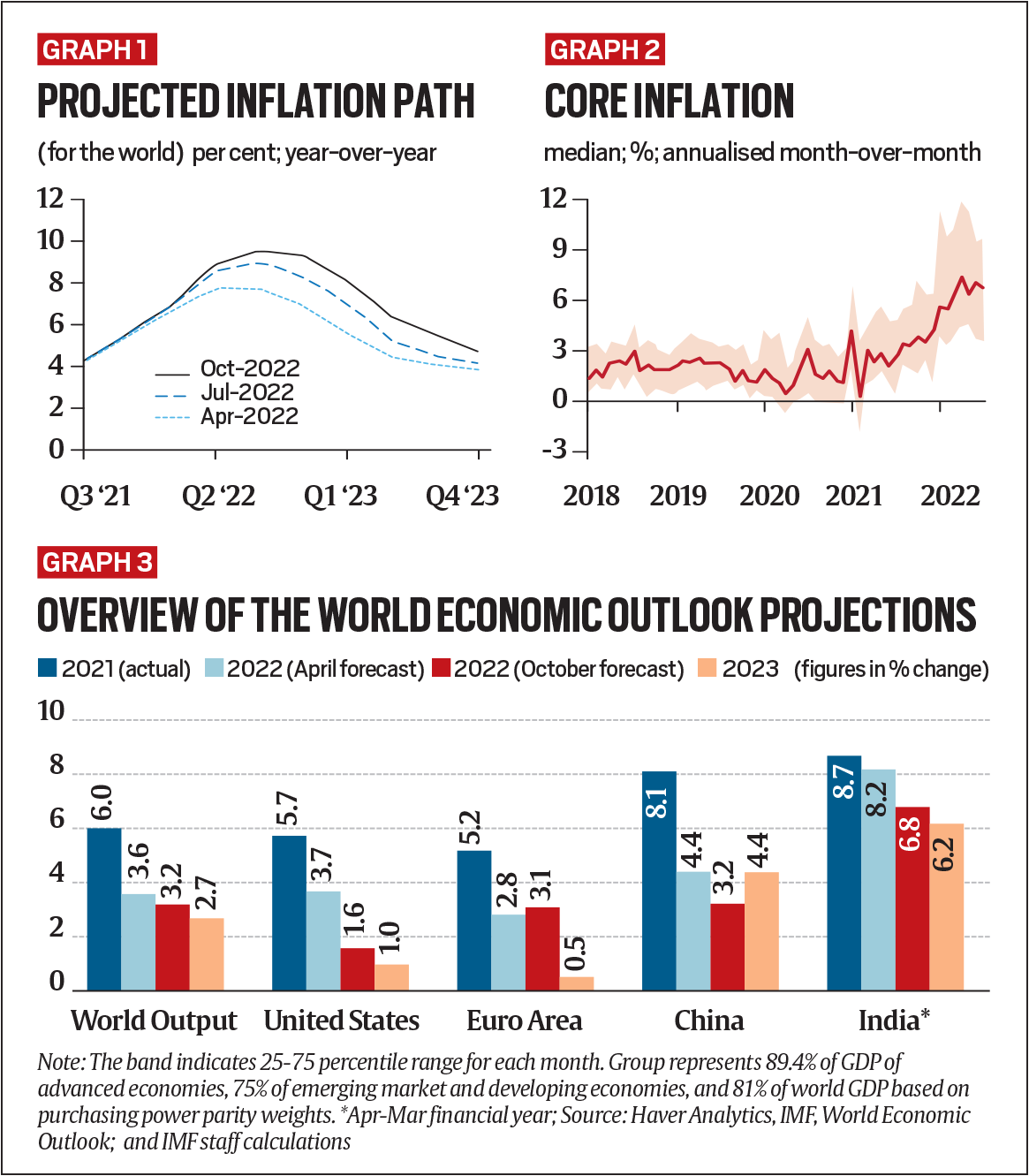

The IMF has drastically reduced its prediction for global growth, going from 6.0% in 2021 to 3.2% in 2022 and 2.7% in 2023. This is the poorest growth profile for the globe since 2001, except for the 2008 global financial crisis and the steep decline that followed the Covid epidemic in 2020.

In his official blog, Gourinchas addresses both the source and the effect of the global economic downturn, including the invasion of Ukraine by Russia, the cost-of-living issue brought on by enduring and expanding inflation pressures, and the slowdown in China. “In general, the shocks of this year will reopen economic scars that were only partially healed after the epidemic. In other words, the worst is yet to come and 2023 will seem like a recession to many people.

On inflation

Now, it’s anticipated that global inflation would reach its high in late 2022, reaching 9.5%. It is predicted to stay high for longer than first thought and will probably only fall to 4.1% by 2024.

Here, the trend of core inflation—that is, the inflation rate after excluding the cost of gasoline and food—is of special concern. Inflation in the core usually increases and decreases more gradually than inflation in food and fuel. According to the IMF, “global core inflation, measured by removing food and energy prices, is estimated to be 6.6% on a fourth-quarter-over-fourth-quarter basis, reflecting the pass-through of energy prices, supply chain cost pressure, and tight labour markets, mainly in advanced economies.” In other words, rising food and fuel prices, which have historically caused a surge in overall inflation, have now filtered down to core inflation and will thus take longer to subside.

Unfavourable projection hazards

The IMF has also listed several downside risks or potential reasons why things may turn out to be worse than expected.

Miscalibration of the policy is the first risk. This is the largest concern since most economies are in a dangerous state and there is a great deal of uncertainty about the future.

For instance, monetary and fiscal policy shouldn’t conflict. An excellent example is what recently occurred in the UK when the Liz Truss administration implemented an expansionary fiscal policy (tax cuts and unfunded increases in expenditures) despite the Bank of England’s efforts to limit historically high inflation by increasing interest rates. Investors lost faith in the decision-makers as a result, and British assets were sold off, causing a mini-financial catastrophe (gilts and pound-sterling).

Even when monetary and fiscal policies are in harmony, errors can still occur. For instance, monetary authorities may overtighten their stance (raising interest rates above what is necessary) or may act in an opposing manner. Overtightening runs the danger of slowing GDP while tightening too little runs the risk of core inflation leaking through and becoming harder to control.

Financial stability and its interactions with an upbeat US dollar are major sources of concern. Sharp interest rate revisions will probably reveal the weakest links in the global credit system, whether they are the pension funds in the UK or other overleveraged nations and businesses. Finally, the conflict in Ukraine has geopolitical concerns. All of the aforementioned stresses might get greater if the dispute intensifies or lasts longer.

Impact for India

India seems to be in a stronger position at first look. India’s GDP growth rate is higher, and the country’s inflation rate is lower. These metrics, however, conceal the fact that, in absolute terms, India is just emerging from the recession it experienced in 2020, that it was home to the greatest number of people (5.6 crores, according to the World Bank) who were pushed below the poverty line in 2020, or that millions are unemployed.

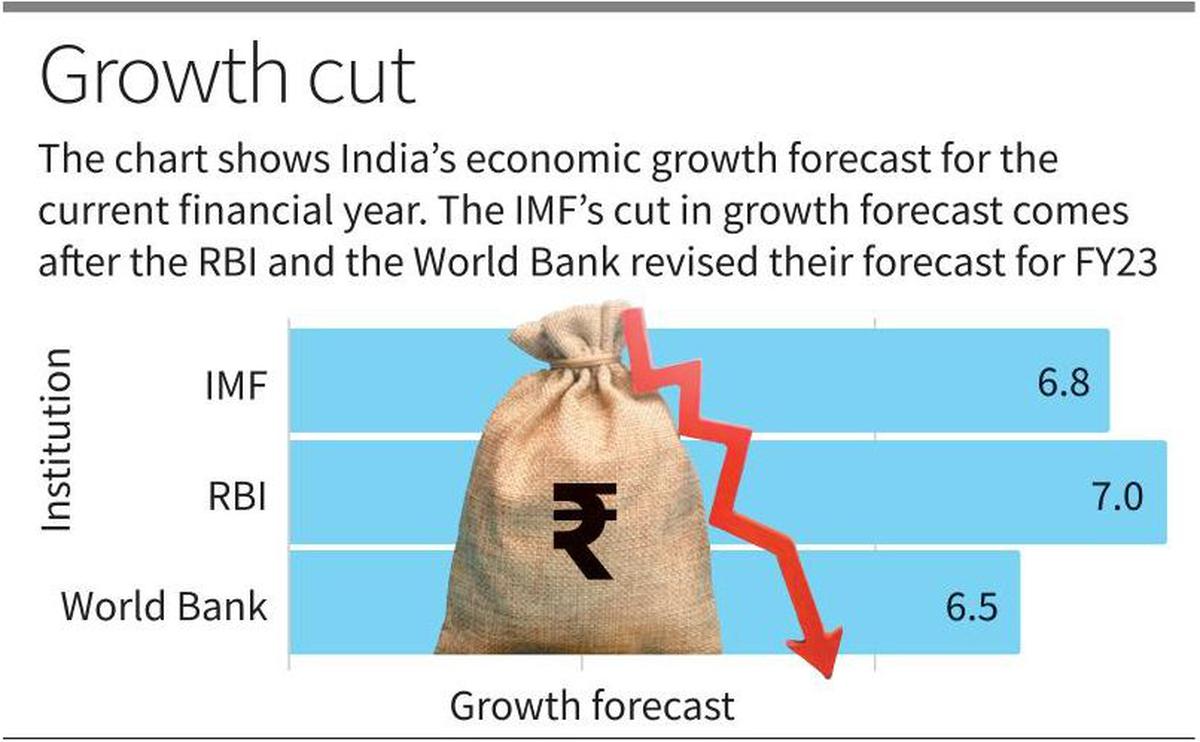

Additionally, if RBI decreases its April growth rate prediction of 7.2% by the same amount as the IMF (1.4% points), India’s growth in 2022–2023 will be 5.8%.

A strong dollar will put pressure on the exchange rate of the rupee, which will likely lead to a decrease in our foreign exchange reserves and a reduction in our ability to import goods when times are tough. Higher prices for crude oil and fertilizer will also increase domestic inflation. A global slowdown will harm exports, slowing domestic growth and widening the trade deficit. Additionally, because there is no demand from the majority of Indians, the government may be obliged to spend more money on subsidizing food and fertilizer to provide basic assistance. The government’s financial situation would worsen as a result.