The global FinTech boom that began in 2021 has now entered a new phase. After a period of rapid expansion and experimentation, the market is gradually moving toward maturity, with several functional segments evolving into distinct industries of their own. Among these, digital lending has emerged as one of the most dynamic and technology-driven verticals.

Unlike traditional lending models, digital lending platforms rely heavily on advanced technologies to scale operations, manage risk, and improve customer experience. In particular, AI and ML are playing a central role in reshaping how credit decisions are made, how risks are assessed, and how financial inclusion is expanded across global markets.

To illustrate how these cutting-edge technologies are transforming the digital lending ecosystem in practice, we invited Dr. Avinash Barnwal, a technological industry leader, to contribute his perspective. He drives impactful change through next-generation machine learning solutions at a leading US-based company in fintech and digital lending. Drawing on real-world lending cases, he shares insights grounded in practical experience and helps to bridge the gap between emerging technology trends and their tangible impact on today’s global digital lending landscape.

Capital Constraints and the Shift Toward Digital Lending

Small businesses and entrepreneurs face persistent funding constraints, which is visible across global markets. For example, in India, Venture Intelligence reports that startups raised only USD 3.8 billion in private equity and venture capital between January and June, compared with USD 18.4 billion in the same period the previous year.

Difficulties in accessing external financing have also contributed to an overall decline in demand for capital. While many investors have paused or reduced their activity, banks have begun tightening lending conditions after a prolonged period of monetary easing driven by COVID-19 stimulus measures. As a result, many small businesses are no longer applying for traditional funding sources such as bank credit. In the United Kingdom, for instance, only 33 percent of small businesses used external finance in Q3 2022, down from 44 percent in Q3 2021.

The Federal Reserve has acknowledged this challenge, noting that small businesses often face greater barriers to credit access because lending to them is perceived as higher risk and more costly than lending to larger firms. This creates a financing gap that conventional banks struggle to address efficiently.

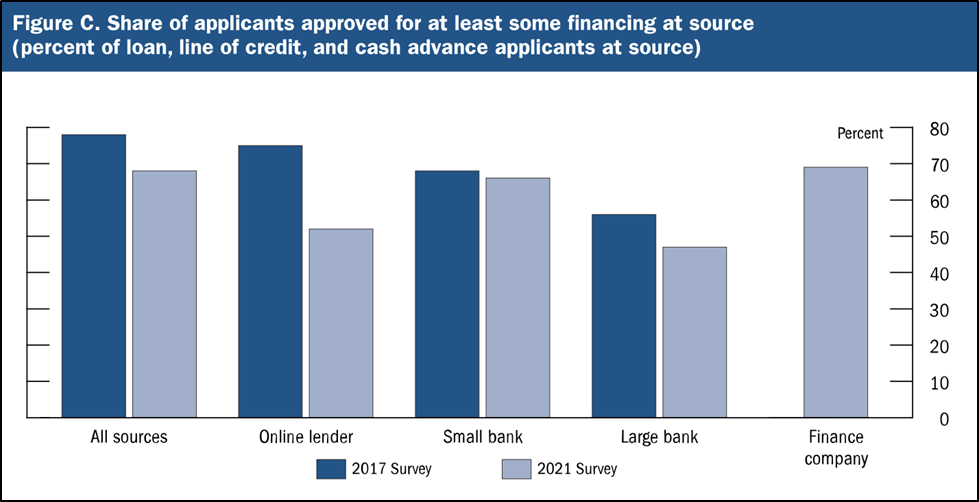

Fintech lenders have begun to fill this gap. According to the Federal Reserve’s 2021 Small Business Credit Survey, fintech firms recorded the highest share of applicants approved for at least some financing and significantly outperformed both large banks and traditional online lenders.

Source: The Federal Reserve

‘It’s evident to me and all my colleagues that small businesses with strong financing needs are moving away from traditional lenders toward digital lending platforms. That is already reshaping the market. The global digital lending sector reached about 12.6 billion dollars in 2022 and is on track to cross 13 billion dollars by the end of 2023. This trend is being driven by wider adoption of AI and ML, continuous fintech innovation, and the demand for faster, data-driven credit decisions. Together, these forces are setting up the industry for rapid growth, which can reach 19 percent annually through 2032,’ notes Dr. Barnwal, Data Science Manager at Kapitus.

AI & ML to the Rescue The Credit Problem

Traditional credit scoring systems were built for a different era. They rely heavily on static rules, limited data sources, and manual processes, making credit decisions slow, rigid, and often difficult to interpret. For fintech startups operating in fast-moving markets, these constraints translate into higher default risk, lower approval efficiency, and reduced ability to serve thin-file or underserved customers. As lending volumes scale, the shortcomings of legacy models become even more visible.

AI and ML are now reshaping this foundation. By processing large and diverse datasets in real time, these technologies enable more precise credit risk assessment and more adaptive decision-making. Advanced models can capture complex behavioral patterns, support personalized loan offerings, and continuously improve through feedback loops. Eventually, they become among key industry drivers, accelerating market growth, as stated by MarketReportsWorld.

To be more precise, ML models bring several practical advantages over traditional scorecards by capturing complex patterns in data and enhancing decision quality:

- Better discrimination between good and bad loans. ML models like gradient-boosted trees (for example, XGBoost) can identify non-linear relationships and interactions among features that traditional logistic regression scorecards often miss. In practice, this leads to higher predictive power—better separating high-risk from low-risk borrowers. For example, when monotonic constraints are applied, tree-based models maintain interpretability while outperforming traditional models in discriminatory ability.

- Enhanced feature interpretation with explainability tools. Although ML models are often viewed as ‘black boxes,’ explainable AI tools like SHAP values and LIME make it possible to interpret individual predictions. These tools reveal how features such as credit utilization, payment behavior, or business financial ratios influence risk scores, improving transparency for model monitoring and business understanding.

‘SHAP summary plots helped me illustrate that increased days past due and declining cash flows were dominant risk drivers. These insights would not surface as clearly in traditional scorecards’, adds Dr. Avinash Barnwal.

- Flexible integration of diverse data sources. ML models can ingest a wider range of inputs—numeric bureau data, alternative data signals, and derived features—simultaneously, enabling richer risk profiles. This flexibility supports more robust predictive scoring for thin-file customers, a frequent challenge in small business lending.

- Adaptive risk policies and rejection insights. When deployed with well–defined adverse action codes, ML-based rejection decisions help lenders understand and communicate why an application was declined. This ensures compliance while still leveraging complex models. For example, instead of a simple rule like ‘credit score < threshold,’ an ML approach may show that high leverage combined with low revenue growth was a decisive factor, improving both decision quality and customer feedback.

- Continuous improvement and model monitoring. ML models support automated retraining and recalibration as new data arrives, enabling lenders to respond quickly to changes in macroeconomic conditions or borrower behavior. Rather than static scorecards, this dynamic approach maintains relevance and reduces model degradation over time.

Building the Engine Behind Digital Lending Success

Developing an effective risk engine does not require enterprise-scale resources, but it does demand disciplined design, governance, and a strong ML team that is typically brought up with an enthusiastic ML leader like Dr. Avinash Barnwal. Once this is set, startups should begin with feature engineering, focusing on variables that reflect real financial behavior rather than relying solely on legacy bureau scores. Transactional patterns, repayment history, and business performance indicators can be transformed into features that capture risk more accurately and adapt to changing borrower profiles.

As models grow more complex, bias and fairness considerations must be addressed early. Credit decisions directly affect access to capital, making transparency and explainability essential. Applying monotonic constraints, validating feature influence, and regularly testing for disparate impact across borrower segments help ensure that predictive power does not come at the expense of fairness or regulatory compliance.

Once deployed, post-launch monitoring becomes critical. Model performance should be tracked continuously using stability metrics, default trends, and population drift indicators. Automated retraining pipelines allow startups to respond to shifts in borrower behavior or macroeconomic conditions without rebuilding systems from scratch. This lifecycle approach—build, validate, monitor, and recalibrate—keeps risk engines both accurate and resilient.

Market signals already point to the strategic value of ML-based credit scoring. In 2023, the release of VantageScore 4 Plus demonstrated how combining open banking data with traditional bureau records can improve predictive accuracy by approximately 10 percent over earlier versions. Similar innovations are emerging across the fintech landscape, where leading digital lenders are investing heavily in proprietary risk systems. Leading fintechs set the trend by elevating small business lending decisions with ML, showing how advanced scoring models can become a core driver of digital lending success.