ED Attaches Nearly 20000 Crore In Reliance Group. Will The Supreme Court Still Allow Anil Ambani To Pay For The Justice And Walk Out Free, Just Like Sandesaras Saga?

Liability Minus Repayment Equals Leniency: Has India's Supreme Court Accidentally Written a Billionaire's Escape Manual?

The Opening Strike — April 28, 2026

On the morning of April 28, 2026, the Enforcement Directorate issued its sixth Provisional Attachment Order in the Reliance Communications bank fraud case, freezing assets valued at ₹3,034.90 crore. The order brought the total value of properties attached across all Reliance Anil Ambani Group cases to ₹19,344 crore — a number large enough to fund a mid-sized country’s annual health budget, and yet still less than half of what the group allegedly owes to India’s public financial institutions.

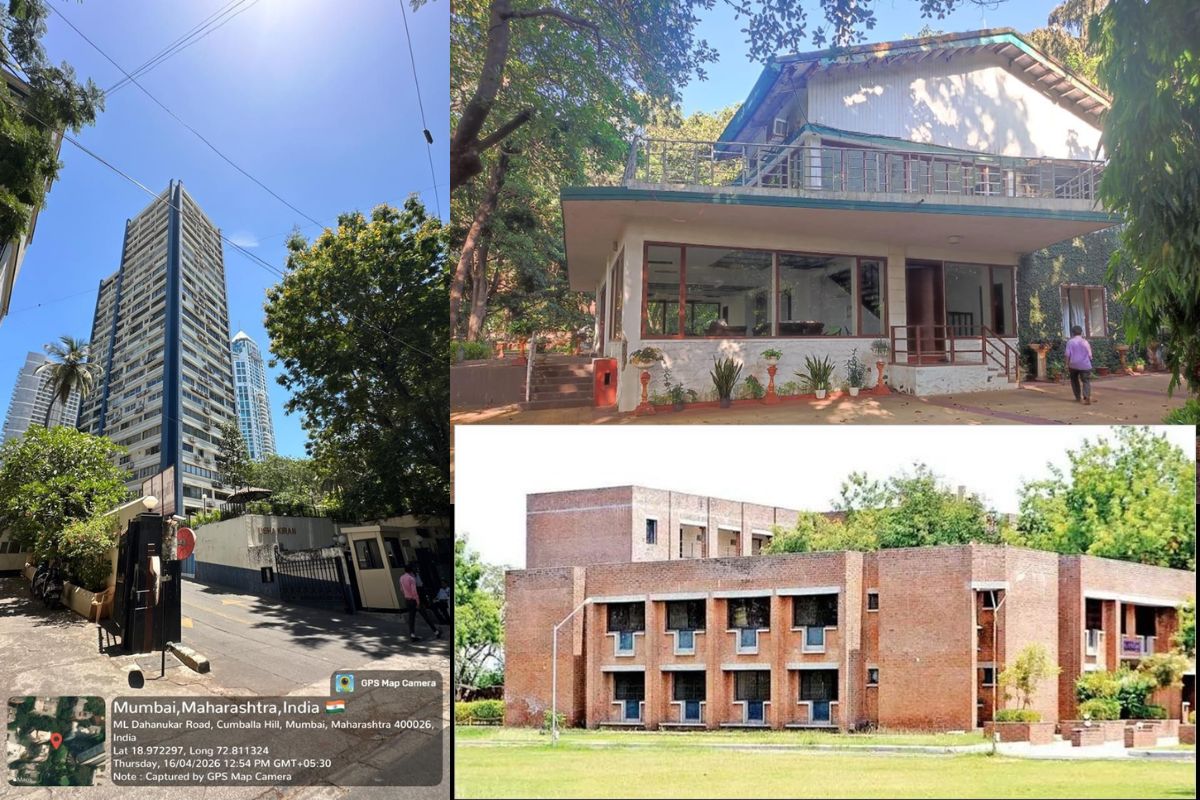

What makes this sixth attachment order particularly striking is not the headline figure but the granular detail of what was seized. The list includes a flat in the Usha Kiran Building on M.L. Dhanukar Road in Cumballa Hill, South Mumbai — one of the city’s most exclusive residential addresses — registered directly in the name of Anil D. Ambani. It includes a farmhouse in Khandala, the hill retreat near Pune, held in the name of the Luna Trust.

It includes land parcels in Sanand, Ahmedabad, registered under the Mudra Foundation for Communications Research and Education, better known as MICA. And critically, it includes 7.71 crore shares of Reliance Infrastructure Ltd. held by RiseE Infinity Pvt Ltd, a promoter group entity operating under the RiseE Trust umbrella.

The RiseE Trust, according to the ED’s own statement, was not an ordinary philanthropic or estate-planning vehicle. The agency alleges it was a private family trust set up specifically to consolidate wealth and insulate it from the personal guarantees Anil Ambani had extended to lender banks against loans sanctioned to RCOM. The properties aggregated under this trust, the ED contends, were “intended to be beneficially used and owned by the Anil Ambani family and not for the distressed public banks whose loans turned NPA.”

That a private family trust allegedly designed to shield assets from bank creditors now finds itself at the centre of the country’s largest ongoing PMLA investigation is, by itself, a significant institutional statement. But it is what happens next — legally, judicially, and politically — that will define whether the ₹19,344 crore number means justice, or merely paperwork.

The Architecture of the Alleged Fraud — How ₹40,185 Crore Disappeared

To understand the scale of what the Enforcement Directorate is investigating, one must first understand the structure of what is alleged to have gone wrong. Reliance Communications and its group companies borrowed from a consortium of lenders that reads like a roll call of India’s public financial system: the State Bank of India, Punjab National Bank, Bank of Baroda, and the Life Insurance Corporation of India. The CBI filed its FIRs on the formal complaints of all four. The total outstanding dues, the money borrowed and not repaid, stand at ₹40,185 crore.

The inclusion of LIC is not incidental. LIC is India’s largest institutional investor and insurer, holding the savings and premiums of hundreds of millions of ordinary policyholders. When LIC files a complaint in a bank fraud case, it is not merely a financial institution seeking recovery of its dues — it is, in a very real sense, representing the financial interests of a significant cross-section of the Indian working population. This is not rhetorical. It is a material fact that shapes the moral weight of the case.

The mechanism of alleged fraud, as pieced together from multiple ED statements, CBI filings, and court records, involved the use of loans sanctioned to RCOM for purposes other than those declared at the time of disbursement. Funds are alleged to have been routed through inter-company transactions across the RAAG cluster — which includes not just RCOM but also Reliance Infrastructure, Reliance Capital, and associated entities — creating a web of intra-group exposures that effectively moved money away from the balance sheets of the borrowing entities without creating traceable returns.

The use of trust structures like RiseE appears, according to the ED, to have been the final layer of insulation: once funds were moved out of the reach of operating companies, they were parked in privately held vehicles whose beneficial ownership remained within the Ambani family but whose legal structure created distance from the lender’s claim.

It is important to be precise here. These are allegations under investigation. No final court conviction has been recorded in the RAAG cases. But the investigation is not being run by a single agency acting on its own initiative. It is being conducted by a Special Investigation Team constituted on the explicit directions of the Supreme Court of India — a fact with profound implications for what comes next, and a fact that distinguishes the RAAG investigation from virtually any other economic offence case in the country’s recent history.

The SIT’s mandate is to examine diversion and laundering of bank and public funds across the RAAG cluster. That mandate has already produced five previous provisional attachment orders before the sixth of April 28, 2026. What the cumulative picture shows is not a single transaction gone wrong but a sustained, allegedly systematic pattern of asset movement away from the entities that bore the legal liability for the borrowed money, and into structures that would be harder for lenders to access through normal insolvency or recovery proceedings.

What the Numbers Actually Tell Us — The Attachment-to-Liability Gap

Numbers in financial crime cases have a way of appearing decisive when they are, in practice, only the beginning of a much longer story. The ₹19,344 crore figure that now headlines every report on the RAAG cases is real, it is significant, and it represents the outcome of years of painstaking investigative work. But it is essential that readers understand exactly what that number means — and, crucially, what it does not mean.

An attachment under Section 5(1) of the Prevention of Money Laundering Act (PMLA) is a provisional freeze. It prevents the owner of an asset from transferring, selling, or otherwise disposing of it. It does not transfer ownership to the government or to the victim banks. For that to happen, the case must proceed through the adjudicating authority under PMLA, the Appellate Tribunal, and potentially the High Court and Supreme Court — a process that, in complex multi-entity cases, routinely takes five to ten years. Only after a final confiscation order under Section 8 of PMLA can the attached property actually be liquidated and the proceeds restored to the victim institutions.

So the honest arithmetic of the RAAG case, as of April 28, 2026, looks like this: ₹40,185 crore was allegedly borrowed from public institutions and not repaid. ₹19,344 crore of assets have been provisionally frozen — approximately 48% of the total outstanding. The actual amount recovered and returned to victim banks is a fraction of even the attached figure, given where the legal process currently stands. The gap between what was borrowed and what has been recovered is not merely a number — it is a measure of the distance between the institutional achievement of the ED’s investigative work and the actual restoration of public money to the institutions and individuals it belongs to.

This gap matters because it creates the conditions in which a settlement conversation becomes not just possible but, from certain angles, attractive. If the legal road to full confiscation and recovery is a decade long, and if the outcome at the end of that road is uncertain, then a negotiated settlement that delivers a guaranteed partial recovery within a defined timeframe begins to look rational to banks, courts, and perhaps even governments. This is not a hypothetical observation. It is, almost exactly, the logic that the Supreme Court articulated in November 2025 in a case that every white-collar defence attorney in India has since studied with considerable interest.

Enter the Sandesara Precedent — The Supreme Court’s November 2025 Ruling

The Sandesara-Sterling Biotech case begins in the pharmaceutical sector and ends in an Albanian passport office, which is in itself a summary of how dramatically India’s economic offence landscape changed in the years following the 2008 financial crisis. Nitin and Chetan Sandesara were the founders of Sterling Biotech, a Gujarat-based pharmaceutical and biotechnology company.

They are accused of defrauding a consortium of Indian banks of over ₹5,383 crore through loan defaults, fraudulent documentation, and diversion of funds. In 2017, as CBI investigations intensified, the brothers left India. They subsequently acquired Albanian citizenship, a manoeuvre that placed them outside the reach of Indian extradition law and made them, for practical purposes, immune to domestic criminal prosecution. They were formally declared Fugitive Economic Offenders — one of only a handful of individuals to carry that designation under the Fugitive Economic Offenders Act, 2018.

What happened next was, in the language of the court itself, driven by “peculiar facts.” On November 19, 2025, a bench of the Supreme Court comprising Justice J.K. Maheshwari and Justice Vijay Bishnoi allowed the closure of all criminal and civil proceedings against the Sandesara brothers — including cases registered by the CBI, the Enforcement Directorate, the Serious Fraud Investigation Office, and the Income Tax authorities — on a single condition: that they deposit ₹5,100 crore with the consortium of lender banks by December 17, 2025.

The court recorded its reasoning with clarity: “It is apparent that since inception, this court was of the view that if the petitioners are ready to deposit the amount as settled in OTS and public money comes back to lender banks, the continuation of this litigation would serve no useful purpose.” The primary objective, the bench held, was recovery of public funds — and with that recovery in prospect, continued prosecution was not the superior public interest.

The court was acutely aware of the precedential weight of what it was doing. It added a sentence that has since been cited in almost every commentary on the ruling: “These directions as issued are in peculiar facts of this case, therefore, they shall not be treated as precedent.” That disclaimer is legally meaningful. Under the Indian system of judicial precedent, a ruling explicitly declared non-precedential cannot be cited as binding authority in subsequent cases. A future bench is not obliged to follow it, and a lower court cannot rely on it as the governing ratio.

But here is the practical limitation of that disclaimer, and it is the limitation that matters most for the RAAG case. A “not a precedent” declaration does not erase a ruling from the legal memory of practitioners. It does not prevent future accused or their counsel from bringing the ruling to the attention of a bench as a persuasive example of reasoning that the Supreme Court itself has found acceptable.

It does not prevent a future court — particularly the Supreme Court itself, which is not bound by its own previous decisions in the way lower courts are — from finding that the “peculiar facts” of a new case are sufficiently similar to justify analogous logic. The disclaimer closes the door of binding precedent. It does not lock it.

The Math of Impunity — What the Sandesara Deal Actually Looks Like on Paper

Legal commentary benefits from arithmetic, and the Sandesara settlement repays close numerical examination. The principal amount alleged to have been defrauded was ₹5,383 crore. The brothers left India in 2017. By November 2025, approximately eight years had elapsed — and with standard banking interest rates applied to the outstanding principal over that period, independent analysts and financial commentators estimated that the true economic cost of the fraud, including interest foregone by the lender banks, had grown well beyond ₹15,000 crore and by some estimates exceeded ₹21,000 crore.

Against that figure, the settlement picture looks considerably less robust than the headline ₹5,100 crore might suggest. The brothers had, in the course of earlier legal proceedings, already deposited approximately ₹3,507 crore with the court. Adding that to the fresh settlement amount of ₹5,100 crore produces a total payment of approximately ₹8,607 crore. On the most conservative estimate of total liability — the ₹15,000 crore figure — that represents a recovery rate of roughly 57%. On the higher interest-adjusted estimates above ₹21,000 crore, the recovery rate falls below 41%.

More troubling, from the perspective of critics who have publicly raised this issue, is the question of the overseas assets. The Sandesara family’s Nigerian oil company, Sterling Oil Exploration and Energy Production, reportedly contributes approximately 2.5% of Nigeria’s federal oil revenue. Estimates of the value of seized overseas assets linked to the Sandesara group ran to approximately ₹14,500 crore. If, as part of the overall settlement, those assets are eventually released back to the Sandesara family rather than liquidated for lender recovery, the arithmetic shifts dramatically in the brothers’ favour.

They would have paid approximately ₹8,607 crore to recover assets worth multiples of that figure — a settlement that, on balance, generates a net financial gain for the individuals accused of the fraud. This is not a claim. It is the arithmetic that legal commentators and financial analysts have raised in the public domain, and it deserves to be part of any serious discussion of what the settlement actually achieved.

The ₹19,344 Crore Question — Could Anil Ambani Try the Same Route?

This is the question that has, since November 2025, been circulating in every serious conversation about the RAAG case among lawyers, bankers, and financial journalists. It deserves to be addressed directly, analytically, and with the full complexity it requires — neither dismissed as alarmist nor accepted as inevitable.

The structural parallels between the Sandesara case and the RAAG case are real but imperfect. Both involve alleged diversion of funds from public sector lenders. Both involve complex multi-entity group structures that make asset tracing difficult. Both involve the use of trust and offshore vehicles to insulate family wealth from lender recourse. And in both cases, the amounts involved are large enough that prolonged litigation offers diminishing returns in terms of actual recovery, even if conviction were eventually secured.

But the differences are equally significant. The most obvious is scale: ₹40,185 crore in outstanding RAAG dues compared to ₹5,383 crore in the Sandesara case is not merely a quantitative difference — it represents a qualitatively different order of public harm, and would demand a proportionately larger settlement figure to achieve even the same recovery rate. A settlement at the Sandesara rate of approximately one-third of principal would require something in the range of ₹13,000 to ₹15,000 crore — a figure that, while theoretically possible for a group of this historical size, is not obviously available given the current state of the RAAG entities’ balance sheets after years of insolvency proceedings.

The second critical structural difference is the institutional architecture of the investigation itself. The Sandesara case was, for most of its life, a matter being pursued by agencies independently. The RAAG investigation, by contrast, is being conducted by an SIT constituted on the Supreme Court’s own directions. This means the court is not a detached forum to which a settlement proposal might be brought after the fact — it is, in a meaningful sense, the directing authority of the very investigation now underway. That institutional investment creates a presumption of seriousness that would be difficult to reconcile with a quiet settlement, particularly one that followed the Sandesara template so closely as to make the “not a precedent” disclaimer look nominal.

On the other side of the ledger, the very feature that makes a RAAG settlement harder — the SC’s direct oversight — is also the feature that makes it theoretically possible in a way it might not be in cases before lower forums. The Sandesara settlement was also a Supreme Court order.

If the court is already institutionally present in the RAAG case, it has the authority to craft a resolution, should it choose to. The legal argument that “recovery of public funds is the primary objective” applies with equal if not greater force to a ₹40,185 crore case than to a ₹5,383 crore one. Prolonged criminal trials serve no obviously superior public purpose if the practical result of a decade of litigation is a lower recovery than a structured settlement would deliver today.

This is the uncomfortable tension the Sandesara ruling has injected into the RAAG case — not as a binding precedent, but as a proof of concept. It has shown that the Supreme Court, faced with a complex fugitive economic offender case where the alternative to settlement is a long and uncertain trial, is willing to prioritise measured financial recovery over the symbolic demands of criminal accountability. Whether that calculus changes at the RAAG scale remains to be seen.

The Systemic Problem — When the Price of Fraud Is Just the Principal

Individual cases are instructive. What they reveal about the system that produces them is more important. Taken together, the Sandesara settlement and the RAAG investigation illuminate a structural flaw in India’s approach to large-scale financial crime — a flaw that neither the ED’s diligence nor the SC’s oversight, however commendable in themselves, can fully correct within the current legal framework.

India’s laws governing economic offences — the PMLA, the Fugitive Economic Offenders Act, the IBC, the CBI’s mandate under the Prevention of Corruption Act — were each designed for specific problems and specific contexts. They were not designed as a coherent, interlocking system capable of dealing with the full lifecycle of a modern large-scale financial fraud: the initial diversion, the layering through group companies, the parking in trust structures, the flight of accused persons, the use of foreign citizenship and extradition gaps, and ultimately the negotiated resolution decades after the original harm was caused.

In the environment that actually exists — where accused persons can and do leave the country before charges are framed, where assets are routinely layered through multiple domestic and international structures before investigators catch up with them, where trials in complex multi-accused economic offence cases routinely stretch beyond ten years — the effective deterrence provided by the criminal justice system is severely degraded. What the Sandesara case has made explicit is the logical endpoint of this degradation: if the cost of committing a large enough fraud is, ultimately, a negotiated payment of a fraction of the principal, then the fraud itself carries a calculable expected return that, for a sufficiently rational and risk-tolerant actor, may exceed the expected cost.

This is what economists call moral hazard — the alteration of behaviour in response to reduced consequences — and it operates at both the individual and systemic levels. At the individual level, the Sandesara outcome rationally signals to future potential fraudsters that the effective penalty floor is not zero, but that it is also not the full cost of the harm caused. At the systemic level, it signals to banks that large loan exposures to powerful business groups carry a recovery risk that the legal system may ultimately compound rather than resolve.

Debopriyo Moulik, a Supreme Court advocate, has noted that practices of settling financial crime cases through monetary penalties exist in other jurisdictions. But those systems typically maintain the distinction between civil recovery and criminal accountability — allowing settlements on the financial side while preserving the possibility of criminal conviction. India’s Sandesara order collapsed that distinction.

What Needs to Change — Policy and Legal Reforms

Identifying a problem without examining available remedies is analysis without purpose. Several concrete reform pathways have been discussed in parliamentary committees, legal commentary, and academic writing, and they deserve direct engagement here.

The most fundamental reform would be the introduction of mandatory minimum criminal sentences for economic offences above a defined threshold — say, ₹500 crore of established loss to public institutions — structured in a manner that removes the court’s discretion to quash criminal proceedings entirely on the basis of a monetary settlement. This would not prevent courts from encouraging partial recovery through civil or restitutive mechanisms. It would prevent a settlement from functioning as a complete substitute for criminal accountability. Several jurisdictions, including the United States through its federal sentencing guidelines for financial fraud, have implemented versions of this principle with measurable deterrent effect.

A second necessary reform concerns the Fugitive Economic Offenders Act of 2018, which was designed precisely for cases like the Sandesara matter. As currently drafted and interpreted, the Act allows for the attachment and forfeiture of assets belonging to declared fugitive economic offenders — but it does not explicitly prevent a court from releasing those assets in exchange for a monetary settlement that falls short of the full value of both the fraud and the forfeited assets.

Amending the Act to require that any settlement in a FEO case include the full liquidation of all attached assets — rather than allowing those assets to be returned to the accused upon payment of a negotiated sum — would close the loophole that critics of the Sandesara deal have most pointedly identified.

At the banking sector level, the distinction between a one-time settlement (OTS) at the bank-borrower level and criminal exoneration needs to be legislatively clarified. Banks have always had the regulatory authority to accept reduced recoveries on NPAs through OTS mechanisms — this is a legitimate banking practice. But OTS was designed as a tool for credit resolution, not as a pathway to criminal immunity. The Reserve Bank of India and the Finance Ministry should jointly clarify, through appropriate regulatory and legislative instruments, that an OTS accepted by a consortium of lenders does not, by itself, provide grounds for a court to extinguish parallel criminal proceedings initiated by investigative agencies on the public interest mandate.

Finally, the practical capacity of India’s international treaty network for asset tracing and mutual legal assistance needs urgent development. The Sandesara case demonstrated clearly that having an accused declared a Fugitive Economic Offender is legally meaningful but practically limited if their assets are in jurisdictions with which India’s MLAT framework is weak or untested. Investing in the legal and diplomatic infrastructure needed to trace, freeze, and repatriate overseas assets would substantially improve the leverage position of Indian agencies in any settlement negotiation — and would reduce the extent to which the accused’s departure from India functions, in practice, as an improvement to their negotiating position.

Conclusion — The Real Test of Justice

The Enforcement Directorate has, across six provisional attachment orders and years of painstaking investigation, built a record of institutional capability that deserves acknowledgment without qualification. ₹19,344 crore in frozen assets in the RAAG cases is a significant investigative achievement. The SIT structure, constituted on the Supreme Court’s own directions, signals that the highest court in the country considers this matter serious enough to warrant its direct supervisory attention. These are not trivial institutional facts.

But institutional achievements are measured not by what agencies freeze, but by what courts ultimately confiscate, what banks ultimately recover, and what signal the final outcome sends to every future actor contemplating a similar course of conduct. The real test of India’s financial justice system in the RAAG case will not come on the day an attachment order is issued. It will come on the day — years from now, in a courtroom that may look very different from the present one — when a judge must decide whether ₹40,185 crore of alleged public harm can be resolved by a cheque, however large.

The Sandesara ruling, whatever the specific and undeniably complex circumstances that produced it, has inserted a question mark into that future moment. It has demonstrated that the Supreme Court is capable of choosing financial recovery over criminal accountability when the two are framed as mutually exclusive alternatives. That choice may have been correct on the peculiar facts of November 2025. It was, however, also predictable — and predictability, in the context of financial crime, is the beginning of a playbook.

The court said its Sandesara directions shall not be treated as precedent. The question India’s legal and financial system now lives with is this: when the next well-resourced accused arrives before a bench with a settlement offer and a citation to a ruling the court itself has said cannot be cited, will the disclaimer hold? Or will the formula — liability minus repayment equals leniency — have quietly become the operating logic of Indian financial justice, one peculiar case at a time?

That is a question the court, the legislature, and the public will all answer together. And the ₹19,344 crore sitting frozen in attachment orders today is the down payment on getting that answer right.