Decoding the RBI’s surprise rate hike in 2022, a liquidity-sapping attempt to combat inflation, and its ramifications

The Reserve Bank of India (RBI) shocked the markets and economists alike on May 4, 2022.

In a spontaneous 15-minute speech on monetary policy, RBI Governor Shaktikanta Das said that the repo rate would go up by 40 basis points, and the cash reserve ratio (CRR) would go up by 50 basis points. This was the first rate increase since August 2018, and it meant that the cycle of rate cuts was over. This year, another 75-100 basis point increase is expected.

The economy is worried about inflation, and the RBI is about to face a critical test in its fight against it, which led to this decision.

Shaktikanta Das also said on May 4: “There is a risk that if inflation stays high at these levels for too long, it could de-anchor inflation expectations, which could cause inflation to rise on its own and hurt financial growth stability. So, we need to be ready to use all policy tools to keep macroeconomic and economic strength while making the economy more resilient.

Economists and people who study the stock market are confused.

A month ago, RBI said it had no plans to raise interest rates to bring down inflation. In just under a month, the Reserve Bank of India’s (RBI) Monetary Policy Committee (MPC) said they wouldn’t raise interest rates while being open to growth, saying they would raise interest rates while still being available to change.

So, what made everyone run so fast between the wickets? There is inflation, but how scary is it?

Consumer Price Index (CPI)-based inflation in India has been above 6% for three months. Because of how quickly these events have happened and how quickly RBI has moved, it is even more important to look at the MPC’s decision. During the MPC meeting in April, RBI’s deputy governor Michael Patra said that 60% of developed countries expect inflation to be above 5%, which hasn’t happened since the 1980s. More than 50% of developing countries expect inflation to be above 7%. Is the RBI right to raise rates? What will that mean for the markets?

Patra said that the rise in prices worldwide is putting people’s patience to the test. So, it seems like a good idea to raise interest rates to stop inflation, or does it?

Should I go hiking or not?

Some economists say that raising rates now would be a bad idea because India’s inflation is mainly caused by supply-side problems and rising global commodity prices. The war between Russia and Ukraine has helped.

Other experts also say that high-interest rates won’t help cool down the economy and lead to a hard landing or even a recession.

But everyone agrees that such a move was necessary to protect the INR in the face of the USD’s steady rise and a steady outflow of capital. High-interest rates will stop the rupee, which is at an all-time low, from going down further. If the interest rates hadn’t gone up, they would have gone down even more. We’ll talk about this soon.

But there is another point of view.

With high inflation around the world and the U.S. Federal Reserve raising interest rates, can India afford to stay behind? When this happens, it’s essential to be part of a global story in which a central bank is seen to act on a problem instead of not working on it. This is especially true in a world where integrated trade and the Indian economy depend significantly on oil imports and software exports.

Big companies’ plans for capital expenditures won’t be affected by high-interest rates. Still, smaller companies and SMEs will have to pay more to refinance their loans, especially in the finance industry.

This is now showing up on stock markets, where the Nifty 50 index is down 8% and the smallcap 100 index is down 15%.

Can raising rates slow down inflation?

First of all, a look at the CPI inflation numbers for March, when it was 6.95 percent, shows that prices have gone up or stayed the same for every good.

Eggs had little inflation at 2.44 percent, while oils and fats had the most at 18.79 percent. With prices going up for most things, like clothes and shoes, housing, transportation and communication, and fun and games, it’s safe to say that inflation is now widespread.

“The RBI’s interest rate hikes don’t change the prices of food or fuel so that these prices will move on their own. But if these start moving to other parts of the economy because they are linked, bad things happen. Now, the tightening of money makes these connections weaker, says DK Joshi, chief economist at Crisil.

Pronab Sen, who is the country director for the India program of the International Growth Centre, says that the RBI policy won’t affect inflation or the economy. Still, it will cause stock prices to drop as the way people hold their assets adjusts to the rising rate.

“The rise in the policy rate and the rise in the CRR won’t change the economy much, except for the stock market, because there is still too much money in circulation. This kind of policy works when you’re close to the edge, have extra cash, or have just the right amount. But if you have a lot of extra cash, taking a little bit out won’t make much of a difference,” says Sen, India’s chief statistician.

When asked what might happen to inflation, he says, “I don’t think it will be very much.” And the reason is that inflation will keep happening as long as corporations have pricing power and can pass on cost increases. This means that inflation will keep happening as long as the prices of global commodities stay high. Nothing will happen on this side (of inflation) until that changes.

The government has told RBI to keep the CPI inflation rate at 4 percent, give or take 2 percent. The Monetary Policy Framework is broken if the CPI inflation rate stays above or below these levels for three straight quarters.

This framework was signed by the RBI and the Finance Ministry in September 2016. The RBI’s main goal was to control inflation, and a Monetary Policy Committee was set up (MPC).

“It’s now clear that the (rate) journey is going only one way, up… “People should expect more of the same in this fiscal year,” says Devendra Kumar Pant, chief economist at India Ratings and Research.

Keeping track of money and money flows

The U.S. Dollar index, or DXY, has been steadily increasing since May of last year. This is because interest rates are rising, and liquidity is going away. The index has gone from a low of 89.5 on May 25, 2021, to just above 104 on May 9, 2022, which is a level that hasn’t been seen since July 2002.

The DXY compares the value of the U.S. Dollar to six other currencies: the Euro, the Swiss Franc, the British Pound, the Canadian Dollar, the Japanese Yen, and the Swedish Krona. The Euro has the most weight in the index, at 57.6%.

Over the past year, the steady rise in DXY has been terrible for currencies in emerging markets. The last one to give up and fall was the Chinese Yuan, which kept its gains against the USD for most of 2021.

Brazil, which makes money when the prices of commodities go up, has also been decimated. When the INR fell below 77 for the first time on May 9, it was the lowest it had ever been against the USD. Thailand, Malaysia, Indonesia, and Taiwan have all seen their currencies fall against the USD.

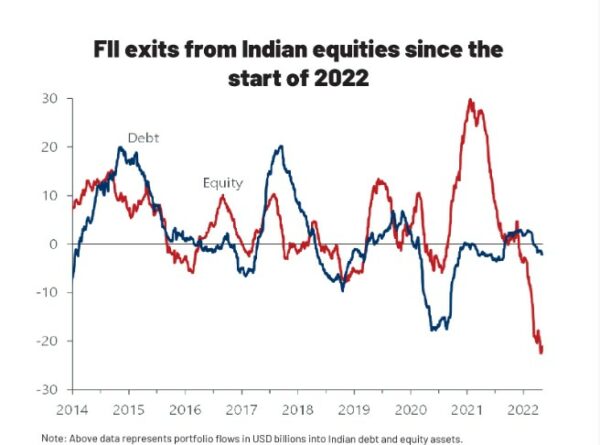

Because of the strength of the USD and the possibility of a long cycle of rate hikes, money is leaving the country.

India’s foreign exchange reserves hit a record high of USD642.45 billion in September 2021. As of the week ending April 29, 2022, they had dropped by USD44.73 billion to USD597.72 billion.

The strong dollar and capital outflows are the main reasons foreign exchange reserves are going down. Since September 2021, foreign portfolio investors have pulled USD21.43 billion out of Indian equity markets.

These things might have made the RBI act before the U.S. Fed did.

If the U.S. raises rates while Indian rates stay the same, the difference between the two economies’ interest rates gets smaller, making the problem of capital flight worse. One of the main reasons for record inflows until April 2021 was that rates in developed markets were close to zero, and rates in India were between 5 and 6 percent.

The rupee has been pretty stable since the RBI raised rates. Pant says that if the RBI hadn’t raised rates, our currency could have lost another 2% against the USD when the U.S. Fed raised rates.

Stock markets and the loss of liquidity

Since the global financial crisis of 2008-2009, liquidity injections by international central banks, led by the U.S. Fed, have become a more significant factor in stock markets than corporate earnings.

Turn on the cash flow. The price of taps and stocks is roaring higher, and if you turn them off, the movement will stop.

Now that central banks are starting to get rid of the liquidity they have been building up since 2008; it is causing problems in the stock, bond, currency, and commodity markets.

Since March 2020, many of India’s plans to help the economy have included steps by the RBI to increase liquidity that cost more than INR8 lakh crore. Now that inflation is hurting, the RBI has also started to take away this liquidity in stages. When the CRR goes up by 50 basis points, more than INR87,000 crore will be taken out of circulation.

With the failure of several measures and payments, the RBI has already taken INR2.94 lakh crore out of the system. Last year, INR2.3 lakh crore was taken out of the economy through open market sales and forex operations.

Some of these funds were going into the stock market, which is where this change is most noticeable. “What do you think will happen to the economy when the RBI starts to cut back on liquidity?” What happened before, and where did the extra cash that wasn’t being used to give out more loans go? “Some of that money was put in the reverse repo window, but a big chunk of it goes into the stock market,” says Sen.

A person who knows what the RBI is thinking says, “The RBI lowered accurate rates below zero because the economy shrank much more after the pandemic. Getting rid of the money is even more complicated than raising interest rates. If the economy doesn’t reach an exit velocity, it’s hard to get out of what’s called the liquidity trap. But as inflation soared, the RBI had to cut off the flow of money to keep inflationary expectations in check.

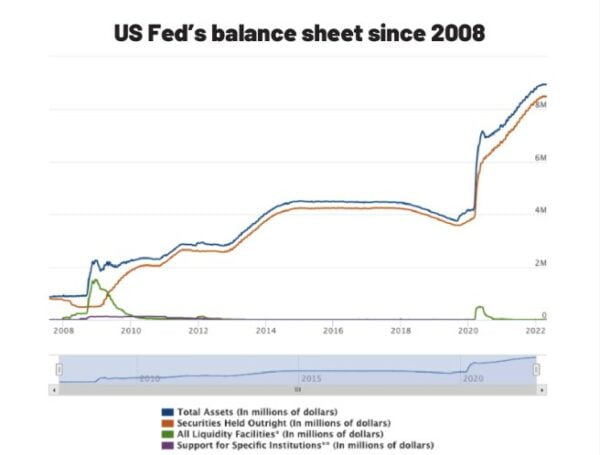

Because of this, stock markets in India and worldwide have dropped sharply. From September 1, 2022, the U.S. Fed will start selling US$95 billion worth of treasury bonds and other securities every month. This is the fastest rate when the U.S. Fed will begin to reduce its nearly USD9 trillion balance sheet.

At this rate, the U.S. Fed’s balance sheet will shrink by a little more than USD1.1 trillion in a year. The speed at which these funds are being taken out makes the USD stronger and makes stocks continue to lose value.

Effects on the debt market and the economy

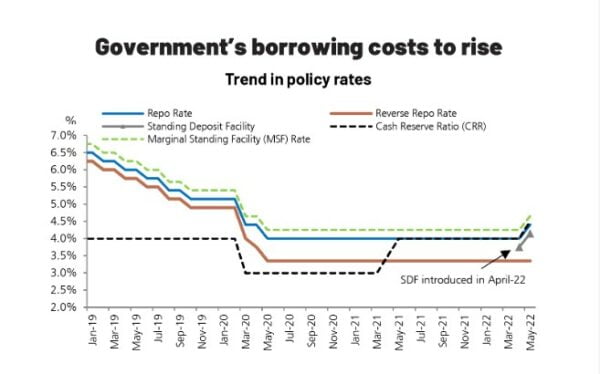

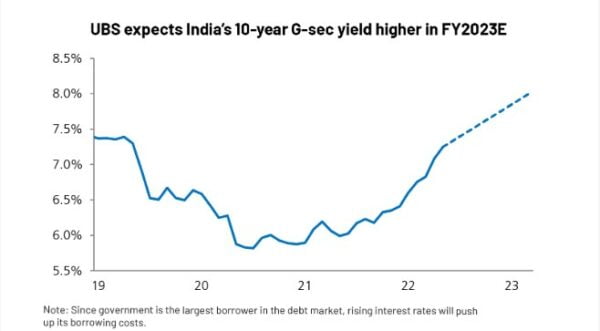

The government is the biggest borrower in the debt market, and its borrowing costs go up when interest rates go up. The 10-year benchmark government security yield has gone up from a low of 5.75 percent in July 2020 to a high of 7.45 percent on May 6, 2022. Most analysts think that profits will go over 8% in the next year, with a peak of around 8.85% in the middle term.

In 2022-2023, the Centre is expected to borrow around INR14,95 lakh crore. As interest rates go up, the average cost of borrowing for the government will go from 6.3% in 2021-22 to over 7% in the current year.

But the government doesn’t think there will be any problems with raising debt. “When yields are between 7.5% and 7.6%, companies usually buy gilts. “Compared to the global financial crisis of 2008, when our borrowings nearly doubled in two years, the increase after Covid is not that big, and the supply can be taken in,” says another government official.

The RBI will deal with the volatility and sharp jumps in yields to keep the debt market stable. “The RBI is willing to let yields go up slowly, but not all at once, and it has the tools to step in when necessary,” says the official.

Effects on the everyday man

Rising yields are likely to cause significant mark-to-market losses on the bond portfolios of commercial banks that are in the AFS or “available-for-sale” bucket. For retail borrowers, the interest rates on their home loans, car loans, and other loans are going up a lot. Saver rates on fixed deposits will also go up, but actual interest rates are expected to stay negative if inflation remains higher than deposit rates.

And the effects on the economy as a whole will be different, depending on which sectors are affected by interest rates and which ones are weak. Industries that were still hurting from the Covid pandemic, such as trade, hospitality, and transportation, will be hit harder than sectors like agriculture and finance, which are more resilient.

Gross value added (GVA) data for 2021-22 showed that the output of all sectors except “trade, transport, communication, and broadcasting services” had risen above the level of 2019-20. This means that “trade, transportation, communication, and broadcasting services” have not yet reached their status before the pandemic. So, rising interest rates could stop this part of the economy from growing before it even starts.

Soft or almost soft landing vs. recession

Policy tightening has brought up whether or not inflation can be fought without putting the economy into a recession. When rates stay high for a long time, economies go into recession, when the GDP falls for two quarters in a row. It could mean that India’s growth rates slow down or even recession.

In this situation, RBI’s Patra’s April 6-April 8 MPC meeting remarks, which were released on April 22, brought the debate about a soft landing vs. a hard landing to the forefront.

“The main question is whether or not it will be a Goldilocks moment. Will central banks provide the perfect deflation, also known as a “soft landing”? Or will they miss the runway and cause an unwelcome recession in a world already tired of pandemics, war, and supply chains that are worn and torn? The idea that inflation has broken glass ceilings and that the only way to stop it is to force a recession, or “hard landing,” is becoming more popular. The problem is even worse for central banks that have two different jobs. “Will their jobs let them kill the economy to keep prices stable?” Patra asked.

At this point, it’s hard to say how these policy actions will turn out.

Joshi of Crisil says, “If they (the RBI) want to control inflation, they have to slow down the economy. They can’t stop inflation without making the economy move more slowly. This is also what the Fed tries to do. That’s why people worry about whether or not this will cause a recession.”

When inflation got too high in the past,

Central bankers like to tell the story that during World War I, if a person went to a bar in Zimbabwe and ordered one mug of beer, they would immediately call a second one.

Because by the time she finished her first beer, the price of the second beer would have gone up a lot. This was a sign of hyperinflation when prices increased by at least 50% per month.

In their study “30 World Hyperinflations,” economists Steve H. Hanke and Nicholas Krus tried to put hyperinflation in perspective by figuring out the equivalent daily inflation rate and its time for prices to double.

It showed that Hungary had the world’s worst hyperinflation. In July 1946, when it was at its worst, the daily inflation rate was about 207 percent, which meant that prices doubled every 15 hours. The next one was Zimbabwe, where prices doubled about every 24 hours and a day in 2007 and 2008.

Even though inflation in the U.S. is nowhere near what it was in these countries, price spikes that stay above “comfort zones” are a big problem for any economy.

“We can handle a certain amount of inflation, and it’s good—but high inflation that lasts for a long time can cause social unrest, bringing down governments. That’s the real fight,” said the senior government official quoted earlier.