India’s financial inclusion goals could be achieved with the help of neobanks

Neobanks might be the best answer for attaining financial inclusion in India, given the rapid expansion of the Internet and the widespread usage of smartphones in both urban and rural areas.

India has a 47 per cent Internet penetration rate, with 34 million new users expected between 2021 and 2022. India is expected to reach one billion smartphone users by 2026, according to a Deloitte estimate. India has 1.2 billion mobile customers, with 750 million of them using smartphones.

No, this isn’t a piece on India’s digital transformation. However, these figures are noteworthy because they show that the Internet is used for a variety of purposes, including entertainment, education, healthcare, commerce, marriage, love, and even house purchases. Indeed, one would believe that if you had access to the internet and a mobile phone, you may traverse the world without ever having to visit a bank, a store, or an airline office. The Internet and mobile phones are, indeed, omnipresent.

Is banking a part of this equation? Digital banking has undeniably changed the way we bank; but, in a huge and varied country like India, the perception of a bank remains a brick and mortar facility, where opening a bank account takes hours, several forms, and tedious processes. In traditional banks, the client experience does not foster trust or loyalty to the institution.

Although digital banking has grown relatively ubiquitous in urban India and is sometimes even taken for granted, a substantial percentage of Indians remain unbanked or neglected. According to the 2017 Global Findex Report, India has the second biggest unbanked population in the world, with 190 million individuals.

Even though programmes like the Pradhan Mantri Jan Dhan Yojana (PMJDY) have succeeded in creating bank accounts, the total number of bank accounts as of October 2021 is 435.7 million. Having a bank account does not guarantee financial inclusion.

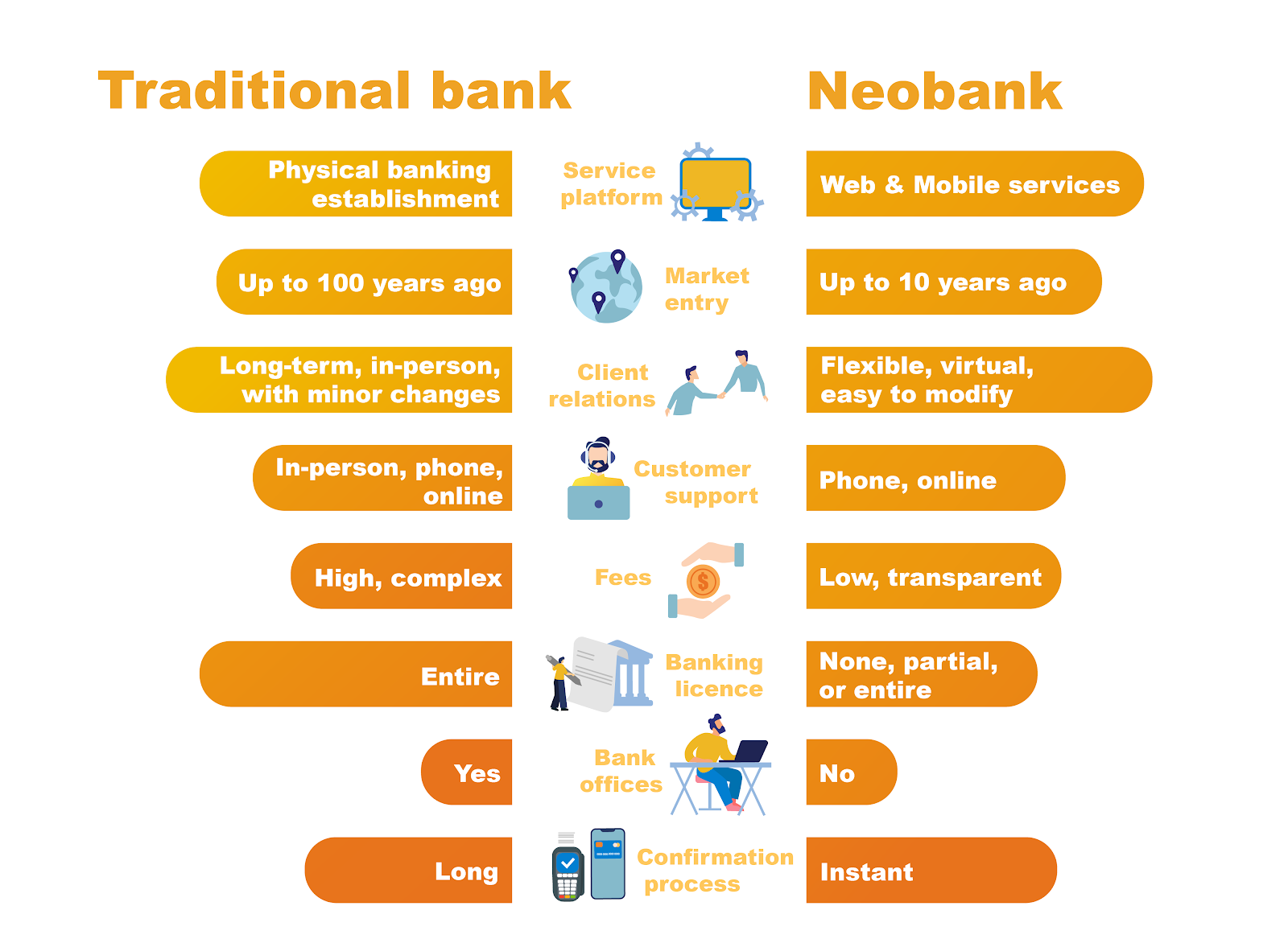

Financial Inclusion Challenges with Traditional Banking

Financial literacy, which includes awareness of financial services as well as an open mind and positive attitude toward banking services including access to loans, simple withdrawals, money transfers, and more, has a long way to go.

At least 52% of respondents in NABARD’s All India Rural Financial Inclusion Survey 2016-17 wanted to maintain their money at home. Many rural people who opened bank accounts under the PMJDY have not conducted any transactions beyond the initial one or two because questions such as “zero balance” or even an “overdraft” facility have not elicited satisfactory explanations, leading to a mistrust of banking services and “inoperative accounts.”

Banks do not consider it commercially viable to open branches in rural areas with few inhabitants. To address some of these issues, banks have developed an omnichannel strategy that combines digital banking with ATM kiosks and physical banking to offer a variety of goods and services.

Despite several attempts and initiatives by the Reserve Bank of India (RBI), nationalized banks, and financial institutions, financial inclusion remains elusive for many people due to a lack of access.

Neobanks Have the Potential to Move the Needle Toward Financial Inclusion

Neobanks are challenging traditional financial services with the unique notion of online-only banking, employing technology that provides more access at no cost to the client. Neobanks is going where no other traditional bank branch has gone before, allowing consumers to get ordinary banking services such as account opening, withdrawals, transfers, loan access, monitoring bank balances, and even investments.

When a business correspondent uses his phone to show the functions of a Neobank, a farm labourer named Kumari in a remote hamlet in Uttar Pradesh may ask questions, get answers, and observe how Neobanks work in real-time.

Being aware of what is available and what can be done with banking is half the battle won, especially in a country where financial literacy has been lacking.

Consider a migrant labourer’s wife maintaining her home and a small piece of land alone, with her children.

It’s a clear validation of how technology can be used effectively for banking service delivery if she doesn’t have to walk miles to the nearest accessible and available kiosk to pay utility payments, but instead can use her Neobank app to do so, or can refer someone in her community about the ease of opening a bank account in minutes, rather than having to first walk to the nearest bank branch, fill out forms, and then wait for the process to be completed.

Neobanks have an advantage over traditional banks in that they can quickly and easily customize their service offerings. Traditional banks, especially in distant areas, need time to pivot their technology to better serve their consumers.

When end customers see that there are products and services tailored to their needs and that they don’t have to deal with rude bank staff or even pay for many of the services, such as a zero balance facility or an overdraft facility, they gravitate toward simplicity, ease, and speed, combined with technology – yes, the Neobank can, and in many cases, is already the bank of choice for the underserved or unbanked.

While Neobanks’ benefits greatly transcend those of traditional banks, because they are tech-driven, they may be limited in their ability to serve non-tech aware parts of the population. However, given the country’s rapid rise in smartphone users and the acceleration of digital adoption spurred by rural India – which is at a solid 13%, with the mobile phone as the preferred device – Neobanks might be the vehicle to bring financial inclusion in the short future.

edited and proofread by nikita sharma