Tax evolution demands coherent rules to run one of the most rigid tax systems in the world. With the commencement of the new fiscal year comes new avenues and targets. Indian tax administration has revamped crucial rules, which would change the dynamics of tax-paying for individual taxpayers. Before moving ahead, the prolepsis of the rigorous tax system has led to an overhaul in the tax rates.

The rates accustomed in India are highly charged due to the government’s accountability to cover their expenditure across various developing units. Tax collection revenue generally differs from state to state and is set according to the average of last year’s collection. The real question is- will the new change ease down the situation amid the harsh circumstances, or will it increase the burden even further? Let us have a lookout for what could be the changes in the Indian taxpayers’ system.

The first year for Option to Choose From Two Tax Regimes

The Annual budget for 2021-22 has introduced a new regime, where an individual taxpayer has choices to opt from. The individual taxpayers now have the privilege of opting out for the best-suited regime according to their income.

They could either opt for lower rates coupled with a few deductions available or go with the regular regime. Additionally, the exceptions deductible under the Income Tax Act would get reduced in the newly adopted regime. It is the first year of the practice, and its implication would require thorough knowledge and understanding of the system. The amendment in rules would exercise you the option to sustain with the current system or migrate into the new system.

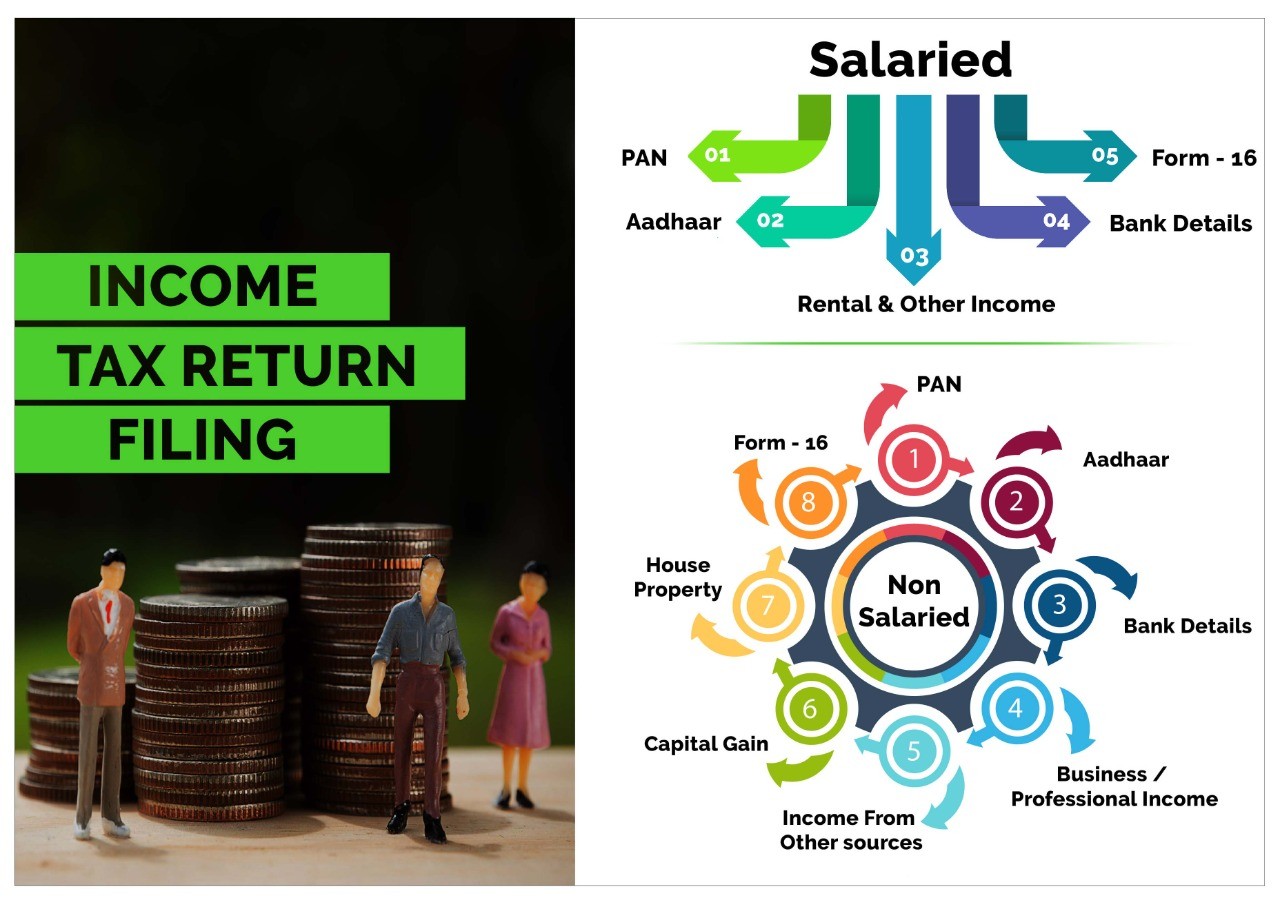

The scenario is slightly different when it comes to salaried people. The salaried people have more flexibility than most of the business income people. The difference gathers a lot of speculation about evasion as the business incomes have to stick to the rigid structure of the regime. The salaried persons have the option to shift from regimes every year, whereas the business income people are restricted to adopt one style of the regime until they force themselves out of action.

The taxpayer would be accustomed to stringently follow the regime unless they discontinue their business. Eventually, the one with business income has to comply with one or the other regime keeping into account the longer-term implications. The jinx among the authorities has been on improving the tax collection while keeping the rates within reach of the taxpayers.

Generally, the salaried people exercise a regime with the employer at the commencement of the financial year. The vital changes in rules avail them of the feasibility of changing the tax regime while filing the ITR. The situation gets complicated when the employers validate the rules according to the company’s norms. The option exercised with the employer is limited to deductions, and hence the change could enhance more flexibility.

The business income has an upheaving concern on their heads, whether to adopt the new regime or exist with the current system. If the businesses do not want to comply with the new regime this year, they can adopt the new regime in any subsequent year. The focal point should be that there is no turning back to the old regime once the new rules are accustomed within the company’s administration.

Why could such a change get implemented by the statutory bodies?

The amendments would create more complications in the state of affairs, and the businesses would have to follow the rigid structure. Although the new regime amends lower rates, it would take great knowledge for the businesses to thrive in the system. The previous year’s changes oversaw many deductions under section 80C including, exemptions on house rent allowance, leave travel allowance, and the deductions on interest paid on home loans being rescinded from the system.

The tax amendments were a severe burden on the heads of the individuals who were not owing to give these many deductions within a single year. The government kept in view the ramifications of the lockdown in its hindsight, but it had no major propelling impact on the income tax slabs. Dividends were hard to come by due to lack of business activities, and the government got compelled to charge the dividend received from mutual funds and domestic companies at the recipient’s hands.

Reduced Period for Filing the belated ITR or for revising your filed ITR

In previous scenarios, if you failed to file your ITR by the due date of July 31, you could still file it by March 31 with a late fee. But not any longer. The Financial bill that was being instituted by the government has reduced the time filing period for ITR. The bill for 2021-22 has a proposal to reduce the time limit by three months.

It efficiently reduces the expanded feasibility that has been awarded to the individual taxpayers for years. Is the government running short on funds despite surrendering so many amounts in terms of schemes? Or is it a genuine effort this time around to reduce the conundrum of tax evasion?

This year would be very challenging for the taxpayers as they have to sort their books by the end of December 31. Our suggestion would be to file your ITR as soon as possible so that you have ample time to revise it in case any mistake gets noticed. Likewise, the flexibility is turning into rigidness as the government does not want to give any due considerations to the tax regime.

The fact that the public debt borrowings have increased, the government is opting to sort out its expenses by the way of tax collection. So it is time that the lower bracket taxpayers get more burden on their hands, or is the right call? The opinion is up for debate and shall be open at all ends for discussion.

Inclusion of dividend income in ITR for the year ended March 31, 2021

Till March 31, 2020, the dividend received from Indian companies and mutual funds was free from the jurisdiction of tax in your hands. But since the emergence of the pandemic, the situation has taken a substantially crazy U-turn.

Nobody in public could believe that the government is looking to increase their revenues by opting for restrictions on human resources. The dividend received is considered as one’s perpetual income which has been kept aside but the government seems to not bother. Previously, the tax on the dividend or income distributed got paid by the company or the mutual fund.

The Budget of 2020 had removed the exemption on dividend income, making the tax bracket more expensive in the Government’s hands. The same exemptions have now become taxable at our ends. If the amount of dividend received does not exceed Rs5,000, the taxpayers would not be accustomed to any tax. The other side of the aspect says that if it exceeds the mentioned amount, the company or the mutual fund houses would have deducted tax while crediting the dividend to your bank account.

Please verify the amount of tax deducted to avoid further complications. In case TDS gets reflected in Form 26AS, you need to gross up your dividend income by adding the amount of tax deducted. The tax regulators would check for the correct and systematic disclosure of your taxable dividend income.

The situation would get overloaded for the taxpayers as so many complications in one go would lead to facing delay in filing the ITR and hence paying late fees to submit the form. Keeping in mind, the grossed-up income is just to reflect an amount that has no tax exemptions available. The regulators are just hyping the government’s code as there is a full reflection as to why such a stubborn system might get enforced.

Removal of Exemption From the Employee Provident Fund.

EPF is a type of security deposit that you contribute as well as the employer contributes some share to your provident fund account. Although, in previous years, there was an exemption on the voluntary contribution in the EPF. It was applicable throughout the states and the central tax regime even if it goes beyond the mandatory 12% of your basic salary. The EPF is a significant fund for all the salaried people as they deposit a certain proportion of their income in it to attain certifiable interests in the future. In the Budget of 2021-22, the woes of the salaried people have worsened.

The Finance Minister has proposed that this exemption on interest credit in your EPF account will no longer be available for the annual contribution made beyond 2.5 lakhs. It has come into effect from April 1, 2021. However, if the employer does not accumulate funds to your provident fund account, the budget has proposed a higher threshold limit. Even though the limit has its debatable weaklings, the finance bill should have proposed some easy measures for the people conceding the bizarre effects of the mishappening.

Changes effective on investments made in ULIP

The maturity proceeds received from any life insurance product including a ULIP are exempt if the premium paid on such policy does not exceed 10% of the sum assured. The focal point of the exemption was to ensure safe and secure return on investments to the investors as the loggerhead suffers from not getting enough of the maturity proceeds. However, it will not be the same with effect from the Financial year 2021-22.

The Budget for 2021-22 is accustomed to removing the exemption partially. In case the aggregate annual premium for all the ULIP policies taken together exceeds Rs 2.50 Lakhs, the exemption would not apply. The bewildering situation asserts that the profits claimed by the recipient will get treated as an equity product. A deduction of 10% would be allowed without indexation.

The exemptions have been cut, the rates have reached eye-catching figures, can we expect any feasible situations related to income tax shortly? That’s the question that the authorities need to answer. The main prolepsis of the wholesale of changes would make the taxpayers comply with rigid tax rules which would enforce them to avail fewer benefits than what they did in preceding years.

The average collection by the government would eventually increase by the hands of the taxpayers thus curbing the in-hand income adversely. Studying and amendments of rates would go on to further levels as it remains intriguing to seek that this would pan out.