NSE’s ₹30,000 Crore IPO Is Finally Here, But Is India’s Most Powerful Market Monopoly Worth ₹5 Lakh Crore?

For nearly a decade, the NSE's ambitions of going public remained trapped in regulatory limbo. Now, with the filing of its draft papers for what could become India's largest-ever IPO, the country's most dominant stock exchange is finally preparing to test public market appetite. Yet beyond the size of the offering lies a more important question: how should investors value one of India's most powerful financial institutions?

Few major Indian companies have had to wait as long for a stock market debut as the National Stock Exchange. While hundreds of startups, banks, manufacturers and technology firms have entered public markets over the past decade, the country’s largest stock exchange remained conspicuously absent from the list.

The journey began in 2016 when NSE first filed draft papers for an initial public offering. At the time, the exchange planned to raise around ₹10,000 crore through an offer-for-sale by existing shareholders. Given NSE’s dominance in India’s capital markets, the listing was expected to be a landmark event that would allow investors to own a stake in the very institution facilitating billions of rupees worth of trades every day.

Those plans, however, soon ran into trouble.

The exchange became embroiled in the infamous co-location controversy, a case that centred on allegations that certain brokers received preferential access to NSE’s trading infrastructure, potentially giving them an unfair advantage over other market participants. The issue triggered years of investigations, regulatory scrutiny and legal proceedings, effectively placing NSE’s listing ambitions on hold.

For SEBI, the matter carried implications far beyond a routine compliance issue. Stock exchanges occupy a unique position within the financial system. They are not merely profit-making enterprises but also critical market institutions entrusted with ensuring fairness, transparency and investor confidence. Any perceived governance shortcomings therefore attracted far greater scrutiny than would ordinarily be the case for a listed company.

As the years passed, NSE repeatedly approached the regulator seeking approval for its IPO. The exchange strengthened governance mechanisms, enhanced compliance frameworks and worked to address concerns that had stalled the listing process. Yet progress remained slow, turning what was expected to be a straightforward market debut into one of the longest IPO waits in India’s corporate history.

The breakthrough finally came after the exchange moved to settle the long-running co-location matter. In 2025, NSE reportedly offered to pay ₹1,388 crore as part of a settlement process aimed at drawing a line under the controversy. Subsequently, regulatory approvals began falling into place, culminating in SEBI granting the necessary clearances that allowed the exchange to move ahead with its long-delayed public offering.

The filing of the Draft Red Herring Prospectus therefore represents far more than just another IPO application. It marks the end of a decade-long regulatory overhang that had become synonymous with NSE’s public market aspirations. More importantly, it opens the door for investors to participate directly in one of the most influential institutions in India’s financial ecosystem.

With an expected issue size of around ₹30,000 crore and a valuation estimated at more than ₹5 lakh crore, the proposed offering is not merely about raising capital or providing an exit route for existing shareholders. It is about bringing India’s largest exchange into the public markets at a time when the country’s equity culture is expanding rapidly, retail participation is at record levels and capital markets have become increasingly central to India’s growth story.

What’s Actually On Offer?

While the headline-grabbing figure is the estimated ₹30,000 crore size of the offering, investors should understand that NSE’s IPO is fundamentally different from many recent public issues. The exchange is not raising fresh capital to fund expansion, acquisitions or new business initiatives. Instead, the proposed offering is entirely an offer-for-sale (OFS), meaning existing shareholders will sell a portion of their holdings to public investors.

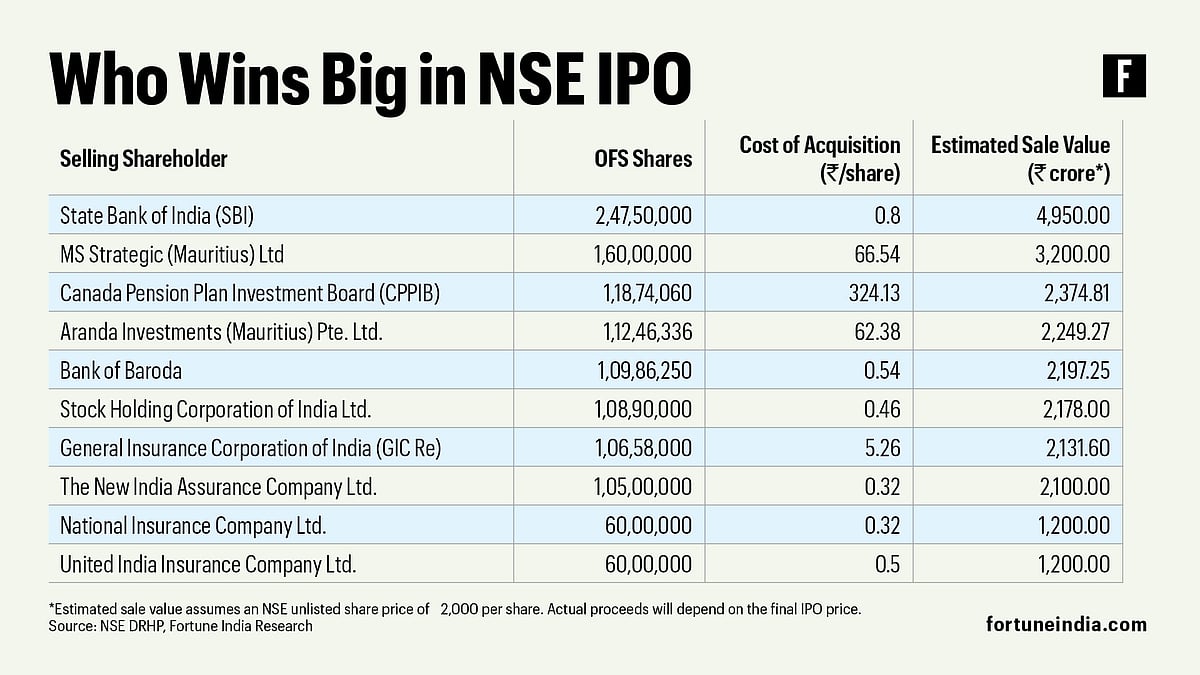

According to the draft papers, up to 14.89 crore equity shares will be offered for sale, representing roughly 6% of NSE’s paid-up equity capital. Because no new shares are being issued, the proceeds from the IPO will flow to the selling shareholders rather than to the exchange itself.

The list of sellers reflects the diverse ownership structure that has evolved over the years. State Bank of India, one of NSE’s earliest institutional backers, is among the largest shareholders participating in the offer. Other prominent sellers include SBI Capital Markets, Bank of Baroda, Stock Holding Corporation of India, New India Assurance, General Insurance Corporation of India and several domestic and international investment entities.

For many of these investors, the IPO represents an opportunity to partially monetise holdings that have remained largely illiquid for years. NSE shares have traded actively in the unlisted market, often commanding premium valuations, but a public listing offers far greater liquidity, transparency and price discovery.

What makes the offering particularly significant is its sheer scale. Market estimates suggest the IPO could be valued at around ₹30,000 crore, comfortably surpassing the previous record set by Hyundai Motor India’s ₹27,870 crore public issue. If achieved, the listing would become the largest IPO ever undertaken in the Indian market.

The numbers become even more striking when viewed through the lens of valuation. Based on prevailing prices in the unlisted market, analysts estimate NSE’s market capitalisation could exceed ₹5 lakh crore. That would place the exchange among the most valuable financial institutions in the country and ahead of numerous established banks, insurers and industrial companies.

Yet the size of the IPO alone does not explain investor interest. Unlike many companies that come to market promising future growth, NSE enters the public arena as a mature, highly profitable business with a dominant market position already firmly established. Investors are not being asked to fund an uncertain expansion story. Instead, they are being offered a chance to own a slice of an institution that sits at the heart of India’s financial system.

This distinction matters because it shifts the investment debate away from questions of growth capital and towards questions of valuation. The key issue is not whether NSE needs the money. Rather, it is whether investors believe the exchange’s dominant position, profitability and strategic importance justify the premium valuation being sought through the offering.

Why Is NSE Worth So Much?

The proposed valuation of more than ₹5 lakh crore may appear staggering at first glance. After all, NSE does not manufacture products, operate factories or sell consumer goods. Its business is far less visible than that of banks, technology companies or industrial conglomerates. Yet that is precisely what makes the exchange such a unique asset.

At its core, NSE benefits from one of the most powerful advantages in business: network effects. Traders, investors, brokers and institutions naturally gravitate towards the platform where liquidity is deepest. More liquidity attracts more participants, which in turn creates even more liquidity. Once that cycle becomes established, it becomes extraordinarily difficult for competitors to break.

Over the years, NSE has built an overwhelming lead in India’s equity and derivatives markets. In the cash segment, the exchange processes average daily trading volumes exceeding ₹1 lakh crore, dwarfing most competitors. Its dominance is even more pronounced in derivatives, where futures and options trading have become a major driver of market activity and exchange revenues.

The result is a business that enjoys a near-monopoly in several of its most profitable segments. While competitors such as BSE continue to grow and innovate, NSE remains the default venue for a significant share of India’s trading activity. For brokers, institutions and investors, participation in Indian capital markets often begins and ends with NSE.

That dominance translates directly into financial performance. In FY26, the exchange generated revenue of over ₹16,600 crore while reporting net profit exceeding ₹10,300 crore. Few businesses anywhere in the world operate with margins of that magnitude. Even more remarkable is the fact that these profits are generated without the capital intensity associated with traditional industries.

Once an exchange has built its technology infrastructure, regulatory framework and market ecosystem, the cost of handling additional transactions becomes relatively small. Whether a million trades take place or ten million trades occur, the incremental cost increase is limited. Revenue, however, continues to grow with market activity.

This creates a highly scalable business model. Every increase in trading volumes, every new listed company, every additional ETF and every surge in retail participation contributes to revenue generation without requiring proportional increases in operating costs. As a result, stock exchanges often enjoy margins that many other industries can only dream of.

Another factor supporting NSE’s valuation is the broader growth trajectory of India’s capital markets. The number of retail investors has expanded dramatically over the past decade. Systematic investment plans continue attracting fresh money every month. More companies are choosing to raise capital through public markets, while domestic participation has increasingly reduced dependence on foreign portfolio flows.

For investors, therefore, buying NSE is not simply a bet on an exchange. It is effectively a wager on the continued expansion of India’s financial markets. As more Indians invest, trade and participate in capital markets, NSE stands to benefit from nearly every stage of that activity.

That helps explain why investors have been willing to assign premium valuations to exchange businesses globally. They combine characteristics that are rarely found together: market leadership, recurring revenue streams, strong cash generation, limited capital requirements and significant barriers to entry. The question facing investors is not whether NSE is a high-quality business. The debate is whether those strengths justify the valuation being demanded through the IPO.

The Business Of Running India’s Markets

One reason stock exchanges command premium valuations is that many investors underestimate how many ways they make money. To the average market participant, an exchange is simply a platform where shares are bought and sold. In reality, it is a diversified financial infrastructure business with multiple revenue streams feeding into the same ecosystem.

Transaction charges remain the largest source of income. Every time an investor buys or sells a stock, futures contract, option or currency derivative, a small fee flows to the exchange. Individually these charges may appear insignificant, but when multiplied across millions of daily transactions, they generate substantial revenue. For NSE, transaction charges contributed more than ₹13,000 crore in FY26, making them the backbone of the business.

Yet trading activity is only one piece of the puzzle.

Whenever a company decides to go public, list bonds or launch products such as REITs, InvITs and exchange-traded funds, it pays listing fees to the exchange. Annual listing fees create an additional recurring revenue stream. As India’s corporate sector expands and capital markets deepen, these revenues continue to grow alongside market activity.

Then comes market data, an increasingly valuable asset in modern finance. Brokers, banks, mutual funds, hedge funds and trading firms rely on real-time market information to make decisions. Exchanges package and sell this data through subscription services, analytics platforms and terminal-based products. In a world where information can create competitive advantages measured in milliseconds, market data has become a lucrative business in its own right.

Index licensing represents another high-margin revenue stream. Every ETF, index fund or derivative product linked to benchmark indices requires licensing agreements with the exchange. As passive investing gains popularity and assets under management continue to expand, these licensing revenues provide a growing source of relatively predictable income.

The exchange also earns through clearing and settlement services. Every trade executed on the platform must ultimately be cleared and settled, ensuring that buyers receive securities and sellers receive payment. This critical function generates additional fees while reinforcing the exchange’s central role within the financial system.

Beyond these visible sources lies a technology-driven revenue stream that rarely receives attention. Brokers and financial institutions pay to host servers within exchange data centres, enabling faster access to trading systems. In markets where execution speed can influence profitability, proximity to exchange infrastructure carries considerable value.

Together, these revenue streams create a remarkably resilient business model. If IPO activity slows, transaction revenues may continue growing. If trading volumes moderate temporarily, listing fees, data services and licensing income provide support. Rather than depending on a single product or customer segment, exchanges benefit from multiple interconnected sources of revenue generated by the same market ecosystem.

This diversification helps explain why stock exchanges are often viewed as some of the most attractive financial businesses globally. They sit at the centre of economic activity, benefiting whenever companies raise capital, investors trade securities or institutions seek market access. Few businesses enjoy such a broad exposure to financial market growth while maintaining relatively limited capital requirements.

For NSE, this model has helped create one of India’s most profitable enterprises. The exchange is not merely a venue where trades occur. It is an infrastructure platform that earns revenue from almost every stage of the capital market value chain, a characteristic that lies at the heart of its premium valuation.

NSE Vs BSE – The Gap Remains Wider Than Most Investors Realise

Any discussion about NSE’s valuation inevitably leads to a comparison with its oldest rival, the Bombay Stock Exchange. Both institutions sit at the heart of India’s capital markets, both benefit from rising investor participation and both operate highly profitable business models. Yet beneath those similarities lies a substantial difference in scale.

In FY26, NSE reported revenue of more than ₹16,600 crore compared to BSE’s ₹4,833 crore. The gap is even more striking at the profitability level. NSE generated net profit exceeding ₹10,300 crore, more than four times BSE’s profit of roughly ₹2,500 crore. Despite a decline from the previous year’s record earnings, NSE remains India’s largest and most profitable exchange by a considerable margin.

The clearest illustration of that dominance is visible in trading volumes. NSE’s average daily cash market turnover exceeds ₹1 lakh crore, while BSE’s stands at under ₹8,000 crore. In derivatives, arguably the most lucrative segment of the exchange business, NSE’s lead is even more pronounced. The exchange has spent years building liquidity, and liquidity tends to attract more liquidity, creating a competitive advantage that becomes increasingly difficult to challenge.

This dominance explains why many analysts view NSE as one of the strongest market franchises in the country. The exchange enjoys a scale advantage that not only boosts revenue but also reinforces its network effects. Investors trade where other investors trade, brokers focus resources where volumes are highest and institutions naturally gravitate towards the platform offering the deepest liquidity.

Yet the comparison is not entirely one-sided.

Over the past few years, BSE has delivered stronger growth rates across several financial metrics. Revenue growth, profit growth and activity in segments such as SME listings have outpaced NSE’s performance. BSE’s stock has consequently emerged as one of the standout performers in the Indian market, rewarding investors who bet on its ability to capture opportunities beyond its traditional role.

This raises an interesting valuation debate. NSE may be significantly larger, but investors do not merely pay for size. They also pay for growth. While NSE remains the undisputed market leader, questions inevitably arise about how much additional market share it can realistically gain from its already dominant position.

On the other hand, supporters of NSE argue that market leadership itself deserves a premium. The exchange controls critical infrastructure, commands the deepest liquidity pools and remains the primary gateway through which domestic and foreign investors access Indian equities and derivatives. Even modest growth in India’s capital markets could translate into substantial earnings growth because of the exchange’s highly scalable business model.

Ultimately, the competition between NSE and BSE is not a winner-takes-all battle. Both exchanges are benefiting from the rapid expansion of India’s financial markets. However, the IPO will force investors to answer a crucial question: should NSE be valued primarily as a mature market leader generating enormous cash flows, or as a business that still has significant room to grow alongside India’s increasingly sophisticated capital markets?

The answer will play a major role in determining whether the exchange’s proposed valuation of more than ₹5 lakh crore is viewed as justified, ambitious or perhaps even conservative.

The Billionaires, Institutions And Unexpected Names Behind NSE

Most IPOs attract attention because of the company coming to market. NSE’s proposed listing, however, has sparked curiosity for another reason: the extraordinary mix of shareholders who already own a piece of India’s largest stock exchange.

The shareholder register reads less like a typical corporate cap table and more like a who’s who of Indian business, global investing and financial institutions. Spread across more than 1.8 lakh shareholders are billionaire entrepreneurs, public sector entities, foreign investment funds, insurance companies, market veterans and even globally renowned academic institutions.

Among the most prominent names is Radhakishan Damani, the founder of DMart and one of India’s most respected investors. Damani’s direct holding, along with stakes held through related entities, has attracted considerable attention given his reputation for identifying high-quality businesses long before they become market favourites. Notably, neither he nor his associated entities are selling shares through the IPO.

The list also includes Infosys co-founder Kris Gopalakrishnan, whose investment reflects the appeal NSE has held for long-term investors over the years. Catamaran Ventures, associated with Infosys founder Narayana Murthy, is also among the shareholders choosing to remain invested.

Corporate India is equally well represented. Sunil Kant Munjal of Hero Enterprise features on the register, while entities linked to the Tata Group and Adani Group also hold stakes. Serum Institute of India, one of the world’s largest vaccine manufacturers, appears among the shareholders as well.

Then there are the institutional investors. Tiger Global, Morgan Stanley-linked entities, Citigroup-affiliated investment vehicles and several international funds have all found a place on the shareholder list. Their presence underscores the confidence that global investors have historically placed in the exchange’s business model and strategic importance.

Perhaps one of the more surprising names is the Massachusetts Institute of Technology (MIT), which appears as a direct shareholder. It is not every day that one finds a world-renowned academic institution sitting alongside billionaire industrialists and sovereign investment vehicles in the ownership structure of a stock exchange.

Retail investors may also recognise the name Dolly Khanna, the Chennai-based investor whose stock picks are closely followed by market participants. Her appearance on the shareholder register highlights the unusual diversity of NSE’s ownership base, where large institutions and individual investors coexist within the same cap table.

What makes this list particularly interesting is not simply the celebrity value of the names involved. Rather, it offers insight into how highly sought after NSE shares have been despite the company remaining unlisted for decades. Many of these investors entered long before the prospect of a public listing became realistic, effectively making a long-term bet on the importance of India’s capital markets and the exchange’s dominant position within them.

The IPO will undoubtedly provide liquidity for some shareholders. Yet the fact that several marquee investors are choosing not to significantly reduce their exposure may be interpreted by the market as a vote of confidence in NSE’s future prospects. For prospective investors evaluating the offering, the shareholder list serves as a reminder that some of India’s most successful wealth creators and institutions have already spent years placing their bets on the exchange.

Of course, famous names alone do not justify a valuation. But they do add another layer of intrigue to what is already shaping up to be one of the most closely watched public offerings in India’s corporate history.

The Real Question – Is NSE A Growth Story Or A Mature Cash Machine?

By the time NSE finally reaches public markets, investors will already know that it is a highly profitable business. The more difficult question is whether it should be valued as a growth company or as a mature cash-generating institution.

On one hand, the case for growth remains compelling. India’s capital markets are still expanding at a remarkable pace. Millions of first-time investors continue entering the market every year. Demat account openings remain strong, mutual fund participation is increasing and domestic investors are becoming an increasingly important source of market liquidity.

The pipeline of companies seeking public listings also continues to grow. From startups and technology firms to manufacturing companies and state-owned enterprises, more businesses are turning to public markets to raise capital. Every IPO, follow-on offering, ETF launch and derivative product creates opportunities for exchanges to generate additional revenue.

Viewed through that lens, NSE is not simply a reflection of today’s market activity. It is a leveraged play on the future development of India’s financial system. If India’s capital markets continue growing over the next decade, NSE stands to benefit from nearly every stage of that expansion.

However, there is another side to the argument.

Unlike many newly listed companies, NSE is already operating from a position of extraordinary strength. It dominates key trading segments, enjoys exceptionally high margins and generates profits that most listed companies would struggle to match. Such dominance naturally raises questions about how much room remains for further growth.

Recent financial performance reflects this debate. While NSE remains immensely profitable, FY26 saw revenue and profit moderate compared to the previous year. The decline does not undermine the quality of the business, but it does remind investors that even dominant market leaders are not immune to cyclical fluctuations in trading activity and market sentiment.

Regulation remains another factor that investors cannot ignore. Exchanges occupy a unique position within the financial ecosystem and therefore operate under intense regulatory oversight. The co-location controversy demonstrated how governance concerns can impact even the most established institutions. Future regulatory changes affecting derivatives trading, market structure or transaction fees could also influence earnings growth.

Competition, though limited, cannot be dismissed either. BSE has demonstrated that smaller rivals can still innovate, gain traction and deliver strong shareholder returns. While NSE remains the market leader, maintaining dominance requires continuous investment in technology, products and market infrastructure.

Ultimately, the investment debate surrounding the IPO comes down to perspective.

Those who view NSE as a mature financial utility may argue that investors are buying stability, predictable cash flows and a dominant market position. For them, the exchange resembles a toll bridge on India’s capital markets, collecting revenue every time investors participate in the system.

Others may see something more dynamic. They may argue that India’s financialisation story is still in its early stages and that NSE remains one of the purest ways to participate in that long-term trend. In their view, the exchange is not merely a beneficiary of current market activity but a platform positioned to capture future growth as India’s capital markets continue to deepen and mature.

The IPO will ultimately force public investors to decide which interpretation is closer to reality. Is NSE a mature cash machine deserving a premium for its stability, or is it still a growth story with its most lucrative years ahead? The answer may determine whether the exchange’s valuation appears expensive today or surprisingly reasonable in hindsight.

)

The Last Bit,

The National Stock Exchange’s IPO is not merely another addition to India’s crowded primary market calendar. It represents the public market debut of an institution that has shaped the way Indians invest, trade and raise capital for more than three decades.

The numbers are undoubtedly impressive: a potential ₹30,000 crore issue, a valuation exceeding ₹5 lakh crore and a business that generates some of the highest margins in corporate India. Yet the true significance of the listing lies elsewhere. NSE is not selling a new technology, launching a consumer brand or promising a disruptive business model. It is offering investors a stake in the infrastructure that underpins India’s financial markets.

After nearly a decade of regulatory hurdles, governance debates and delayed ambitions, the exchange has finally reached the starting line. The market must now decide how much that position is worth.

Whether investors ultimately view NSE as a near-monopoly, a financial utility, a growth story or some combination of all three, one thing is clear: when India’s largest exchange finally lists, it will not just be another IPO. It will be a landmark moment for India’s capital markets themselves.