₹4,619 Crore, 14,105 Dreams, 0 Homes: The TDI Infrastructure Story That India Must Read

How a Delhi Real Estate Giant Allegedly Turned Thousands of Middle-Class Families Into Permanent Tenants in Their Own Story

There is a very particular kind of heartbreak that comes with Indian real estate fraud. It doesn’t announce itself with a bang. It creeps in quietly; first as a delayed possession date, then as an unanswered phone call, then as a notice from the bank about a loan still outstanding on a flat that, years later, still doesn’t have four walls.

That is the story of over 14,000 Indian families who put their faith, and their life savings into TDI Infrastructure Limited.

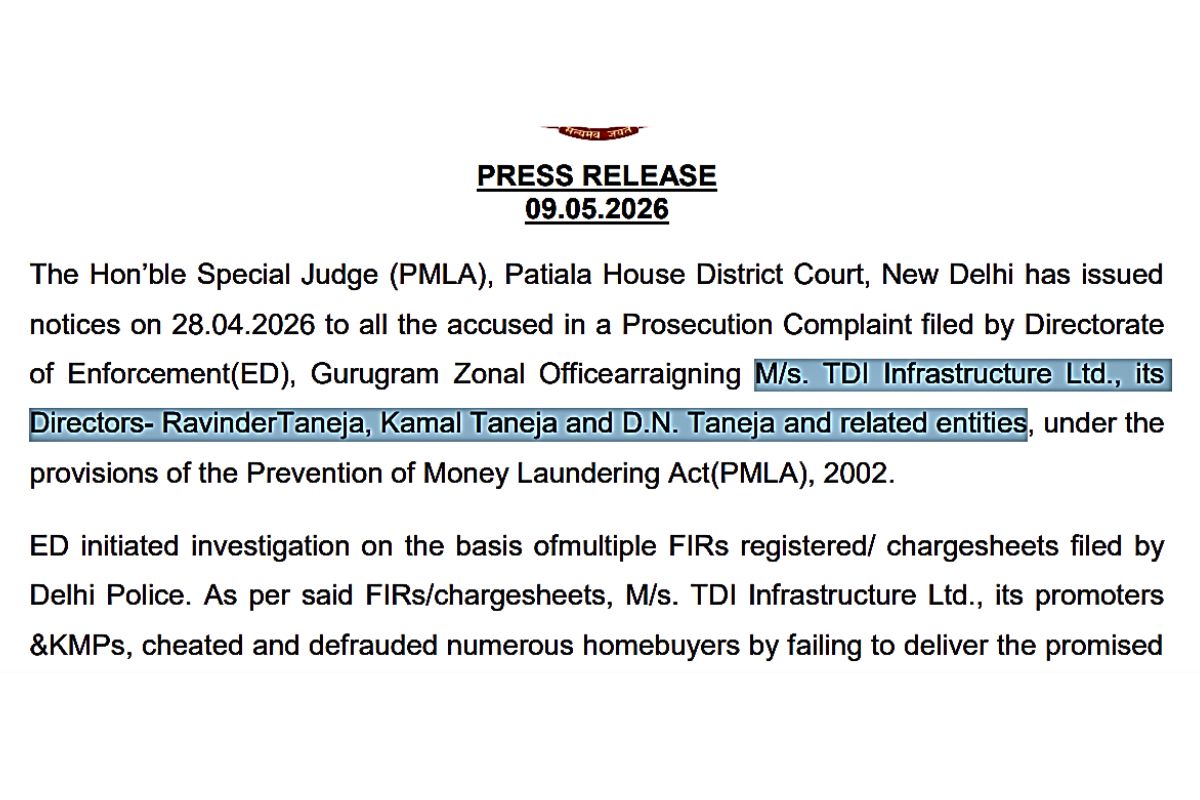

Now, in May 2026, those families finally have what they never truly had before: the law on their side. The Enforcement Directorate has filed a prosecution complaint under the Prevention of Money Laundering Act against TDI Infrastructure Limited, its Managing Director Ravinder Taneja, and fellow directors Kamal Taneja and D.N. Taneja. A Special PMLA Court at Patiala House in New Delhi issued notices to all the accused on April 28, 2026. Total assets attached so far? A staggering ₹349.55 crore.

But here’s the question that keeps gnawing at anyone who looks at this case closely: how does a company collect ₹4,619.43 crore from ordinary Indians — teachers, government employees, middle-class professionals saving up across decades — across 26 projects, over nearly two decades, and still not deliver what it promised?

That question is not just about TDI. It is about India’s real estate sector, its regulators, its banks, its courts, and a system where the buyer is almost always the last person standing when the music stops.

From Sonipat Plots to a National Scandal

TDI Infrastructure Limited, formerly known as Intime Promoters Private Limited, built its reputation during the real estate boom of the mid-2000s. It was a recognisable name in the North Indian property landscape: Punjab, Haryana, the National Capital Region. Flashy project names. Grand promises. Glossy brochures showing modern townships with wide roads, green parks and swimming pools.

Between 2005 and 2014, TDI launched 26 residential and commercial projects, primarily in Kundli, Sonipat, Haryana. These were not obscure, fly-by-night schemes. They were marketed aggressively to buyers who wanted a piece of the great Indian real estate boom — the decade when property investment felt like the safest bet you could make.

The company collected approximately ₹4,619.43 crore as advance booking amounts from 14,105 customers across these projects. Think about that number. Fourteen thousand one hundred and five families. Each one writing a cheque, sometimes the biggest cheque of their lives, based on a promise. But…that promise, in many cases, was never kept.

The Modus Operandi: Money In, Projects Stalled

The Enforcement Directorate’s investigation cuts to the heart of what allegedly happened to all that money. And the findings are damning.

Instead of using the funds collected from buyers to actually build the promised homes and commercial spaces, TDI’s promoters and directors are accused of diverting “substantial quantum” of those funds to subsidiaries, erstwhile subsidiaries and associated entities. The ED’s complaint specifically flags that money was routed out under the head of “advances for purchase of land parcels and other purposes.”

This means money meant to build homes in Sonipat was allegedly being used to buy more land elsewhere, or to service the company’s existing debts, or to make investments that had nothing to do with the buyer who had paid for Flat No. 4B in some half-built tower. The ED also found that customer funds were used to repay existing loans. This is a particularly insidious form of fund diversion — using new money from homebuyers to service debt obligations, a kind of internal “compromising” logic where the building of one project is perpetually deferred to finance the obligations of another.

The result was entirely predictable: construction stalled, possession dates passed, and then years passed. Occupation Certificates for four projects are still pending as of the investigation’s findings. One project, “Park Street”, remains incomplete. In some cases, the ED found delays stretching to an almost incomprehensible 16 to 18 years. Sixteen to eighteen years. Understand the context- a child born in the year a buyer paid for their flat would be old enough to vote before the flat was handed over.

The FIRs: When 26 Police Cases Weren’t Enough to Move the Needle

The ED’s prosecution complaint was triggered not by a sudden discovery, but by an existing mountain of criminal complaints. The investigation is based on multiple FIRs registered and chargesheets filed by Delhi Police and its Economic Offences Wing (EOW), totalling at least 26 cases.

Twenty-six FIRs. Let that sink in. This is not a company that accidentally stumbled into trouble. This is a company that accumulated two dozen police cases over the years, with buyers going to police stations, consumer courts and RERA forums, documenting the same story over and over: money paid, possession not given, promises broken. The Delhi Police’s Economic Offences Wing, which investigates financial crimes, had already filed chargesheets against TDI’s promoters and key managerial personnel.

The ED’s Enforcement Actions: Too Late, But Better Than Never

The Enforcement Directorate has moved on two fronts. First, asset attachment. Second, prosecution.

On attachment, the ED has been building its case progressively. An earlier attachment in 2024 secured assets worth ₹45.49 crore. Then, in March 2026, the agency carried out a fresh provisional attachment of properties worth ₹304.06 crore, including approximately 8.3 acres of land and commercial units in Kamaspur village, Sonipat. Total proceeds of crime attached so far: ₹349.55 crore. The ED has prayed for confiscation of all these assets in its prosecution complaint.

This is not an insignificant number. ₹349.55 crore in attached assets represents a tangible pool of value that, if eventually confiscated and distributed, could provide some measure of compensation to at least a portion of the 14,105 affected buyers.

But here is the uncomfortable arithmetic. The company collected ₹4,619 crore from buyers. The ED has attached assets worth ₹349 crore. That is roughly 7.5 per cent of the alleged proceeds of crime. If those assets are eventually confiscated and somehow distributed among all 14,105 buyers equally, each buyer would receive approximately ₹2.47 lakh, which is a fraction of what most of them invested.

Justice, in other words, is going to be incomplete at best.

The HRERA Angle: When Regulatory Orders Don’t Translate to Action

The Haryana Real Estate Regulatory Authority has been fielding complaints against TDI for years. RERA, which came into force in 2016, gave homebuyers an unprecedented legal tool, which was the ability to file complaints, get orders, and theoretically enforce them against defaulting developers. In practice, the gap between an RERA order and actual recovery has been the story of TDI’s buyers. Orders were passed. Execution proceedings were filed.

The broader problem is structural. RERA authorities can order refunds and impose penalties. But they are not equipped to investigate money laundering, attach assets across multiple jurisdictions or pursue criminal prosecution. That is the ED’s domain. And the ED requires PMLA predicate offences, typically FIRs filed under the Indian Penal Code, before it can act.

What this means in practice is a relay race of justice where the baton gets dropped repeatedly between agencies: consumer courts to RERA to Economic Offences Wing to ED to Special PMLA Courts. Each handoff takes time. Each agency has limitations. And while the institutional relay runs its course, homebuyers continue paying rent, servicing loans, and waiting.

The Human Face of the ₹4,619 Crore Number

Numbers in fraud cases are seductively easy to discuss. ₹4,619 crore. 14,105 buyers. 26 projects. 16–18 year delays. These figures carry weight, but they can also anaesthetise the reader to what they actually represent. They represent a government employee in Rohtak who saved for 15 years, contributed his provident fund towards a down payment, and signed an agreement in 2009 for a flat he thought he’d move into by 2013. It is now 2026.

They represent the retired schoolteacher in Delhi who was persuaded by a relative to invest in a “township plot” in Sonipat as a safe retirement nest egg. The plot exists on paper. Construction never happened. They represent the young couple who stretched their budget, took a home loan, and are now paying both EMIs and rent — because the flat they borrowed money for was never built, but the bank loan is very much real.

Consumer forums, RERA complaint records and media reports are full of individual stories that fit these templates. And there is a particular cruelty in the timing — many of these projects were launched between 2005 and 2014, years when India’s middle class was genuinely optimistic, when real estate felt like a safe investment, when brochures from TDI with professional photography and architect renderings looked like a promise that the country itself was making to them.

The Corporate Governance Question: Where Were the Checks?

Beyond the criminal allegations, the TDI case raises serious questions about corporate governance within large real estate companies, and about the systems that were supposed to prevent exactly this kind of fraud. How does a company collect ₹4,619 crore from buyers without the regulatory ecosystem catching the fund diversion early? The answer involves several overlapping failures.

Banks financed many of these buyers — and in some cases, project financing too. Under the subvention schemes that were common in the 2010s, banks disbursed large portions of loans directly to developers before construction was complete. This gave developers a significant float of money that was, structurally, very easy to divert.

RERA was not yet in existence for most of the period when these projects were launched. When it finally came into force in 2016, it created an escrow account mandate — developers must park 70 per cent of funds in a dedicated account for use only on that specific project. But for TDI’s projects launched between 2005 and 2014, this safeguard arrived years after the damage was done.

The Companies Act requires statutory auditors to flag unusual fund flows. Whether those red flags were raised, and what happened to them if they were, is a question worth asking.

The ED’s investigation is, at this point, the most detailed forensic examination of TDI’s finances that has been made public. That it took multiple FIRs, years of complaints, and a sustained enforcement campaign to get here says something uncomfortable about how the system responds — or doesn’t — to real estate fraud at scale.

What Happens Next: The Road to Justice Is Long

With the prosecution complaint filed and the Special PMLA Court having issued notices, the legal process has entered a new phase. But “a new phase” in Indian criminal justice is not the same as “imminent resolution.”

The accused will file replies. There will be hearings. Applications, adjournments, bail proceedings. The confiscation of attached assets — which is what could actually translate into money for buyers — requires the court to ultimately rule against the accused following a full trial. In complex financial crime cases of this scale, that process can take years. What buyers and legal observers are watching for:

Whether the confiscated assets can be distributed to victims. The PMLA does allow for restitution to victims, but the mechanics of actually distributing money from confiscated proceeds to thousands of individual buyers is complex and rarely swift.

Whether the promoters face arrest and prosecution. Filing a prosecution complaint is different from securing a conviction. The ED has the case before a court; now it must prove its allegations beyond reasonable doubt.

Whether HRERA strengthens enforcement. The Tribune’s reporting indicates that the HRERA order directing action against TDI directors may embolden other buyers to pursue execution proceedings more aggressively — a positive signal that regulatory bodies are beginning to treat these cases with the seriousness they deserve.

Whether this triggers wider sector accountability. TDI is not unique. The NCR is full of developers who collected money between 2005 and 2015 and delivered partial or zero construction. The question is whether sustained enforcement action against TDI — and against others like it — changes the incentive structure enough to deter future fraud.

The Bigger Picture: Real Estate’s Original Sin

TDI Infrastructure is a case study, but it is also a symptom. It represents what happens when a sector grows too fast, is regulated too loosely, and is trusted too naively by buyers who had nowhere else to go with their savings.

India’s housing market in the 2000s was a speculative gold rush. Land prices were rising. New middle-class wealth was flooding in. Developers who were sophisticated at marketing but financially reckless — or fraudulent — could collect enormous sums simply by producing a brochure and a model flat.

In that environment, it was easy to be TDI. Launch 26 projects. Collect ₹4,619 crore. Divert the money. Buy more land. Service old debts. Repeat. And keep repeating, because for years, nobody — not the banks, not the regulators, not the courts — was fast enough or equipped enough to stop the machine. RERA changed some of this. The ED’s PMLA powers changed some of this. But the change came too late for the 14,105 buyers who trusted TDI with their savings.

A Final Word: What Justice Looks Like

When the Patiala House PMLA Court ultimately rules in this case, justice for TDI’s buyers will be measured not by the length of the sentence handed to any director, but by something more immediate and more painful: how much money, if any, comes back to the people who were cheated. For most of them, a partial refund after 15-20 years of waiting is not justice in any full sense of the word. It is, at best, a small acknowledgment that the system eventually noticed their suffering.

The real test for India’s real estate sector is whether “eventually” becomes “early” — whether the regulatory, judicial and enforcement machinery can respond to fraud fast enough to actually protect buyers, rather than simply punishing those who defrauded them years after the fact. Until that changes, the TDI story will not be the last of its kind. It will just be the most recent.