Another Ponzi Scheme In Making. How India’s Most Wanted ‘Alleged’ Hawala Operator Hari Shankar Tibrewal Reinvented Himself As An Investment Guru!

Pump, Dump, and Pontificate: The Brazen Double Life of Hari Shankar Tibrewal

There is a particular kind of audacity that commands respect, even if the emotion you feel as you read about it is closer to jaw-dropping disbelief. It is the audacity of the man who allegedly launders over ₹1,186 crore in illegal betting proceeds through a web of shell companies, manipulates the Indian stock market using a classic pump-and-dump strategy, gets named publicly as a “huge hawala operator” by the Enforcement Directorate in an official press release, gets his shares in 14 listed companies seized by the government, and then, seemingly undisturbed by any of this, proceeds to give media interviews about long-term investment philosophy, market volatility, and responsible capital allocation.

Ladies and gentlemen, meet Hari Shankar Tibrewal- alleged hawala kingpin, absconder, ED-named accused, and, apparently, a thought leader for India’s investment community.

Born and raised in Kolkata, Tibrewal emerged from modest beginnings, cutting his teeth in informal finance during the early 2000s through the gems trading business, building a cross-border remittance network. By the early 2020s, he had relocated to Dubai, a global hub for hawala operations, where he allegedly established entities like Zenith Multi Trading DMCC and Tano Investment Opportunities Fund as fronts for money laundering. A classic rags-to-riches arc, except the “riches” part allegedly had considerably less to do with legitimate entrepreneurship and considerably more to do with one of India’s largest online gambling frauds.

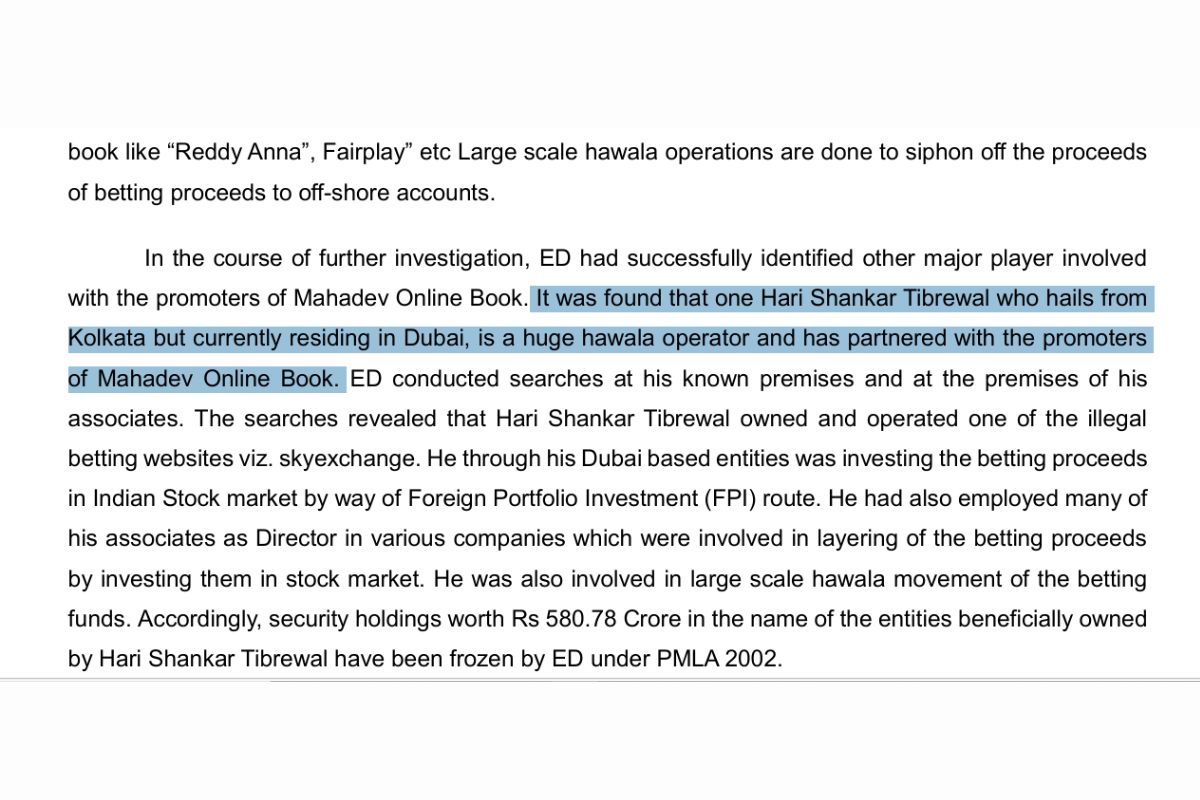

According to the Enforcement Directorate, Tibrewal, who hails from Kolkata but currently resides in Dubai, is a “huge hawala operator” who partnered with the promoters of Mahadev Online Book. The ED conducted searches at his known premises and at the premises of his associates. The searches revealed that Tibrewal owned and operated one of the illegal betting websites, Skyexchange. Through his Dubai-based entities, he invested the betting proceeds in the Indian stock market using the Foreign Portfolio Investment (FPI) route.

This is not speculative journalism. This is the Enforcement Directorate of India, in an official government press release dated March 1, 2024, using the phrase “huge hawala operator” in reference to a person who would, just months later, be appearing on financial media platforms dispensing investment wisdom.

The Mahadev Ecosystem and Its Most Useful Plumber

To understand Tibrewal’s role, one must first understand the Mahadev machine. Proceeds from the Mahadev betting app were funneled through benami (dummy) bank accounts, siphoned to Dubai via hawala operators like Hari Shankar Tibrewal, and “cleaned” through foreign portfolio investments (FPI) and foreign direct investments (FDI). During the COVID-19 lockdown, usage exploded, with daily revenues hitting ₹200–240 crore. The genius of the scheme was not just in the gambling; it was in the laundering, and Tibrewal was allegedly the architect of that laundry.

ED filings describe him as Accused No. 24 in the third chargesheet, crediting him with laundering ₹1,500 crore through stock pumps. He didn’t just move money; he turned dirty betting proceeds into what appeared to be clean, legitimate FPI investment in India’s capital markets. The searches in Kolkata revealed that Tibrewal was also involved in manipulating the stock market in collusion with the promoters of listed companies. Tibrewal, using his immense capital, created temporary fluctuations in share prices, driving them upwards, and then withdrew funds once the prices reached a desirable level.

This is what the financial world calls a “pump-and-dump.” What Tibrewal allegedly ran was a pump-and-dump at an industrial scale, powered by criminal proceeds, and disguised as foreign portfolio investment. Since December 2022, he had invested in over 24 small and mid-cap enterprises, bringing money into India from Dubai through hawala. He pumped up the share price of Cellecor Gadgets Ltd from ₹96 to ₹200 in just a few months.

Tibrewala-owned companies, Zenith Multi Trading DMCC, Ecotek General Trading LLC, and Caterfield Global DMCC, were shareholders in 14 small-cap companies with a combined market capitalisation of ₹21,880 crore. Tibrewala set up Zenith in June 2013, followed five years later by Ecotek in 2018 and Caterfield in 2020, according to registration filings with the Dubai Multi Commodities Centre, the UAE’s free trade zone. The scope and architecture of this enterprise did not spring up overnight, it was methodically built, brick by offshore brick.

The question that should keep every retail investor awake at night is not what Tibrewal did, but what India’s regulatory ecosystem did, or more pointedly, did not do about it.

In March 2024, the ED froze security holdings worth ₹580.78 crore in the name of entities beneficially owned by Tibrewal under the Prevention of Money Laundering Act (PMLA). A week later, on March 8, 2024, the ED found that Tibrewala was “also involved in the manipulation of the stock market in collusion with the promoters of the listed companies.” By February 2025, the ownership of these shares had been formally transferred from Tibrewala-owned entities to the Enforcement Directorate, Raipur.

Meanwhile, SEBI, the Securities and Exchange Board of India, whose explicit mandate is to “protect the interests of investors” and “promote the development of, and regulate the securities market” was initially vocal. SEBI Chairperson Madhabi Puri Buch publicly expressed concern about the surging valuation of small-cap stocks, saying, “It may not be appropriate to allow that froth to keep building. A bubble will burst because, by definition, bubbles burst. So, when they burst, they impact investors adversely, and that’s not a good thing.”

Strong words. Poetic, even. But one must ask, when a single individual allegedly used ₹1,186 crore in gambling money to inflate small-cap stocks through fraudulent FPI routes, where was SEBI’s pre-emptive action? Where was the investigation into the FPI entities like Zenith Multi Trading DMCC and Tano Investment, that were visibly active in dozens of small-cap counters? Front entities of Tibrewala that picked up a stake in all the small and mid-cap companies and even SME-listed companies came under SEBI’s scanner only after the ED raids.

Only after. That is the key phrase. India’s market regulator appears to have discovered the problem not through its own surveillance machinery, but because the ED stumbled upon it while investigating online betting. This is a bit like a bank’s fraud department learning about a forgery operation from a parking warden.

Tibrewal’s evasion tactics perhaps include multiple passports and encrypted apps, that delayed his summons until July 2025, when SEBI flagged his manipulations. July 2025. A full sixteen months after the ED publicly named him a hawala operator. Sixteen months during which India’s capital markets continued to host investors, retail and institutional, who had no idea that some of the small-cap stocks in their portfolios had been inflated by laundered gambling money.

The Dubai Fortress and the Extradition Maze

Why hasn’t Tibrewal simply been arrested? The answer is simultaneously fascinating and infuriating. The India-UAE extradition treaty exists, but requires “dual criminality”, hawala isn’t explicitly illegal in the UAE. The UAE’s Golden Visa shields Tibrewal, and local banks have stonewalled Mutual Legal Assistance (MLA) requests. The arrest of Mahadev’s co-promoter Saurabh Chandrakar in 2024 succeeded via drug charges; Tibrewal’s comparatively “clean” profile has delayed Red Notices.

The ED issued summons in January 2025; Tibrewal’s lawyers cited “lack of evidence” in the Delhi High Court, stalling the warrant process. The CBI’s FIR under PMLA requires a court nod for overseas operations, and SEBI’s parallel probes into entities like Gensol have fragmented the investigative effort.

In essence, the machinery of Indian law enforcement, formidable when it operates on home soil, finds itself in the grip of international procedural quicksand. Tibrewal has reportedly acquired Vanuatu citizenship, a jurisdiction with notoriously limited extradition treaties, adding another layer to an already complex legal shield. The alleged hawala operator, it turns out, has better citizenship diversification than most of his investors.

The Reinvention: Thought Leader, Chairman, and Investment Philosopher

And here is where the story pivots from the merely scandalous to the genuinely surreal.

As all of the above was unfolding, including the ED raids, the share seizures, the legal proceedings, the mounting allegations, Hari Shankar Tibrewal appears to have simultaneously embarked on a remarkable personal rebrand. In February 2026, Zenith Global Limited, described as “a fast-emerging investment and trading company”, announced a strategic global expansion plan, with Tibrewal quoted as saying: “Global markets today are deeply interconnected. Our expansion strategy is focused on disciplined growth, intelligent capital deployment, and building long-term value across geographies.”

“Disciplined growth.” “Intelligent capital deployment.” “Long-term value.”

These are not the words one typically associates with a person whose shares in 14 public companies were confiscated by the Indian government. Yet here we are, asking “is this the same person the ED called a hawala operator?”

A popular media house ran a piece describing Tibrewal as “an intelligent investor and Chairman of Zenith Global Limited, whose approach to growth reflects both market maturity and global ambition,” adding that his emphasis on “intelligent capital allocation” ensures Zenith Global Limited remains “resilient, even amid global volatility.”

One appreciates the irony. A man who allegedly manufactured stock market volatility, through pump-and-dump schemes funded by gambling proceeds, is now publicly positioned as an authority on managing volatility. The audacity is, if nothing else, consistent.

The official Zenith Group website describes Tibrewal as “a strong global leader with a passion to make change happen and the vision and leadership ability to turn under-performing businesses in Asia, Africa and Middle East.” Technically, he did change the performance trajectory of several Indian small-cap stocks. He just also allegedly left retail investors holding worthless paper on the way down.

The broader question raised by this piece is one that uncomfortable fingers at India’s financial media ecosystem. Articles on big news media houses framed Tibrewal and Zenith Global Limited in entirely flattering terms, discussing international expansion, global governance frameworks, and long-term investment philosophy, with no mention of the ED proceedings, the PMLA charges, or the frozen assets. Perhaps, most of these were paid content or press releases, not editorial journalism, and that distinction matters. But it also raises a structural problem: when paid content about an alleged financial fugitive is distributed through the platforms of credible financial news organisations, it acquires a veneer of legitimacy that no press release alone could provide.

Media reports describe Tibrewal as a “huge hawala operator” who manipulated Indian stock markets via FPIs. Yet those very same platforms, or their PR-linked channels, simultaneously carry his self-promotional content. This is not a paradox unique to India, but it is one that demands urgent editorial introspection, asking the question as why ‘the fourth pillar of democracy is shaking!‘

The very few publications that has consistently and aggressively reported on Tibrewal’s activities, Inventiva, has been rewarded for its efforts with a defamation suit. As of January 2026, Tibrewal has filed a defamation suit against Inventiva for publishing articles that echo the very allegations leveled by the ED. Remarkably, he has not made the ED a party to this suit, despite the agency being the first to publicly brand him a hawala operator. This legal strategy, to sue the journalists, not the government agency whose press release you’re objecting to is creative, to say the least. It is also, one suspects, precisely calibrated to intimidate smaller publications without confronting the evidentiary weight of official government findings.

What Comes Next: The Zenith Global Alarm

The concern, expressed in the headline of this article, is not merely historical. Recent ED attachments of ₹388 crore in December 2024 and raids on associated figures like Vikas Garg in November 2025 link Tibrewal to broader ₹40,000 crore benami fraud investigations. Even as recent as 2026, ED attached Rs 1,700 crore Dubai assets in Mahadev betting app case; villas in Burj Khalifa seized. The network is not dormant. It is not wound down. It appears, in several dimensions, to still be operational.

On April 16, 2025, the ED conducted a fresh round of raids targeting 15 locations across India, including Delhi, Mumbai, Jaipur, and Chennai. JTL Industries, a company previously linked to Tibrewal, saw its stock plunge over 16% during this period, while Balu Forge, another company with suspected past associations, fell by 9%.

The pattern is familiar. Stocks linked to the network spike. Then they collapse. Retail investors, the same people SEBI says it exists to protect, absorb the losses. The architects of the scheme, operating behind layers of Dubai-registered shell entities and Mauritius-based FPIs, remain largely untouchable.

Zenith Global Limited’s global expansion plan speaks of “cross-border investment opportunities” and “strategic partnerships worldwide,” framed in the impeccable language of modern corporate governance. One wonders: which markets are next? Which small-cap stocks, which retail investors, in which jurisdiction, will serve as the next vehicle for “intelligent capital deployment”?

The Mahadev Betting App scam is estimated at anywhere between ₹6,000 crore and ₹40,000 crore, depending on which ED filing you reference. The total attachment and freezing in the case as of early documentation had reached ₹1,296 crore, and has grown substantially since. Yet the man allegedly at the financial nerve centre of this operation is at large, publishing press releases, and apparently eager to explore emerging markets in Asia, Africa, and the Middle East.

SEBI issued warnings. The ED froze assets. The CBI filed FIRs. And yet no arrest. No red corner notice that has materialised in custody. No extradition proceedings that have concluded. SEBI’s parallel probes fragment rather than consolidate the investigative effort, creating the bureaucratic equivalent of too many cooks, except the kitchen has allegedly already been robbed.

And then comes the uncomfortable Conclusion…

The Tibrewal affair is, at its core, a stress test of India’s institutional architecture. It tests whether SEBI can be proactive rather than reactive in detecting manipulative FPI activity. It tests whether the ED can successfully prosecute a transnational money laundering operation when the suspect operates from a country with structural barriers to extradition. It tests whether India’s financial media can distinguish between an advertorial and a news article. And it tests whether a person named publicly as a hawala operator by a government agency can simultaneously operate as a publicly celebrated investment guru, and whether anyone in authority notices, let alone acts.

On at least three of those four tests, the results so far are not encouraging.

SEBI Chairperson Madhabi Puri Buch was correct that “a bubble will burst because, by definition, bubbles burst,” and that “when they burst, they impact investors adversely.” The small-cap stocks inflated by Tibrewal’s alleged network did burst, and retail investors did suffer. The question that hangs unanswered in the air like the wherabouts of Tibrewal himself is whether anyone in India’s regulatory framework will ensure that the next bubble is stopped before it bursts, rather than after.

Until then, one supposes, we can look forward to more press releases from Zenith Global Limited about disciplined growth, responsible governance, and long-term value creation. They do make for remarkably soothing reading, provided you don’t look too hard at who’s writing them, or why.