Can Jio And NSE Bring Foreign Capital Back To India? The IPO Test Begins.

India's primary market is about to witness one of its biggest tests in recent years. The long-awaited IPOs of Jio Platforms and the National Stock Exchange are expected to raise nearly Rs 70,000 crore, bringing two of the country's most dominant franchises to public markets. Yet the real significance of these listings extends far beyond their size. Arriving at a time when foreign investors remain cautious, market returns have disappointed and retail enthusiasm has cooled, these IPOs are shaping up as a referendum on confidence in India's growth story.

Most companies come to the stock market seeking visibility, capital or validation. Jio and NSE need none of those things.

Between them, they already touch the lives of hundreds of millions of Indians. Jio transformed India’s telecom industry by making mobile data affordable and now serves more than 500 million subscribers. NSE, meanwhile, has become the backbone of India’s capital markets, handling the overwhelming majority of equity trading in the country and serving as the primary gateway for wealth creation for millions of investors.

What makes these IPOs unique is that they involve businesses that already enjoy dominant positions in sectors protected by high entry barriers. Telecom has effectively evolved into a three-player market where Jio remains the clear leader. Stock exchanges, despite technological disruption elsewhere in finance, continue to operate as natural monopolies or duopolies because of regulation, network effects and liquidity concentration. In both industries, new challengers face enormous hurdles.

Indian investors are also unusually familiar with both brands. Unlike many IPO candidates that spend years convincing investors about their business models, Jio and NSE are already household names. Investors understand what they do, how they make money and why they matter. That familiarity significantly reduces uncertainty, making the upcoming offerings less a bet on an unproven future and more a chance to participate in businesses that have already established their dominance.

For years, investors have waited for an opportunity to own a piece of these companies. Their arrival in the public markets therefore represents more than another fundraising exercise. It marks the opening of two closely guarded corporate fortresses to public ownership. That alone guarantees attention. The bigger question is whether it can also generate the confidence India’s markets currently need.

The Timing Could Not Be More Important

If Jio and NSE were listing during a raging bull market, their success would be almost taken for granted. Instead, they are heading to the market at a moment when investor sentiment is far less enthusiastic.

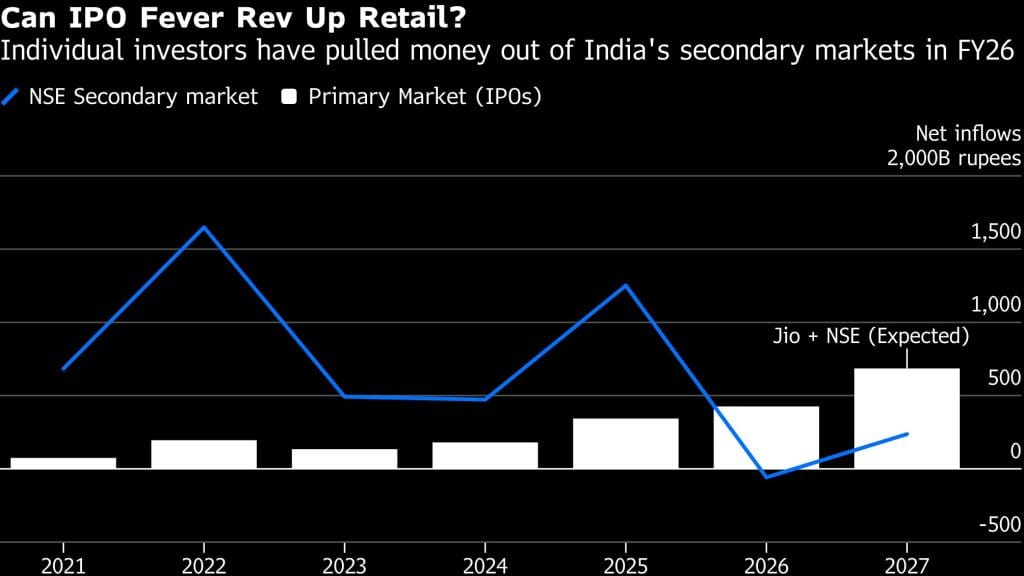

For nearly two years, Indian equities have struggled to deliver the kind of returns investors had grown accustomed to. While markets in the United States, South Korea and Taiwan have been lifted by the artificial intelligence boom, Indian benchmarks have largely moved sideways. Foreign institutional investors have repeatedly pulled money out of Indian stocks, citing rich valuations and better opportunities elsewhere. Even domestic investors, who emerged as the market’s strongest support base during periods of foreign selling, have become increasingly selective.

Recent IPOs have done little to improve sentiment. Several high-profile listings have either delivered muted gains or disappointed investors altogether, reinforcing concerns about aggressive valuations and shrinking upside for retail participants. The result is a market environment where investors are no longer willing to subscribe to an IPO simply because it carries a well-known name.

This is where the contrast with the United States becomes striking. Companies such as OpenAI and Anthropic are preparing for public listings amid extraordinary excitement surrounding artificial intelligence. Investors are actively searching for opportunities to participate in the AI boom, creating an environment where demand often arrives before the prospectus.

Jio and NSE do not enjoy that luxury.

Neither company is riding a speculative theme capable of generating instant investor euphoria. Instead, both are entering the market at a time when investors are demanding stronger fundamentals, realistic valuations and clearer visibility on future growth. Their challenge is not merely to attract capital but to persuade investors that Indian equities still deserve attention in an increasingly competitive global investment landscape.

In that sense, these IPOs are arriving under very different circumstances from many of the world’s headline-grabbing listings. American technology IPOs are benefiting from optimism that already exists. Jio and NSE may have to create optimism where it is currently in short supply.

That is what makes their timing so important. Success would signal that investors remain willing to back India’s strongest franchises despite broader market concerns. Failure, or even a lukewarm response, would raise uncomfortable questions about the depth of confidence in India’s markets at a time when the country is competing aggressively for global capital.

Why The Structure Of The Two IPOs Matters

While Jio and NSE are often spoken about together because of their size and significance, the two offerings are fundamentally different in what they are trying to achieve.

The NSE IPO is expected to be a pure Offer For Sale (OFS), meaning existing shareholders will sell part of their holdings to the public. The exchange itself will not receive any fresh capital from the issue. For investors, ownership will change hands, but the company’s balance sheet will remain largely unaffected.

Jio’s IPO, on the other hand, is expected to include a substantial primary component that will bring fresh money into the business. Part of those proceeds could be used to reduce debt, strengthen the balance sheet and fund future investments across telecom, digital services and emerging technologies.

At first glance, this distinction may appear technical. In reality, it could significantly influence how investors view the two offerings.

When a company raises fresh capital, investors can at least make the argument that their money is helping finance future growth. The proceeds become part of the business, potentially creating additional value over time. An offer-for-sale works differently. The money largely goes to existing shareholders who are monetising their investments.

That does not make the NSE IPO unattractive. Far from it. The exchange remains one of the most profitable and strategically important financial institutions in India. However, it does mean investors are likely to scrutinise valuations even more closely. When no fresh capital is entering the business, the question inevitably becomes: how much of the future growth has already been priced in?

The structure also matters because of market psychology. Jio’s IPO represents new capital flowing into a corporate growth story. The NSE IPO, by contrast, is primarily a liquidity event for existing shareholders. Investors often react differently to these narratives, particularly in uncertain market conditions where capital allocation decisions are becoming more selective.

For both issuers, pricing will therefore be critical. The market has repeatedly shown that investors are willing to reward quality businesses, but only when they believe there is adequate upside left for them. Even the strongest franchise can struggle if investors feel that existing shareholders are extracting maximum value at the expense of new participants.

Ultimately, the success of these IPOs will depend not only on the strength of the businesses but also on whether investors believe they are getting a fair share of the opportunity. In a market that has become increasingly sensitive to valuations, that distinction may prove decisive.

India’s IPO History Offers A Warning

The assumption that large IPOs automatically translate into strong investor returns has repeatedly been challenged by history.

Over the past few years, several marquee companies have entered the stock market amid enormous excitement, only to leave investors disappointed. Paytm’s record-breaking public issue became a lesson of what happens when valuation expectations run ahead of business fundamentals. LIC‘s much-anticipated listing struggled to justify its pricing in the secondary market, while other large offerings have delivered far more modest returns than investors had hoped for.

These experiences have changed investor behaviour.

Retail investors today are far more informed and valuation-conscious than they were a decade ago. Easy access to information, analyst reports and market data means that many investors now look beyond brand recognition and focus on factors such as earnings growth, peer comparisons and future profitability. The days when a famous name alone could guarantee overwhelming enthusiasm are rapidly fading.

This shift places Jio and NSE in an interesting position. On one hand, they possess the kind of brand strength, market leadership and visibility that most companies can only dream of. On the other hand, investors have become increasingly sceptical of paying premium prices simply for the privilege of owning a well-known business.

The lesson from recent IPO history is straightforward: investors do not mind companies making money, but they want some of that opportunity reserved for them as well. When issues are priced too aggressively, the perception quickly emerges that existing shareholders are capturing all the upside while new investors are being asked to assume all the risk.

That is why pricing may ultimately become the most important factor determining the success of both IPOs. Investors are unlikely to question the quality of either business. The debate will instead revolve around valuation and whether the offers leave sufficient room for post-listing gains.

In many ways, Jio and NSE are entering a market that has learned from past mistakes. Investors are no longer chasing every large issue that comes their way. They are asking tougher questions, demanding better value and showing a greater willingness to walk away when pricing appears excessive.

For the issuers, that may be an inconvenience. For the market, however, it is a sign of growing maturity.

Can Jio And NSE Become India’s Next Maruti Moment?

Whenever a landmark IPO approaches, investors inevitably search for historical parallels. In the case of Jio and NSE, the comparison that surfaces most often is Maruti Suzuki’s public issue in 2003.

The timing is not entirely coincidental. Maruti came to the market when investor confidence was still recovering from the aftermath of the dot-com crash and the Ketan Parekh stock market scandal. Retail participation was weak, sentiment was fragile and many investors remained wary of equities. Yet the IPO proved to be a turning point. It attracted widespread participation, restored confidence in the primary market and arrived just before one of the strongest bull runs in Indian market history.

Understandably, some market participants are hoping that Jio and NSE can play a similar role today.

There are certainly similarities. Like Maruti at the time, both companies are dominant players in sectors that ordinary Indians understand well. Their businesses are not dependent on complicated technologies or speculative future promises. Investors know what they do, why they matter and how deeply they are embedded in India’s economy.

Yet the differences are arguably more important than the similarities.

The India of 2026 is not the India of 2003. Back then, equity ownership was relatively limited and the market still had significant room to attract first-time investors. Today, domestic participation is already at record levels. Millions of investors entered the market during the post-pandemic boom, mutual fund inflows have become a structural feature of the financial system and equities are no longer viewed as a niche asset class.

As a result, the challenge facing Jio and NSE is fundamentally different. Maruti helped bring Indian investors into the market. Jio and NSE are entering a market where investors are already present but are becoming more cautious about where they deploy their money.

There is also the broader economic backdrop to consider. The early 2000s coincided with a period of accelerating economic growth, rising corporate earnings and increasing optimism about India’s future. Today’s environment is more complex. Global growth remains uneven, geopolitical tensions continue to influence capital flows and investors have a wider range of opportunities across international markets.

That does not mean Jio and NSE cannot have a positive impact. Their listings could improve sentiment, deepen market participation and provide investors with exposure to two of India’s strongest franchises. But expecting them to trigger a Maruti-style transformation may be unrealistic.

The circumstances are different, the market is different and the investor is different. If Maruti’s IPO was about introducing investors to the possibilities of Indian equities, Jio and NSE are more likely to test whether those investors still believe the best opportunities lie ahead.

The Real Audience Is Not Retail Investors

Much of the discussion surrounding the Jio and NSE IPOs has focused on retail participation, subscription numbers and listing-day gains. While those metrics will dominate headlines, they may ultimately miss the bigger picture.

The real audience for these IPOs is global capital.

Over the past two years, foreign investors have become increasingly selective about India. Concerns around elevated valuations, slowing earnings growth and better opportunities elsewhere have resulted in periods of sustained outflows. Even investors who remain positive on India’s long-term prospects have become more cautious about paying a premium simply because a company carries the India label.

This is where Jio and NSE occupy a unique position.

Unlike many Indian companies that are assessed primarily as part of broader emerging market allocations, both businesses have characteristics that allow them to be evaluated on their own merits. Jio dominates one of the world’s largest telecom markets and sits at the centre of India’s digital economy. NSE effectively controls the infrastructure through which India’s capital markets operate. Both enjoy powerful competitive advantages that would be difficult to replicate.

That is why the success of these IPOs cannot be measured solely by oversubscription figures. Retail investors have historically shown an ability to support India’s markets during periods of uncertainty. The more important question is whether international investors see enough value to commit meaningful capital.

A strong response would send a powerful signal that India’s investment case remains intact despite recent concerns over valuations and market performance. It would suggest that investors are still willing to back dominant Indian franchises with long growth runways and strong competitive moats.

A weaker response, however, could reinforce fears that India is struggling to justify the premium valuations that have become a defining feature of its equity markets. That would have implications extending far beyond these two listings, influencing how global investors view future Indian IPOs and the broader market itself.

The Last Bit,

Jio and NSE are almost certain to attract attention. They are household names, dominant businesses and among the most anticipated IPOs India has seen in years. But subscription numbers alone will not determine whether these offerings are successful.

The larger question is whether they can achieve something the market currently needs: renewed confidence. Confidence among retail investors that valuations remain reasonable. Confidence among institutions that India’s growth story remains compelling. And confidence among foreign investors that Indian equities still deserve a place in global portfolios.

Two decades ago, Maruti’s IPO helped bring domestic investors back to the market. Jio and NSE face a different challenge. Their task is not to introduce investors to Indian equities but to remind them why they believed in them in the first place.

That is what makes these IPOs more than corporate fundraising exercises. They are a test of whether India can still inspire the kind of conviction that turns market participation into long-term investment.