Is “the big default” finally happening? Several dozen nations are heading toward economic disaster in 2022.

Is “the big default” finally happening? Several dozen nations are heading toward economic disaster in 2022.

A quarter-trillion dollar mountain of distressed debt risks are triggering an unprecedented wave of defaults in developing countries.

Due to unmanageable food and fuel prices that sparked protests and political unrest, Sri Lanka was the first to stop paying its foreign bondholders this year. After being sanctioned because of the conflict in Ukraine, Russia followed in June.

Currently, attention is being paid to Pakistan, El Salvador, Ghana, Egypt, Tunisia, and other countries that Bloomberg Economics considers, being at risk of default.

Numerous developing countries are currently experiencing a debt crisis, as seen by measures like collapsing currencies, 1,000 basis point bond spreads, and depleted foreign exchange reserves. Rising borrowing costs, inflation, and debt all contribute to worries about an economic collapse, which is why Belarus is on the edge of default, at least a dozen other nations are in danger of bankruptcy, and countries like Lebanon, Sri Lanka, Russia, Suriname, and Zambia are already in default.

The overall cost is astounding. Analysts use a pain threshold of 1,000 basis points in bond spreads to determine that $400 billion in debt is at risk.

With about $150 billion, Argentina is the largest, followed by Egypt and Ecuador, each with between $40 and $45 billion. However, these are the nations that remain susceptible. Crisis veterans feel that many can still avoid default, especially if global markets stabilise and the IMF moves in to offer aid.

There won’t be any significant debt for the Argentine government to pay off until 2024. However, the weight will only increase from there, and there are growing worries that Argentina’s tenacious vice president Cristina Fernandez de Kirchner may try to force the country to violate its deal with the International Monetary Fund. The $1.2 billion bond payments from Ukraine are due in September. Reserves and aid funds may enable Kyiv to make payments. However, in light of state-run Naftogaz’s request for a two-year debt freeze this week, investors think the government will do the same.

Some concerns are getting, or at least adhering to, an IMF programme in Tunisia may be challenging due to President Kais Saied’s efforts to maintain his hold on power and the country’s powerful and recalcitrant labour union. It has one of the world’s highest public sector wage bills and a budget deficit of about 10%. Furious borrowing has caused Ghana’s debt to GDP ratio to increase to almost 85%. It has already used more than half of its tax revenue to pay off loan interest, and this year, the value of its currency, the cedi, has decreased by almost a quarter. Inflation is also getting very close to 30 per cent.

Egypt has had one of the most significant outflows of foreign capital this year, JPMorgan estimates, totalling $11 billion, with a debt-to-GDP ratio of around 95%. Kenya invests a bit over 30% of its income in interest. This scenario is significant because it now has no access to the capital markets and has debts with a 2024 maturity date worth more than $500 million. Ethiopia will be among the first countries to benefit from debt relief under the G20 Common Framework plan. Although the protracted civil war in the nation has hindered development, it is nonetheless making interest payments on its sole $1 billion international bond.

Countries having the most significant risk of default is 2022

countries having the most excellent chance of default is 2022

Sri Lanka, a country in South Asia, made its first financial default in May 2022. The country’s government was allowed a 30-day grace period to pay the unpaid interest of $78 million but ultimately did not.

This affects Sri Lanka’s economic destiny and also raises the crucial question of which other nations face default risk.

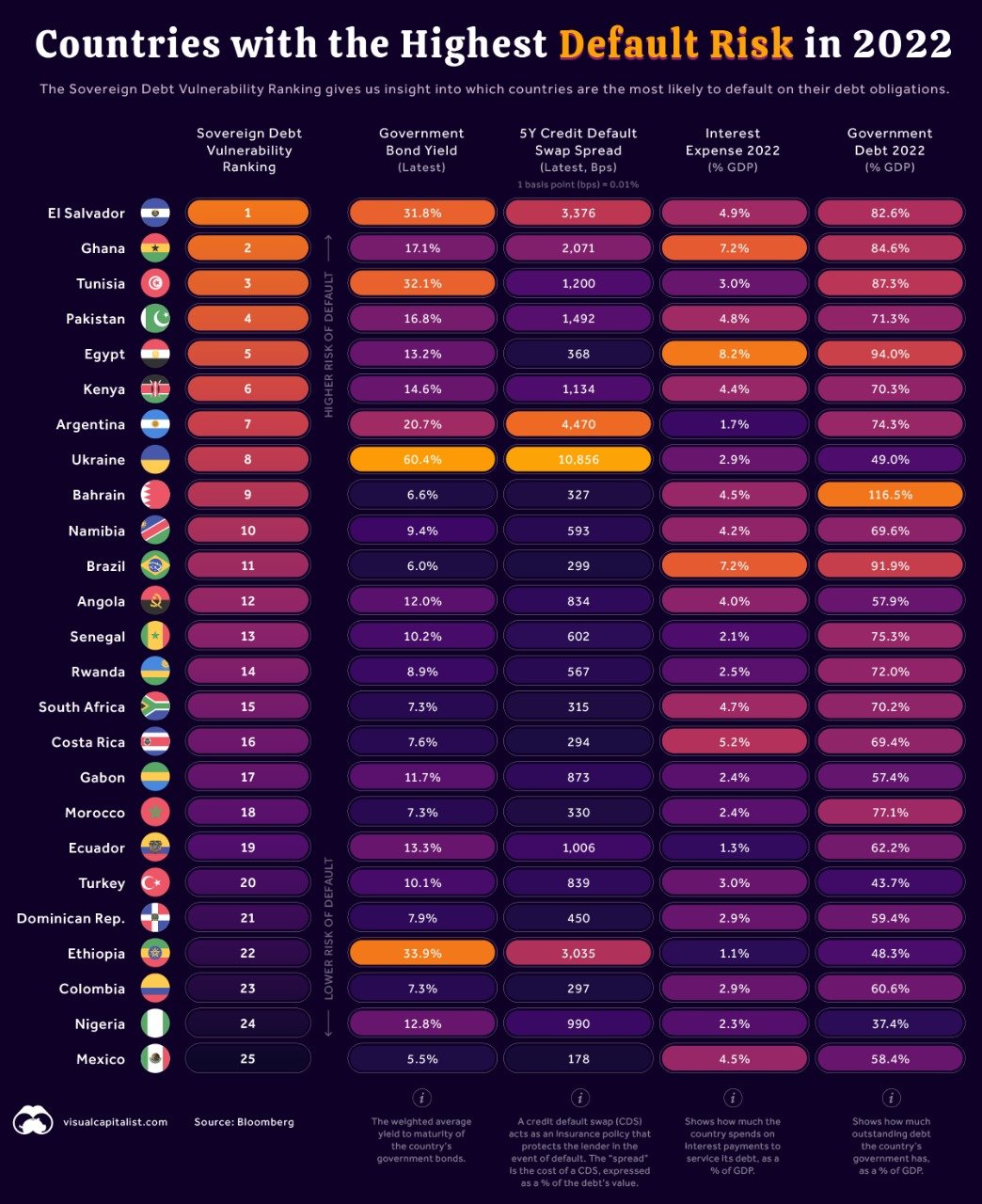

The ranking of sovereign debt vulnerability

Bloomberg’s Sovereign Debt Vulnerability Ranking comprehensively assesses a nation’s default risk. It is founded on four fundamental metrics:

- Government bond yields (the country’s dollar bonds’ weighted average yield)

- Credit default swap (CDS) spread over five years

- Interest costs as a share of GDP

- Amount of government debt concerning GDP

- Let’s use El Salvador and Ukraine as examples to comprehend this ranking better.

Why are the yields on Ukraine’s bonds so high?

Because of its ongoing confrontation with Russia, Ukraine faces a substantial default risk. Consider a situation in which Russia was to take over the nation to see why. The current debt commitments of Ukraine might never be paid off if this occurred.

Ukrainian government bonds have fallen to around 30 cents on the dollar due to a sell-off sparked by that scenario. This implies that a bond with a $100 face value might be obtained for $30.

The average yield on these bonds has increased to a very high 60.4 per cent because crops grow in the opposite direction of price. A 10-year government bond issued by the United States now has a yield of 2.9 per cent.

What are the CDS Spread?

A derivative (financial contract) called a credit default swap (CDS) offers insurance to a lender in the event of a default. Between the lender (investors) and borrower, the seller of the CDS is a middleman (in this case, governments).

The buyer of a CDS pays the price known as the spread, measured in basis points, in exchange for coverage (bps). If a CDS has a distance of 300 basis points (3%), the investor must pay $3 annually to insure $100 in debt.

An investor would have to fork up $108.56 annually to insure $100 in debt, based on Ukraine’s 5-year CDS spread of 10,856 bps (108.56 per cent).

This indicates minimal market confidence in Ukraine’s capacity to avert default.

Why is El Salvador in a higher position?

El Salvador is ranked higher than Ukraine despite having lower values for the two categories mentioned above due to its higher interest costs and overall public debt.

The information mentioned above indicates that El Salvador pays an annual interest rate of 4.9 per cent of its GDP, which is considerable. Once more, in comparison to the U.S., federal interest expenses in that country in 2020 came to 1.6 per cent of GDP.

El Salvador’s total unpaid debts equal 82.6 per cent of its GDP. Although it is high by modern standards, this is considered high by historical standards.

The nation’s $800 million sovereign bond matures in January 2023. Thus this is the following date to keep an eye on.

Recent research shows El Salvador’s default would have a severe, albeit brief, detrimental impact.

Bitcoin is yet another popular topic in El Salvador.

El Salvador became the first nation in the world to accept bitcoin as legal money in September 2021. This indicates that using Bitcoin to pay off debts and fulfil other obligations is permitted by law.

Early in 2022, the International Monetary Fund (IMF) opposed this choice and urged the nation to rescind its legal tender status. These cautions were reasonable retrospectively, as Bitcoin’s value has decreased by 56 per cent this year.

Although this has nothing to do with El Salvador’s likelihood of default, it does provide some potential respite. For instance, major crypto companies would be eager to help the state maintain the idea of “nation-state bitcoin acceptance.”

Pakistan is on the verge of loan default after Sri Lanka.

Fitch Ratings have listed seventeen nations as potentially nearing default.

According to international rating agencies, Pakistan could be the next group of nations to experience difficulties after Sri Lanka and Zambia defaulted on their sovereign deposits and were left without any foreign reserves.

According to Bloomberg, which anticipates a cascade of defaults among emerging nations due to rising energy and food prices and global interest rates, Turkey, Egypt, Tunisia, Ethiopia, Pakistan, Ghana, and El Salvador are in immediate danger of not being able to repay debts.

On the other hand, Fitch Ratings has identified 17 nations, including Pakistan, that may be close to default. The U.S. Government has prohibited organisations from collecting money from Moscow, so even though Russia has the money, it has been unable to pay its foreign creditors. As a result, Russia has been added to the list.

The other nations on the verge of a sovereign debt default are Pakistan, Lebanon, Tunisia, Ghana, Ethiopia, Ukraine, Tajikistan, El Salvador, Suriname, Ecuador, Belize, Argentina, Russia, Belarus, and Venezuela, however Sri Lanka and Zambia are the two most prominent examples.

Argentina

The world leader in sovereign default appears certain to increase its total. In the illicit market, the peso currently trades at a near 50% discount, reserves are at an all-time low, and bonds are now worth 20 cents on the dollar, less than half of their post-2020 debt restructuring value.

Even while there won’t be much debt for the government to pay off until 2024, it will start to accumulate, and there are growing concerns that strong vice president Cristina Fernandez de Kirchner may try to persuade Argentina to violate its pledge to the International Monetary Fund.

Tunisia

Africa has several nations applying to the IMF, but Tunisia appears to be among the most vulnerable.

The nation’s strong and unyielding labour union and President Kais Saied’s efforts to maintain his hold on power have contributed to the country’s budget deficit, which is about 10%, making it one of the highest public sector salary bills in the world. There are concerns that obtaining or maintaining an IMF programme may be difficult.

The premium investors’ demand to purchase Tunisian debt over U.S. bonds has increased to almost 2,800 basis points, placing the country alongside El Salvador and Ukraine as Morgan Stanley’s top three most likely defaulters.

According to Marouan Abbasi, the head of Tunisia’s central bank, an agreement with the IMF is now necessary.

Ghana

Furious borrowing has caused Ghana’s debt to GDP ratio to increase to almost 85%. Its currency, the cedi, has lost approximately a quarter of its value this year, and it has already spent more than half of its tax revenue on debt interest payments. Inflation is also getting very close to 30 percent.

Egypt

Egypt has had one of the largest outflows of foreign capital this year, JPMorgan estimates, totaling around $11 billion, with a debt-to-GDP ratio of about 95%.

Egypt is expected to have to pay $100 billion in hard currency debt over the next five years, including a sizable $3.3 billion bond, in 2024, according to to fund management company FIM Partners.

Cairo reduced the pound’s value by 15% and requested assistance from the IMF in March. Still, bond spreads have since risen to over 1,200 basis points, and credit default swaps (CDS), an instrument used by investors to manage risk, now factor in a 55 per cent possibility that Cairo will default on a payment.

However, according to Francesc Balcells, CIO of E.M. debt at FIM Partners, about half of the $100 billion Egypt must pay by 2027 would go to the IMF or bilateral agreements, mainly in the Gulf. Egypt “should be able to pay under normal circumstances,” said Balcells.

Kenya

Kenya spends almost 30% of its income on interest payments. This scenario is significant because it now has no access to the capital markets and has debts with a 2024 maturity date worth more than $500 million.

“These nations are the most susceptible solely because of the quantity of debt coming due relative to reserves, and the fiscal issues in terms of stabilising debt burdens,” said Moody’s David Rogovic about Kenya, Egypt, Tunisia, and Ghana.

Ethiopia

Addis Abeba is one of the first nations to receive debt relief under the G20 Common Framework programme. Although the protracted civil war in the nation has hindered development, it is nonetheless making interest payments on its sole $1 billion international bond.

South America

The possibility of making bitcoin legal tender was essentially eliminated. Trust levels have plummeted to the extent that an $800 million bond with a six-month maturity trades at a 30% discount and longer-term bonds at a 70% discount.

Pakistan

This week, Pakistan reached an important IMF agreement. The discovery could not have come at a better moment, as rising energy import costs are putting the nation in danger of experiencing a balance of payments crisis.

The country’s foreign exchange reserves have dwindled to only $9.8 billion, just enough for five weeks’ worth of imports. To record lows, the Pakistani rupee has declined. Since the incoming administration spends 40% of its revenue on interest payments, spending reductions are now urgently required.

Belarus

After standing beside Moscow in the Ukraine campaign, Belarus is now subject to the same harsh penalties that forced Russia into default last month.

Ecuador

The Latin American nation only went into default two years ago, but violent protests and an effort to remove President Guillermo Lasso have plunged it into turmoil.

It has an immense debt, and JPMorgan has increased its prediction for the public sector fiscal deficit to 2.4% of GDP this year and 2.1% of GDP next year because the government is subsidizing food and fuel. Spreads on bonds have surpassed 1,500 bps.

Nigeria

Bond spreads are just over 1,000 bps, but Nigeria’s reserves, which have been gradually increasing since June, should comfortably meet the country’s next $500 million bond payment in a year. Nevertheless, it spends nearly 30% of taxable income on debt interest.

Brett Diment, head of emerging market debt at investment firm abrdn, stated, “I think the market is overpricing a lot of these risks.”