Why Is The Government Not Taking Any Action On HDFC And Kotak Bank For Forming An Illegal Syndicate With Builders For Loan Fraud?

In India’s rapidly developing urban life, buying a home is referred to as the ultimate middle-class benchmark. For the majority of homebuyers, however, and especially those who had taken advantage of subvention schemes, made possible by big banks like HDFC and Kotak in partnership with builders, that dream has turned into a nightmare. Reports and growing numbers of victimized homebuyers point towards an extremely sophisticated and cunning nexus between bank and builders; a syndicate carefully planned to profit at the expense of common citizens. The most mystifying question that arises is:

Why Is The Government Not Taking Any Action On HDFC And Kotak Bank For Forming An Illegal Syndicate With Builders For Loan Fraud?

The Anatomy of the Scam – How It Works?

The way this works is both nice and harmful. Builders work with banks to provide “no EMI until possession” plans, which are also called subvention plans. With these plans, banks give the entire home loan amount to builders right away, even before important construction steps are completed. In exchange, builders agree to pay the EMIs until the homebuyer moves in.

This arrangement is just fine, until it is not. When developers default on EMI payments, the onus inexplicably shifts to the unsuspecting buyer, who begins to receive recovery calls, penalty notices, and credit score downgrades from the same banks that had guaranteed a no-EMI term. Even after paying their dues in advance and with no possession materializing, homebuyers are financially throttled.

A number of High Court and Supreme Court rulings have laid the basis for consumer protection under subvention schemes today:

Ashish Tiwari v. Union Bank of India (Delhi High Court): The Court observed that banks disbursed loans without determining the speed of construction, which was contrary to RBI guidelines and was at the expense of homebuyers.

Satbir Singh & Anr. v. Raheja Developers Ltd. & Anr.: The court ruled that the conditions for lending money were a part of a lawful agreement, but the default by the builders in delivering possession provided a reason to act against the builder and perhaps the financier.

These instances indicate that consumers do not have to suffer due to errors by institutions or malpractices by developers.

The Banks’ Role: Beyond Being a Silent Partner

Banks like HDFC and Kotak have been accused of actively facilitating these arrangements without due diligence. In many cases, loan disbursements occurred despite clear violations of RBI lending norms, such as failure to ensure stage-wise construction-linked payments. What makes this even more disturbing is that many of these housing projects had no approval from local development authorities or were severely delayed or even abandoned.

Take the example of Maharashtra’s famous Ambernath scam, where it was exposed that a shocking nexus of fraud has been caught involving builders, architects, cooperative registras, banks, and regulators. Over 3000+ homebuyers have been defrauded through forged certificates, illegal construction, and negligence by authorities.

The banks, such as HDFC and Kotak, are blamed for extending loans without verifying them, thus aggravating the crisis. This indicates major issues in the system. Of all the banks, HDFC and Kotak are turning into major players in the controversy. So, why would reputed financial institutions compromise their reputation? The reason might be greed, a desire to make money overnight, and a robust system of mutual gains with influential real estate firms.

Regulatory Failure or Willful Blindness?

RBI and National Housing Bank (NHB) have issued guidelines against subvention schemes for decades. But these have never been enforced or not enforced at all. There has been no punishment, audit, or cancellation of licenses that has motivated banks to continue distributing such risky products. The SEBI, which oversees listed companies and safeguards investors, has also not intervened despite numerous complaints from angry homebuyers and associations of investors.

It all revolves around a particular scheme called subvention scheme- which was deliberately formed and used to harass the homebuyers. This divine scheme, known as ‘Subvention scheme’ can be seen with tags like ‘No EMI till possession’.

This major plot in this subvention scheme is that the buyer will start to pay the EMI only after ‘possession’. Now, this intentional ‘delay in project’ or ‘delay in possession’ is the centre of the universe. Since it was a pre-planned game by the builder-bank nexus, the innocent homebuyers never knew that they would never get their homes. This is because, even after knowing that the documents are forged, the banks have disbursed huge amounts of loans to builders, in some cases without the foundation of any single block.

Most of the developers introduced subvention plans between 2015 and 2019 in the city to counter a real estate market slowdown. They partnered with banks to offer interest-free loan facility up to possession, levying the buyers with a little extra price for the apartments. And the banks always had the assurance that there will always be a possession delay, and thus the whole liability of EMIs will be transferred to the homebuyers. The question remains how despite the Reserve Bank of India disallowing such creative home loan plans, subvention plans persisted?

Consider the Ambernath scheme. Despite complaining to MahaRERA on May 1, 2024, not even a single hearing or step has been taken. This inaction is a gross failure of the regulations that are in place to guard homebuyers.

Political Influence and Lobbying Power

One cannot rule out the role of political lobbying in shielding these financial behemoths. HDFC and Kotak are no ordinary banks; they are deeply connected with India’s corporate and political life. For instance, imagine the amount of electoral bonds Kotak had purcahsed. With board members sitting on government committees, industry task forces, and powerful business councils, these entities have a degree of immunity that discourages any serious government action. Further, the real estate industry, a significant contributor to GDP and jobs, is closely linked to political funding, particularly at the state level. Action against key players in this sector would risk disturbing a powerful nexus that feeds political campaigns.

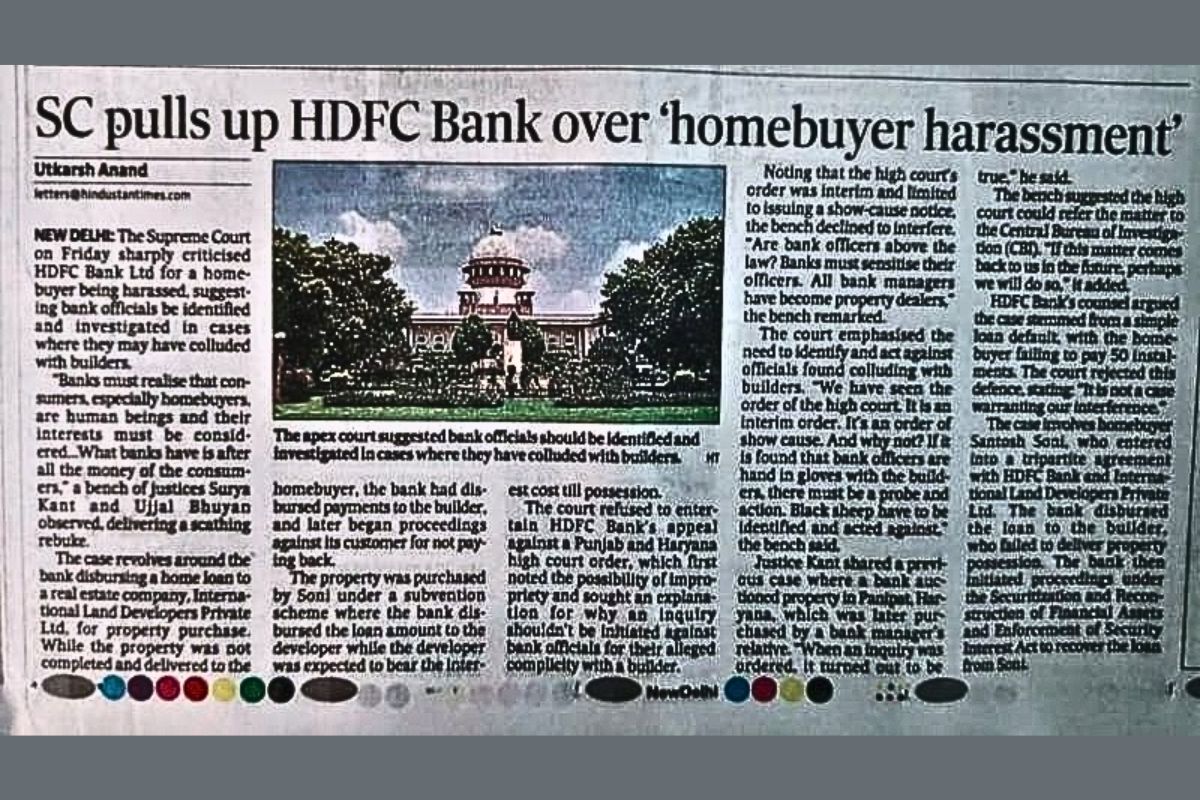

In March 2025, the Supreme Court recognised the troubles and rebuked builders and banks for a nexus in the name of subvention. It also ordered a CBI to probe. But the situation was never easy. Senior Advocate Dr Abhishek Manu Singhvi, appearing for one of the financers, contended that a few parties had acted bonafide and the financer was not at fault if a particular builder went into Corporate Insolvency Resolution Process. However, Justice Kant, who was hearing the case was quick to add that the financiers were to be blamed for releasing more than half of the funds despite knowing that “not a brick had been laid” at the site.

This indicates that banks such as HDFC and Kotak had intentionally created a nexus with the builders and released them massive amounts of loans even after being aware that the documents are fake, the banks have released massive amounts of loans to builders, in some instances without the foundation of any individual block. Thus, this is to inquire ‘why the government is not doing anything against HDFC and Kotak for creating an illegal syndicate with the builders and intimidating homebuyers like anything?

The penalty for regular homebuyers is very harsh. Many families have lost their savings, taken on debt, and experienced tarnished credit ratings. Some have even faced mental illnesses, marital disputes, and court cases, but without homes. Obtaining legal help is time-consuming and difficult. Real Estate Regulatory Authorities (RERAs) were put in place to protect consumers, but they have limited resources, no regulations to enforce, and often take the side of politically influential developers. Consumer courts are congested and ill-equipped to deal with complex cases of financial fraud committed by large corporations.

The effect of this harassment is way beyond calculations. A person X from Pune applied for Credit Card and his credit card was rejected due to low CIBIL Score. He was totally lost as he never defaulted on any of the payments. In his CIBIL report, payment default was observed on Home Loan EMI’s. When thoroughly checked, he said that he bought joint property with his father from a builder under the Subvention Scheme.

In this scheme, the builder was supposed to pay EMI for 48 months but he started defaulting on EMI’s after the 8th month. This is the biggest drawback of the Subvention Scheme. It is very difficult to ensure whether the builder is paying EMI on time or not. Homebuyers’ understanding of “NO EMI for a certain number of Months” is that there is No EMI payment to Bank / HFC. Fact of the matter is that the builder has to pay Pre-EMI on behalf of the buyer. By handing over the key of your CIBIL Score to the builder, person X has taken a huge credit risk.

Why There is a Deafening Silence from the Government?

In a democratic nation, the government is meant to safeguard its people from exploitation. But no proper inquiry has been conducted, no joint parliamentary panels have been formed, and no serious attempt has been made to punish the culprits. Why is there so much hullabaloo? It may be attributed to slow government processes by some, but the reality is worse. It has too much to lose, and large financial institutions tend to play it safe by having excellent rapport with regulators, politicians, and media firms. It seems that the government doesn’t care about common people the most. It only forgets about them when it requires their votes or their money.

At the end…

The suspected connections between builders and banks is not just a housing scam. It’s an indication of how far corruption seeps into the Indian economy. It’s an indication of how effortlessly companies are able to take advantage of loopholes in law, ignore regulations, and exploit the weak, and the government does nothing. If the government keeps ignoring this, it is logical to assume that it won’t just lose the faith in its banks but also the trust that it has with its people. Action must be rapid, clear, and firm. Because ultimately, it is not just about houses lost but also trust lost. And once trust is lost, it takes a much longer time to rebuild than any concrete structure.