Zepto/Swiggy Eyeing For IPO: Is The Quick Commerce Segment Really The ‘Apple Of The Eye’ Or Just ‘Pulling The Wool Over The Eye’?

As per sources, quick-commerce firm Zepto, which raised nearly $1 billion from private investors over the past two months, has begun active discussions with top Wall Street bankers, including Morgan Stanley and Goldman Sachs, for an IPO. The Mumbai-based startup is also thought to be talking to domestic investment banks about the potential listing of shares by August next year. Swiggy, the parent of Zepto’s rival Instamart, is also readying to hit the public market later this year with a $1.25 billion IPO. Its other more significant competitor, Blinkit, is owned by Zomato, a listed company since 2021.

The buzzing quick commerce space also continues to see new entrants as more and more companies try to take a piece of the pie. E-commerce majors Amazon and Flipkart and mobility major Ola are planning to enter the segment even as existing players like Zomato-owned Blinkit, Zepto, and Swiggy’s Instamart continue to strengthen their play. The market also witnessed the entry of the nation’s big players like Reliance Retail’s Jiomart and Tata’s Bigbasket.

So, what’s driving the quick commerce segment to become everyone’s apple’s eye?

Quick commerce, once viewed with scepticism in India, has recently demonstrated its value as startups like Blinkit begin to report encouraging results. Unlike worldwide markets, where the rapid growth of quick commerce has slowed due to consolidations and shutdowns, it continues to prosper in India.

The golden wave of Quick commerce.

Starting with the market leader Zomato, the parent of Blinkit- With an enterprise value of $15.4 billion, quick commerce platform Blinkit is contributing a higher share to Zomato’s valuation than the Gurugram-based company’s mainstay food delivery business. On August 1, Zomato declared its quarterly results. Blinkit is now on a ₹10k cr annual revenue run rate, growing at 150% annually.

At ₹6k cr, Swiggy’s Instamart and Zepto at ₹7.5k cr are also of significant scale. The former is on the verge of an IPO, looking for a valuation of between $12 bn and $15 bn. Zepto is already flying high with its high funding and super valuations. Therefore, what started as a somewhat gimmicky business is now becoming a tsunami threatening to engulf conventional e-commerce platforms such as Amazon and Flipkart.

What’s driving these quick commerce companies to drive high?

A consumer behaviour of instant gratification.

The first pillar of this change is the human imagination. While the rest of the world was grappling with the issues of next-day delivery, a creative mind dreamed of a ‘10-minute’ delivery model for consumer items as the way ahead. The move was even more exaggerated by the onset of deadly COVID that thrashed everyone behind doors, making them dependent on delivery by someone.

Fundamental elements were copied from the leading competitors’ playbooks, such as Amazon’s ease and quickness. Amazon Prime’s value proposition, which included same-day or next-day deliveries, had already conditioned buyers to expect instant gratification. Quick commerce firms shifted from quick to instant gratification, shortening the desire-to-consumption cycle to 10 minutes. And hence, this is obviously where the lure of instant satisfaction debuts.

Collaborations lead to increased transactions.

Though some players deliver on specific niches, the active players have built their infrastructures so that they can deliver anything from groceries to apparel to electronics and whatnot. Who would have thought that consumers would require beauty goods or apparel delivered to their homes within 10 minutes till a few years ago? But here we are. According to the community-engagement site LocalCircles, Indian customers have spent more money on sports gear, cosmetics, and sexual wellness through quick-commerce platforms in the previous one year, in addition to groceries.

Electronics, particularly smartphones, are the main sales category for e-commerce platforms like Amazon and Flipkart, accounting for about 40% of total business, according to industry estimates. As a result, it’s no surprise that companies like Blinkit, BigBasket, Zepto, and Swiggy Instamart are now vying for a larger portion of the consumer budget by entering the electronics market, selling anything from smartphones to televisions to refrigerators.

In July 2024, it was reported that Blinkit and Instamart were in advanced talks with leading apparel and shoe manufacturers like Arvind Fashions, Fabindia, Woodland and Puma to sell their products to capitalise on a large section of consumers in the top 15 cities moving to buy products other than groceries through quick commerce. These firms want to capitalise on the rising fashion market, which is presently the second-largest selling category in India’s e-commerce industry behind electronics and smartphones, accounting for 20-25% of sales. Woodland India chief Harkirat Singh stated that consumers are increasingly demanding instant delivery and that quick commerce has the potential to be significant in fashion, with e-commerce currently accounting for 30% of the company’s sales.

Furthermore, logistics companies are joining the bandwagon. Ecommerce and hyperlocal logistics companies, like Warburg Pincus-backed Ecom Express, Flipkart-backed Shadowfax, and Tiger Global-backed Loadshare, have all gotten on the quick delivery bandwagon in an effort to get a share of rising order volumes. It was reported in June that Delhivery and Xpressbees intended to enter the quick commerce market.

According to recent reports, quick commerce companies are partnering for the first time with fast-moving consumer goods (FMCG) giants such as Parle, Mondelez, and ITC on deals, special packs, and promotional banners for the festive season. These Diwali promotions come as quick commerce has emerged as most quick commerce companies had intended to rapidly expand into high-value electronic products such as smartphones and television sets, as well as fashion, by the festive season, but those partnerships are still being negotiated, so the platforms have decided to shift their focus to festive purchases and gifting.

The onset of the younger generation.

According to the survey, Indian Gen Zs (born between 1996 and 2010) are the world’s largest digitally savvy generation who shop, work, and eat online. According to a Bernstein study on ‘India Internet’, this digitally savvy, app-first Gen Z cohort is taking centre stage in India’s consumer markets, authoring “major adjustments” in consumption trends such as the increase of quick commerce delivery and direct-to-consumer (D2C) companies.

This Gen Z habit has helped to scale up internet use cases, resulting in an increase in monthly or daily active users (MAU/DAU) across app ecosystems. According to Meta, India has the world’s greatest presence across their app ecosystem (Facebook, Instagram, WhatsApp, FB Messenger), and fast commerce solutions such as Blinkit and Zepto are enabling digital-first firms to access GenZ clients, swiftly boosting growth. Therefore, the younger generation’s adoption of the purchase platform is acknowledged to be driving growth for quick commerce’s success.

As of 2024, the estimated revenue of quick commerce amounted to over three billion U.S. dollars in India. The revenue is likely to increase by about nine billion dollars by 2028. The gross merchandise value (GMV) of quick commerce in India has shown consistent growth, reaching 2.8 billion in 2023. This rising trend in GMV highlights the growing consumer demand for swift delivery services, setting the stage for further market expansion. The sector’s growth is further evidenced by the increasing number of monthly transacting users, which surpassed eight million, representing a 46 % year-over-year increase.

Hence, one must assume that quick commerce is going to be the magnet that will attract the honchos of the industry as it is expected to rise exponentially in the future.

However, there are always two sides of the coin. Though quick commerce has made it to big picture in recent times and is determined to maintain their growth; however, there are critics who are signalling red flags in the quick commerce industry.

The reality beneath the glimmery dust.

The discount wars, if ended, have the potential to disrupt the company negatively.

Have you ever seen that you search for one food from Zomato, and then again check the same on Swiggy, and go with the one that gives better discounts? The same phenomenon goes with Blinkit and Zepto as well. These fresh capital infusions (let’s say Zepto) will eventually lead to discounting wars between players. Everyone has virtually worked out delivery times, and customers don’t care if it’s 10 minutes or 20 minutes. Timing is important when comparing 15-20 minute delivery to one-hour delivery. Short delivery times, according to industry leaders, no longer provide an advantage, and platforms will strive to entice customers through price.

Zomato, which owns Blinkit, has $1.5 billion in cash, while Swiggy’s upcoming IPO will provide $450 million or more in new money. Therefore, this again points out the fact that this quick delivery sounds like no sustainable business model, and every game is played just on the sword of discounts, which eventually, one day will lose all its sharpness, drying the company’s cash reserves.

If two of India’s leading e-commerce businesses, Amazon and Flipkart, are still losing money after more than a decade — Jeff Bezos has invested $11 billion in India in as many years — is there or will there be a sustainable recipe for quick commerce companies and its ilk to profit handsomely? Unlikely- This paves the way for questioning the long-term profitability of these businesses and, thereby, the market value they can generate in future!

If the discount wars die and the prices as per delivery platform fees and convenience fees, then the customer will be no late to point out the success of these quick commerce models, as seen in the recent case where Zepto User’s Rs 60 Order Came With Rs 112 Extra Fees and the Internet was hurried to Cry ‘Scam’. Similar incidents can also be seen when orders from restaurants and food delivery platforms have an enormous difference in their final billing amounts (delivery app being at the higher end), questioning the suitability of these delivery companies.

Market penetration is not so easy in Tier 2-3 cities.

As of 2021, 31% of India’s population was considered middle class, which is about 432 million people. The middle class is growing at a rate of 6% per year and is expected to reach 38% of the population by 2031 and 60% by 2047. In recent quarters, several of these players’ gross order value (GOV) increased by 93% year on year. Even still, the quick commerce maths requires a single dark store to generate Rs 2 crores in sales each month. Such revenue density in a single circle of distribution is only conceivable in four metropolises and a few state capitals, limiting the total addressable market to a maximum of certain cities only.

Expecting the average order/transaction value (AOV) on these platforms to double by FY29 is similarly ambitious. The greater these organisations’ future AOV targets, the smaller their target size of affluent clients will be. As a result, the market’s size is also under review. However, there are better reviews as Swiggy take Instamart to 43 cities ahead of the festive season, and Zepto and Blinkit have determined to increase their number of dark stores to great numbers. So, whether or not the penetration of market size with an increase in the number of dark stores will be successful is a point of the question.

The basis of Quick commerce growth is that a large percentage of Indian customers would continue to make unexpected purchases. While time constraints, laziness, and click-happy habits of instant gratification borrowed from the e-commerce industry may be working in tandem, particularly in metros and tier-1 cities, as well as among Gen Z consumers, it is naive to assume that even in these geographies, everyone wants ten-minute delivery for all products.

Global data show that this precise logic contributed to the Quick commerce boom since customers never truly shifted to such consumption in perpetuity. Quick commerce firms such as Gopuff, Jiffy, and Gorillas have exited numerous global marketplaces, implemented major layoffs, and scaled back their aspirations after realising that customers never sought genie-like delivery. Therefore, whether people really want 10-minute delivery or quick or instant delivery for everything remains a question.

Sustainability of business- Is 10-minute delivery, aka the quick commerce, a sustainable business model?

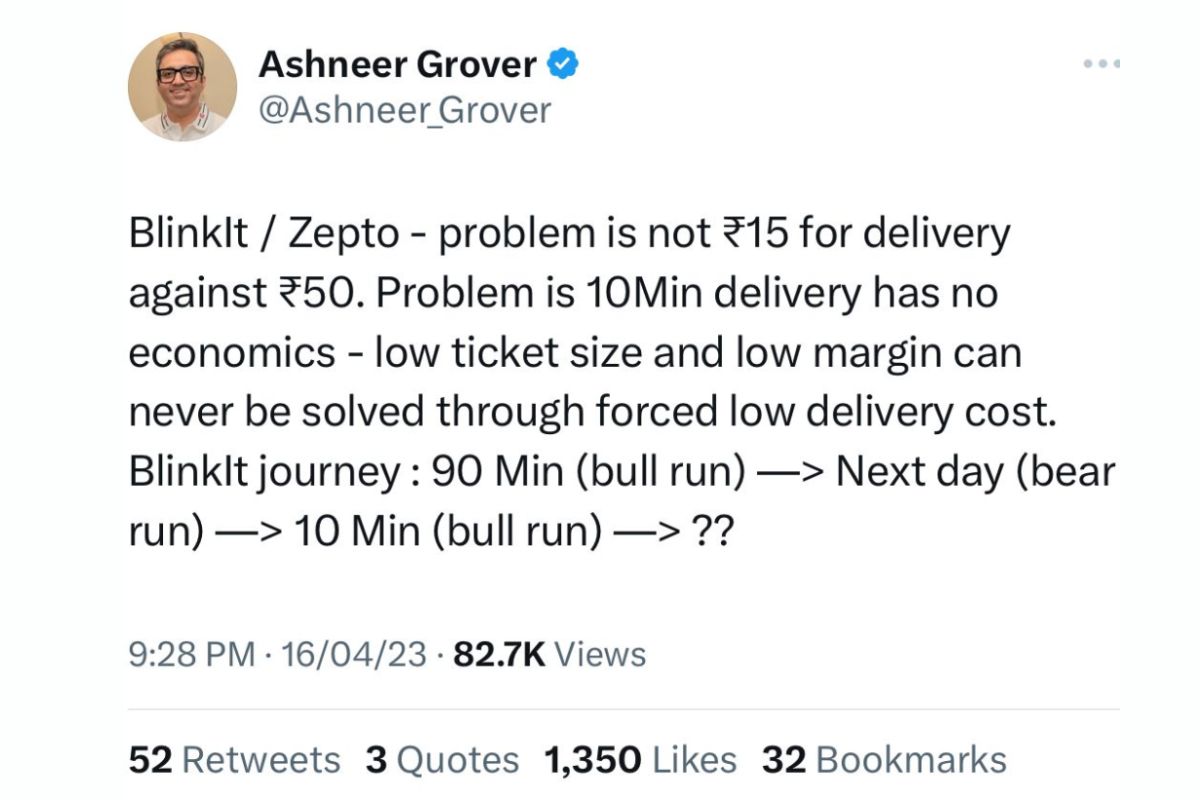

Mr Ashneer Grover, the famous Shark took to X in April last month and said that delivering goods in 10 minutes “has no economics” asserting that low ticket size and low margin can never be solved by forced low delivery cost. Grover’s tweet quickly received a deluge of reactions from disgruntled Blinkit and other delivery app users who had to wait far longer than 10 minutes to get their purchase delivered or even registered.

One user wrote that it took him more than an hour to get the deliveries, whereas the panel showed 6 minutes from the time he ordered till cancelling it, eventually turning the customer to shop from a nearby physical store. Another user replied to this by saying that this 10-minute quick delivery fails and takes up to 30 minutes during peak hours.

Another is irked that one may order because of the urgent urge to snack and get delivered in 20 minutes, but why should one purchase veggies, butter, etc? Of course, they can purchase these from their nearby Kirana store while coming back from office hours! These real-time events, as mentioned by X users, question the sustainability of these quick commerce business’s delivery models.

Scalability presents three areas of concern: the dark store model, delivery partners, and governance, all of which are under strain. Future orders – frequency, minimum order value (MOV), and repeat orders – are critical to scalability. Blinkit predicts that each dark store needs 1500-2000 orders per day to break even. Blinkit and Instamart intend to expand the number of dark stores and product offerings (which are presently over 6000 and increasing). In order to enhance MOV, there are plans to introduce product categories ranging from cosmetics to sports products, as well as electronics and household equipment. These options lack realism; certain consumers will eventually purchase a set of earbuds from Blinkit. But what about all consumers? Regularly? I doubt!

Groceries and basics are more likely to remain in the basket over time. While the number of orders may grow, the MOV will stay low, thus impacting unit economics. With the anticipated launch of ‘Flipkart Minutes’ and the previously announced limited entry of JioMart, the space will become more crowded. This will result in a lack of consumer loyalty and competitive discounting, hence deteriorating unit economics and validating Mr Grover’s statements.

Recent cases highlighting unhygienic, infected, and outdated items have brought the operations of dark markets under scrutiny. Separating food from non-food goods, maintaining sanitation in storage, handling, and transportation, and guaranteeing enough product life at the point of sale are all critical to ensuring platform trust. The absence of platform control is obvious, and it already hampers Zomato and Swiggy’s food delivery operations.

Furthermore, delivery partners face terrible physical and mental strain as they continually struggle against time in extreme and poor weather conditions and geographies (including ascending many staircases with hefty items). They frequently wait 10-15 minutes between orders and do not receive enough breaks while on the job. Can Quick commerce platforms even be concerned and survive for the long term on that?

The effect on society doesn’t sound promising.

The negative externalities of the Quick commerce have yet to be established, however there are some anecdotal accounts. Even as delivery partners navigate these spaces, Quick commerce enterprises are likely to generate traffic chaos in the immediate area. A rise in the quantity of orders will lead to more packing and storage waste, as well as pollution.

The already restricted metropolitan infrastructure, which bears the burden of e-commerce and food delivery, will degrade much faster. Furthermore, the development of dark stores drives up real estate values, especially as Quick Commerce focuses on metros and tier 1 cities. According to global data, zoning regulations that limit the amount of business space in local regions serve to keep real estate values in check and prevent communities from being overly commercialised. However, there are no such restrictions in India.

Also, Commerce and Industry Minister Piyush Goyal’s recent statements on suspected rule violations by big e-commerce giants, notably Amazon, have sparked debate about whether the government is finally ready to impose harsher controls. Goyal’s comments have fuelled speculation that a new set of e-commerce laws, as well as a complete regulatory framework, might be on the way.

He expressed concern about shifting consumption patterns, particularly among young people, and predicted that Indians would become a country of couch potatoes, drawn to OTT shows and ordering food at home every day. Goyal emphasised that activities such as dining out or visiting friends for coffee are critical for human growth, establishing relationships that may be lost as more people rely on digital conveniences. Although these statements are for e-commerce giants specially Amazon, but it also engulfs within itself the industry of quick commerce.

The end game.

Success is also based on advertising revenues, which are reliant on the reach and discovery orientation of any given platform. Being quick does not guarantee more discovery. E-commerce platforms can easily add brands and categories with a single click, based on data sets that change every second, and corner more advertising since they have a backend to facilitate the switchover.

Quick commerce gloomy shops can only carry so much. The advertising assumptions that these Quick Commerce companies make to make their enterprises lucrative are just too high. They will fall short if they try to compete with Amazon or Flipkart. When it comes to selling rice and milk, value stores like D-Mart will provide considerably more scientific metrics. The early trends in advertising will eventually plateau, and the struggle will begin.

It seems like we are all getting carried away by the top-line growth. There are points to believe that when the dust settles down, and players are forced to look at the bottom line, they will have to start asking consumers for a service fee by whatever name, and that’s when we shall truly know the growth trajectory of quick commerce. It is necessary that these companies realise that the Indian consumer will always do a cost-benefit.

If the discounts and freebies don’t result in a lower cost or the same cost as the local Kirana store or a local restaurant that does free home delivery, 98% of Indian consumers will shun them, or else, within no time, these quick commerce companies will be quick in becoming a black hole which will be engulfing all of the funding without any sustainable business model. However, we wish the quick commerce giants good luck and will be happy to be proven wrong!