From Importing Missiles To Building Them: How India’s Private Defence Revolution Could Redefine National Security, Manufacturing, And Global Arms Exports

For decades, India bought missiles.

Today, India wants to build them.

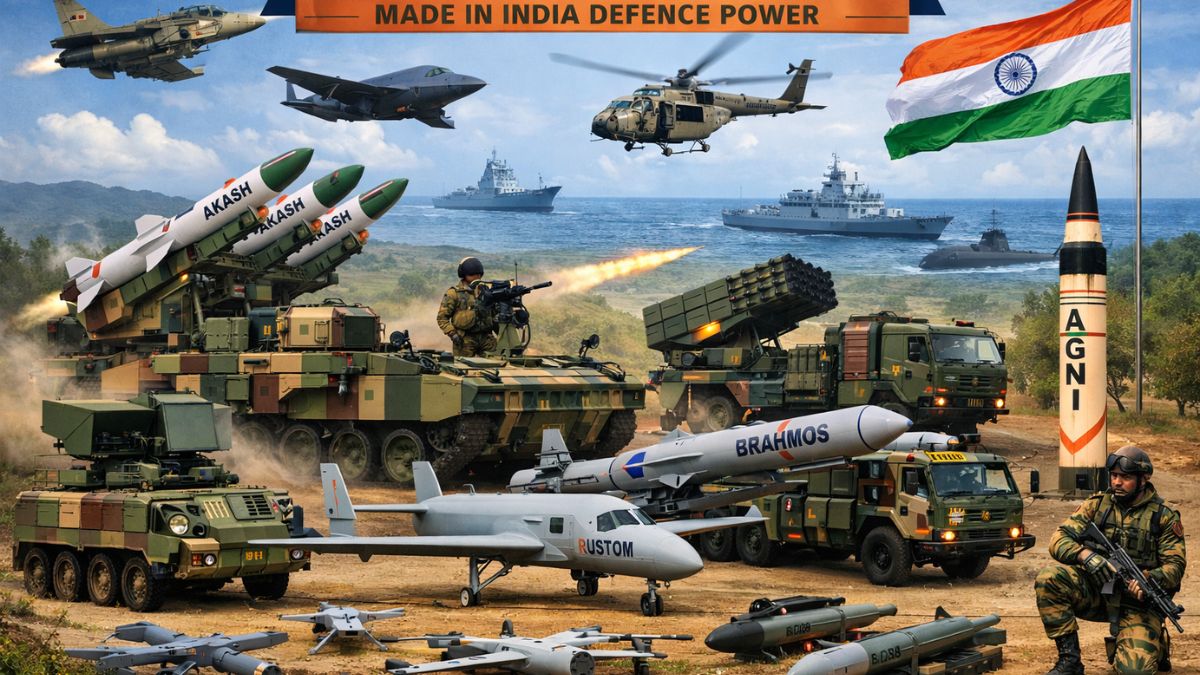

On July 5, 2026, Adani Defence & Aerospace broke ground on a ₹2,500-crore project in Shivpuri, Madhya Pradesh — an integrated missile manufacturing ecosystem billed as South Asia’s largest private-sector facility of its kind. The complex will combine missile system assembly with composite propellant production and TNT (Trinitrotoluene) manufacturing at a single site, a backward-integrated capability that, until now, existed only within India’s public sector. Jeet Adani, Director of Adani Defence & Aerospace, described the ambition in stark terms at the foundation ceremony: the facility would help “replace foreign dependency with domestic power.”

It is tempting to read this as simply another large corporate investment — Adani Group, again, entering a new industrial sector. But that framing understates what is actually happening. The Shivpuri project is a visible marker of a much larger structural shift: India’s transition from being one of the world’s largest importers of arms to becoming a country that manufactures, and increasingly exports, sophisticated weapons systems — with private industry, not just state-run behemoths, driving the change.

For most of independent India’s history, its military strength was measured by what it could buy from abroad. The next phase of its strategic journey may instead be measured by what it can design, build, and sell. The question worth asking is not just “why is Adani building missiles?” but something bigger: Is India witnessing the birth of its own military-industrial complex?

India’s Long Dependence on Imported Weapons

To understand why the Shivpuri project matters, it helps to look at where India has come from.

Since the Cold War, India’s defence establishment has leaned heavily on foreign suppliers. The relationship with the Soviet Union, and later Russia, has been the backbone of this dependence — from MiG and Sukhoi fighter jets to tanks, submarines, and air defence systems. Over the decades, India diversified: French Rafale fighters, Israeli precision-guided munitions and drones, and American surveillance aircraft and artillery all found their way into the Indian arsenal.

The scale of this dependence is difficult to overstate. According to the Stockholm International Peace Research Institute (SIPRI), India was the world’s second-largest importer of major arms between 2021 and 2025, accounting for roughly 8.2 percent of global arms imports — behind only Ukraine, whose imports were driven by active war. Russia has remained India’s largest single supplier, though its share of Indian arms imports has fallen sharply, from around 72 percent in the early 2010s to closer to a third of imports in the most recent five-year period, as India has diversified toward France, the United States, and Israel.

This is not a new phenomenon, but it has always carried strategic risk. A nation that depends on foreign powers for the tools of its own defence is vulnerable in ways that are easy to overlook during peacetime and painfully obvious during conflict. Spare parts can be delayed. Technology transfers can be withheld. Political relationships can shift overnight, and with them, the willingness of a supplier nation to honour a contract. During an actual war, an import-dependent military risks running short of ammunition, missiles, or replacement components at the exact moment it needs them most — a vulnerability India has been acutely conscious of, given tensions along both its western and northern borders.

It is this vulnerability that India’s defence planners have spent the last decade trying to engineer away.

Why Private Companies Are Now Entering Defence

Historically, Indian defence manufacturing was the near-exclusive domain of the state. The Defence Research and Development Organisation (DRDO) handled research and design; Hindustan Aeronautics Limited (HAL) built aircraft; Bharat Electronics Limited (BEL) handled electronics; and a network of Ordnance Factories — since corporatised — produced ammunition and equipment. Private firms, where they existed at all, were relegated to supplying components.

That has changed markedly over the past several years. Government policy — including the “Make in India” initiative, the Aatmanirbhar Bharat (self-reliant India) push, and reforms like the Defence Acquisition Procedure of 2026, which raised indigenous-content requirements and streamlined procurement categories — has deliberately opened space for private companies to move up the value chain, from component suppliers to full system integrators.

The result is a new generation of private defence conglomerates. Tata Advanced Systems has grown into a comprehensive defence integrator spanning aircraft structures, armoured vehicles, and unmanned systems, with a growing international footprint. Larsen & Toubro has built deep expertise in naval systems, submarines, and missile launch infrastructure, leveraging its civil and nuclear engineering base. Bharat Forge has repurposed its metallurgical and forging expertise into artillery systems and armoured platforms. Mahindra Defence has moved into drones and electronic warfare. And Adani Defence & Aerospace, having already built a small-arms manufacturing base in Gwalior producing rifles, carbines, and light machine guns for the armed forces, is now extending that footprint into missile manufacturing at Shivpuri.

The scale of this shift shows up in the numbers. India’s overall defence production touched an all-time high of roughly ₹1.78 lakh crore in the 2025-26 financial year, with private industry’s order book expected to cross ₹55,000 crore by the end of the fiscal year — driven partly by urgent capability demands that emerged from recent border skirmishes involving drones and missile threats.

Perhaps most tellingly, the government has shortlisted Tata Advanced Systems, Larsen & Toubro, and Bharat Forge — not HAL, the traditional public-sector monopoly — to develop prototypes for India’s Advanced Multirole Combat Aircraft (AMCA), the country’s most ambitious fighter jet programme. For the first time in India’s defence history, its most complex and capital-intensive weapons platform may be led by private industry rather than a state monopoly.

Why Missile Manufacturing Is Different

Building a missile is categorically harder than assembling a truck or a rifle. A rifle is, at its core, a mechanical object. A missile is a system of systems: propulsion, guidance, warheads, sensors, composite materials, and precision electronics, all of which have to work together flawlessly, often under extreme stress, heat, and speed.

This is what makes the Shivpuri facility notable beyond its price tag. Rather than simply assembling missile bodies from imported or centrally supplied components, the complex is designed to bring propellant production, TNT and explosive-grade material manufacturing, and final system integration under one roof — described by the company as India’s first backward-integrated private-sector capability of its kind. That kind of vertical integration matters because it reduces dependence on a scattered, often import-reliant supply chain for critical sub-components.

A missile programme that has to wait for propellant or explosive-grade materials sourced from elsewhere is only as fast, and only as secure, as its weakest supplier link. Owning that chain end-to-end is what allows a manufacturer to scale production quickly once a design is approved — a capability India has historically lacked in the private sector.

The facility is expected to support the serial production of several indigenous missile systems developed by DRDO, as they move from successful trials into mass manufacturing — including next-generation anti-radiation missiles, naval anti-ship missiles, and long-range precision-guided munitions. In other words, this is not R&D from scratch; it is industrial-scale production capacity being built for weapons India has already designed but has struggled to manufacture at the volumes its armed forces require.

The Rise of India’s Military-Industrial Complex

The term “military-industrial complex” was coined in the United States in the mid-20th century to describe the close, mutually reinforcing relationship between the armed forces, the government that funds them, and the private companies that supply them. It was often used critically — as a warning about how deeply defence spending could become entangled with corporate and political interests.

Whatever one makes of that history, the term is a useful lens for what is emerging in India. A functioning defence-industrial ecosystem is not just about factories; it requires the government setting policy and demand signals, private industry providing capital and manufacturing scale, research institutions and DRDO providing technology, MSMEs providing components and specialised parts, universities and training institutes providing skilled labour, and — eventually — export networks providing revenue and geopolitical leverage.

India now has visible pieces of each of these. The government’s iDEX initiative has drawn hundreds of startups and small manufacturers into the defence supply chain. Large private conglomerates are providing the capital and industrial scale that public-sector units historically could not match. DRDO continues to anchor core research and design. And, as detailed below, an export architecture is slowly taking shape. Whether these pieces cohere into a truly self-sustaining ecosystem — one that doesn’t just assemble weapons but owns the intellectual property behind them — remains the open question defence analysts are debating.

Madhya Pradesh’s Transformation into a Defence Manufacturing Hub

One of the more overlooked angles of this story is geographic. Madhya Pradesh, not traditionally associated with heavy defence manufacturing, is emerging as a serious hub for it.

Adani’s presence in the state did not begin with Shivpuri. Since 2020, the company has operated a small-arms manufacturing complex in Gwalior that produces pistols, carbines, assault rifles, and light machine guns for the Indian armed forces — a programme that, according to the company, delivered 2,000 light machine guns to the armed forces months ahead of schedule. The Shivpuri missile ecosystem, roughly 100 kilometres from Gwalior, extends that industrial base into far more complex territory. Company officials have described Gwalior and Shivpuri together as “twin engines” of the state’s defence manufacturing ambitions.

Several factors make the Gwalior-Shivpuri-Guna belt in central India attractive for this kind of investment: available land at scale, proximity to national highway and rail corridors connecting to both northern and western India, and a state government actively courting large industrial investment. Madhya Pradesh Chief Minister Mohan Yadav welcomed the project as reinforcing the state’s emergence as “a preferred destination for strategic manufacturing,” while Union Minister Jyotiraditya Scindia, representing the neighbouring Guna constituency, called it the start of “a new industrial chapter” for the region.

The Shivpuri project is itself part of a much larger commitment — Adani Group has pledged roughly ₹1.10 lakh crore in investment across Madhya Pradesh, spanning energy, cement, mining, and smart infrastructure, with a target of generating over a lakh jobs in the state by 2030. The missile facility alone is projected to create around 5,000 direct and indirect jobs and to draw in more than 50 micro, small, and medium enterprises into a specialised defence supply chain. For a state whose industrial identity has traditionally centred on agriculture and mid-sized manufacturing, this represents a genuine shift — and a template other states, from Uttar Pradesh to Tamil Nadu, are also pursuing through their own defence industrial corridors.

Can India Become a Global Missile Exporter?

Domestic capacity is only half the story. The other half is whether India can turn that capacity into export revenue — and there is meaningful evidence that it already has begun to.

The clearest example is the BrahMos supersonic cruise missile, developed jointly by DRDO and Russia’s NPO Mashinostroyeniya. In 2022, India signed its first major missile export contract, worth roughly $375 million, to supply the Philippines with BrahMos coastal defence batteries — deliveries of which have since been made, including a shipment transported by sea in 2025. Indonesia has separately sought a deal valued at around $450 million, and countries including Vietnam, Malaysia, the UAE, Chile, and South Africa have expressed varying degrees of interest. India’s defence minister has confirmed additional BrahMos-related export contracts worth roughly $450 million, without naming the buyer nations.

Beyond BrahMos, India has begun exporting other complete weapons platforms rather than just components. Armenia has emerged as a major buyer of Indian-made Akash surface-to-air missile systems and Pinaka multi-barrel rocket launchers, alongside artillery guns — reportedly becoming the largest single destination for Indian weapons exports outside component supply chains. Meanwhile, private firms like Tata Advanced Systems and Dynamatic Technologies have built a different kind of export relationship, supplying structural components — fuselages, airframe parts, engine components — into the global supply chains of Boeing, Lockheed Martin, and Airbus, embedding Indian manufacturing into NATO-grade production standards even where the finished product isn’t Indian-branded.

The overall trajectory is dramatic by any measure. India’s defence exports rose from a modest ₹686 crore in 2013-14 to roughly ₹38,424 crore in the 2025-26 financial year — a more than fifty-fold increase over twelve years, and a jump of over 60 percent in the most recent year alone. Private firms accounted for roughly 45 percent of that export figure, a meaningful share for an industry that, a decade ago, private companies barely participated in.

Potential future markets extend well beyond current customers: Southeast Asian nations wary of Chinese assertiveness in the South China Sea, African states seeking affordable and reliable military hardware, Gulf countries diversifying their defence partnerships beyond Western and Russian suppliers, and Latin American militaries looking for cost-effective alternatives. Whether India can convert interest into signed contracts at scale — and whether it can do so while maintaining the trust of both buyers and its own strategic partners — will determine how large a defence-exporting nation it eventually becomes.

Economic Impact Beyond Defence

The ripple effects of a growing private defence sector extend well past the factories themselves. Missile and weapons manufacturing at scale requires steel, specialty chemicals and explosives-grade materials, precision electronics, composite materials, and increasingly, artificial intelligence for guidance and targeting systems — all of which pull in adjacent industries and specialised suppliers.

The Shivpuri project alone is expected to generate around 5,000 direct and indirect jobs and to integrate more than 50 local MSMEs into its supply chain, according to Adani Group’s own projections. At a national level, government data cited by industry analysts suggests the broader private defence order book could exceed ₹55,000 crore in the current fiscal year, with related sectors — testing laboratories, skill development institutes, and precision engineering firms — expanding alongside the primary manufacturers. Financial analysts, including at Goldman Sachs, have projected annual earnings growth north of 30 percent for listed private defence companies between FY25 and FY28, driven by both export momentum and continued domestic self-reliance mandates.

This is not merely a defence story; it is an industrial policy story, with implications for regional employment, MSME growth, and India’s broader manufacturing ambitions under initiatives like Make in India.

Challenges India Still Faces

None of this should be mistaken for a solved problem. India’s defence-industrial ambitions still run into real technological and structural constraints.

Aero-engine technology remains one of the most stubborn gaps — India has struggled for decades to indigenously develop a reliable jet engine, and even its flagship Tejas fighter programme depends on imported American engines, a dependency that has caused repeated production delays. Advanced semiconductors, sophisticated guidance and seeker systems, and next-generation sensor technology also remain areas where India leans on foreign expertise or components. Research and development spending compounds the problem: Indian defence companies, on average, invest a little over 1 percent of revenue in R&D, compared to a global industry average closer to 3.4 percent — though there are notable exceptions, such as HAL and Bharat Dynamics, which invest considerably more.

There are also softer, less visible constraints: export control regulations that can complicate international sales of technology with dual-use origins; intellectual property questions, particularly where Indian systems are built on licensed or jointly developed foreign technology; a shortage of highly specialised manpower in fields like propulsion engineering and precision guidance; and testing infrastructure that, in some categories, still lags what more mature defence-exporting nations maintain.

India is also not operating in a vacuum. It is competing for defence export markets against the United States, China, Israel, Turkey, South Korea, and France — all of which have decades of head start in some segments, established customer relationships, and, in several cases, far larger R&D budgets. Turkey and South Korea, in particular, have emerged as aggressive competitors in the same price-and-capability tier India is targeting for exports to developing nations.

The Geopolitical Dimension

Every missile India manufactures domestically, rather than imports, has implications beyond economics. It reduces the leverage foreign suppliers can exert during a crisis, strengthens India’s claim to strategic autonomy in an increasingly multipolar world, and, over time, sharpens deterrence along its contested borders.

Defence exports carry their own geopolitical weight. When India sells BrahMos missiles to the Philippines or Akash systems to Armenia, it is not simply making a commercial sale — it is deepening a security relationship, embedding itself in that country’s military planning for years or decades to come, and signalling where its own strategic sympathies lie. As one Indian official put it when discussing the BrahMos deal with the Philippines, India is increasingly playing the role of “a giver, not just a taker” in the global defence order — a notable rhetorical shift for a country that spent most of its post-independence history as a buyer of last resort.

This matters most acutely in the Indo-Pacific, where countries wary of Chinese assertiveness are actively looking for alternatives to Chinese or even Western suppliers. An India capable of supplying credible, affordable, and increasingly indigenous weapons systems has an opening to become a preferred partner for exactly these nations — a role that carries diplomatic as well as commercial value.

Risks and Ethical Questions

None of this transformation is without legitimate concerns, and a fair accounting of it has to include them.

The growing role of large private conglomerates in an area as sensitive as missile and explosives manufacturing raises questions about corporate concentration — a small number of large business houses gaining outsized influence over a strategically critical sector. It raises questions about procurement transparency, given the scale of government contracts now flowing to private players, and about the adequacy of regulatory oversight for an industry historically insulated from public scrutiny by its national-security classification. There are also more mundane, but serious, safety and environmental concerns associated with TNT and explosive-grade material manufacturing at scale, which require rigorous safety protocols and independent oversight, not just self-certification by the manufacturers themselves.

None of these concerns are arguments against India building a defence-industrial base — most analysts agree that reducing import dependence is a legitimate and overdue strategic goal. But they are reasons why the shift to private-sector-led defence manufacturing deserves continued scrutiny from journalists, regulators, and lawmakers, rather than being treated as an unambiguous success story simply because the investment numbers are large.

Conclusion

For decades, India measured its military strength by the weapons it purchased. The next phase of its strategic journey may be measured by the weapons it designs, manufactures, and exports.

Projects like the Shivpuri missile ecosystem are not simply industrial investments — they are a test of whether India can build a globally competitive, self-reliant defence manufacturing base that goes beyond assembly and genuinely owns the technology it produces. The early signals are promising: record production figures, a private sector moving from components to complete systems, and export contracts reaching markets from Southeast Asia to the Caucasus.

But success will not be measured only in factories built or capital deployed. It will depend on whether India closes its remaining technology gaps in propulsion and sensors, whether it can scale R&D spending closer to global norms, whether its regulatory institutions keep pace with an increasingly powerful private defence sector, and whether it can sustain the trust of both international buyers and its own citizens along the way. The Shivpuri groundbreaking is a milestone. Whether it becomes a turning point depends on everything that happens after the ribbon is cut.