Is Sugar Cosmetics Shutting Down? What Went Wrong With Sugar?

Sugar Cosmetics Has Never Had a Profitable Year. Its Employees, Investors, and Consumers Deserve to Know Why.

Is Sugar Rush Over? A Financial Reckoning of India’s One Of The Most Glamorous Bleeding Startup

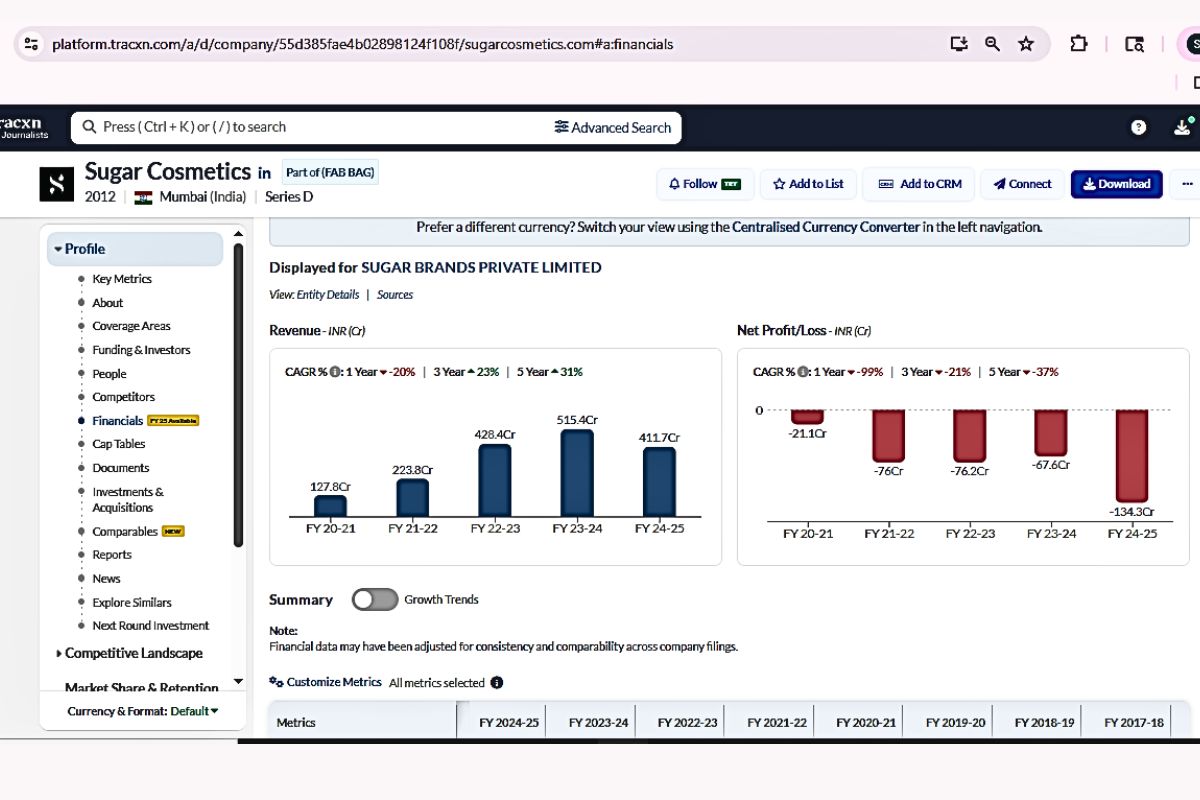

In FY2024-25, Sugar Cosmetics, formally Sugar Brands Private Limited earned ₹411.7 crore in revenue and lost ₹134.3 crore. That is a loss-to-revenue ratio of 32.6%.

A healthy Series D consumer brand, one that has raised over $96 million across 16 rounds over more than a decade, should, by this stage, be approaching EBITDA breakeven at minimum, with a loss-to-revenue ratio trending toward zero. The global benchmark for D2C beauty companies at scale is a net margin of 8-12% positive. Sugar Cosmetics is not approaching zero. In FY25, it moved in the opposite direction, losses nearly doubled from ₹67.6 crore the previous year, even as revenue fell 20%.

Then came FY26. Revenue declined further, to approximately ₹380 crore, according to Mint’s reporting in May 2026. The company has been in the grip of a “severe cash crunch” for six months. Promoters, Vineeta Singh and Kaushik Mukherjee, have reportedly settled employee salaries from their personal accounts. Sugar is now seeking ₹100-150 crore as “rescue funding,” at a valuation of ₹1,400-1,500 crore, roughly half its peak valuation of ₹3,000 crore in 2022.

This is not a speed bump. This is a structural collapse in slow motion.

THE YEAR-ON-YEAR STORY

Sugar Cosmetics was founded in 2012 as part of FAB BAG, a subscription beauty box service. The SUGAR brand was carved out as a standalone colour cosmetics label. Its early years were lean and largely unfiled publicly. The trackable financial record, beginning FY2020-21, tells the following story.

In FY21, revenue stood at ₹127.8 crore with a net loss of ₹21.1 crore, a loss-to-revenue ratio of 16.5%. In FY22, revenue nearly doubled to ₹223.8 crore, but losses more than tripled to ₹76 crore, the ratio exploding to 34%. The company had made a classic D2C mistake, like, it spent heavily to grow fast, and the cost curve ran well ahead of the revenue curve.

In FY23, revenue reached ₹428.4 crore, an impressive 91% year-on-year jump. But losses held stubbornly at ₹76.2 crore, only ₹0.2 crore better than the year before despite revenue nearly doubling. The loss ratio improved to 17.8%, which was the one year the trajectory looked hopeful. In FY24, revenue climbed to ₹515.4 crore, and losses actually narrowed to ₹67.6 crore, the ratio falling to 13.1%. This was the moment. The year management told investors the IPO was two to three years away, contingent on profitability above ₹1,000 crore revenue. And then the cliff.

In FY25, revenue fell to ₹411.7 crore, a ₹103 crore decline, the first revenue contraction since inception. Losses exploded to ₹134.3 crore, the highest in the company’s history, nearly double the previous year’s figure. The loss ratio went from 13.1% back to 32.6%. In FY26, revenue slid further to approximately ₹380 crore. The cumulative five-year loss total is approximately ₹375 crore. The company has never been profitable for a full fiscal year, and the gap between the story it told investors in January 2024 and the reality of May 2026 is not a tactical setback. It is a complete narrative implosion.

What does this trajectory say about the fundamental economics of the business model? It says, bluntly, that Sugar Cosmetics has not found a way to grow profitably. The FY23-FY24 period created the illusion of an inflection point, hinting losses narrowing, revenue growing. But that period was likely the high-water mark of a specific wave, because the post-pandemic beauty boom, the D2C tailwind, and the aggressive offline expansion into 45,000+ retail touchpoints and 550+ cities. When that expansion stopped generating incremental revenue, when the stores stopped pulling their weight, the cost structure did not shrink with it. It stayed. And it ate the company.

WHERE IS THE MONEY GOING?

The first and largest cost head is almost certainly retail infrastructure and employee costs. At its peak, Sugar operated 45,000+ retail touchpoints across 550 cities; an offline expansion that required field sales teams, store-level inventory management, distributor networks, and significant working capital locked into the supply chain. When revenue fell 20% in FY25, these costs did not fall proportionally because leases, salaries, and distributor agreements are largely fixed in the short term. This is precisely the cost-structure rigidity that produces the situation where revenue drops ₹103 crore but losses grow ₹67 crore, that the company spent its way into a fixed overhead base it could no longer afford.

The second cost head is marketing and brand spend. Sugar Cosmetics built its brand identity on the back of Vineeta Singh’s personal visibility — her Shark Tank India presence turned her into one of India’s most recognised startup founders — and on celebrity marketing, influencer campaigns, and a colour cosmetics identity built around bold, matte-finish products for Indian skin tones. This was genuine differentiation in 2016-2019. By 2024-25, it was table stakes. Minimalist, Nykaa’s private labels, Renee Cosmetics, and a wave of Shark Tank-funded challengers had cloned the “Indian skin, affordable premium” proposition. Maintaining brand salience in that environment requires continuous marketing investment, which, like retail infrastructure, is not easily turned off.

The third cost head is working capital and inventory. A brand with 45,000 retail touchpoints has enormous working capital tied up in stock at the distributor and retail level. When revenue declined, this stock did not liquidate cleanly. Unsold inventory generates dead working capital, and the only way out is discounting — which further compresses margins. The reported restructuring moves, closing stores and ending expensive distributor ties, generated a one-time ₹95 crore improvement to the bottom line. But this was largely a recognition of prior losses, not new value creation.

The question that every investor must sit with is this. When this spending stops, what remains? Does Sugar own manufacturing facilities? No. Does it hold patents on formulations? None publicly filed. Does it have exclusive retail relationships that cannot be replicated? No, its retail is through general trade, modern trade, and its own website, none of which is exclusive. What it owns is brand recall, a strong product range in colour cosmetics, and Vineeta Singh’s personal brand equity. Those are real assets. But they are not durable moats. They require continuous reinvestment to maintain.

THE MOAT QUESTION

This is, in many ways, the most important question to ask about any consumer brand that has spent $96 million building itself. What, specifically, has that capital constructed that cannot be easily replicated?

Sugar Cosmetics does colour cosmetics well. Its matte lipsticks and eyeliners built genuine cult status among urban Indian millennials. It understood Indian skin tones and climate at a time when multinationals were selling products formulated for European complexions. That insight was its founding competitive advantage. The problem is that this insight is now widely shared across the Indian beauty industry. WOW, Mamaearth, Nykaa, Renee, Plum, and dozens of newer entrants have all built product ranges with the same “formulated for Indian skin” thesis. The differentiation that once justified a premium and a loyal following has been commoditised.

Sugar’s manufacturing is entirely outsourced. It has no proprietary ingredient, no patented formula, and no manufacturing process that a competitor could not replicate by walking into the same contract manufacturing ecosystem in Noida or Daman. Its D2C website provides customer data, but this advantage is shared by every brand that sells online. Its offline retail presence, once a genuine differentiator when competitors were purely digital, is now a cost liability as the company retracts its footprint.

The honest answer to the moat question, therefore, is: brand recall and Vineeta Singh’s personal visibility. Those are meaningful but expensive to maintain and cannot, on their own, justify the capital that has been consumed to build them.

/entrackr/media/post_attachments/wp-content/uploads/2022/03/Sugar.jpg)

THE FUNDING DEPENDENCY

Sugar Cosmetics has raised approximately $96-101 million (approximately ₹800+ crore) across 16 funding rounds from 73 investors. Its marquee backers include L Catterton, the luxury consumer investment arm affiliated with LVMH, Elevation Capital, A91 Partners, India Quotient, Anicut Capital, Malabar Investments, and Stride Ventures. This is a legitimate, high-quality cap table.

At its peak in 2022, the company raised a ₹420 crore Series D led by L Catterton at a valuation of approximately ₹3,000 crore ($370 million). At the time of that raise, revenue was on a strong trajectory — the FY22 figures had been filed showing ₹223.8 crore in revenue, and the market was in the grip of D2C euphoria post-pandemic.

Two years later, the picture has inverted. The company is seeking ₹100-150 crore at a valuation of ₹1,400-1,500 crore, a 50-53% haircut from the 2022 peak. This “typical growth investors are unlikely to invest in the current state,” and that the fundraise is being targeted at family offices and HNIs rather than institutional venture or growth funds. That is a critical signal. When a company has to descend from institutional investors to family offices for a rescue round, it reflects that the institutional smart money has done its own math and stepped back.

The cumulative loss of approximately ₹375 crore means that a substantial portion of the $96 million raised has been consumed in operations rather than in building permanent assets. The question of cash runway is not publicly disclosed, but if the company has been settling salaries from promoter personal funds as reported, the working capital position is clearly acute. The ₹95 crore improvement from store closures and distributor rationalisation provides some relief, but it is a one-time correction, not a recurring cash flow improvement.

What happens if the ₹100-150 crore rescue round does not close? That is a question the company has not publicly answered.

THE MARKET CONTEXT

India’s beauty and personal care market is, by every forecast, one of the most attractive consumer categories in the world. The market is heading toward $40 billion by 2030, growing at approximately 10-12% annually. The Indian woman is spending more on cosmetics, skincare is growing faster than colour cosmetics, and the premiumisation trend is genuine and sustained. Sugar Cosmetics is not operating in a dying market. It is losing ground in a growing one, which is, arguably, worse.

Its three most dangerous competitors illuminate why. Nykaa, publicly listed, profitable, and with a gross margin-generating marketplace model that does not require it to own inventory, has the distribution and brand relationships that Sugar cannot match at its current scale. More importantly, Nykaa’s house brands are priced and positioned in direct competition with Sugar’s core colour cosmetics range, and Nykaa has the platform advantage of first-party discovery data that no standalone brand can replicate.

Renee Cosmetics, founded in 2020, reached profitability faster than Sugar did and has been growing in tier-2 and tier-3 India. The very markets Sugar expanded into expensively and is now retreating from. Renee’s leaner cost structure is a direct rebuke to Sugar’s capital-intensive model.

Minimalist, which targets the skincare-science consumer with transparent ingredient formulations at accessible prices, represents the secular shift within the beauty category, from colour cosmetics toward skincare. Sugar’s strength is in colour; its skincare range has not gained the same traction. As the category mix shifts, Sugar’s core strength becomes relatively less valuable.

WHAT THE COMPANY SAYS VS WHAT THE NUMBERS SAY

In January 2024, Vineeta Singh told an interviewer: “We are looking at about a two to three years’ timeline in terms of an IPO because it is important to have some solid track record of profitability in the bank before taking the company public. We had an aspiration that we should go into the market at a ₹1,000-crore plus revenue, plus profitability.”

By FY25, revenue had declined to ₹411.7 crore, 59% below the ₹1,000 crore target, and losses had nearly doubled to ₹134.3 crore. The IPO has since been pushed back by at least 2 more years, according to Wikipedia’s contemporaneously updated entry on Singh.

In a 2023 interview with FashionNetwork, Singh said: “Over the last year, we have improved our profitability by 15%, and we see this trend continuing to help the company become profitable in the upcoming fiscal year.” The “upcoming fiscal year” she was referring to was FY24. FY24 did see losses narrow, to ₹67.6 crore from ₹76.2 crore, so the improvement was real at the time. But it reversed catastrophically in FY25, suggesting the cost structure was never fundamentally reformed. The profitability improvement was cyclical, not structural.

When L Catterton led the Series D in 2022, Vineeta Singh said: “L Catterton’s brand-building and value-creation capabilities will fortify our growth as we continue on our journey of delighting and over-delivering on the expectations of our customers and fans.”

Three years later, L Catterton’s investment, made at ₹3,000 crore, is worth approximately half that in the rescue round valuation. The journey of “over-delivering” has, by the arithmetic of VC returns, under-delivered materially.

None of this makes Vineeta Singh a dishonest person. Startup founders are, by professional necessity, optimists. The problem is when optimism becomes a substitute for structural reform, and when timelines for profitability are moved forward and backward without the fundamental economics ever changing.

THE BULL CASE

It would be intellectually lazy to conclude this only as a story of failure. There is a genuine bull case for Sugar Cosmetics, and it deserves honest engagement.

The restructuring is real and materially significant. Closing underperforming stores and terminating expensive distributor contracts generated a ₹95 crore improvement. If the cost structure can be sustainably reduced to match a ₹380-400 crore revenue base, EBITDA breakeven is mathematically achievable. A company earning ₹400 crore at 20% gross margins with a leaner cost base could, in theory, generate ₹10-15 crore in operating profit — not spectacular, but the beginning of a flywheel.

The brand equity is genuine and durable at the core product level. Sugar’s matte colour cosmetics have a loyal customer base that repurchases without heavy inducement. If the company focuses its limited capital on deepening penetration in proven markets rather than expanding into new ones, the unit economics could improve significantly.

Vineeta Singh’s personal brand remains one of the most powerful assets in Indian D2C — her Shark Tank visibility, her marathon-running public persona, and her frank communication style generate organic brand attention that most beauty companies would spend crores trying to buy. If the company can survive the cash crunch, that equity does not disappear.

The ₹100-150 crore rescue round, if it closes, provides approximately 18-24 months of operational runway at the restructured cost base — enough time to test whether the leaner model can reach breakeven. L Catterton, with its LVMH relationships and global beauty brand playbook, has every incentive to protect its investment and facilitate a recovery. The bull case is narrow but it is not zero.

THE QUESTIONS THAT DEMAND ANSWERS

These are the questions that every prospective investor, every employee considering joining, and every consumer who cares about the brands they support deserves answered, with specificity, not in a podcast interview:

One: The company settled employee salaries from promoter personal accounts, per Mint’s reporting. Is this a one-time bridge or an ongoing arrangement? What is the current cash position of Sugar Brands Private Limited, and how many months of operational runway does it have at the current burn rate?

Two: The rescue round is being targeted at family offices and HNIs rather than institutional investors. This implies that institutional investors — including existing backers — have declined to lead. Which existing institutional investors have been approached and declined to participate in the current round, and what specific concerns did they cite?

Three: The company generated ₹95 crore in savings from store closures and distributor rationalisations. These are one-time actions. What is the recurring annual EBITDA improvement from these changes, and what does the path to operating breakeven look like, specifically, at what revenue level and with what cost structure?

Four: Sugar Cosmetics has never held a patent on any product formulation and manufactures entirely through contract manufacturers under non-exclusive arrangements. If the rescue round closes and the company survives, what is the plan to build any form of defensible intellectual property or proprietary manufacturing capability that would justify a future IPO valuation premium?

Five: The rescue round is being discussed at ₹1,400-1,500 crore — half the 2022 peak. L Catterton invested at ₹3,000 crore. What are the liquidation preference terms in the existing shareholder agreements, and in a downside scenario — a distressed sale or wind-down — how much, if anything, would common shareholders and employees with ESOPs receive?

Six: Vineeta Singh has been the dominant public face and marketing asset of this brand. What succession or de-risking plan exists for the brand’s identity in the event that she reduces her public profile, exits an executive role, or the company is acquired by an entity for whom her personal brand is not part of the strategic rationale?

Seven: Revenue in FY26 has declined further to approximately ₹380 crore — below FY23 levels. At what revenue or loss threshold does the board consider a strategic sale, merger, or shutdown of the business to be preferable to continued independent operation? Has this threshold been defined, and if so, what is it?

Sugar Cosmetics is not a fraud. It is a genuine brand, built by a genuinely talented founder, in a genuinely large market. Vineeta Singh turned down a ₹1 crore annual salary offer from a private equity firm at the age of 23 to build this company — and she has built something that millions of Indian women recognise and trust. That is not nothing.

But trust, as a business asset, has a balance sheet. And on Sugar Cosmetics’ balance sheet, ₹375 crore in cumulative losses, promoters paying salaries from personal funds, and a rescue round at half the peak valuation are entries that cannot be explained away by market conditions or bad timing alone. They are evidence that the business model, as currently constructed, does not generate enough value to cover its own costs.

The Indian beauty market will reach $40 billion by 2030 with or without Sugar Cosmetics. The question that the next ₹100-150 crore will answer is whether this brand gets to be part of that story — or whether it becomes a cautionary footnote in the longer history of the D2C boom that was funded by cheap capital, built on expensive optimism, and priced, in the end, by the cold arithmetic of cash flows.